13

Accounting for

1. The matching principle estimates the bad expense in the same period the sale is made, although the

write-off of the actual bad debt may not occur until future periods.

2. The Allowance for Doubtful Accounts accumulates estimated accounts receivable that will not be

3. Accounts Receivable

5. It has the opposite balance of accounts receivable. It shows the doubtful accounts that are not

expected to be collected.

7. Disagree. The income statement approach is based on the net credit sales on the income statement.

9. A company would age its accounts receivable to identify uncollected amounts to individual

10. Write-off:

Allowance for Doubtful Accounts

11. Both the Allowance account and Accounts Receivable are decreasing by same amount.

12. The direct write-off method recognizes a Bad Debts Expense when a receivable is deemed

14. Pete could avoid bad debts by accepting the use of credit cards by customers. It is common practice

to pass on the cost of credit cards to customers.

SOLUTIONS TO CONCEPT CHECKS

Account Category Increase/Decrease

1.

a. Bad Debts Expense

Expense

↑

Debit

Accounts Receivable

Asset

↓

Credit

b.

Bad Debt Expense will appear on the

income statement.

Accounts Receivable will appear on the

balance sheet.

2.

It is ignored in the income statement approach. If the credit balance in the Allowance for

Doubtful Accounts is $200 and the new estimate is $400, the $400 should be added to the

Allowance account balance for a total of $600.

3.

