Principles of Managerial Finance, Brief Ed., 8e (Zutter/Smart)

Chapter 10 Capital Budgeting Techniques

10.1 Overview of capital budgeting

1) Capital budgeting techniques are used to evaluate a firm’s fixed asset investments which

provide the basis for the firm’s earning power and value.

2) The purchase of additional physical facilities, such as additional property or a new factory, is

an example of a capital expenditure.

3) Capital budgeting is the process of evaluating and selecting short-term investments that are

consistent with the firm’s goal of maximizing owners’ wealth.

4) A capital expenditure is an outlay of funds invested only in fixed assets that is expected to

produce benefits over a period of time less than one year.

5) An outlay for advertising and management consulting is considered to be a fixed asset

expenditure.

6) Capital expenditure proposals are reviewed to assess their appropriateness in light of a firm’s

overall objectives and plans, and to evaluate their economic validity.

7) The basic motives for capital expenditures are to expand operations, to replace or renew fixed

assets, or to obtain some other, less tangible benefit over a long period.

8) The primary motive for capital expenditures is to refurbish fixed assets.

9) Research and development is considered to be a motive for making capital expenditures.

10) The capital budgeting process consists of five distinct but interrelated steps: proposal

generation, review and analysis, decision making, implementation, and follow-up.

11) The capital budgeting process consists of four distinct but interrelated steps: proposal

generation, review and analysis, decision making, and termination.

12) Independent projects are projects that compete with one another for a firm’s resources, so that

the acceptance of one eliminates the others from further consideration.

13) If a firm has unlimited funds to invest in capital assets, all independent projects that meet its

minimum investment criteria should be implemented.

14) In capital budgeting, the preferred approaches in assessing whether a project is acceptable

are those that integrate time value procedures, risk and return considerations, and valuation

concepts.

15) A $60,000 outlay for a new machine with a usable life of 15 years is an operating

expenditure that would appear as a current asset on a firm’s balance sheet.

16) A nonconventional cash flow pattern associated with capital investment projects consists of

an initial outflow followed by a series of inflows.

17) Time value of money should be ignored in capital budgeting techniques to make accurate

decisions.

18) If a firm has limited funds to invest, all the mutually exclusive projects that meet its

minimum investment criteria should be implemented.

19) Mutually exclusive projects are projects whose cash flows are unrelated to one another; the

acceptance of one does not eliminate the others from further consideration.

20) The availability of funds for capital expenditures does not affect a firm’s capital budgeting

decisions.

21) Independent projects are those whose cash flows are unrelated to one another; the acceptance

of one does not eliminate the others from further consideration.

22) Mutually exclusive projects are those whose cash flows are constant over a specified period

of time and more than one project needs to be accepted in order to implement capital budgeting

decisions.

23) Independent projects are those whose cash flows compete with one another and therefore

more than one project needs to be accepted in order to implement the capital budgeting decision.

24) Mutually exclusive projects are those whose cash flows compete with one another; the

acceptance of one eliminates the others from further consideration.

25) If a firm is subject to capital rationing, it is able to accept all independent projects that

provide an acceptable return.

26) If a firm has unlimited funds, it is able to accept all independent projects that provide an

acceptable return.

27) If a firm is subject to capital rationing, it has only a fixed number of dollars available for

capital expenditures and numerous projects compete for these dollars.

28) The ranking approach involves the ranking of capital expenditure projects on the basis of

some predetermined measure such as the rate of return.

29) The accept-reject approach involves the ranking of capital expenditure projects on the basis

of some predetermined measure, such as the rate of return.

30) A conventional cash flow pattern is one in which an initial outflow is followed only by a

series of inflows.

31) Large firms evaluate the merits of individual capital budgeting projects to ensure that the

selected projects have the best chance of increasing the firm value.

32) A nonconventional cash flow pattern is one in which an initial inflow is followed by a series

of inflows and outflows.

33) ________ is the process of evaluating and selecting long-term investments that are consistent

with a firm’s goal of maximizing owners’ wealth.

