3

Beginning the

Accounting Cycle

ANSWERS TO DISCUSSION QUESTIONS AND CRITICAL

THINKING/ETHICAL CASE

2. Disagree; it is based on the income statement.

4. Interim statements are financial statements prepared for parts of the fiscal period.

6. The debit(s) and credit(s) parts of recording a transaction are located on the same page of the journal. In the

ledger, they would be on separate pages.

8. A compound journal entry is a journal entry that requires three or more accounts.

10. False. The side that increases the account is the normal balance.

12. Cross-referencing updates the PR column in the journal after the ledger account has been updated.

14. The question in this case is whether Pete should be allowed to copy another company’s software. I believe that

there is something wrong with Pete asking his friend if he can copy his software. Software is protected under

SOLUTIONS TO CONCEPT CHECKS

1.

a.

201X

f.

Initial Investment by Owner

b.

Mar.

g.

$19,400

c.

2

h.

$19,400

d.

Cash and

i.

Page 1

Equipment

e.

B. Munro, Capital

2.

A.

Owner investment of cash and equipment

B.

Performed services for cash and on account

C.

Salary expense incurred but not paid

3.

Cash

111

Balance

Date

PR

Dr.

Cr.

Dr.

Cr.

201X

Mar. 6

GJ1

29

29

10

GJ1

90

119

15

GJ2

7

112

18

GJ3

75

187

PR column of cash tells us from which page of journal information came from. The

Acct. #111 will be used to cross reference back to the PR column of the Journal to tell

it was posted to Acct. #111 in the General Ledger.

4.

KENNEDY COMPANY

TRIAL BALANCE

JULY 31, 201X

Dr.

Cr.

Cash

13

Equipment

112

Accounts Payable

43

D. Kennedy, Capital

88

D. Kennedy, Withdrawals

5

Taxi Fees

18

Rent Expense

12

Advertising Expense

7

___

Totals

149

149

5.

Date Account Titles Dr. Cr.

201X

June

10

Telephone Expense

250

Repair Expense

250

A correcting entry may not be needed if the mistake is detected prior to posting.