a. Bad Debts Expense

680

Allowance for Doubtful Accounts

680

Estimate of Bad Debts

b. Bad Debts Expense

330

Allowance for Doubtful Accounts

330

Estimate of Bad Debts

4. #1

Allowance for Doubtful Accounts

100

Accounts Receivable, Janice Lake

100

Wrote off Lake account

#2

Accounts Receivable, Janice Lake

100

Allowance for Doubtful Accounts

100

Reinstated Lake Account

Cash

100

Accounts Receivable, Janice Lake

100

Collected from Lake

5. #1 Bad Debt Expense 100

Accounts Receivable, Janice Lake 100

SOLUTIONS TO SET A EXERCISES

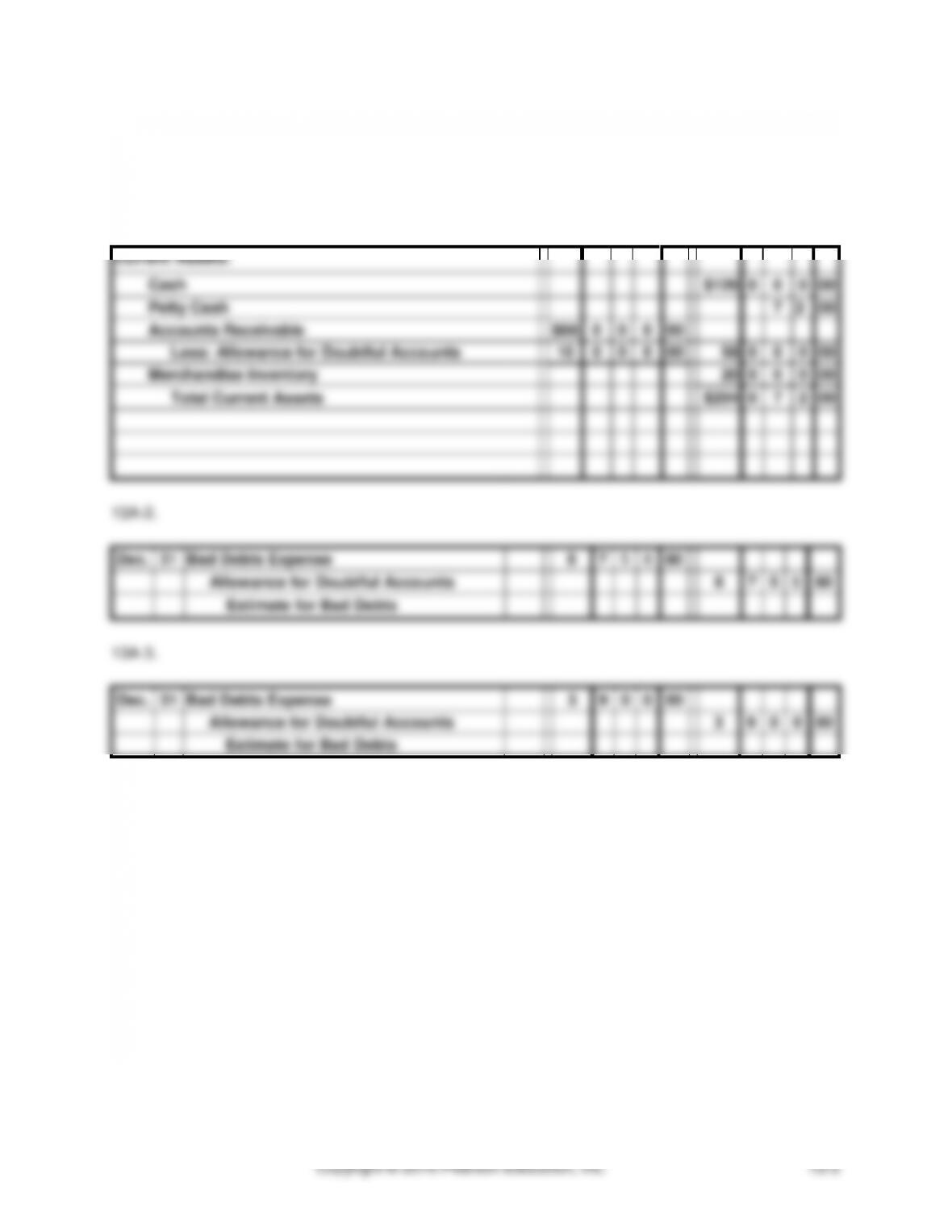

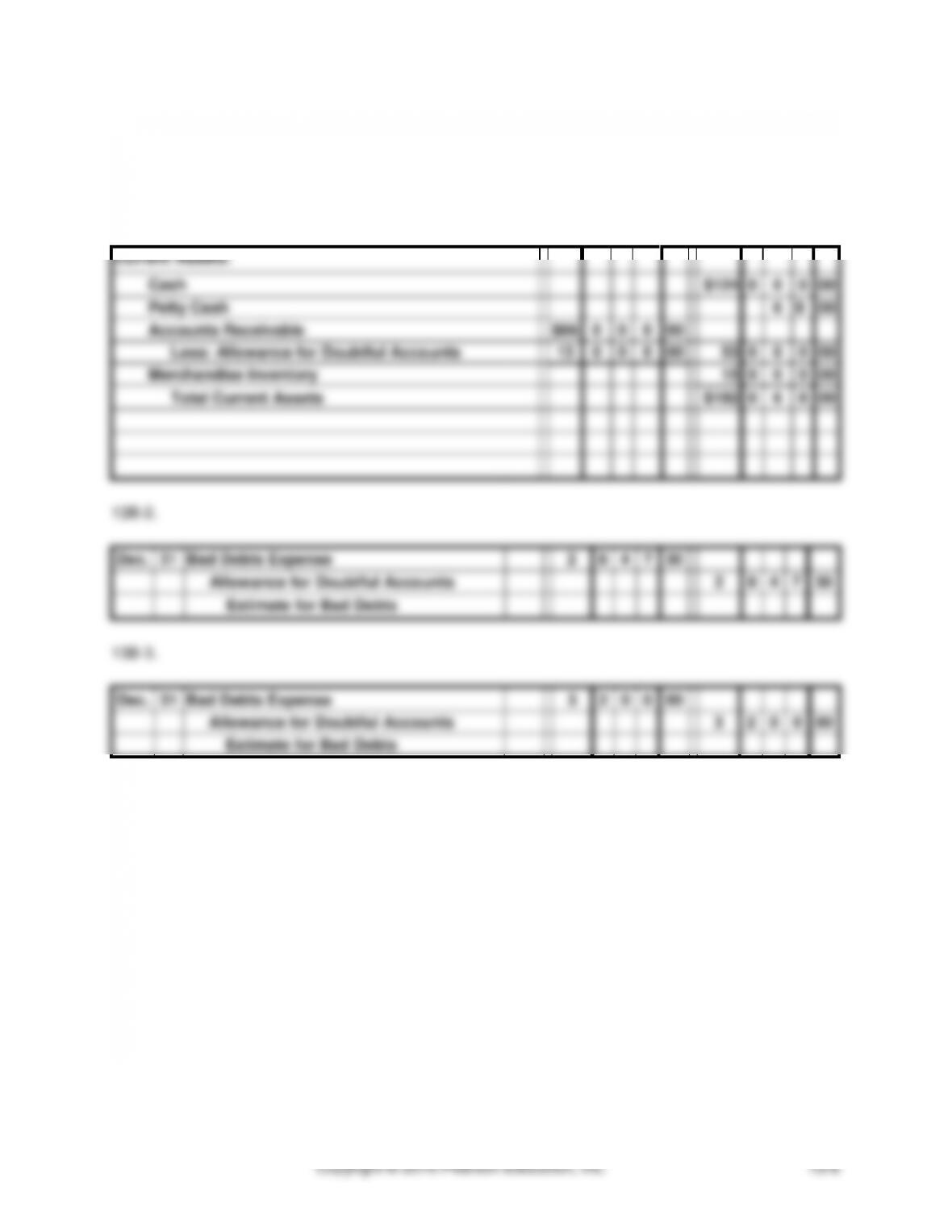

13A-1.

ACRES.COM

PARTIAL BALANCE SHEET

DECEMBER 31, 2015

Current Assets:

Cash

$126

0

0

0

00

Petty Cash

7

2

00

Accounts Receivable

$68

0

0

0

00

Less: Allowance for Doubtful Accounts

10

0

0

0

00

58

0

0

0

00

Merchandise Inventory

20

0

0

0

00

Total Current Assets

$204

0

7

2

00

13A-2.

