1

Financial Accounting, 4e (Kemp)

Chapter 8 Long-Term and Other Assets

8.1 Describe the differences between fixed assets, intangible assets, and natural resources

1) Timber, coal, and other minerals are long-term assets called natural resources.

Question Type: Concept

2) The cost of long-term assets must be allocated to an expense as the asset is used up.

Question Type: Application

3) An example of an other asset would be a trademark.

Question Type: Concept

A) amortized.

B) depleted.

C) depreciated.

D) expensed.

Question Type: Concept

5) Equipment, buildings, and vehicles are:

A) amortized.

B) depleted.

C) depreciated.

D) expensed.

Question Type: Concept

6) Minerals, timer and coal are:

A) amortized.

B) depleted.

C) depreciated.

D) expensed.

Question Type: Concept

2

7) Assets that CANNOT be seen, touched, or held are called:

A) intangible assets.

B) natural resources.

C) plant assets.

D) tangible assets.

Question Type: Concept

8) Which of the following would NOT be considered an intangible asset?

A) Goodwill

B) Franchise

C) Land

Question Type: Concept

9) Which of the following would be considered a natural resource?

A) Corn

B) Livestock

C) Timber

D) Wheat

Question Type: Concept

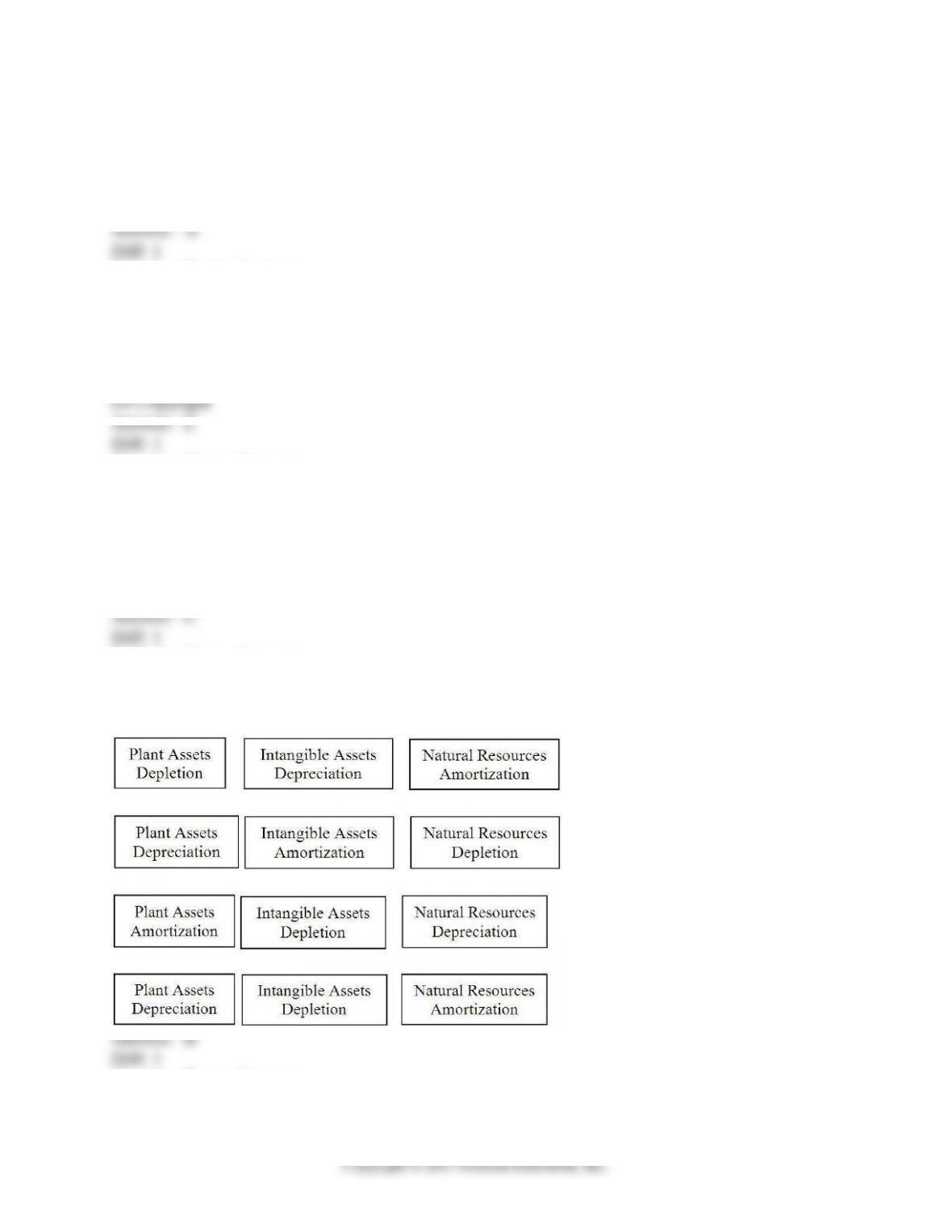

10) Which of the following matches the correct cost allocation terms with the given assets?