SOLUTIONS TO SET A EXERCISES

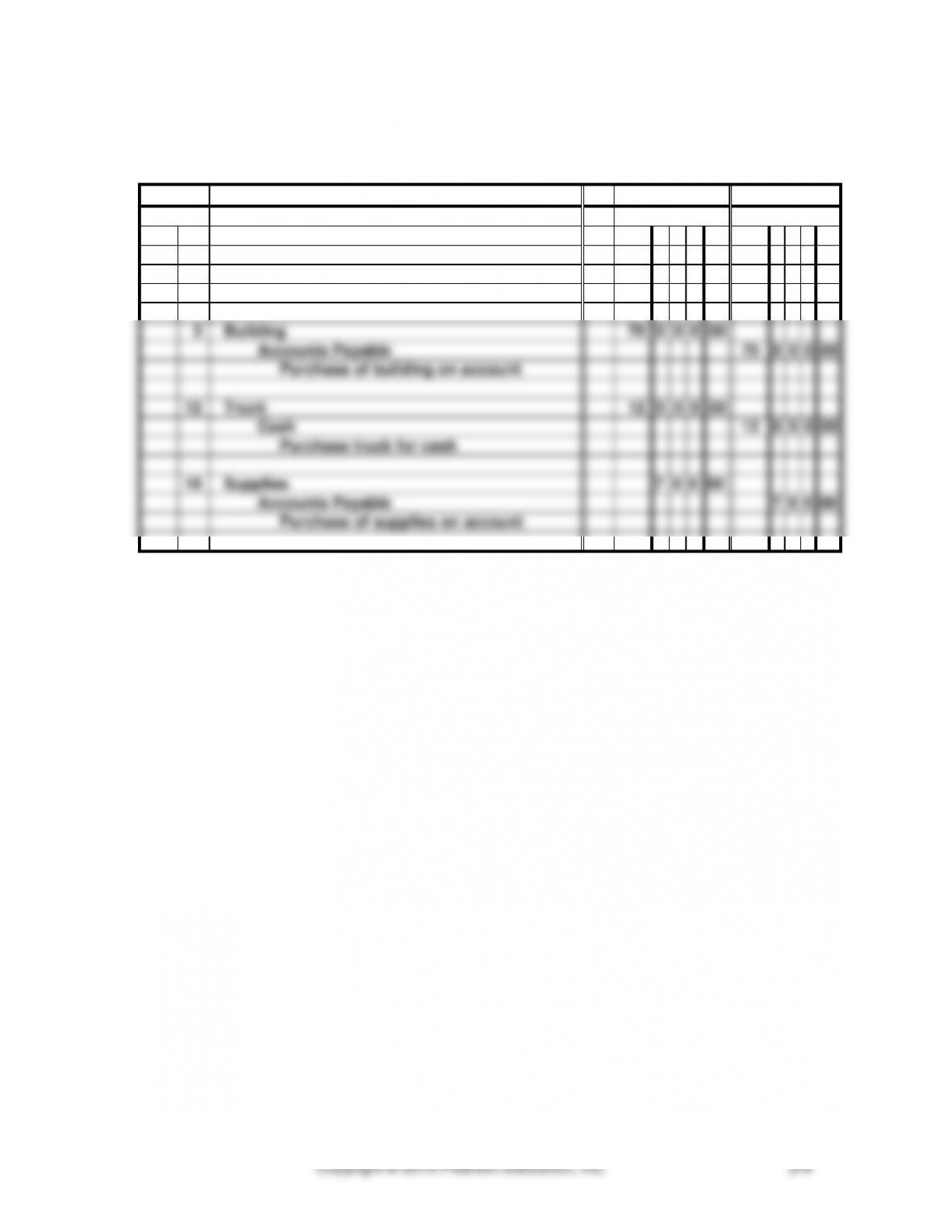

3A-1.

Date

Account Titles and Description

PR

Dr.

Cr.

201X

Apr

1

Cash

110

0

0

0

00

Equipment

12

0

0

0

00

J. Moore, Capital

122

0

0

0

00

Owner investment

3

Building

70

0

0

0

00

Accounts Payable

70

0

0

0

00

Purchase of building on account

12

Truck

12

0

0

0

00

Cash

12

0

0

0

00

Purchase truck for cash

18

Supplies

7

0

0

00

Accounts Payable

7

0

0

00

Purchase of supplies on account

EXERCISES (CONTINUED)

3A-2.

Date

Account Titles and Description

PR

Dr.

Cr.