Dec.

31

Bad Debts Expense

8

7

5

8

80

Allowance for Doubtful Accounts

8

7

5

8

80

Estimate for Bad Debts

13A-3.

Dec.

31

Bad Debts Expense

3

9

0

0

00

Allowance for Doubtful Accounts

3

9

0

0

00

Estimate for Bad Debts

EXERCISES (CONTINUED)

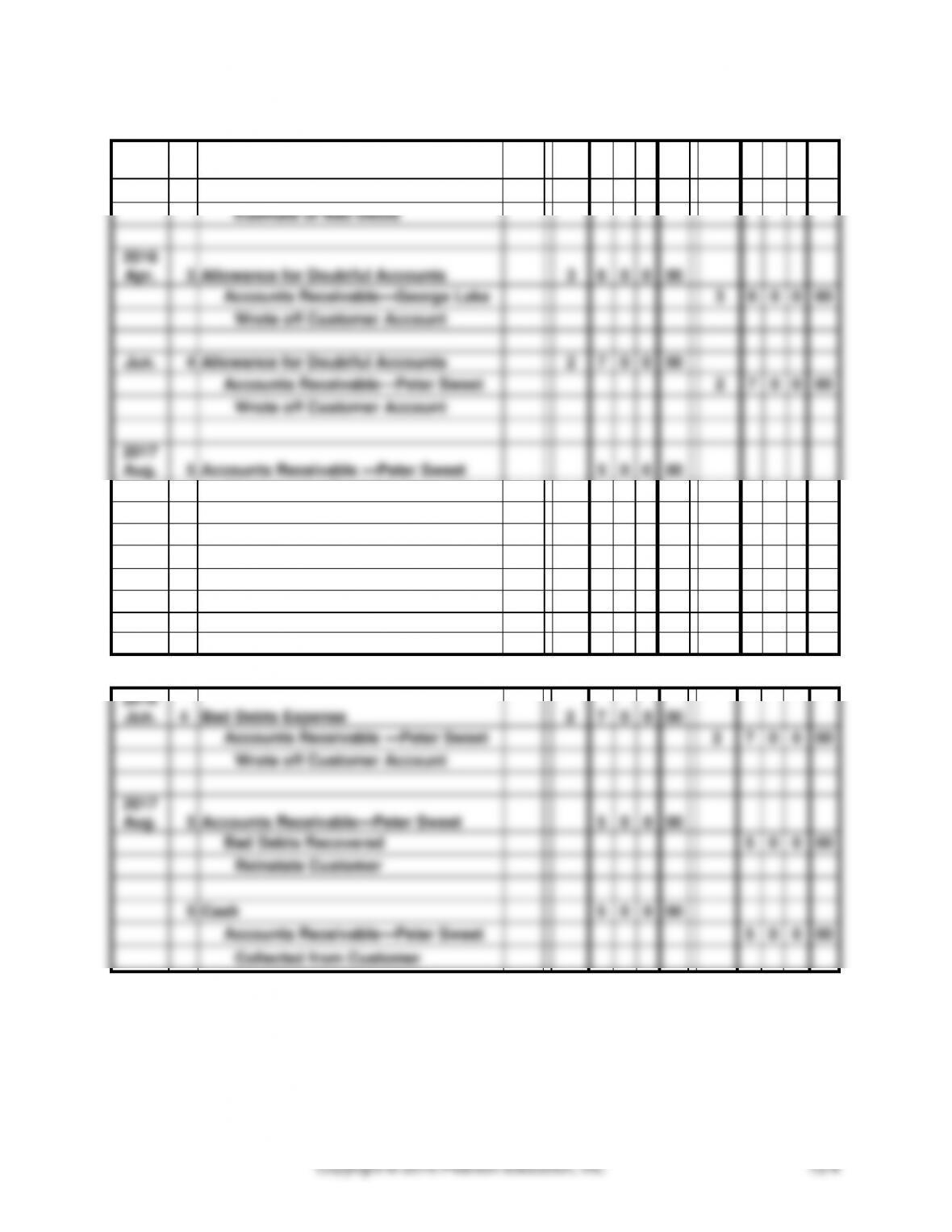

13A-4.

(a)

2015

Dec.

31

Bad Debts Expense

12

3

0

0

00

Allowance for Doubtful Accounts

12

3

0

0

00

Estimate of Bad Debts

2016

Apr.

3

Allowance for Doubtful Accounts

3

6

0

0

00

Accounts Receivable—George Lake

3

6

0

0

00

Wrote off Customer Account

Jun.

4

Allowance for Doubtful Accounts

2

7

0

0

00

Accounts Receivable—Peter Sweet

2

7

0

0

00

Wrote off Customer Account

2017

Aug.

