Multinational Business Finance, 14e (Eiteman)

Chapter 15 Multinational Tax Management

15.1 Tax Principles

1) The issue of ethics in the reporting of income and the payment of taxes is a considerable one.

The authors state that most MNEs operating in foreign countries tend to follow the general

principle of:

A) “when in Rome, do as the Romans do.”

B) full disclosure to the tax authorities.

C) maintain a competitive playing field by cheating as much as the local competition, no more,

no less.

D) none of the above

2) Which of the following is an unlikely objective of U.S. government policy for the taxation of

foreign MNEs?

A) to raise revenues

B) to provide an incentive for U.S. private investment in developing countries

C) to improve the U.S. balance of payments

D) All of the above are objectives.

3) A ________ tax policy is one that has no impact on private decision-making, while a

________ policy is designed to encourage specific behavior.

A) flat; tax incentive

B) neutral; flat

C) neutral; tax incentive

D) none of the above

4) Which of the following is NOT an example of a tax incentive policy?

A) The federal government gives a tax credit to MNEs that make domestic capital improvements

but not foreign capital improvements.

B) Corporations are allowed to take a direct tax credit for each dollar of matching donations they

make to institutions of higher education.

C) A tax law is passed that makes interest on property non tax-deductible, but interest payments

on durable goods are.

D) All are examples of a tax incentive policy.

5) Toyota Motor Company operates in many different countries and pays taxes at many different

rates. However, they always pay the same rate as their local competitors. Toyota Motor

Company is operating in an environment of ________ tax policy.

A) domestic neutrality

B) foreign neutrality

C) territorial approach

D) none of the above

6) The United States taxes the domestic and remitted foreign earnings of U.S. based MNEs no

matter where the earnings occurred. This is an example of a/an ________ approach to levying

taxes.

A) worldwide

B) territorial

C) neutral

D) equitable

7) The United States taxes all earnings on U.S. soil by both domestic and foreign firms. This is

an example of a ________ approach to levying taxes.

A) worldwide

B) neutral

C) territorial

D) none of the above

8) Bacon Signs Inc. is based in a country with a territorial approach to taxation but generates

100% of its income in a country with a worldwide approach to taxation. The tax rate in the

country of incorporation is 25%, and the tax rate in the country where they earn their income is

50%. In theory, and barring any special provisions in the tax codes of either country, Bacon

should pay taxes at a rate of ______ in the country of incorporation.

A) 75%.

B) 62.5%.

C) 0%.

D) 50%.

9) The territorial approach to taxation policy is also termed the ________ approach.

A) source

B) ethical

C) greedy

D) location

10) A tax that is effectively a sales tax at each stage of production is defined as a/an ________

tax.

A) flat

B) equitable

C) value-added tax

D) none of the above

11) What is the total value of taxes paid in the following example if the value added tax is 10%?

A farmer raises wheat that he sells for $1.50 to the grain company. The grain company sells to

the processor for $2.00 per bushel. The processor turns the wheat into a breakfast cereal and

wholesales it for $3.00 per bushel. The retailer sells the cereal for $4.00 per bushel.

A) $0.15

B) $0.20

C) $0.30

D) $0.40

12) A tax that is a form of social redistribution of income is defined as a/an ________ tax.

A) un-American

B) transfer

C) flat

D) none of the above

13) Tax treaties typically result in ________ between the two countries in question.

A) lower property taxes for U.S. citizens overseas

B) elimination of differential tax rates

C) increased double taxation

D) reduced withholding tax rates

14) The primary objective of multinational tax planning is to minimize the firm’s worldwide tax

burden.

15) A country CANNOT have both a territorial and a worldwide approach as a national tax

policy.

16) Tax treaties generally have the effect of increasing the withholding taxes between the

countries that are negotiating the treaties.

17) A value-added tax has gained widespread usage in Western Europe, Canada, and parts of

Latin America.

18) All indications are that the value-added tax will soon be the dominant form of taxation in the

U.S.

19) Among the G7 nations, the U.S. has a below average corporate income tax rate that makes it

attractive for other countries to invest in the U.S.

20) In the mid 1980s the U.S. led the way to higher corporate income tax rates worldwide.

Today, most of the G7 nations have surpassed the U.S. and have higher corporate income tax

rates than the U.S.

21) The ideal tax should not only raise revenue efficiently but also have as few negative effects

on economic behavior as possible.

22) The worldwide approach, also referred to as the residential or national approach to tax

policy, levies taxes on the income earned by firms that are incorporated in the host country,

regardless of where the income was earned (domestically or abroad).

23) The territorial approach, also referred to as the source approach to tax policy, levies taxes on

the income earned by firms that are incorporated in the host country, regardless of where the

income was earned (domestically or abroad).

24) Of the OECD 30 countries, most employ a worldwide approach to tax policy, but a few,

including the United States, use the worldwide approach.

25) FEW governments rely on income taxes, both personal and corporate, for their primary

revenue source.

