16

Accounting for Property,

1. The costs involved in acquiring the asset and getting the asset in position and condition for use in the

company.

3. Revenue expenditures relate to expenses that do not extend the plant asset’s useful life, or improve

4. Straight-line: Depreciation expense is the same amount each year. Units–of-production:

5. The Modified Accelerated Cost Recovery System is used for tax purposes. It speeds up the

depreciation schedule.

7. Double declining-balance method.

9. True.

11. It is a contra-asset that recorded the amount of depletion accumulated.

13. The question in this case is whether the dealer is being fair to Pete. It does not seem that the dealer

SOLUTIONS TO CONCEPT CHECKS

2. The annual straight-line depreciation is $900.00

4. The first year depreciation is $375.00.

6.

Situation

Capital

Expenditure

Revenue

Expenditure

Addition

Betterment/

Extraordinary Repair

a. New truck engine replaced

X

X

b. New furnace filters

X

c. Oil change on truck

X

d. New addition on prep school

X

X

7. Account Category Financial Statement Found

a.

Gain on Sale of Plant Assets

Other Income

Income Statement

b.

Accumulated Depletion

Contra-Asset

Balance Sheet

c.

Loss on Disposal of Plant Assets

Other Expense

Income Statement

8.

a. What is the book value of the old machine? $8,500

What is the loss? $2,500

b.

Machinery-New

18,700

Loss on Exchange of Machinery

2,500

Accumulated Depreciation, Machinery

11,100

Machinery-Old

19,600

Cash

12,700

CONCEPT CHECKS (CONTINUED)

9.

a.

What is the book value of the old machine? $8,500

What is the gain? $4,000

b.

Machinery (new)

14,700

Accumulated Depreciation, Machinery

11,100

Machinery (old)

19,600

Cash

6,200

10.

Machinery (new)

21,200

Accumulated Depreciation, Machinery

11,100

Machinery (old)

19,600

Cash

12,700

SOLUTIONS TO SET A EXERCISES

16A-1.

The actual cost of the machine is $27,578.

16A-2.

(a) Straight-Line

Year

Cost

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book Value

End of Year

1

$1,470

$236

$236

$1,234

2

$1,470

$236

$472

$ 998

(b) Units-of–Production

Year

Cost

Output

Depreciation

Expense

Accumulated

Depreciation

Book Value

1

$1,470

50

$100

$100

$1,370

2

$1,470

200

$400

$500

$ 970

(c) Double Declining- Balance

Year

Cost

Accumulated

Depreciation

Beginning of

Year

Book Value

Beginning

of Year

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book

Value

End of

Year

1

$1,470

$0

$1,470

$588.00

$588.00

$882.00

2

$1,470

$588.00

$ 882.00

$352.80

$940.80

$529.20

EXERCISES (CONTINUED)

16A-3.

(a)

Straight-Line

Year

Cost

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book Value

End of Year

1

$6,780

$1,498

$1,498

$5,282

2

$6,780

$1,498

$2,996

$3,784

(b)

Double Declining-Balance

Accumulated

Depreciation

Book Value

Accumulated

Depreciation

Book

Value

Yr.