201X

May

1

Cash

150

0

0

0

00

R. Tarsia, Capital

150

0

0

0

00

Owner investment

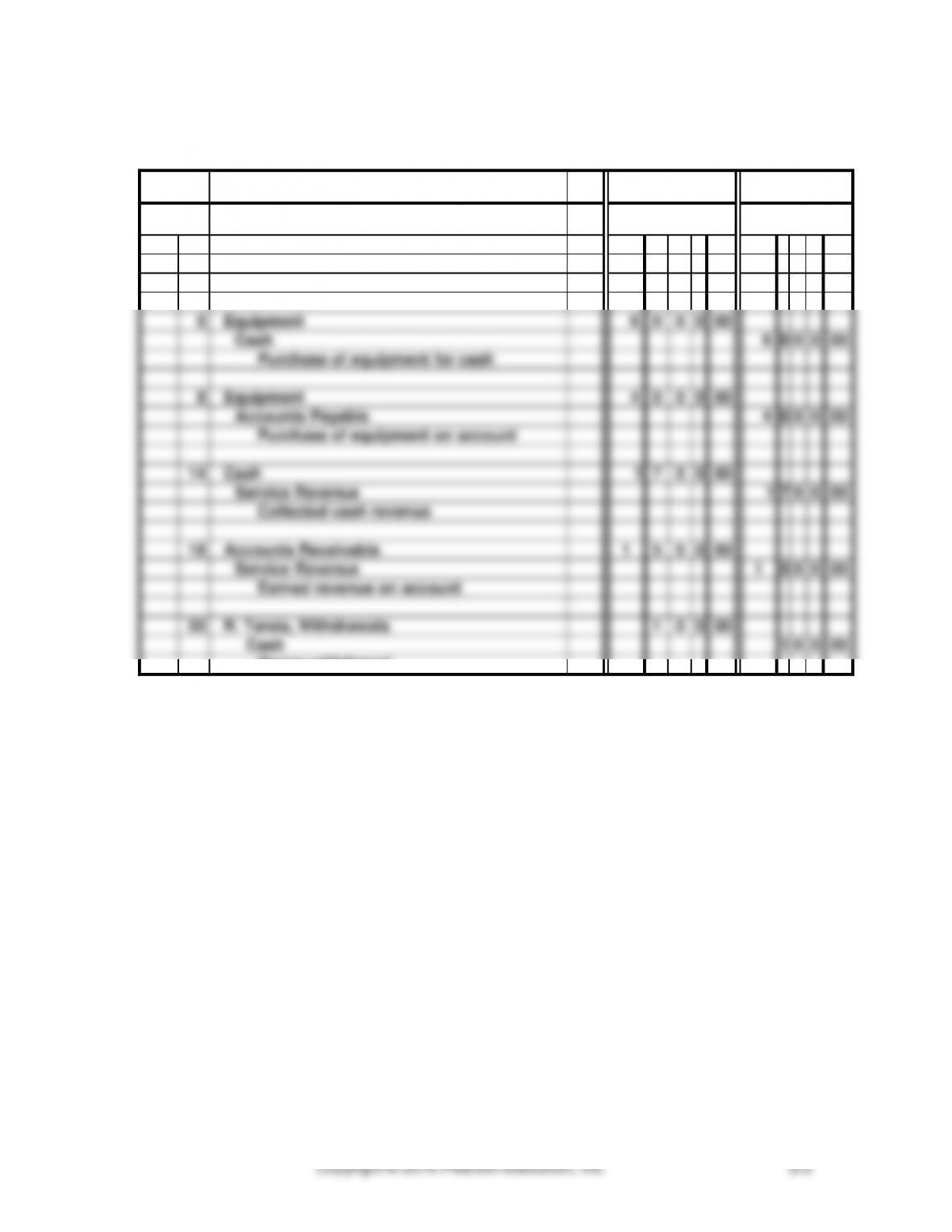

5

Equipment

6

0

0

0

00

Cash

6

0

0

0

00

Purchase of equipment for cash

8

Equipment

4

0

0

0

00

Accounts Payable

4

0

0

0

00

Purchase of equipment on account

14

Cash

1

7

0

0

00

Service Revenue

1

7

0

0

00

Collected cash revenue

18

Accounts Receivable

1

5

0

0

00

Service Revenue

1

5

0

0

00

Earned revenue on account

20

R. Tarsia, Withdrawals

1

0

0

00

Cash

1

0

0

00

Owner withdrawal

EXERCISES (CONTINUED)

