20

Corporations and

2. Secured bonds pledge assets as security, while debenture bonds pledge no specific

assets.

4. False. Buyer pays more.

6. It has to be adjusted to prorate the increase in interest expense over the life of the

bond.

8. Disagree; it will result in an even amount.

10. The interest method is used so that interest is a constant percentage of the carrying

value; thus the need to use the market rate in the calculation.

11. Amortization of discount or premium must be up to date. When a bond is retired, the

unamortized premium or discount as well as the liability must be removed. Cash is

13. One stock show does not guarantee success in the stock market. Both husband and

SOLUTIONS TO CONCEPT CHECKS

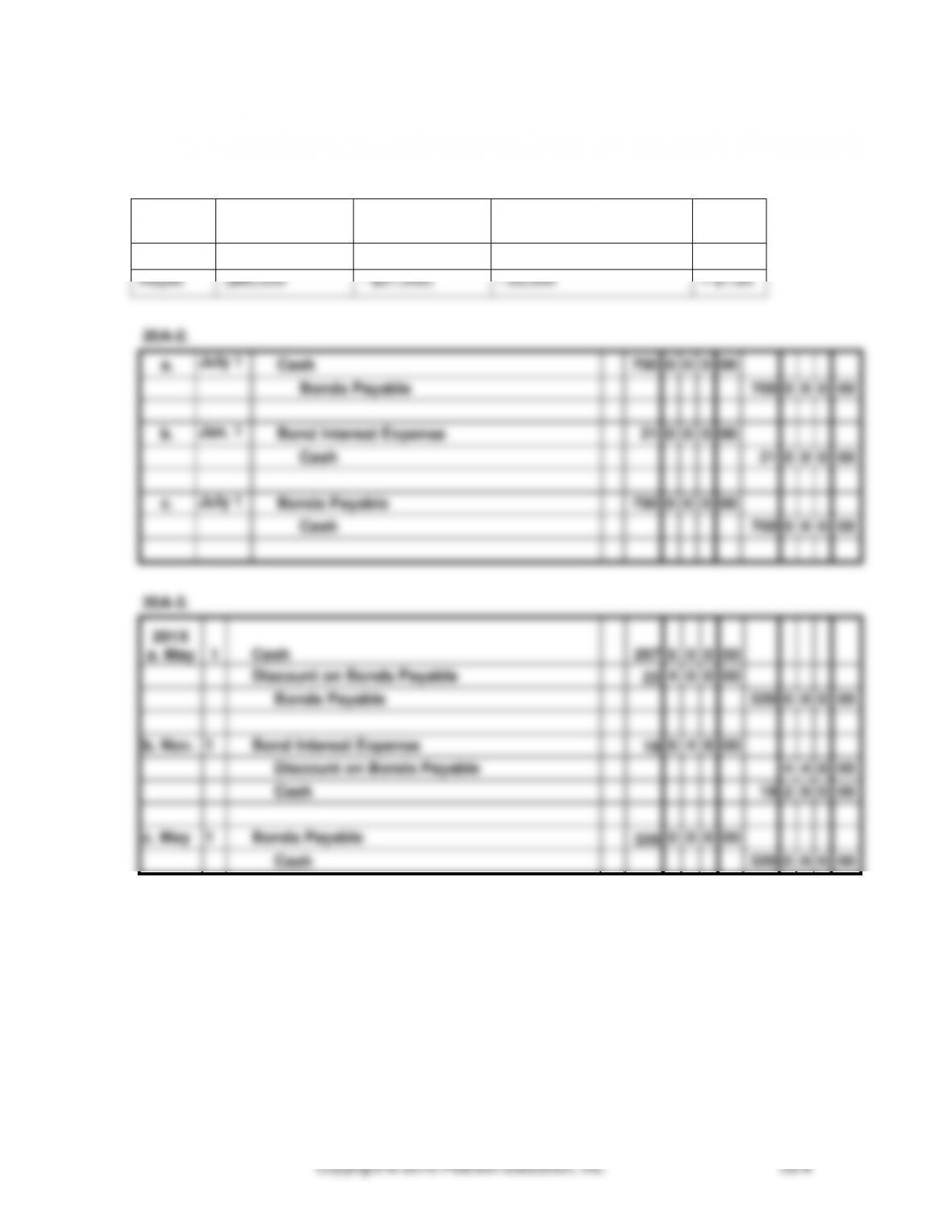

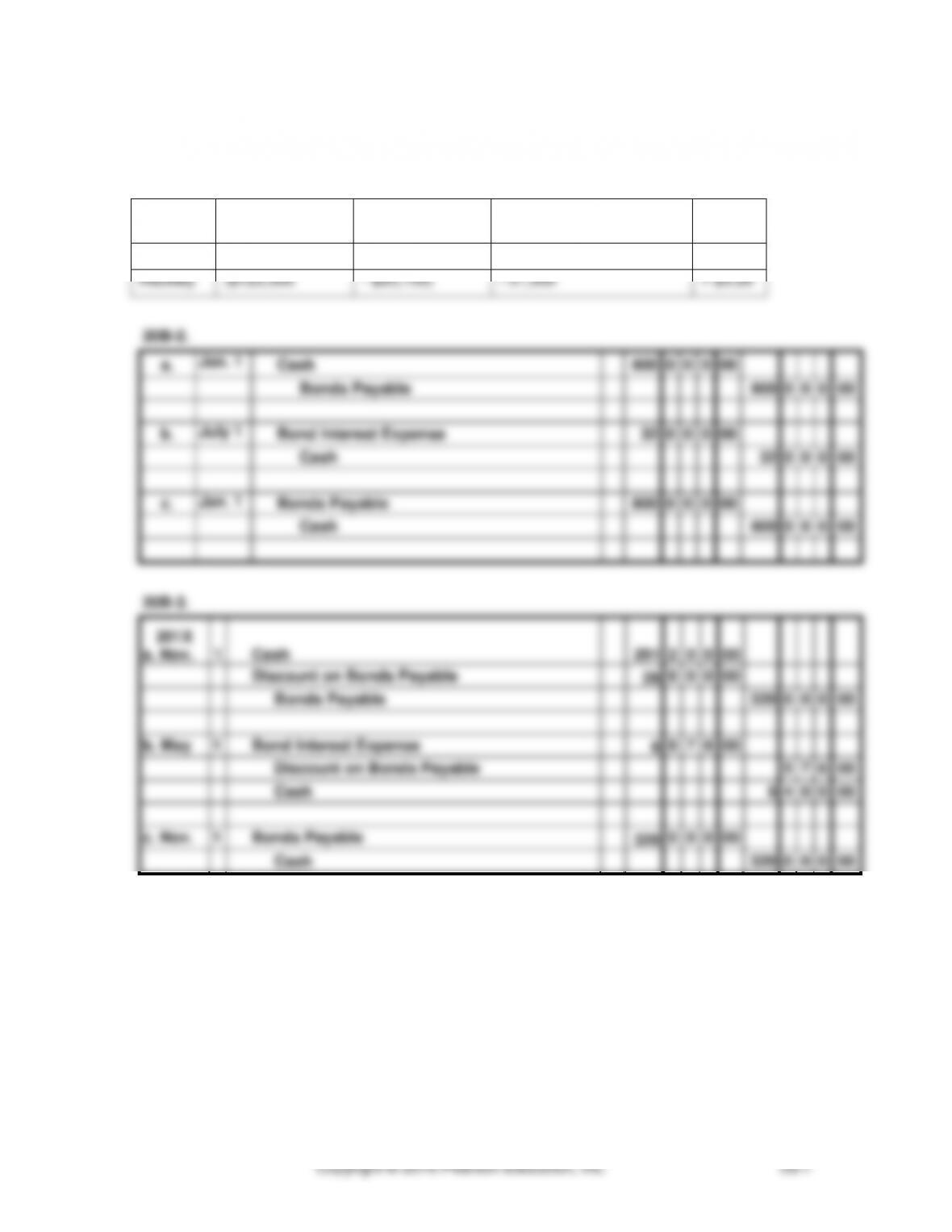

1.

a.

Sep. 1

Cash

50

0

0

0

00

Bonds Payable

50

0

0

0

00

b.

Feb. 28

Bond Interest Expense

2

2

5

0

00

Cash

2

2

5

0

00

c.

Sep. 1

Bonds Payable

50

0

0

0

00

Cash

50

0

0

0

00

Date Accounts Dr. Cr.

2.

Oct. 1

Cash

42,750

Discount on Bonds Payable

2,250

Bonds Payable

45,000

3.

Mar. 31 Bond Interest Expense

1,687.50

Discount on Bonds Payable

112.50

Cash

1,575.00

4.

Oct. 1

Cash

46,800

Premium on Bonds Payable

1,800

Bonds Payable

45,000

5.

Mar.