26) Between 2006 – 2012, global corporate tax rates have trended upward.

27) Tax treaties typically result in reduced withholding tax rates between the two signatory

countries.

28) Explain the worldwide and territorial approaches of national taxation. The authors state that

the United States uses both approaches. How can this be? Give an example of each taxation

approach.

29) What is a value-added tax? Where is this type of tax in wide usage? Why do you suppose

this form of taxation has NOT been widely accepted in the United States?

Answer: A value-added tax (VAT) is a form of national sales tax, where goods are taxed at each

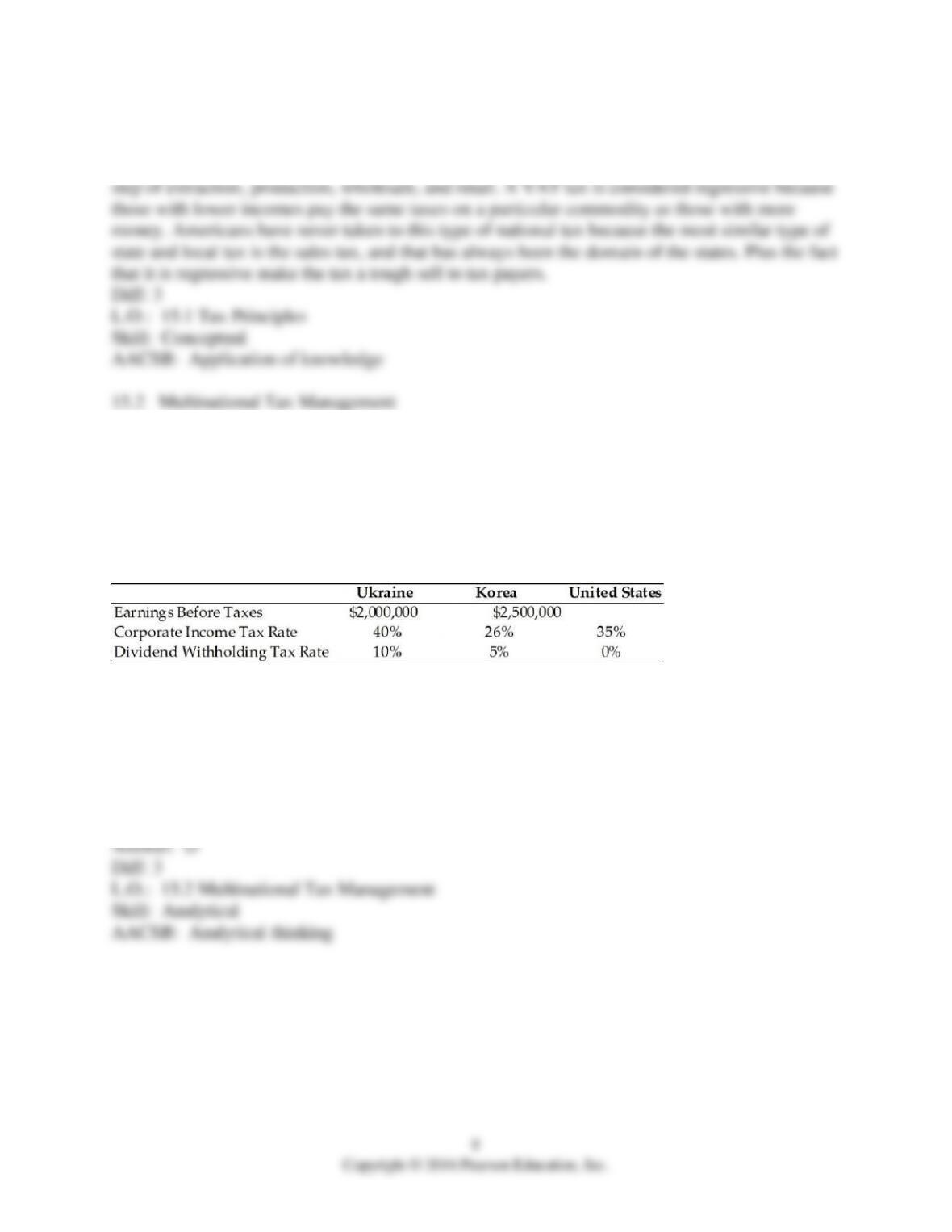

TABLE 15.1

Use the information to answer following question(s).

BayArea Designs Inc., located in Northern California, has two international subsidiaries, one

located in the Ukraine, the other in Korea. Consider the information below to answer the next

several questions.

1) Refer to Table 15.1. If BayArea pays out 50% of its earnings from each subsidiary, what are

the additional U.S. taxes due on the foreign sourced income from the Ukraine and Korea

respectively.

A) Ukraine = $0; Korea = ($30,000)

B) Ukraine = $100,000; Korea = $0

C) Ukraine = $0; Korea = $66,250

D) none of the above