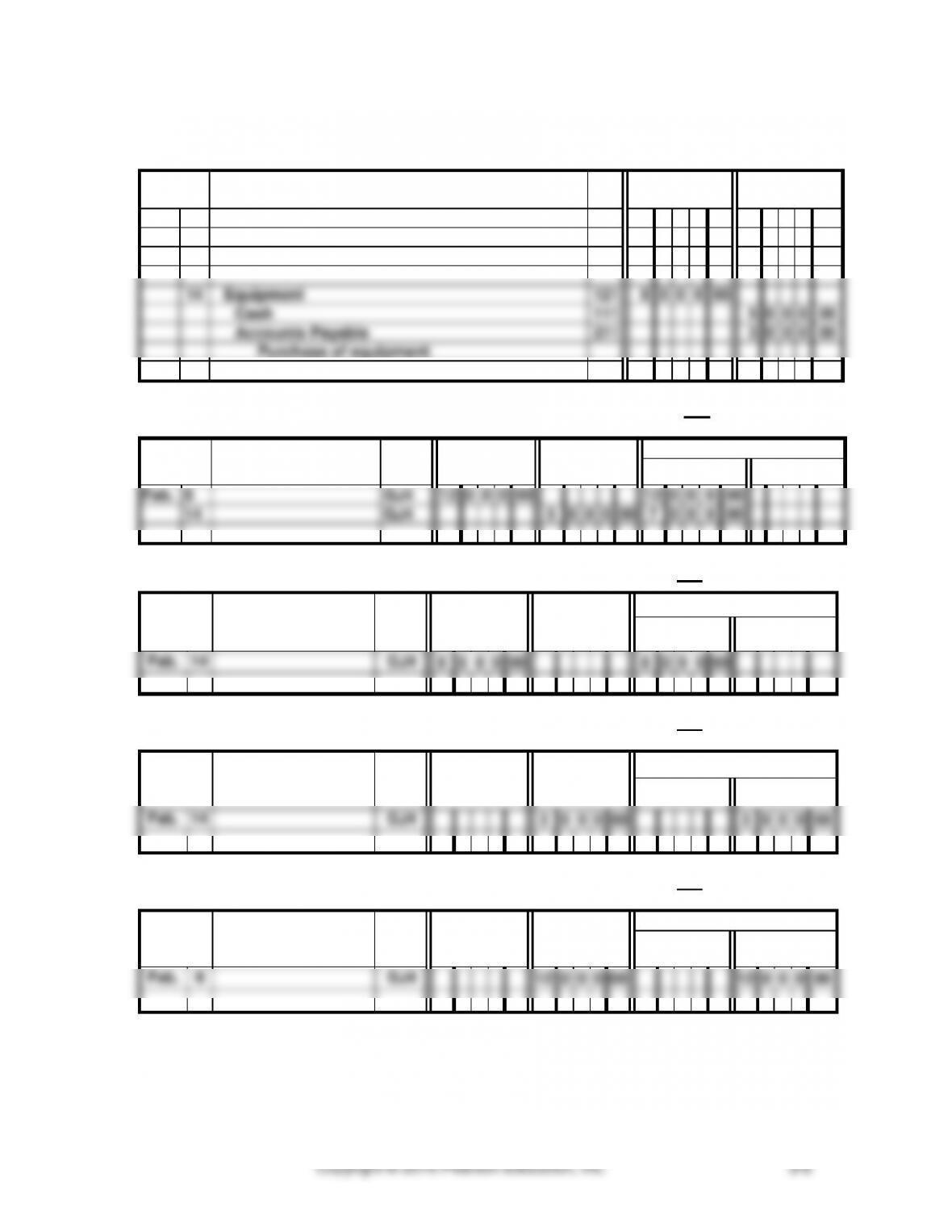

3A-3.

Date

201X

Account Titles and Description

PR

Dr.

Cr.

Feb.

6

Cash

111

12

0

0

0

00

A. Kramer, Capital

311

12

0

0

0

00

Cash investment

14

Equipment

121

8

0

0

0

00

Cash

111

5

0

0

0

00

Accounts Payable

211

3

0

0

0

00

Purchase of equipment

CASH

ACCOUNT NO. 111

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

Feb.