A) Recapitalizing assets

B) Capital budgeting

C) Ratio analysis

D) Securitization

34) A $60,000 outlay for a new machine with a usable life of 15 years is called ________.

A) capital expenditure

B) financing expenditure

C) replacement expenditure

D) operating expenditure

35) Fixed assets that provide the basis for a firm’s earning and value are often called ________.

A) tangible assets

B) noncurrent assets

C) earning assets

D) book assets

36) Which of the following is TRUE of a capital expenditure?

A) It is an outlay made to replace current assets.

B) It is an outlay expected to produce benefits within one year.

C) It is commonly used for current asset expansion.

D) It is commonly used to expand the level of operations.

37) The final step in the capital budgeting process is ________.

A) implementation

B) follow-up

C) review and analysis

D) decision making

38) The first step in the capital budgeting process is ________.

A) review and analysis

B) implementation

C) decision making

D) proposal generation

39) ________ projects do not compete with each other; the acceptance of one ________ the

others from consideration.

A) Capital; eliminates

B) Independent; does not eliminate

C) Mutually exclusive; eliminates

D) Replacement; eliminates

40) ________ projects have the same function; the acceptance of one ________ the others from

consideration.

A) Capital; eliminates

B) Independent; does not eliminate

C) Mutually exclusive; eliminates

D) Replacement; eliminates

41) A firm with limited dollars available for capital expenditures is subject to ________.

A) capital dependency

B) capital gains

C) working capital constraints

D) capital rationing

42) Projects that compete with one another, so that the acceptance of one eliminates the others

from further consideration are called ________.

A) independent projects

B) mutually exclusive projects

C) replacement projects

D) capital projects

43) A conventional cash flow pattern associated with capital investment projects consists of an

initial ________.

A) outflow followed by a broken cash series

B) inflow followed by a broken series of outlay

C) outflow followed by a series of inflows

D) outflow followed by a series of outflows

44) A nonconventional cash flow pattern associated with capital investment projects consists of

an initial ________.

A) outflow followed by a series of both cash inflows and outflows

B) inflow followed by a series of both cash inflows and outflows

C) outflow followed by a series of inflows

D) inflow followed by a series of outflows

45) Which of the following is an example of a nonconventional pattern of cash flows?

A)

Year

0

1

2

3

4

cash flow

-200

150

310

265

200

B)

Year

0

1

2

3

4

cash flow

200

100

-100

200

-300

C)

Year

0

1

2

3

4

cash flow

-200

100

100

200

300

D)

Year

0

1

2

3

4

cash flow

-200

150

150

150

150

1) In the case of annuity cash inflows, the payback period can be found by dividing the initial

investment by the annual cash inflow.

2) The payback period is the amount of time required for a firm to dispose a replaced asset.

3) For calculating payback period for an annuity, all cash flows must be adjusted for time value

of money.

4) If a project’s payback period is less than the maximum acceptable payback period, we would

accept it.

5) If a project’s payback period is greater than the maximum acceptable payback period, we

would reject it.

6) If a project’s payback period is greater than the maximum acceptable payback period, we

would accept it.

7) The payback period of a project that costs $1,000 initially and promises after-tax cash inflows

of $300 for the next three years is 3.33 years.

8) The payback period of a project that costs $1,000 initially and promises after-tax cash inflows

of $300 each year for the next three years is 0.333 years.

9) The payback period of a project that costs $1,000 initially and promises after-tax cash inflows

of $3,000 each year for the next three years is 0.333 years.

10) The payback period of a project that costs $1,000 initially and promises after-tax cash

inflows of $2,000 each year for the next three years is 0.5 years.

11) The payback period is generally viewed as a flawed capital budgeting technique, because it

does not explicitly consider the time value of money by discounting cash flows to find present

value.

12) A project must be rejected if its payback period is less than the maximum acceptable

payback period.

13) By measuring how quickly a firm recovers its initial investment, the payback period gives

implicit consideration to the time value of money and ignores the timing of cash flows.

14) One strength of payback period is that it fully accounts for the time value of money.

15) One weakness of the payback period approach is its failure to recognize cash flows that

occur after the payback period.

