30

11) If the amount harvested in a timber operation was different every year for four years, you

would:

A) recompute the depletion expense rate per unit each year.

B) use the same depletion expense rate per unit each year.

C) debit Depletion Expense for the same amount each year.

D) credit Accumulated Depletion–timber for the same amount each year.

Question Type: Concept

12) Subtracting accumulated depletion from the asset account coal mine would yield the:

A) current market value of the coal mine.

B) original cost of the coal mine.

C) net book value of the coal mine.

D) current period’s depletion expense for the coal mine.

Question Type: Concept

13) Information needed to compute a depletion charge per unit includes the:

A) estimated total amount of resources available for removal.

B) amount of resources removed during the period.

C) cumulative amount of resources removed.

D) amount of resources sold during the period.

Question Type: Concept

14) Properties whose physical substance consists of natural resources that are consumed in the

operation of a business are called:

A) depreciable assets.

B) depletable assets.

C) amortizable assets.

D) intangible assets.

Question Type: Concept

15) When calculating depletion, what is the proper treatment of residual value?

A) There is no residual value in the calculation of depletion expense.

B) The residual value is subtracted from cost to determine the depletable base.

C) The residual value is added to cost to determine the depletable base.

D) Residual value is ignored until the end of the asset‘s life at which time it is used to limit the

final year’s expense amount.

Question Type: Concept

31

16) Which of the following is NOT true regarding depletion?

A) Depletion is the systematic reduction of a natural resource’s carrying value on the books.

B) Depletion is computed in a similar manner to straight-line depreciation.

C) Depletion is an expense that applies to the natural resources in the same way depreciation

applies to fixed assets.

D) Depletion is an expense that applies to natural resources in the same way amortization applies

to intangible assets.

Question Type: Concept

8.8 Account for other assets

1) Equity securities which management intends to hold for less than one year would be

considered other long-term assets.

Question Type: Concept

2) Investments in debt securities, may be classified as either current or long-term assets based on

their maturity date.

3) Increases in the value of a security while the company still owns it are considered realized

gains.

Question Type: Concept

4) Realized gains and losses only occur when the security is sold for more or less than the

original cost.

Question Type: Concept

5) Trading securities are shown as long-term assets on the Balance Sheet.

Question Type: Concept

6) Available-for-sale securities are reported at their current market value, and any increases or

decreases in market value are reported as part of net income.

Question Type: Application

32

7) Which of the following is NOT a classification for marketable securities?

A) Saleable securities

B) Available-for-sale securities

C) Trading securities

D) Held-to-maturity securities

Question Type: Concept

8) Which of the following marketable securities are reported at market value on the Balance

Sheet date?

A) Held-to-maturities securities

B) Available-for-sale securities

C) Trading securities

D) Available-for-sale and trading securities

Question Type: Concept

9) Which of the following marketable securities are reported at cost on the Balance Sheet date?

A) Trading securities

B) Available-for sale securities

C) Held-to-maturity securities

D) Trading and held-to-maturity securities

Question Type: Concept

10) For which kind of marketable securities are any unrealized gains and losses shown on the

income

statement?

A) Trading securities

B) Available-for sale securities

C) Held-to-maturity securities

D) Trading and held-to-maturity securities

Question Type: Concept

33

11) For which of the following securities are any increases or decreases in value reported as a

separate change in Stockholders’ Equity for the period?

A) Trading securities

B) Available-for sale securities

C) Held-to-maturity securities

D) Trading and held-to-maturity securities

Question Type: Concept

12) Interest and dividends earned during the period are reported on the Income Statement for

which kind of marketable securities?

A) Trading securities

B) Available-for-sale securities

C) Held-to-maturity securities

D) All types of securities show interest and dividend income on the Income Statement.

Question Type: Concept

13) Securities that are actively managed in order to maximize profit as a result of short-term

changes in price are:

A) trading securities.

B) available-for sale securities.

C) held-to–maturity securities.