6

GJ4

12

0

0

0

00

12

0

0

0

00

14

GJ4

5

0

0

0

00

7

0

0

0

00

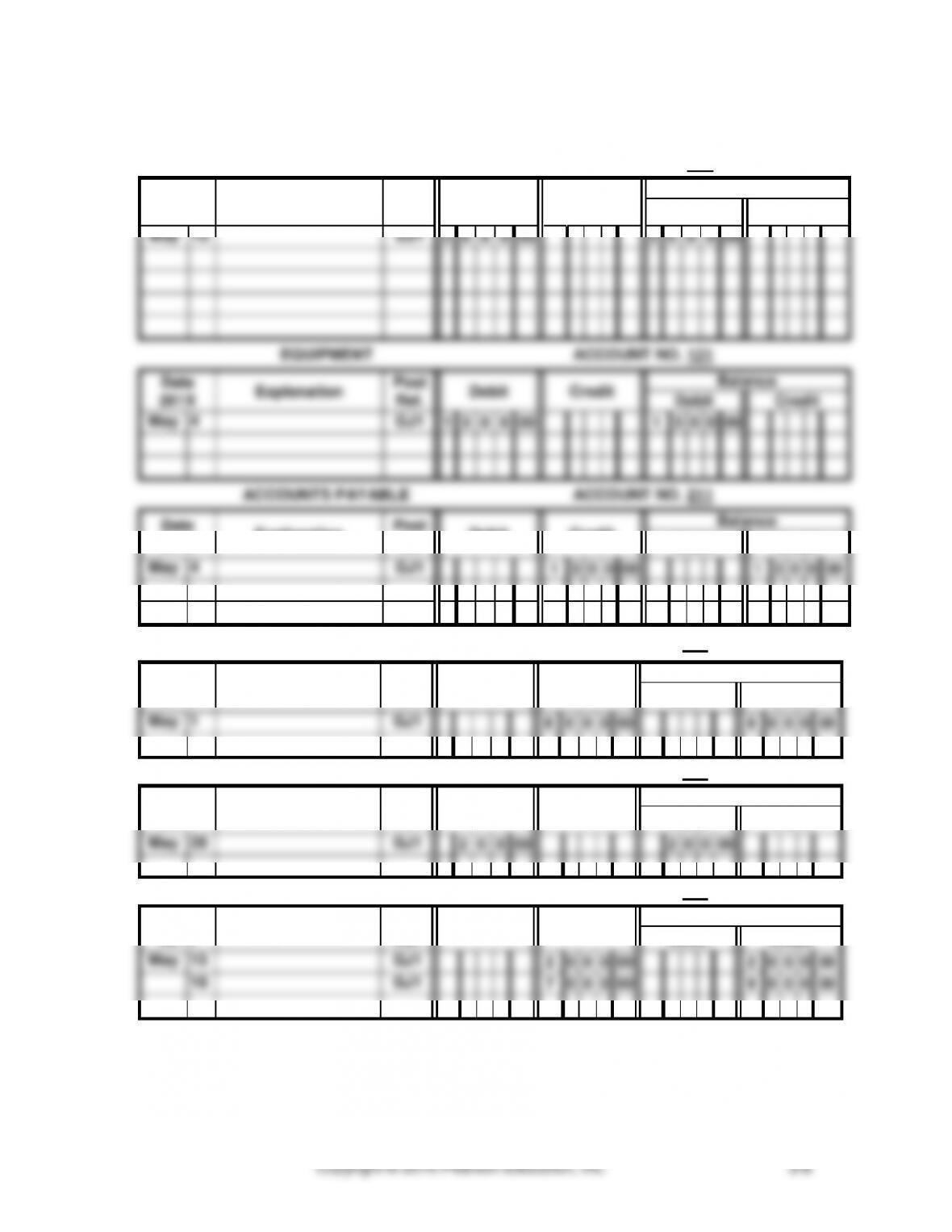

EQUIPMENT

ACCOUNT NO. 121

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

Feb.

14

GJ4

8

0

0

0

00

8

0

0

0

00

ACCOUNTS PAYABLE

ACCOUNT NO. 211

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

Feb.

14

GJ4

3

0

0

0

00

3

0

0

0

00

A. KRAMER, CAPITAL

ACCOUNT NO. 311

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

Feb.

6

GJ4

12

0

0

0

00

12

0

0

0

00

EXERCISES (CONTINUED)

3A-4

(a) PAGE 1

Date

201X

Account Titles and Description

PR

Dr.

Cr.