16) Since the payback period can be viewed as a measure of risk exposure, many firms use it as a

supplement to other decision techniques.

17) A major weakness of payback period in evaluating projects is that it cannot specify the

appropriate payback period in light of the wealth maximization goal.

18) Which of the following is the capital budgeting technique that has the weakest connection to

the goal of value maximization?

A) internal rate of return

B) payback period

C) profitability index

D) net present value

19) Which of the following capital budgeting techniques ignores the time value of money?

A) payback period approach

B) net present value

C) internal rate of return

D) profitability index

20) The ________ measures the amount of time it takes a firm to recover its initial investment.

A) profitability index

B) internal rate of return

C) net present value

D) payback period

16

21) An annuity is ________.

A) a mix of cash flows in conventional and nonconventional

B) a stream of perpetual cash flows

C) a series of constantly growing cash flows

D) a series of equal annual cash flows

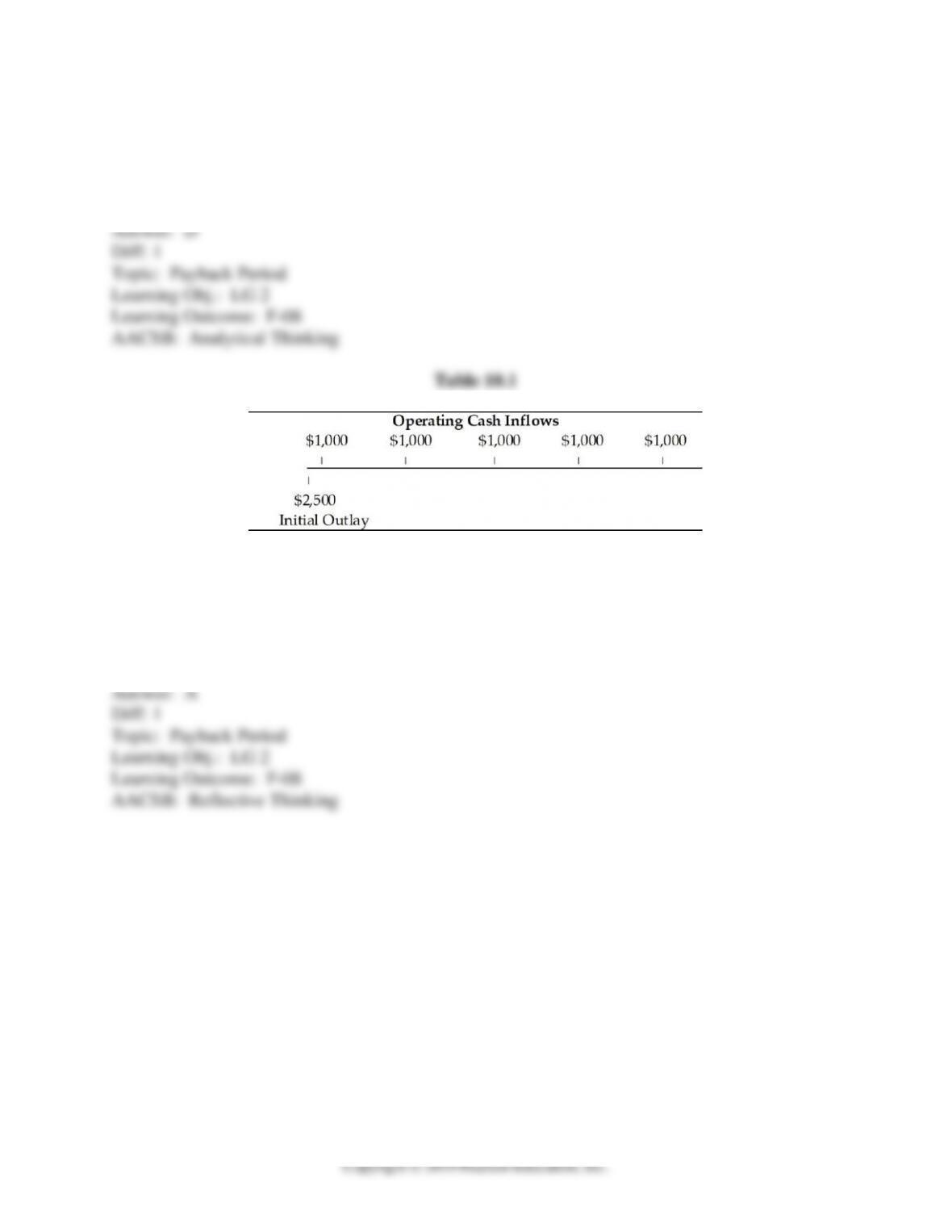

22) The cash flow pattern depicted is associated with a capital investment and may be

characterized as ________. (See Table 10.1)

A) an annuity and a conventional cash flow

B) a mixed stream and a nonconventional cash flow

C) an annuity and a nonconventional cash flow

D) a mixed stream and a conventional cash flow

17

Copyright © 2019 Pearson Education, Inc.