5

Accounts Receivable —Peter Sweet

5

0

0

00

Allowance for Doubtful Accounts

5

0

0

00

Reinstate Customer

5

Cash

5

0

0

00

Accounts Receivable —Peter Sweet

5

0

0

00

Collected from Customer

(b )

2016

Jun.

4

Bad Debts Expense

2

7

0

0

00

Accounts Receivable —Peter Sweet

2

7

0

0

00

Wrote off Customer Account

2017

Aug.

5

Accounts Receivable—Peter Sweet

5

0

0

00

Bad Debts Recovered

5

0

0

00

Reinstate Customer

5

Cash

5

0

0

00

Accounts Receivable—Peter Sweet

5

0

0

00

Collected from Customer

EXERCISES (CONTINUED)

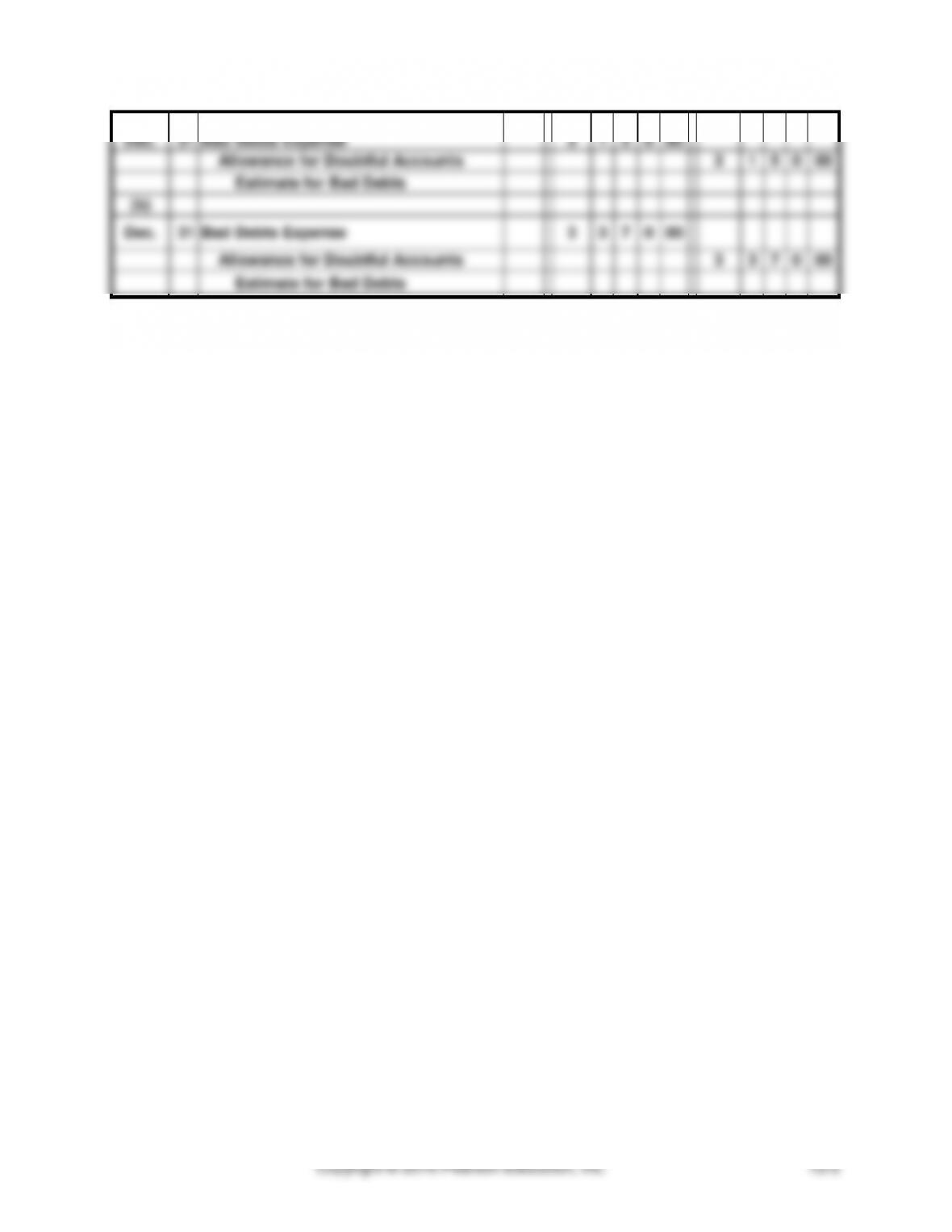

13A-5.

(a)

Dec.

31

Bad Debts Expense

3

1

5

0

00

Allowance for Doubtful Accounts

3

1

5

0

00

Estimate for Bad Debts

(b)

Dec.

31

Bad Debts Expense

3

3

7

0

00

Allowance for Doubtful Accounts

3

3

7

0

00

Estimate for Bad Debts

SOLUTIONS TO SET B EXERCISES

13B-1.