D) trading and held-to-maturity securities.

Question Type: Concept

14) Shakes, Inc. purchased 200 shares of Netflix stock, which it plans to sell as soon as the

market price increases by 10%. This stock will be classified as:

A) available-for-sale securities.

B) trading securities.

C) held-to–maturity securities.

D) profit-prone securities.

Question Type: Application

34

15) Woods Corporation purchased $15,000 in bonds which it plans on owning until they’re

repaid. Woods does not anticipate that it will need to sell the bonds to generate cash. The bonds

will be classified as:

A) trading securities.

B) held-to–maturity or available-for-sale.

C) held-to–maturity securities.

D) available-for-sale securities.

Question Type: Application

16) Sienna Co. purchased 1,000 shares of Microsoft stock. Management is not actively managing

this stock , and only plans to sell it if there is a need to generate cash. This stock would be

classified as:

A) trading securities.

B) held-to–maturity securities.

C) trading securities or available-for-sale.

D) available-for-sale securities.

Question Type: Application

8.9 Report long-term assets on the balance sheet

1) Long-term assets usually begin with the listing of natural resources first.

Question Type: Concept

2) GAAP does not allow property, plant, and equipment to be shown at net book value on the

Balance Sheet.

Question Type: Concept

equipment, as well as after natural resources, on a company‘s long-term assets portion of the

Balance Sheet.

Question Type: Concept

4) Long-term marketable securities, such as five–year held-to–maturity securities, would be listed

last in the long-term assets portion of a company’s Balance Sheet.

Question Type: Concept

35

5) The footnotes to the financial statements will include a description of the intangible asset and

its estimated useful life.

Question Type: Concept

6) TNT Co. has the following assets:

I) Timber reserves $400,000, with accumulated depletion of $220,000.

II) Property, Plant and Equipment $600,000 with accumulated depreciation $275,000.

III) Other long-term assets $125,000.

IV) Goodwill $75,000

In what order should these be presented on the Balance Sheet?

A) I, II, IV, III

B) III, II, I, IV

C) II, I, IV, III

D) IV, II, III, I

Question Type: Application

8.10 Calculate the return on assets and the fixed asset turnover

1) The return on assets (ROA) is the ratio of net income divided by average fixed assets.

Question Type: Concept

2) The fixed asset turnover is the ratio of sales to average fixed assets.

Question Type: Concept

3) The return on assets and the fixed asset turnover are usually computed monthly.

Question Type: Concept

4) Charmed Inc. has net income of $50,000, sales of $250,000, beginning total assets of

$150,000 and ending total assets of $200,000. The return on assets is (rounded) 33%.

Question Type: Application

36

5) Charbucks has net income of $50,000, sales of $250,000, beginning fixed assets of $150,000

and ending fixed assets of $200,000. The fixed asset turnover is (rounded) 1.4.