A)

B)

C)

D)

Question Type: Concept

3

11) Which of the following would be considered a fixed asset?

A) land

B) patents

C) timber

D) both A and C are fixed assets

Question Type: Concept

12) Which of the following would NOT be considered a fixed asset?

A) office equipment

B) company car

C) oil

D) office building

Question Type: Concept

13) McDonald‘s “golden arches” are an example of a(n) _______, which would be classified as

a(n) _______.

A) patent; intangible asset

B) trademark; plant asset

C) trademark; intangible asset

D) patent; plant asset

Question Type: Application

14) The cash registers at WalMart are an example of a(n) _______, which would be expensed

through _________.

A) fixed asset; depreciation

B) physical asset; depletion

C) plant asset; amortization

D) intangible asset; amortization

Question Type: Application

4

Copyright © 2017 Pearson Education, Inc.

8.2 Calculate and record the cost of acquiring fixed assets

1) When determining the cost of a plant asset, GAAP requires the use of the market value

principle.

Question Type: Concept

2) Neither land nor land improvements are depreciated.

Question Type: Concept

3) When a company pays a single price for a group of assets, the purchase is referred to as a

basket purchase.

Question Type: Concept

4) Whether a building is purchased or constructed, the same items are used to compute the price

of the building.

Question Type: Concept

5) Costs of testing machinery or equipment before they are used would be included in the price

of the machinery or the equipment.

Question Type: Concept

6) The cost of furniture and fixtures, such as file cabinets or shelving, includes its basic cost plus

all other costs to ready the asset for its intended use.

Question Type: Concept

7) When a company buys a building, realtor commissions are NOT included in the cost of the

building.

Question Type: Concept

5

8) The costs associated with clearing land and removing buildings are considered land

improvements.

Question Type: Concept

9) Costs that should be charged to the land account include:

A) the cost of removing unwanted buildings.

B) paving the parking lot.

C) installing fences.

D) the cost of a sign.

10) Which of the following would NOT be considered part of the cost of the land?

A) Survey and legal fees

B) Realtor commissions

C) Paving

D) Unpaid property taxes on the land

Question Type: Concept

11) Which of the following would be considered part of land improvements?

A) Removal of unwanted building on the land

B) Title transfer fees

C) Paving of the parking lot

D) Surveying fees

Question Type: Concept

12) Which of the following would NOT be a part of land improvements?

A) Paving of the parking lot

B) Installing fences around the property

C) Putting in sidewalks

D) Grading and leveling the land

Question Type: Concept

6

13) Which of the following would be included in the cost of a constructed building?

A) Purchase price of the building

B) Payments for material, labor, and overhead

C) Survey and legal fees

D) Realtor commissions

Question Type: Concept

14) Which of the following would NOT be considered as part of the cost of a constructed

building?

A) Building permit fees

B) Contractor charges

C) Realtor commissions

D) Architectural fees

Question Type: Concept

15) Which of the following would be considered as part of the cost of purchasing an existing

building?

A) Architectural fees

B) Contractor charges

C) Title transfer fees

D) Payment for materials

Question Type: Concept

16) Which of the following would NOT be considered part of the cost of machinery and

equipment?

A) Repairs and maintenance after start-up

B) Delivery charges

C) Installation costs

D) In-transit insurance costs

Question Type: Concept

17) Which of the following would be considered part of the cost of machinery and equipment?

A) Sales taxes

B) Repairs after start-up

C) Maintenance

D) Insurance after purchase

Question Type: Concept

7

18) Rose Corp. purchased land for $77,000. Additionally, Rose paid title insurance of $700, a

commission of $7,000, and back taxes due in the amount of $1,000. To ready the land for

construction, Rose paid $3,000 to remove an unwanted building, $6,000 to level and grade the

property, and $12,000 for paving. The cost of the company’s land is _______, and the land

improvements are _______.

A) $77,000; $29,700

B) $85,700; $21,000

C) $88,700; $15,000

D) $94,700; $12,000

Question Type: Application

19) Manitou, Inc. purchased land for $94,000 by signing a note payable for the same amount.

Additionally, Manitou paid cash for the following: title insurance of $1,600, a commission of

$9,400, $5,000 to remove an unwanted building, $3,400 to level and grade the property, $26,000

for paving, $23,000 to construct a fence around the perimeter, and $5,400 for lighting. The

journal entry for the cash payment is:

A) debit land $19,400, debit land improvement $54,400, credit cash $73,800

B) debit land $11,000, debit land improvement $62,800, credit cash $73,800

C) debit land $113,400, debit land improvement $54,400, credit cash $167,800

D) debit land $105,000, debit land improvement $62,800, credit cash $167,800

Question Type: Application

20) The total cost allocated to each item in a basket purchase is based upon:

A) the original cost of the items.