ACORN.COM

PARTIAL BALANCE SHEET

DECEMBER 31, 2015

Current Assets:

Cash

$124

0

0

0

00

Petty Cash

6

8

00

Accounts Receivable

$66

0

0

0

00

Less: Allowance for Doubtful Accounts

13

0

0

0

00

53

0

0

0

00

Merchandise Inventory

15

0

0

0

00

Total Current Assets

$192

0

6

8

00

13B-2.

Dec.

31

Bad Debts Expense

2

8

4

7

30

Allowance for Doubtful Accounts

2

8

4

7

30

Estimate for Bad Debts

13B-3.

Dec.

31

Bad Debts Expense

3

2

0

0

00

Allowance for Doubtful Accounts

3

2

0

0

00

Estimate for Bad Debts

EXERCISES (CONTINUED)

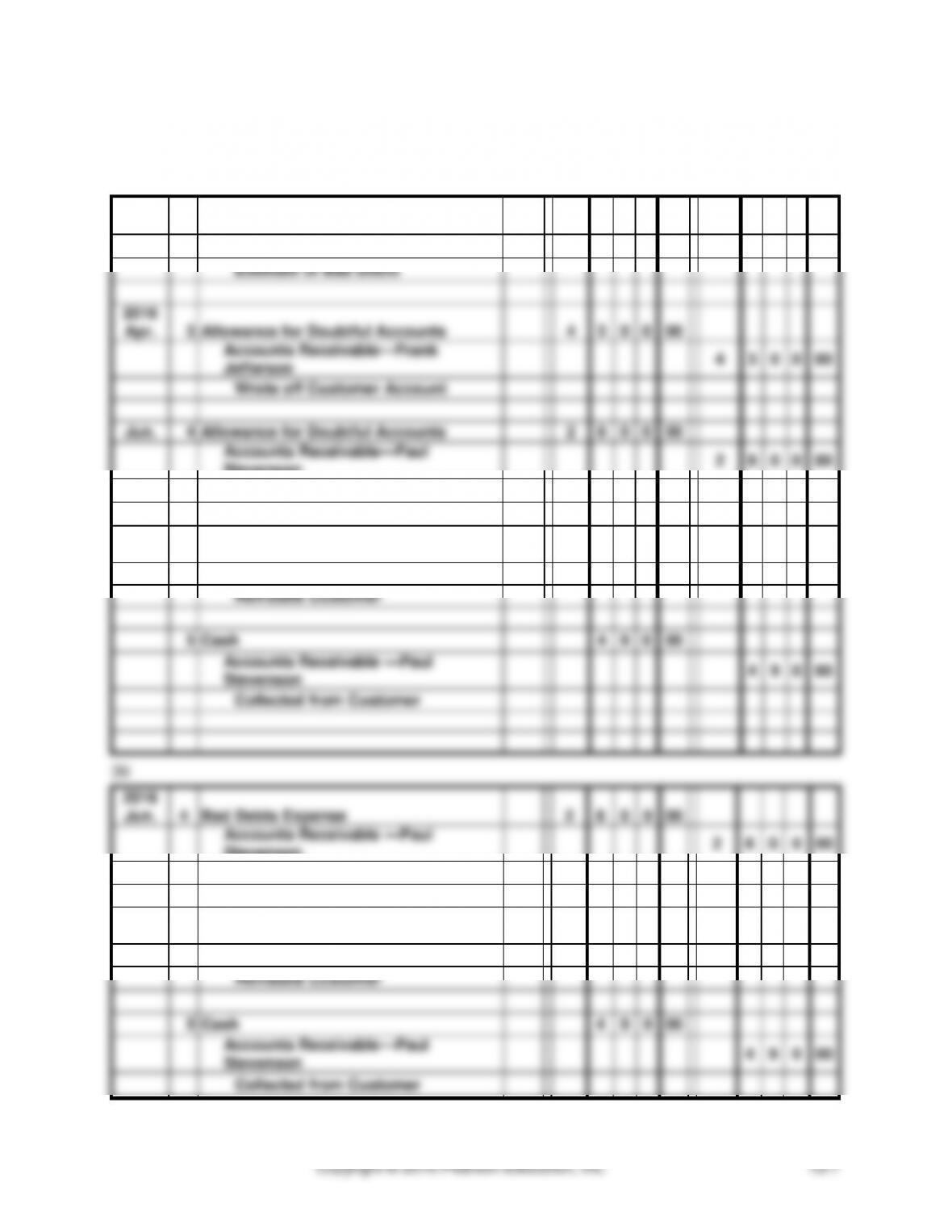

13B-4.

(a)

2015

Dec.

31

Bad Debts Expense

11

6

0

0

00

Allowance for Doubtful Accounts

11

6

0

0

00

Estimate of Bad Debts

2016

Apr.

3

Allowance for Doubtful Accounts

4

3

0

0

00

Accounts Receivable—Frank

Jefferson

4

3

0

0

00

Wrote off Customer Account

Jun.