May

1

Cash

111

8

0

0

0

00

J. Lucas, Capital

311

8

0

0

0

00

Owner investment

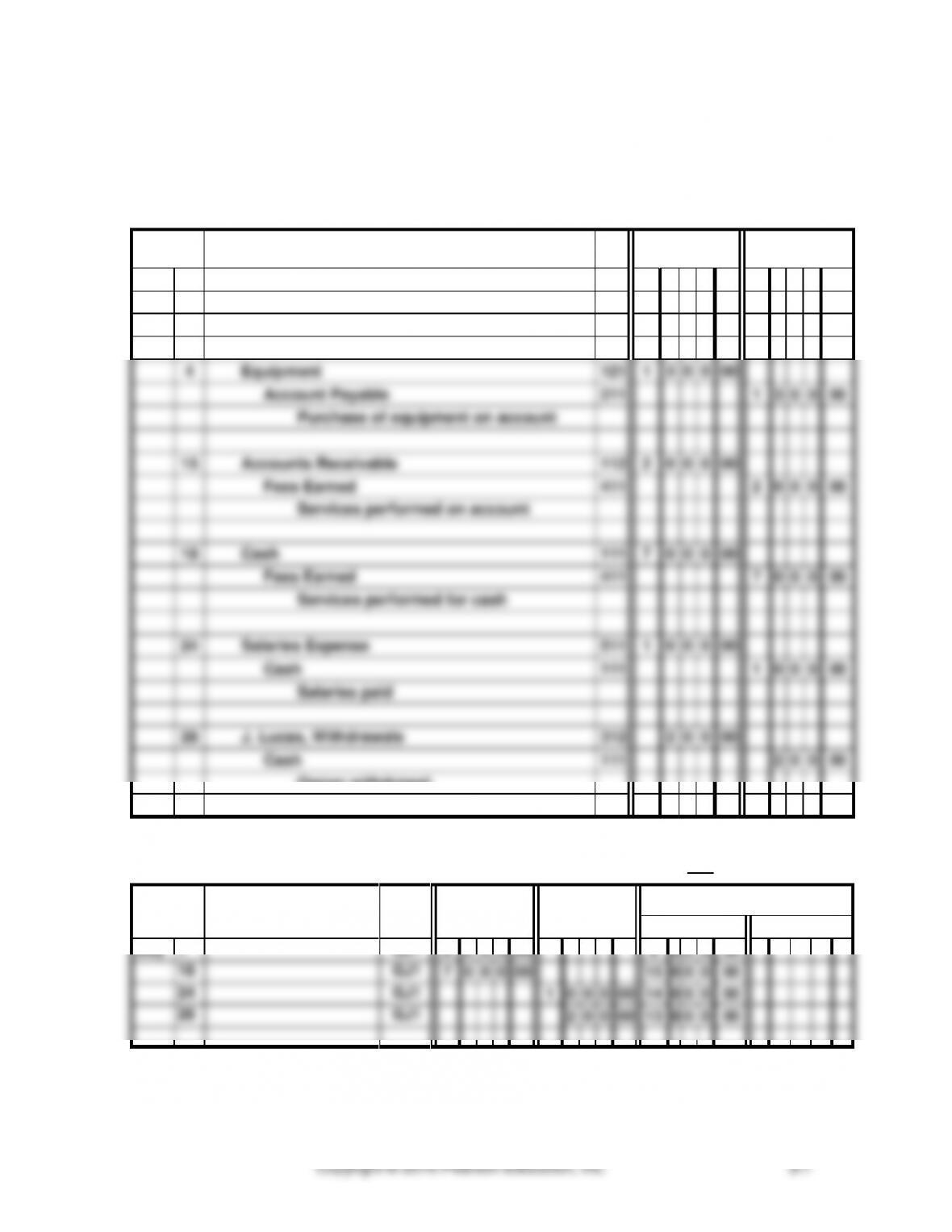

4

Equipment

121

1

3

0

0

00

Account Payable

211

1

3

0

0

00

Purchase of equipment on account

15

Accounts Receivable

112

2

0

0

0

00

Fees Earned

411

2

0

0

0

00

Services performed on account

18

Cash

111

7

0

0

0

00

Fees Earned

411

7

0

0

0

00

Services performed for cash

24

Salaries Expense

511

1

0

0

0

00

Cash

111

1

0

0

0

00

Salaries paid

28

J. Lucas, Withdrawals

312

2

0

0

00

Cash

111

2

0

0

00

Owner withdrawal

(b)

CASH

ACCOUNT NO. 111

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

1

GJ1

8

0

0

0

00

8

0

0

0

00

18

GJ1

7

0

0

0

00

15

0

0

0

00

24

GJ1

1

0

0

0

00

14

0

0

0

00

28

GJ1

2

0

0

00

13

8

0

0

00

EXERCISES (CONTINUED)

ACCOUNTS RECEIVABLE

ACCOUNT NO. 112

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

15

GJ1

2

0

0

0

00

2

0

0

0

00

EQUIPMENT

ACCOUNT NO. 121

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

4

GJ1

1

3

0

0

00

1

3

0

0

00

ACCOUNTS PAYABLE

ACCOUNT NO. 211

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

4

GJ1

1

3

0

0

00

1

3

0

0

00

J. LUCAS, CAPITAL

ACCOUNT NO. 311

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

1

GJ1

8

0

0

0

00

8

0

0

0

00

J. LUCAS, WITHDRAWALS

ACCOUNT NO. 312

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

28

GJ1

2

0

0

00

2

0

0

00

FEES EARNED

ACCOUNT NO. 411

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

15

GJ1

2

0

0

0

00

2

0

0

0

00

18

GJ1

7

0

0

0

00

9

0

0

0

00

EXERCISES (CONTINUED)

SALARIES EXPENSE

ACCOUNT NO. 511

Date

201X

Explanation

Post

Ref.