Question Type: Application

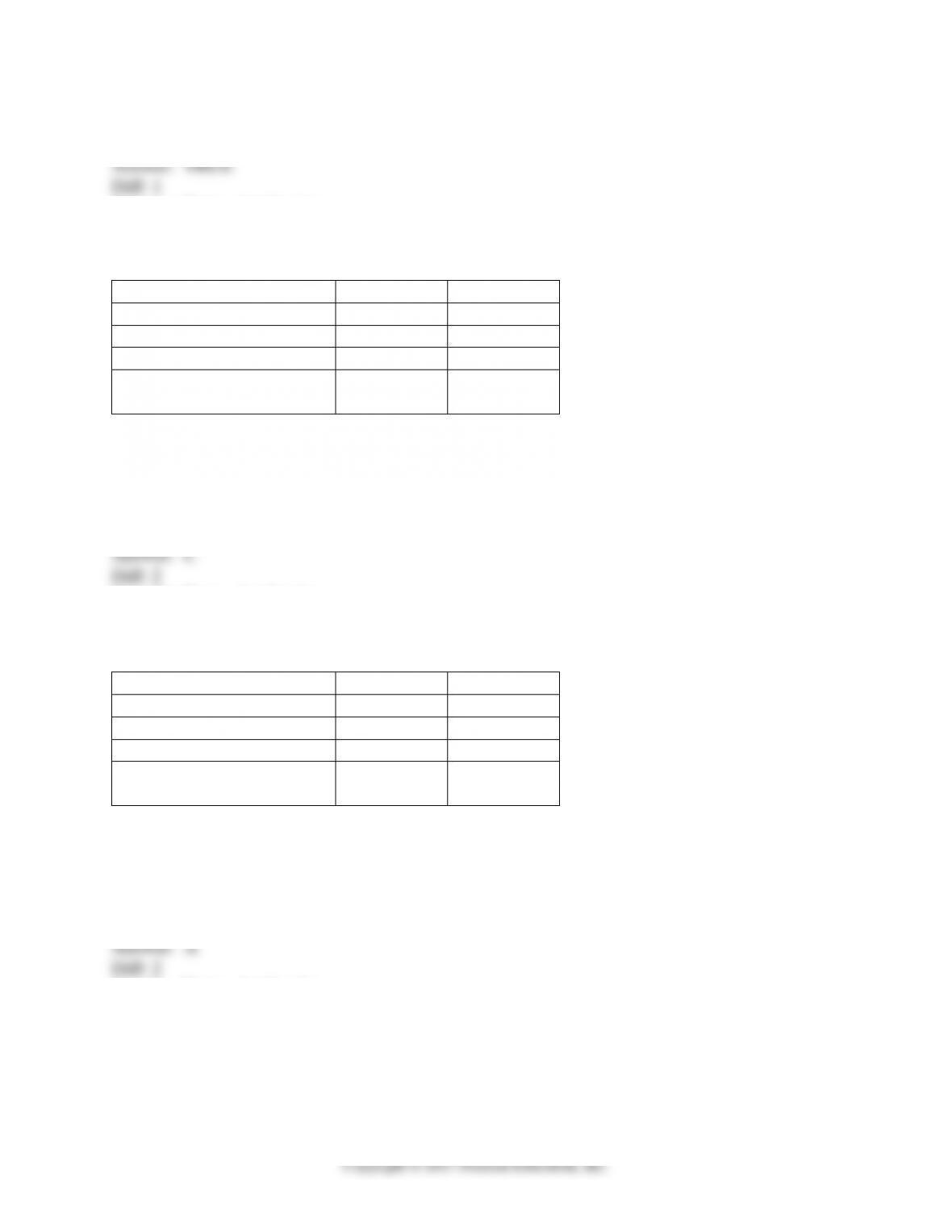

6) The following is selected data for Inland Industries:

2016

2015

Sales

$1,200,000

$1,300,000

Net Income

117,000

110,000

Total Current Assets

164,000

150,000

Property, Plant and

Equipment

646,000

638,000

The return on assets for 2016 was: (Round your final answer two decimal places, X.XX%.)

A) 28.89%.

B) 18.34%.

C) 14.64%.

D) 18.11%.

Question Type: Application

7) The following is selected data for Northwest Industries:

2016

2015

Sales

$1,700,000

$1,743,000

Net Income

173,000

210,000

Total Current Assets

190,000

163,000

Property, Plant and

Equipment

724,000

650,000

The return on assets for 2016 was: (Round your final answer two decimal places, X.XX%.)

A) 20.03%.

B) 18.93%.

C) 23.9%.

D) 21.28%.

Question Type: Application

37

8) The following is selected data for Bach Co.:

2016

2015

Sales

$1,254,498

$1,132,604

Net Income

142,000

128,000

Total Current Assets

177,000

151,000

Property, Plant and

Equipment

563,000

542,000

The fixed asset turnover for 2016 was: (Round your final answer to two decimal places.)

A) 1.75

B) 0.20

C) 2.27

D) 0.26

Question Type: Application