Cost

Beginning of

Year

Beginning

of Year

Depreciation

Expense

End of Year

End of

Year

1

$6,780

$0

$6,780

$3,390

$3,390

$3,390

2

$6,780

$3,390

$3,390

$1,695

$5,085

$1,695

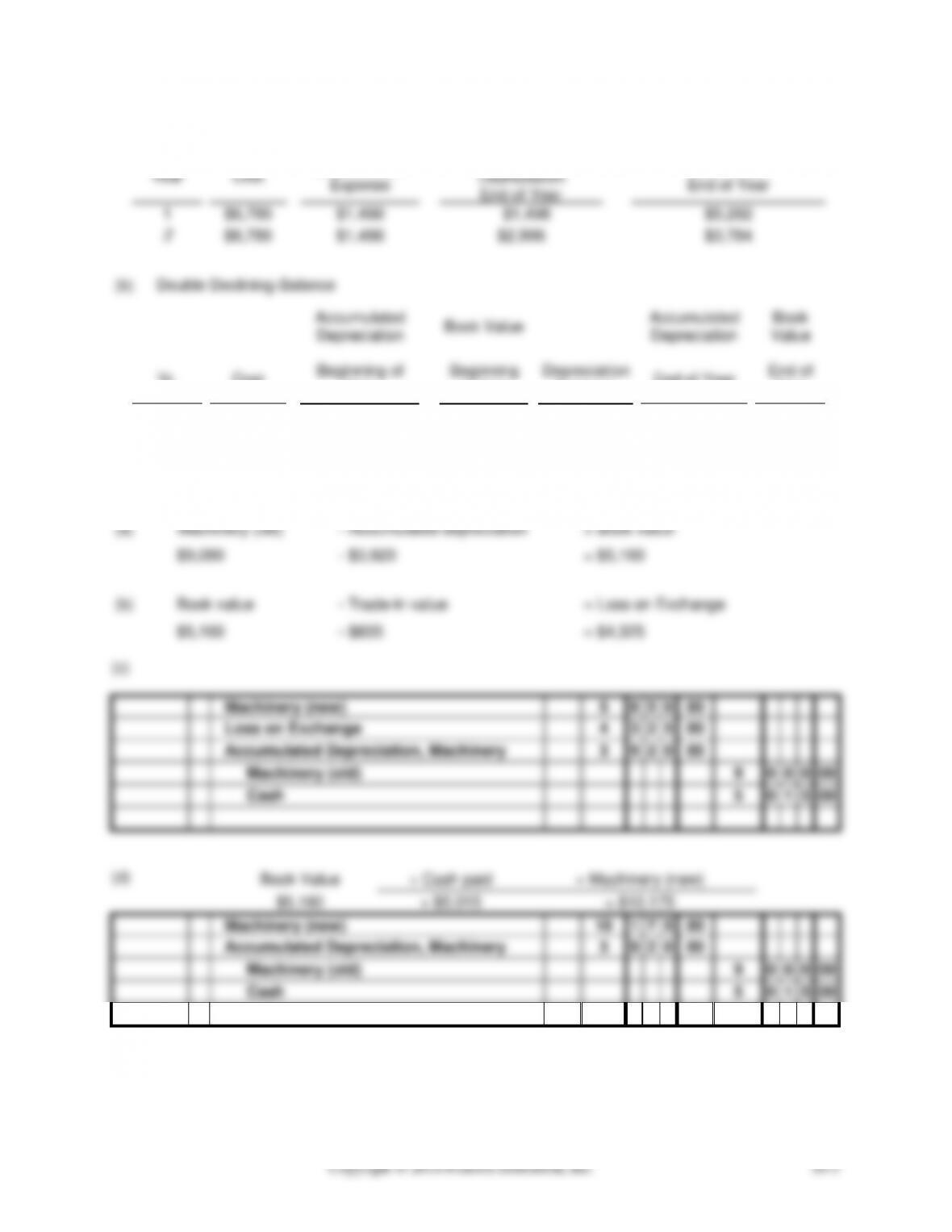

16A-4.

(a)

Machinery (old)

– Accumulated depreciation

= Book value

$9,080

– $3,920

= $5,160

(b)

Book value

– Trade-in value

= Loss on Exchange

$5,160

– $835

= $4,325

(c)

Machinery (new)

5

8

5

0

00

Loss on Exchange

4

3

2

5

00

Accumulated Depreciation, Machinery

3

9

2

0

00

Machinery (old)

9

0

8

0

00

Cash

5

0

1

5

00

(d)

Machinery (new)

10

1

7

5

00

Accumulated Depreciation, Machinery

3

9

2

0

00

Machinery (old)

9

0

8

0

00

Cash

5

0

1

5

00

Book Value

+ Cash paid

= Machinery (new)

$5,160

+ $5,015

= $10,175

EXERCISES (CONTINUED)

16A-5.

2014

Dec.

31

Amortization Expense, Patents

4

0

0

00

Patents

4

0

0

00

2015

Dec.