B) their relative market values.

C) their individual selling price.

D) their individual market values.

Question Type: Concept

21) Metropolitan Masonry made a basket purchase of three items. Item X was appraised at

$39,000; item Y was appraised at $57,000 and item Z was appraised at $61,000. The purchase

price was $129,000. The amount at which item Y should be recorded is:

A) ($57,000/$129,000) × $157,000.

B) ($57,000/$157,000) × $129,000.

C) ($57,000/$100,000) × $157,000.

D) ($57,000/$100,000) × $129,000.

Question Type: Application

8

22) Capitol Construction Company made a basket purchase of three items. Item X was appraised

at $55,000; item Y was appraised at $65,000 and item Z was appraised at $40,000. The purchase

price was $125,000. The amount at which item Z should be recorded (rounded to the nearest

dollar) is: (Round any intermediary calculations to the nearest cent and your final answer to the

nearest dollar.)

A) $51,200.

B) $40,000.

C) $31,250.

D) $42,969.

Question Type: Application

23) Lionworks Corporation made a basket purchase of three items. Item X was appraised at

$30,000; item Y was appraised at $55,000; and item Z was appraised at $65,000. The purchase

price was $125,000. The amount at which item X should be recorded (rounded to the nearest

dollar) is: (Round any intermediary calculations to the nearest cent and your final answer to the

nearest dollar.)

A) $36,000.

B) $25,000.

C) $5,000

D) $30,000.

Question Type: Application

24) Other than land, long-term assets that are capitalized are:

A) expensed in the year of purchase.

B) depreciated over the life of the asset.

C) recorded at market value.

D) recorded at net realizable value.

Question Type: Concept

25) Sydney’s Siding made a basket purchase involving four assets. Their market values were A:

$41,000; B: $40,000; C: $45,000; and D: $54,000. The price Sydney’s paid for the four assets

was $170,000. What percentage of the $170,000 price would be allocated to asset C to the

nearest one-tenth of a percent? (Round any intermediary calculations to the nearest cent and your

final answer to the nearest dollar.)

A) 33.3%

B) 26.5%

C) 25%

D) 22.2%

Question Type: Application

9

26) Bob’s Bakery made a basket purchase involving four assets. Their market values were A:

$50,000; B: $46,000 C: $48,000; and D: $56,000. The price Bob’s paid for the four assets was

$150,000. To the nearest dollar, what final price will be recorded for asset D? (Round any

intermediary calculations to the nearest cent and your final answer to the nearest dollar.)

A) $6,000

B) $36,000

C) $56,000

D) $42,000

Question Type: Concept

27) Which of the following would be considered part of the cost of a printing press?

A) The medical fees for a worker who was injured while installing the press

B) The cost of a test run to make sure the press worked properly

C) Both A and B are part of the cost of the printing press.

D) Neither A nor B are part of the cost of the printing press.

Question Type: Concept

28) In accounting, what is the meaning of capitalized?

A) Capitalized means that a liability account is credited (increased) for the cost of an asset.

B) Capitalized means that an asset account is debited (increased) for the cost of an asset.

C) Capitalized means that the cost of an asset is recorded as a debit (increase) to expense.

D) Capitalized means that a given city has been selected as a government center.

Question Type: Concept

8.3 Calculate and record the depreciation of fixed assets

1) Depreciation is a process of valuation of an asset.

Question Type: Concept

2) Depreciation is based upon cost, useful life and salvage value.

Question Type: Concept

3) A fixed asset’s useful life may be shorter than its physical life due to obsolescence.

Question Type: Concept

10

4) Book value is depreciable cost minus accumulated depreciation.

Question Type: Concept

5) Calculating depreciation using a base such as miles driven per year would be an example of

double-declining balance depreciation.

Question Type: Concept

6) Double-declining balance is an accelerated method of calculating depreciation where salvage

value is NOT part of the initial computation.

Question Type: Concept

7) A company purchased a computer on August 1, 2016. Using straight-line depreciation, the

company would report four (4) months depreciation on December 31, 2016.

Question Type: Application

8) The choice of depreciation method depends on the cost of the asset and its’ expected useful

life.

Question Type: Concept

9) A company should choose a depreciation method that most closely matches the cost of the

asset against the future revenues it generates.

Question Type: Concept

10) A new vehicle was purchased on January 1 for $46,000. It has a salvage value of $7,000 and

a useful life of 6 years. To the nearest dollar, how much will the depreciation expense for the

vehicle be for the first year using the straight-line method?

A) $6,500

B) $639

C) $7,667

D) $542

Question Type: Application