31

Bond Interest Expense

1,485.00

Premium on Bonds Payable

90.00

Bonds Payable

1,575.00

6.

a.

The carrying value of the bond at the beginning of the period is $129,569.

b.

The interest payment to the bondholders every six months is $6,750.

c.

The interest expense for the first semiannual period is $7,126.30.

d.

The discount to be amortized for the first semiannual period is $376.30.

e.

The carrying value at the end of the first semiannual period is $129,945.30.

Copyright © 2016 Pearson Education, Inc.

20-3

CONCEPT CHECKS (CONTINUED)

8.

a.

The carrying value of the bond at the beginning of the period is $191,805.

b.

The interest paid to the bondholders every six months is $6,175.

c.

Interest expense for the first semiannual period is $5,754.15.

d.

The premium to be amortized for the first semiannual period is $420.85.

e.

The carrying value at the end of the first semiannual period is $191,384.15.

9.

Oct 1

Bond Interest Expense

5,754.15

Premium on Bonds Payable

420.85

Cash

6,175

10.

a.

Bond Sinking Fund

6,200

Cash

6,200

b.

Bond Sinking Fund

160

Bond Sinking Fund Interest

Earned

160

c.

Bonds Payable

23,000

Bond Sinking Fund

23,000

SOLUTIONS TO SET A EXERCISES

20A-1.

(After-tax

earnings

– Dividends for

preferred)

/ Common shares

outstanding

= EPS

Evans

($58,400

– $0)

/ 29,000

= $2.01

Hayes

($80,000

– $27,000)

/ 29,000

= $1.83

EXERCISES (CONTINUED)