31

Amortization Expense, Patents

6

0

0

00

Patents

6

0

0

00

16A-6.

The depreciation for year 1 is $1,840.00.

The depreciation for year 2 is $2,944.00.

The depreciation for year 3 is $1,766.40.

The depreciation for year 4 is $1,059.84.

The depreciation for year 5 is $1,059.84.

The depreciation for year 6 is $529.92.

SOLUTIONS TO SET B EXERCISES

16B–1.

The actual cost of the machine is $29,256.

16B–2.

(a) Straight-Line

Year

Cost

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book Value

End of Year

1

$1,460

$240

$240

$1,220

2

$1,460

$240

$480

$980

(b) Units-of–Production

Year

Cost

Output

Depreciation

Expense

Accumulated

Depreciation

Book Value

1

$1,460

100

$190

$190

$1,270

2

$1,460

240

$456

$646

$814

(c) Double Declining- Balance

Year

Cost

Accumulated

Depreciation

Beginning of

Year

Book Value

Beginning

of Year

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book

Value

End of

Year

1

$1,460

$0

$1,460

$584.00

$584.00

$876.00

2

$1,460

$584.00

$ 876.00

$350.40

$934.40

$525.60

EXERCISES (CONTINUED)

16B–3.

(a)

Straight-Line

Year

Cost

Depreciation

Expense

Accumulated

Depreciation

End of Year

Book Value

End of Year

1

$6,800

$1,490

$1,490

$5,310

2

$6,800

$1,490

$2,980

$3,820

(b)

Double Declining-Balance

Accumulated

Depreciation

Book Value

Accumulated

Depreciation

Book

Value

Yr.

Cost

Beginning of

Year

Beginning

of Year

Depreciation

Expense

End of Year

End of

Year

1

$6,800

$0

$6,800

$3,400

$3,400

$3,400

2

$6,800

$3,400

$3,400

$1,700

$5,100

$1,700

16B–4.

(a)

Machinery (old)

– Accumulated depreciation

= Book value

$9,050

– $3,940

= $5,110

(b)

Book value

– Trade-in value

= Loss on Exchange

$5,110

– $820

= $4,290

(c)

Machinery (new)

5

8

7

0

00

Loss on Exchange

4

2

9

0

00

Accumulated Depreciation, Machinery

3

9

4

0

00

Machinery (old)

9

0

5

0

00

Cash

5

0

5

0

00

Accumulated Depreciation, Machinery

3

9

4

00

Machinery

9

0

5

0

00

Cash

5

0

5

0

00

EXERCISES (CONTINUED)

16B–5.

2014

Dec.

31

Amortization Expense, Patents

6

8

0

00

Patents

6

8

0

00

2015

Dec.

31

Amortization Expense, Patents

1

0

2

0

00

Patents

1

0

2

0

00

16B–6.

The depreciation for year 1 is $1,820.00.

The depreciation for year 2 is $2,912.00.

The depreciation for year 3 is $1,747.20.

The depreciation for year 4 is $1,048.32.

The depreciation for year 5 is $1,048.32.

The depreciation for year 6 is $524.16.

Copyright © 2016 Pearson Education, Inc.

