16) When computing the present value of a bond, which interest rate is used? Why?

17) When computing a bond’s cash flow for interest, which interest rate is used? Why?

1) The effective-interest amortization method allocates an amount of bond discount or premium, based

on the stated rate of interest, to each interest period over the life of the bond.

2) The effective-interest amortization method allocates an amount of bond discount or premium, based

on the market interest rate at issuance, to each interest period over the life of the bond.

3) Generally accepted accounting principles require that interest expense be measured using the straight–

line amortization method.

4) Generally accepted accounting principles require that interest expense be measured using the effective–

interest amortization method, unless the straight-line amounts are similar.

5) When using the effective-interest amortization method, the discount amortization is the excess of the

calculated interest expense based on the effective interest rate over the interest payment.

6) When using the effective-interest amortization method, the discount amortization is the excess of the

calculated interest expense based on the stated interest rate over the interest payment.

7) When using the effective-interest amortization method, the amount of the interest expense is calculated

using the carrying value of the bonds and the market interest rate.

8) When using the effective-interest amortization method, the amount of the interest expense is calculated

using the face value of the bonds and the market interest rate.

9) When using the effective-interest amortization method, the amount of the interest expense is calculated

using the face value of the bonds and the stated interest rate.

10) When using the effective-interest amortization method, the amount of the interest payment is

calculated using the face value of the bonds and the stated interest rate.

11) On January 1, 2019, French Company issued $74,000 of five-year, 8% bonds when the market interest

rate was 12%. The issue price of the bonds was $62,000. French uses the effective-interest method of

amortization for bond discount. Semiannual interest payments are made on June 30 and December 31 of

each year. How much interest expense will be recorded when the first interest payment is made? (Round

your answer to the nearest dollar number.)

A) $2480

B) $3720

C) $2960

D) $4440

12) On January 1, 2019, Agree Company issued $85,000 of five-year, 8% bonds when the market interest

rate was 12%. The issue price of the bonds was $62,401. Agree uses the effective-interest method of

amortization for bond discount. Semiannual interest payments are made on June 30 and December 31 of

each year. Which of the following is the correct journal entry to record the first interest payment? (Round

all amounts to the nearest whole dollar.)

A)

Interest Expense

5100

Cash

5100

B)

Interest Expense

3744

Discount on Bonds Payable

344

Cash

3400

C)

Interest Expense

3400

Discount on Bonds Payable

1700

Cash

5100

D)

Interest Expense

5100

Discount on Bonds Payable

3400

Cash

1700

13) On January 1, 2019, Parker Advertising Company issued $50,000 of six-year, 3% bonds when the

market interest rate was 4%. The bonds were issued for $47,356. Parker uses the effective-interest method

of amortization for bond discount. Semiannual interest payments are made on June 30 and December 31

of each year. Prepare the amortization table for the first four interest payments. (Round your answers to

the nearest dollar number.)

Date

Cash Paid

Interest

Expense

Discount

Amortized

Carrying

Amount

1/1/19

6/30/19

12/31/19

6/30/20

12/31/20

Date

Cash Paid

Interest

Expense

Discount

Amortized

Carrying

Amount

1/1/19

$47,356

6/30/19

$750

$947

$197

47,553

12/31/19

750

951

201

47,754

6/30/20

750

955

205

47,959

12/31/20

750

959

209

48,168

Explanation:

Cash paid each interest payment date = $50,000 × 3% × 6/12 = $750

First interest expense = $47,356 × 4% × 6/12 = $947

Diff: 3

LO: 12-8

AACSB: Application of knowledge

AICPA Functional: Measurement

PE Question Type: Application

H2: Effective-Interest Amortization for a Bond Discount

14) When a bond is issued at a premium, the interest expense calculation using the effective-interest

amortization method uses the carrying amount of the bonds and the market rate of interest.

15) Using the effective-interest amortization method, the calculation for the amount of premium

amortization is the difference between the cash paid for interest and the calculated interest expense based

on the effective interest rate.

16) Using the effective-interest amortization method, the amount of premium amortization remains the

same over the life of the bond.

17) On January 1, 2018, Ling Services issued $168,000 of six-year, 12% bonds when the market interest

rate was 11%. The issue price of the bonds was $177,110. Ling uses the effective-interest method to

amortize the bond premium. Semiannual interest payments are made on June 30 and December 31 of

each year. How much interest expense will be recorded when the first interest payment is made? (Round

the final answer to the nearest dollar.)

A) $10,627

B) $9741

C) $10,080

D) $9240

18) On January 1, 2019, Castle Services issued $169,000 of six–year, 12% bonds when the market interest

rate was 11%. The bonds were issued for $172,000. Castle uses the effective-interest method to amortize

the bond premium. Semiannual interest payments are made on June 30 and December 31 of each year.

Which of the following is the correct journal entry to record the first interest payment? (Round your

answers to the nearest dollar number.)