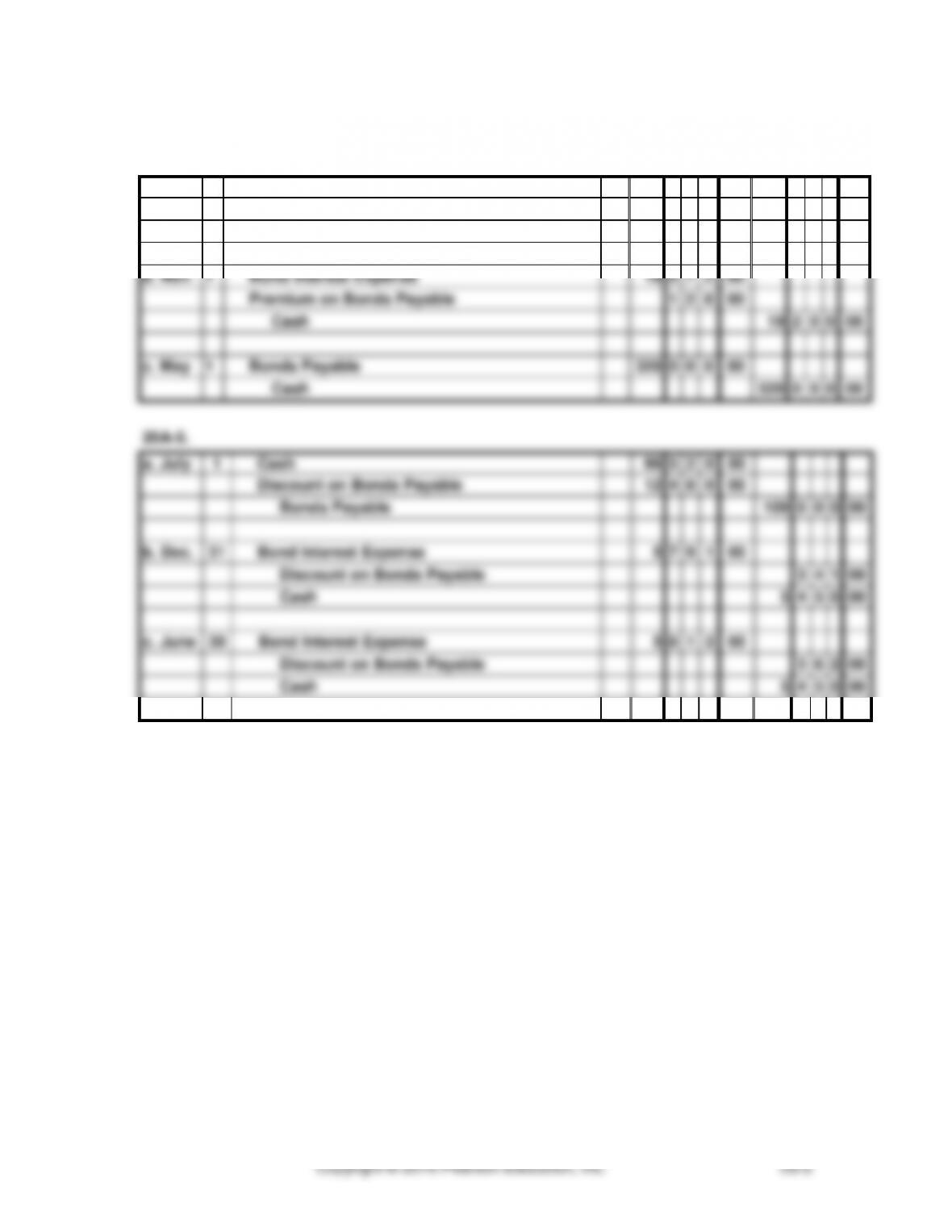

20A-4.

a. May

1

Cash

326

4

0

0

00

Premium on Bonds Payable

6

4

0

0

00

Bonds Payable

320

0

0

0

00

b. Nov.

1

Bond Interest Expense

19

0

7

2

00

Premium on Bonds Payable

1

2

8

00

Cash

19

2

0

0

00

c. May

1

Bonds Payable

320

0

0

0

00

Cash

320

0

0

0

00

20A-5.

a. July

1

Cash

96

5

2

0

00

Discount on Bonds Payable

12

4

8

0

00

Bonds Payable

109

0

0

0

00

b. Dec.

31

Bond Interest Expense

5

7

9

1

00

Discount on Bonds Payable

3

4

1

00

Cash

5

4

5

0

00

c. June

30

Bond Interest Expense

5

8

1

2

00

Discount on Bonds Payable

3

6

2

00

Cash

5

4

5

0

00

EXERCISES (CONTINUED)

20A-6.

a.

Bond Sinking Fund

23

6

0

8

00

Cash

23

6

0

8

00

b.

Bond Sinking Fund

1

1

8

0

00

Bond Sinking Fund Interest Earned

1

1

8

0

00

c.

Cash

4

0

0

00

Bonds Payable

340

0

0

0

00

Bond Sinking Fund

340

4

0

0

00

20A-7.

Long-Term Liabilities

12% Bonds Payable

$575,000

Add: Premium on Bonds Payable

10,000

$585,000

13% Bonds Payable

180,000

Deduct: Discount on Bonds Payable

11,000

169,000

Total Long-Term Liabilities

$754,000

SOLUTIONS TO SET B EXERCISES

20B-1.

(After-tax

earnings

– Dividends for

preferred)

/ Common shares

outstanding

= EPS

Moniz

($110,045

– $0)

/ 31,500

= $3.49

Hackley

($123,500

– $20,700)

/ 31,500

= $3.26

EXERCISES (CONTINUED)

20B-4.

a. Nov.

1

Cash

342

4

0

0

00

Premium on Bonds Payable

22

4

0

0

00

Bonds Payable

320

0

0

0

00

b. May

1

Bond Interest Expense

5

9

5

2

00

Premium on Bonds Payable

4

4

8

00

Cash

6

4

0

0

00

c. Nov.

1

Bonds Payable

320

0

0

0

00

Cash

320

0

0

0

00

20B-5.

a. July

1

Cash

94

7

4

9

00

Discount on Bonds Payable

12

2

5

1

00

Bonds Payable

107

0

0

0

00

b. Dec.

31

Bond Interest Expense

5

6

8

5

00

Discount on Bonds Payable

3

3

5

00

Cash

5

3

5

0

00

c. July

1

Bond Interest Expense

5

7

0

5

00

Discount on Bonds Payable

3

5

5

00

Cash

5

3

5

0

00

EXERCISES (CONTINUED)

20B-6.

a.

Bond Sinking Fund

23

6

1

5

00

Cash

23

6

1

5

00

b.

Bond Sinking Fund

2

3

6

2

00

Bond Sinking Fund Interest Earned

2

3

6

2

00

c.

Cash

4

5

0

00

Bonds Payable

370

0

0

0

00

Bond Sinking Fund

370

4

5

0

00

20B-7.

Long-Term Liabilities

14% Bonds Payable

$460,000

Add: Premium on Bonds Payable

4,000

$464,000

15% Bonds Payable

210,000

Deduct: Discount on Bonds Payable

10,000

200,000

Total Long-Term Liabilities

$664,000