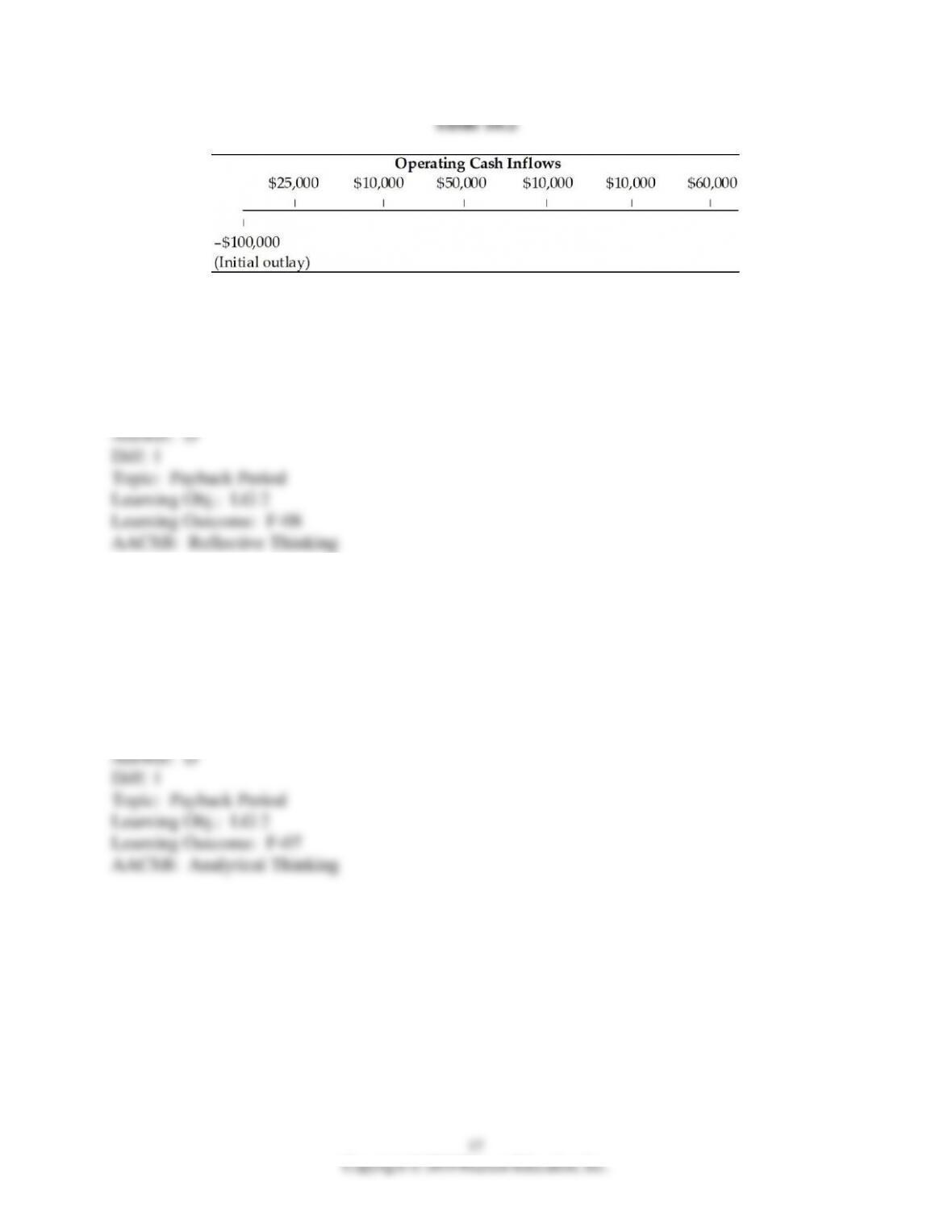

Table 10.2

23) The cash flow pattern depicted is associated with a capital investment and may be

characterized as ________. (See Table 10.2)

A) an annuity and a conventional cash flow

B) a mixed stream and a nonconventional cash flow

C) an annuity and a nonconventional cash flow

D) a mixed stream and a conventional cash flow

24) Payback is considered a flawed capital budgeting because it ________.

A) gives explicit consideration to the timing of cash flows and therefore the time value of

money.

B) gives explicit consideration to risk exposure due to the use of the cost of capital as a discount

rate.

C) does not gives explicit consideration on the recovery of initial investment and possibility of a

calamity.

D) it does not explicitly consider the time value of money.

25) A firm is evaluating a proposal which has an initial investment of $35,000 and has cash

flows of $10,000 in year 1, $20,000 in year 2, and $10,000 in year 3. The payback period of the

project is ________.

A) 1 year

B) 2 years

C) between 1 and 2 years

D) between 2 and 3 years

26) A firm is evaluating a proposal which has an initial investment of $50,000 and has cash

flows of $15,000 per year for five years. The payback period of the project is ________.

A) 1.5 years

B) 2 years

C) 3.3 years

D) 4 years

27) Which of the following statements is TRUE of payback period?

A) If the payback period is less than the maximum acceptable payback period, management

should be indifferent.

B) If the payback period is greater than the maximum acceptable payback period, accept the

project.

C) If the payback period is less than the maximum acceptable payback period, accept the project.

D) If the payback period is greater than the maximum acceptable payback period, management