A)

Interest Expense

9295

Cash

9295

B)

Interest Expense

9295

Discount on Bonds Payable

845

Cash

10,140

C)

Interest Expense

9460

Premium on Bonds Payable

680

Cash

10,140

D)

Cash

10,140

Premium on Bonds Payable

845

Interest Expense

9295

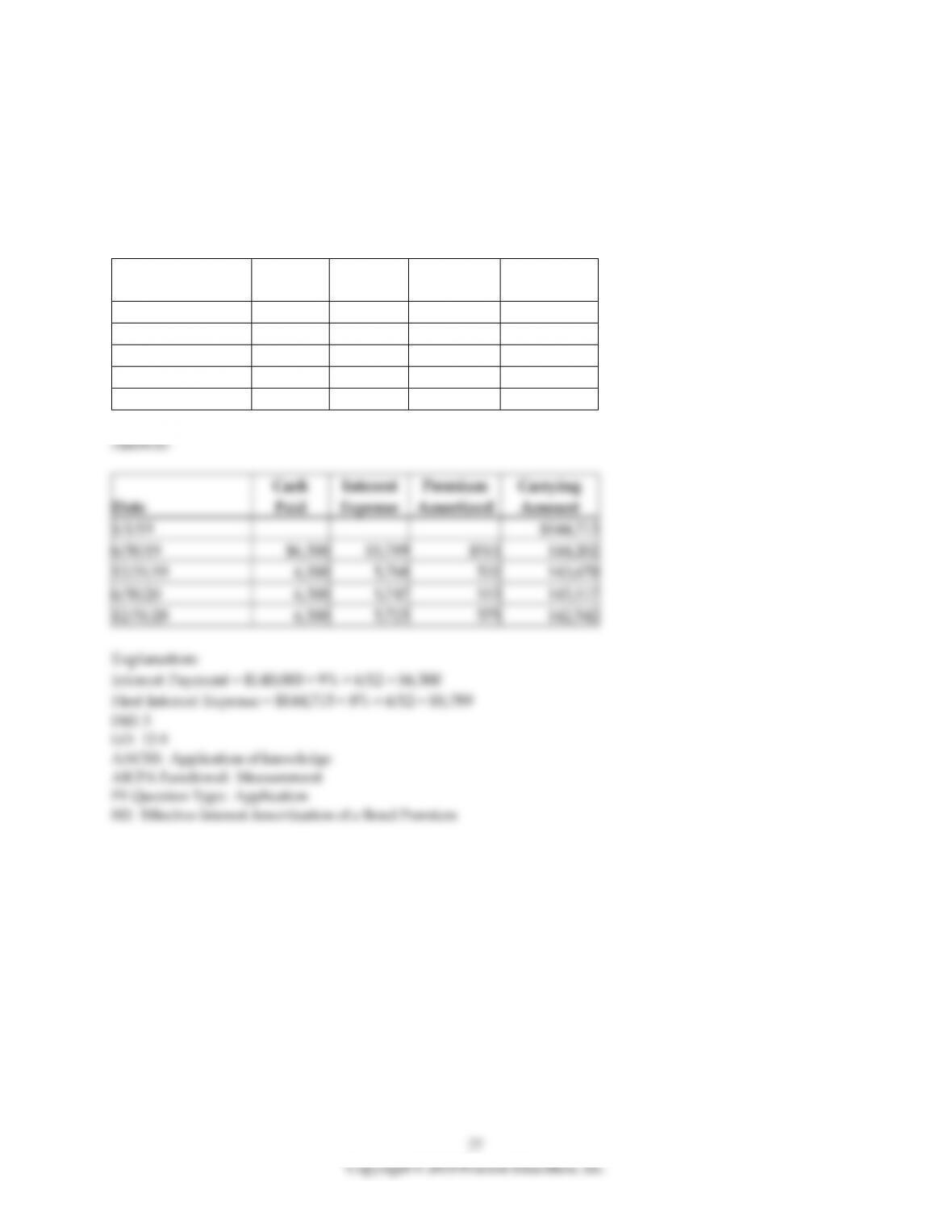

19) On January 1, 2019, Eastern Services issued $140,000 of four-year, 9% bonds when the market rate was

8%. The bonds were issued at $144,713. Eastern uses the effective-interest method to amortize the bond

premium. Semiannual interest payments are made on June 30 and December 31 of each year. Prepare the

amortization table for the first four interest payments. (Round your answers to the nearest dollar

number.)

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount

1/1/19

6/30/19

12/31/19

6/30/20

12/31/20

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount

1/1/19

$144,713

6/30/19

$6,300

$5,789

$511

144,202

12/31/19

6,300

5,768

532

143,670

6/30/20

6,300

5,747

553

143,117

12/31/28

6,300

5,725

575

142,542

Explanation:

Interest Payment = $140,000 × 9% × 6/12 = $6,300

First Interest Expense = $144,713 × 8% × 6/12 = $5,789

Diff: 3

LO: 12-8

AACSB: Application of knowledge

AICPA Functional: Measurement

PE Question Type: Application

H2: Effective-Interest Amortization of a Bond Premium