4

Allowance for Doubtful Accounts

2

8

0

0

00

Accounts Receivable—Paul

Stevenson

2

8

0

0

00

Wrote off Customer Account

2017

Aug.

5

Accounts Receivable —Paul Stevenson

4

9

0

00

Allowance for Doubtful Accounts

4

9

0

00

Reinstate Customer

5

Cash

4

9

0

00

Accounts Receivable —Paul

Stevenson

4

9

0

00

Collected from Customer

(b)

2016

Jun.

4

Bad Debts Expense

2

8

0

0

00

Accounts Receivable —Paul

Stevenson

2

8

0

0

00

Wrote off Customer Account

2017

Aug.

5

Accounts Receivable—Paul Stevenson

4

9

0

00

Bad Debts Recovered

4

9

0

00

Reinstate Customer

5

Cash

4

9

0

00

Accounts Receivable—Paul

Stevenson

4

9

0

00

Collected from Customer

EXERCISES (CONTINUED)

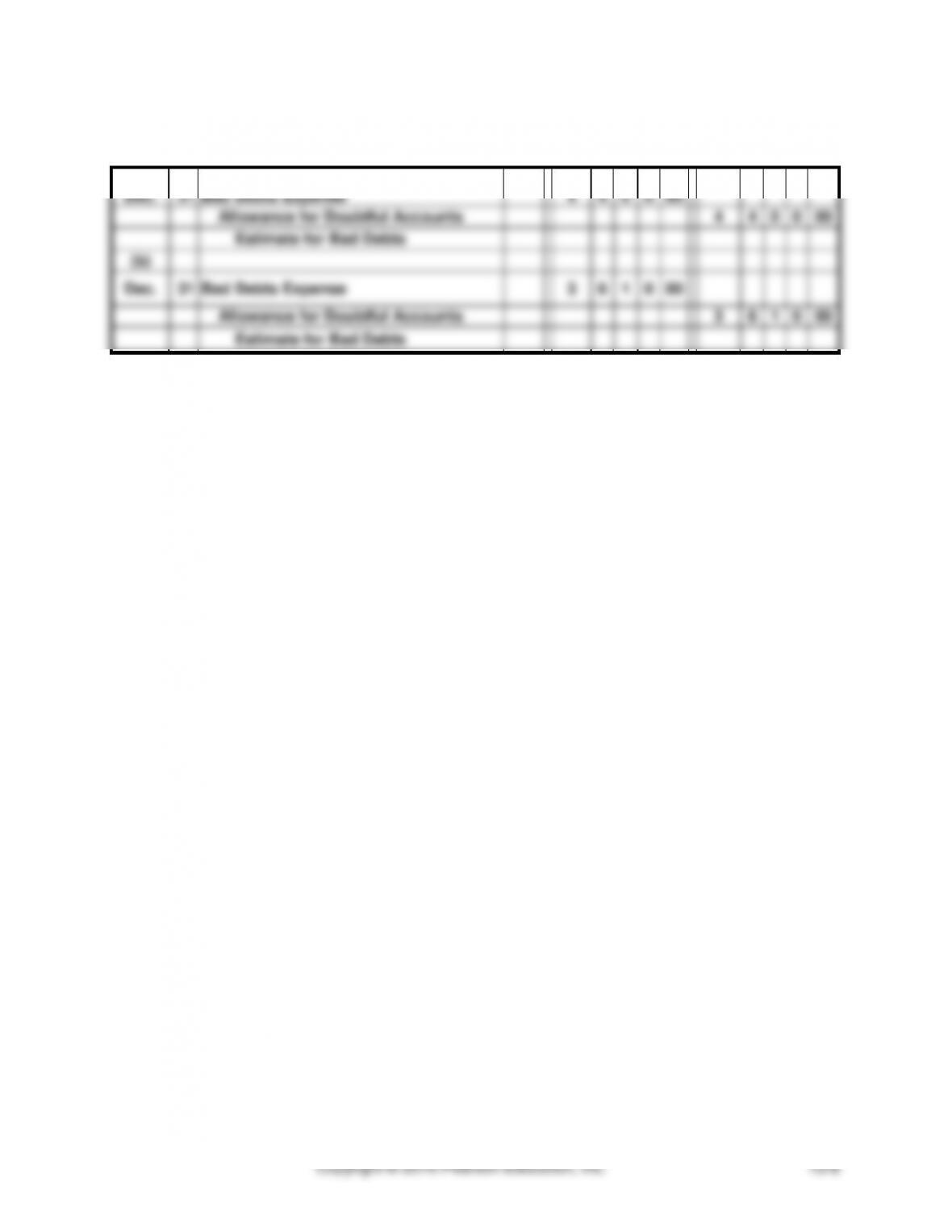

13B–5.

(a)

Dec.