16–10

SOLUTIONS TO SET A PROBLEMS

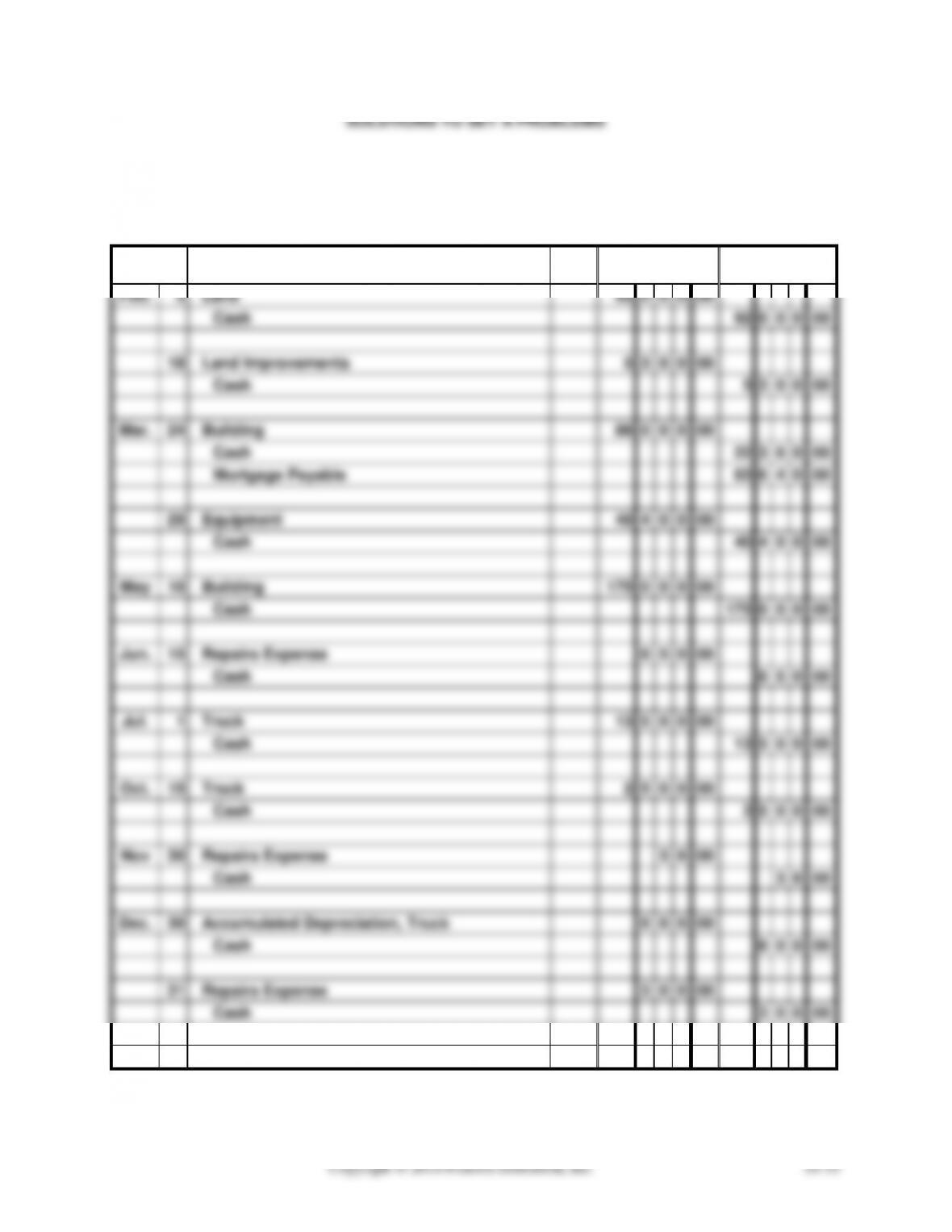

PROBLEM 16A-1

ORANGE COMPANY

GENERAL JOURNAL

PAGE 4

Date

201X

Account Titles and Description

PR

Dr.

Cr.

Feb.

5

Land

92

0

0

0

00

Cash

92

0

0

0

00

18

Land Improvements

5

3

0

0

00

Cash

5

3

0

0

00

Mar.

24

Building

86

0

0

0

00

Cash

22

3

6

0

00

Mortgage Payable

63

6

4

0

00

29

Equipment

40

4

0

0

00

Cash

40

4

0

0

00

May

10

Building

175

0

0

0

00

Cash

175

0

0

0

00

Jun.

15

Repairs Expense

8

5

0

00

Cash

8

5

0

00

Jul.

1

Truck

13

5

0

0

00

Cash

13

5

0

0

00

Oct.

15

Truck

2

5

0

0

00

Cash

2

5

0

0

00

Nov

30

Repairs Expense

3

6

00

Cash

3

6

00

Dec.

30

Accumulated Depreciation, Truck

8

0

0

00

Cash

8

0

0

00

31

Repairs Expense

3

0

0

00

Cash

3

0

0

00