should be indifferent.

28) What is the payback period for Tangshan Mining company’s new project if its initial after-tax

cost is $5,000,000 and it is expected to provide after-tax operating cash inflows of $1,800,000 in

year 1, $1,900,000 in year 2, $700,000 in year 3, and $1,800,000 in year 4?

A) 4.33 years

B) 3.33 years

C) 2.33 years

D) 1.33 years

29) Should Tangshan Mining company accept a new project if the company’s maximum payback

is 3.5 years and the project’s initial after-tax cost is $5,000,000 followed by after-tax operating

cash inflows of $1,800,000 in year 1, $1,900,000 in year 2, $700,000 in year 3, and $1,800,000

in year 4?

A) Yes, since the payback period of the project is less than the maximum acceptable payback

period.

B) No, since the payback period of the project is more than the maximum acceptable payback

period.

C) Yes, since the risk exposure of the project is less than the maximum acceptable risk exposure.

D) No, since the risk exposure of the project is more than the maximum acceptable risk

exposure.

30) Should Tangshan Mining company accept a new project if its maximum payback is 3.25

years and its initial after-tax cost is $5,000,000 followed by after-tax operating cash inflows of

$1,800,000 in year 1, $1,900,000 in year 2, $700,000 in year 3, and $1,800,000 in year 4?

A) Yes, since the payback period of the project is less than the maximum acceptable payback

period.

B) No, since the payback period of the project is more than the maximum acceptable payback

period.

C) Yes, since the risk exposure of the project is less than the maximum acceptable risk exposure.

D) No, since the risk exposure of the project is more than the maximum acceptable risk

exposure.