31

Bad Debts Expense

4

4

0

0

00

Allowance for Doubtful Accounts

4

4

0

0

00

Estimate for Bad Debts

(b)

Dec.

31

Bad Debts Expense

3

6

1

0

00

Allowance for Doubtful Accounts

3

6

1

0

00

Estimate for Bad Debts

SOLUTIONS TO SET A PROBLEMS

PROBLEM 13A-1

LAMBERT CO.

GENERAL JOURNAL

PAGE 3

Date

Account Titles and Description

PR

Dr.

Cr.

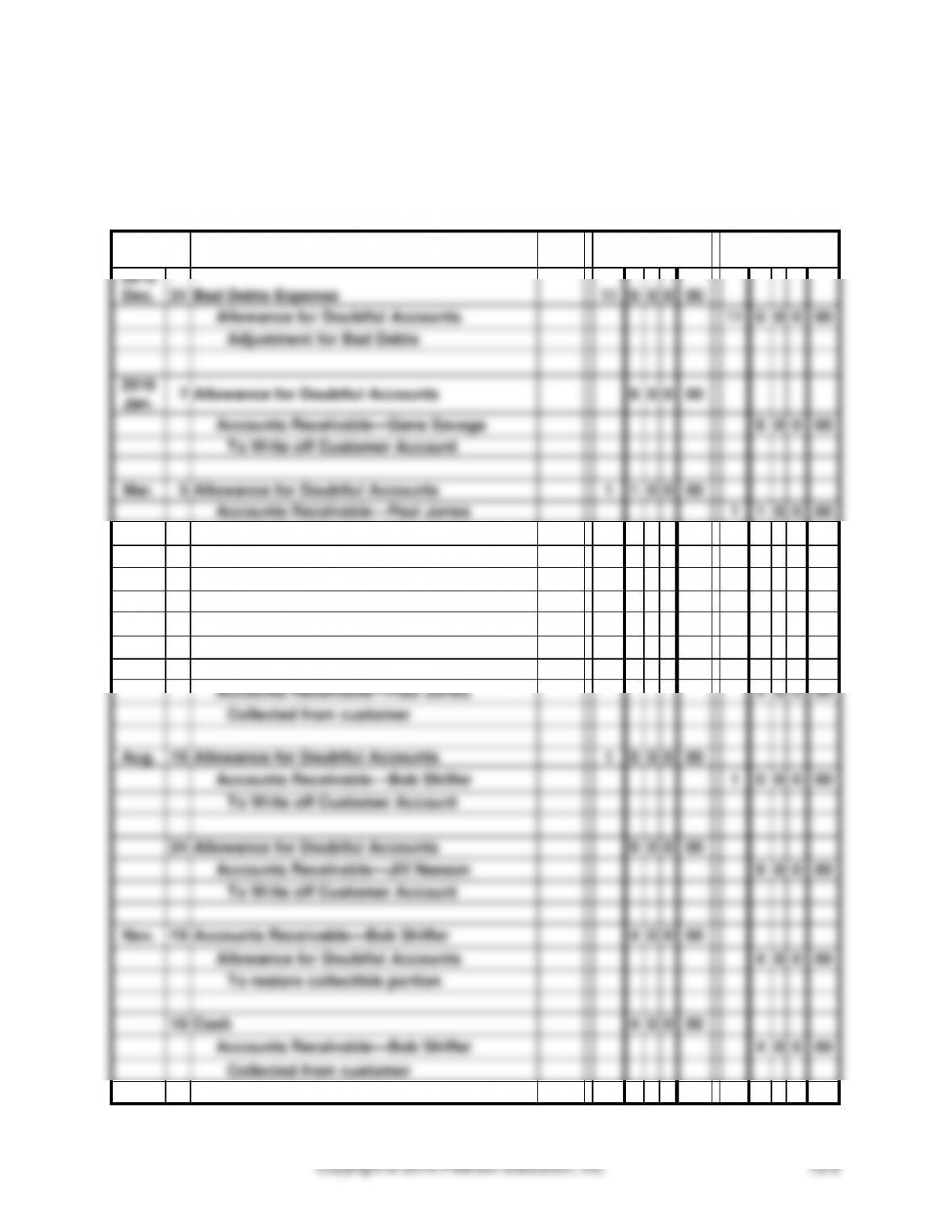

2015

Dec.

31

Bad Debts Expense

11

0

0

0

00

Allowance for Doubtful Accounts

11

0

0

0

00

Adjustment for Bad Debts

2016

Jan.

7

Allowance for Doubtful Accounts

8

0

0

00

Accounts Receivable—Gene Savage

8

0

0

00

To Write off Customer Account

Mar.

5

Allowance for Doubtful Accounts

1

1

0

0

00

Accounts Receivable—Paul Jones

1

1

0

0

00

To Write off Customer Account

Jul.

8

Accounts Receivable—Paul Jones

4

0

0

00

Allowance for Doubtful Accounts

4

0

0

00

To restore collectible portion

8

Cash

4

0

0

00

Accounts Receivable—Paul Jones

4

0

0

00

Collected from customer

Aug.