Debit

Credit

Balance

Debit

Credit

May

24

GJ1

1

0

0

0

00

1

0

0

0

00

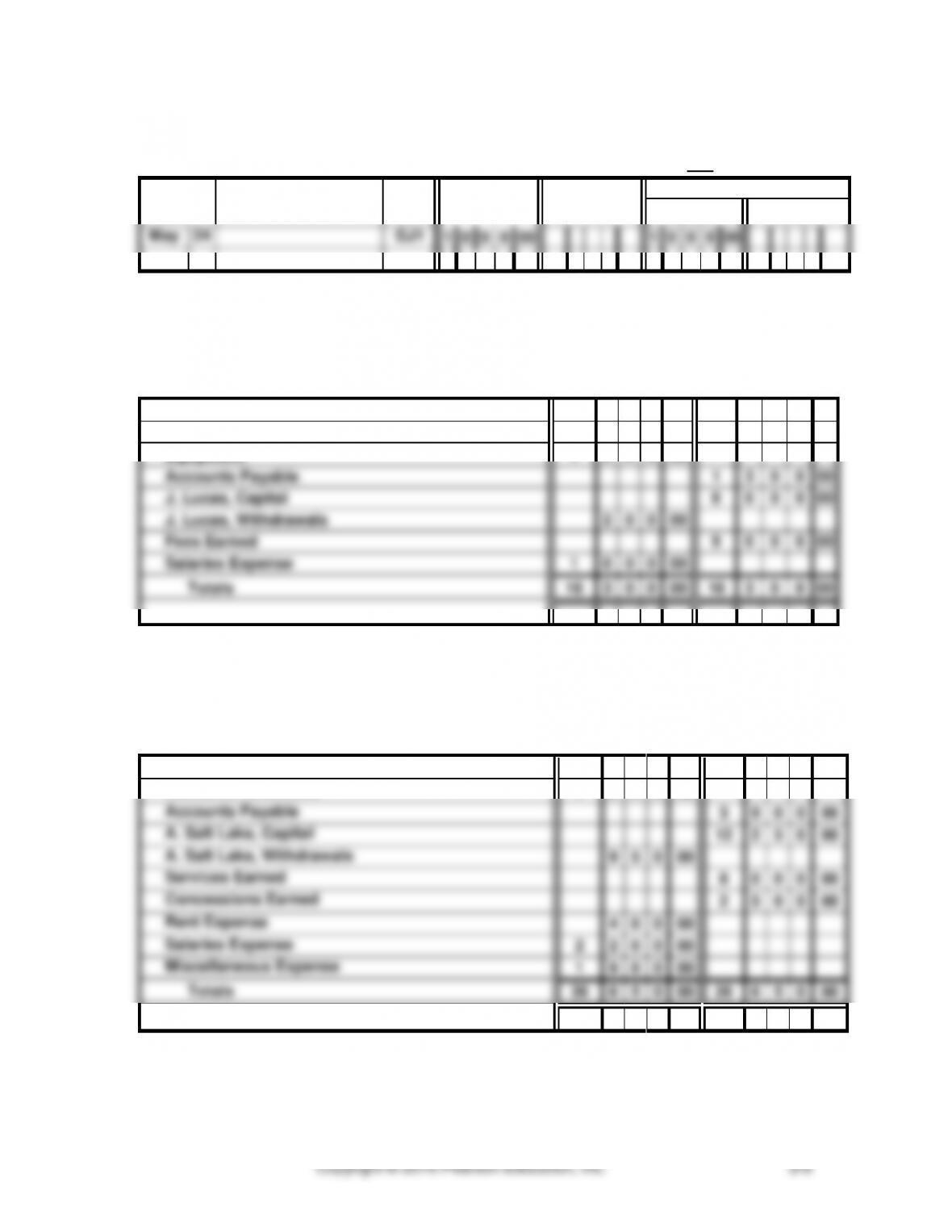

(c)

LUCAS COMPANY

TRIAL BALANCE

MAY 31, 201X

Dr.

Cr.

Cash

13

8

0

0

00

Accounts Receivable

2

0

0

0

00

Equipment

1

3

0

0

00

Accounts Payable

1

3

0

0

00

J. Lucas, Capital

8

0

0

0

00

J. Lucas, Withdrawals

2

0

0

00

Fees Earned

9

0

0

0

00

Salaries Expense

1

0

0

0

00

Totals

18

3

0

0

00

18

3

0

0

00

3A-5

SALT LAKE CO.

TRIAL BALANCE

OCTOBER 31, 201X

Dr.

Cr.

Cash

20

0

0

0

00

Accounts Receivable

1

2

0

0

00

Accounts Payable

3

9

0

0

00

A. Salt Lake, Capital

12

2

5

0

00

A. Salt Lake, Withdrawals

9

5

0

00

Services Earned

8

0

0

0

00

Concessions Earned

2

5

0

0

00

Rent Expense

4

0

0

00

Salaries Expense

2

2

0

0

00

Miscellaneous Expense

1

9

0

0

00

Totals

26

6

5

0

00

26

6

5

0

00

EXERCISES (CONTINUED)