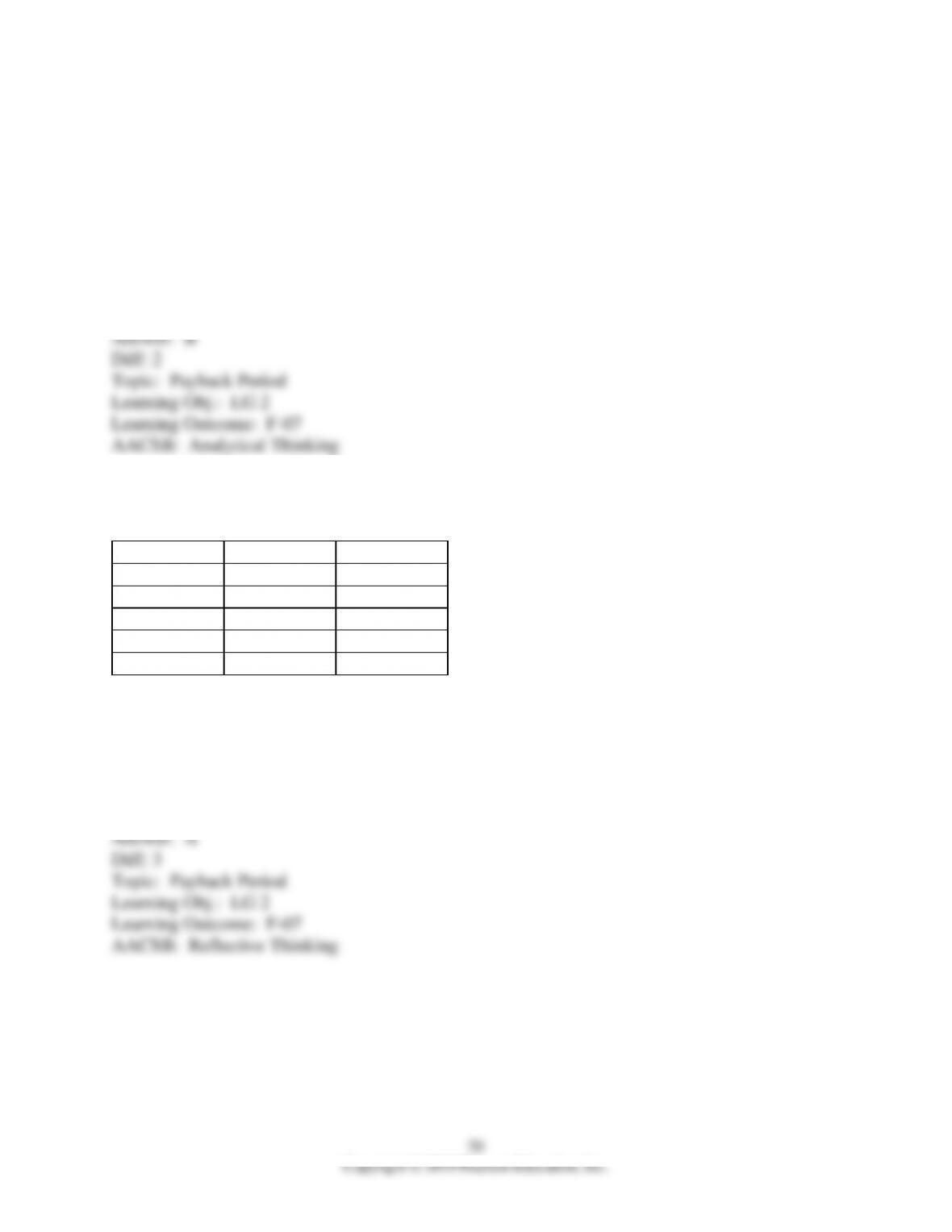

31) Evaluate the following projects using the payback method assuming a rule of 3 years for

payback.

Year

Project A

Project B

0

-10,000

-10,000

1

4,000

4,000

2

4,000

3,000

3

4,000

2,000

4

0

1,000,000

A) Project A can be accepted because the payback period is 2.5 years but Project B cannot be

accepted because its payback period is longer than 3 years.

B) Project B should be accepted because even though the payback period is 2.5 years for Project

A and 3.001 for project B, there is a $1,000,000 payoff in the 4th year in Project B.

C) Project B should be accepted because you get more money paid back in the long run.

D) Both projects can be accepted because the payback is less than 3 years.