19

Allowance for Doubtful Accounts

1

0

0

0

00

Accounts Receivable—Bob Shiffer

1

0

0

0

00

To Write off Customer Account

24

Allowance for Doubtful Accounts

9

0

0

00

Accounts Receivable—Jill Neeson

9

0

0

00

To Write off Customer Account

Nov.

19

Accounts Receivable—Bob Shiffer

4

0

0

00

Allowance for Doubtful Accounts

4

0

0

00

To restore collectible portion

19

Cash

4

0

0

00

Accounts Receivable—Bob Shiffer

4

0

0

00

Collected from customer

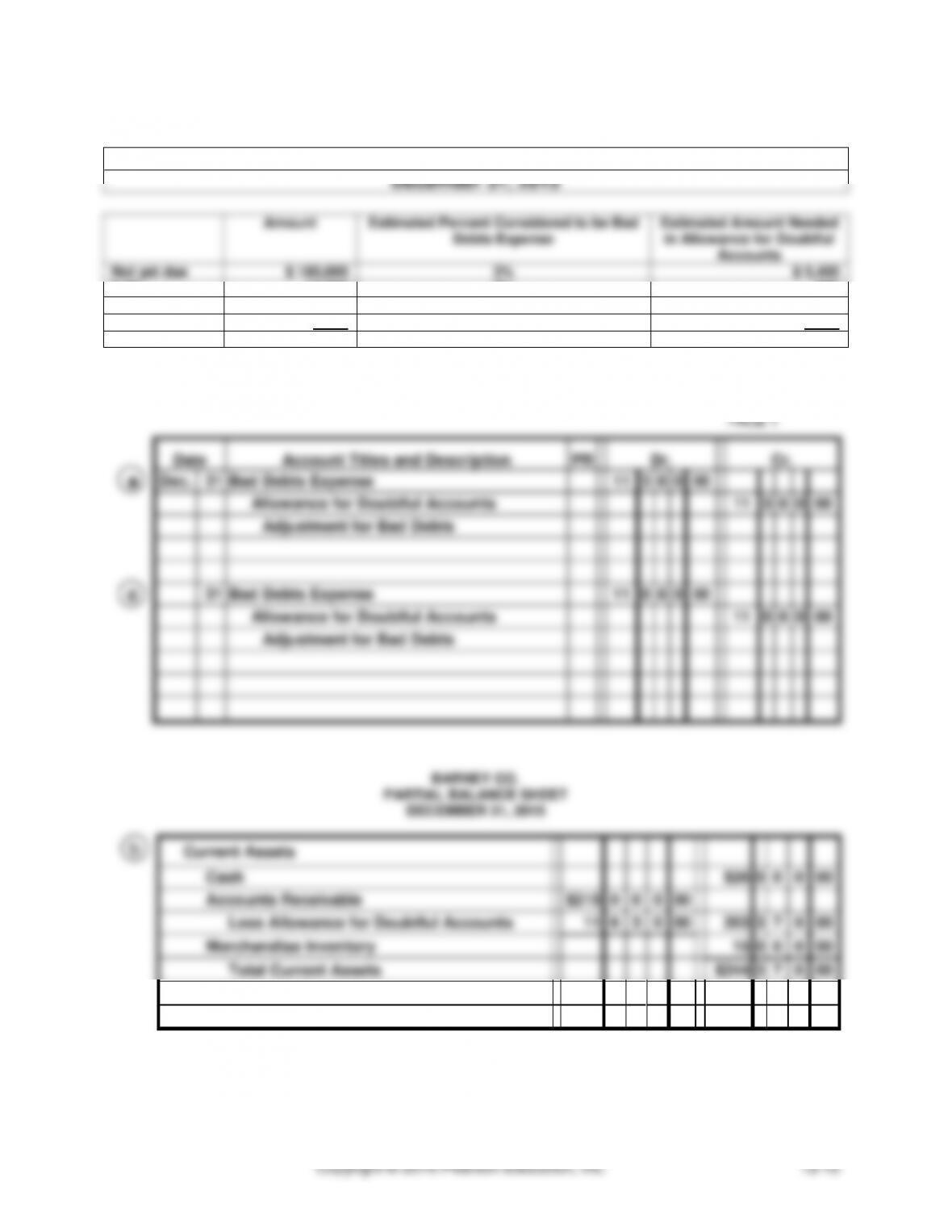

PROBLEM 13A-2

Barney Co.

December 31, 2015

Amount

Estimated Percent Considered to be Bad

Debts Expense

Estimated Amount Needed

in Allowance for Doubtful

Accounts

Not yet due

$ 180,000

3%

$ 5,400

0-60

14,000

7%

980

61–180

12,000

16%

1,920

Over 6 months

9,000

37%

3,330

$ 215,000

$ 11,630

BARNEY CO.

GENERAL JOURNAL