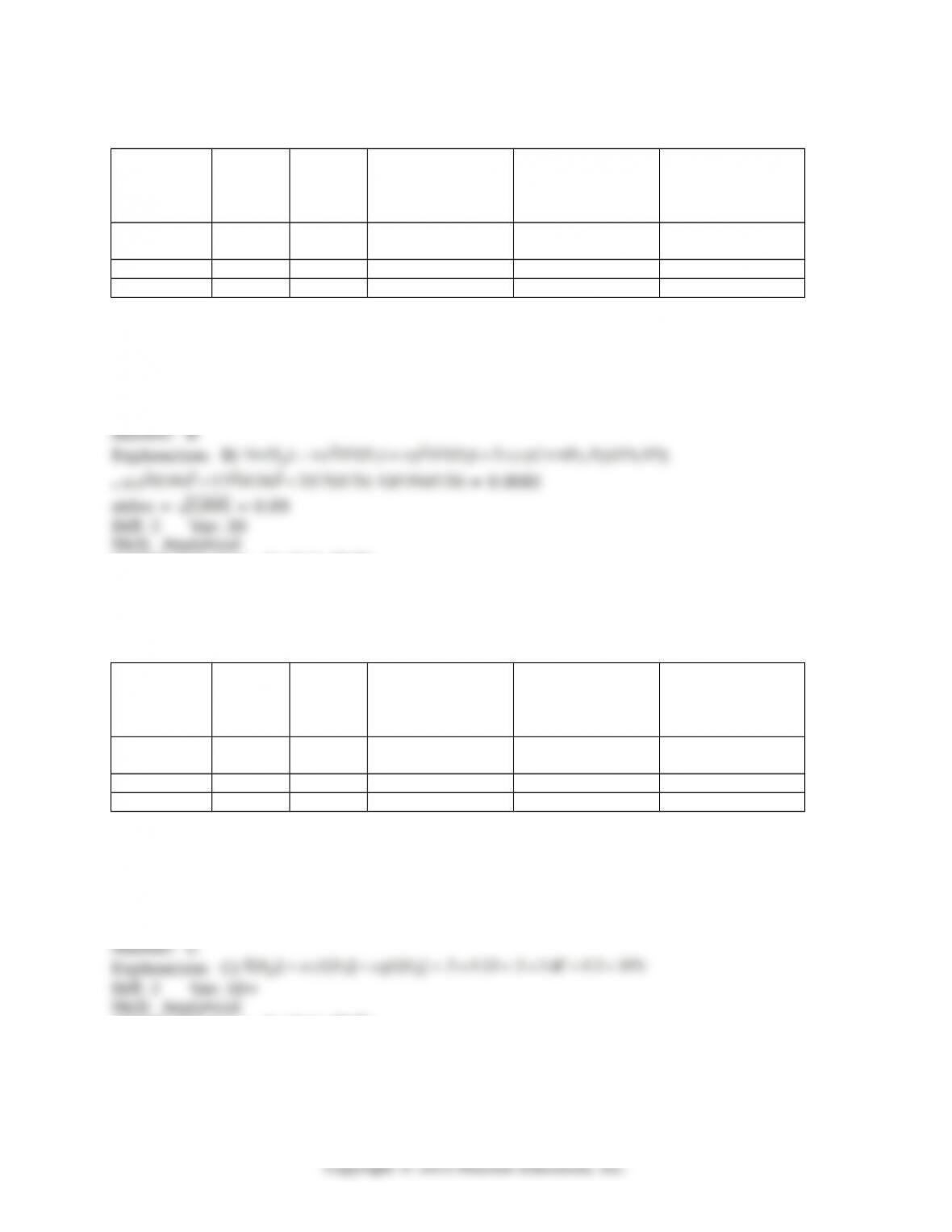

24) Consider the following returns:

Year-End

Lowes

Realized

Return

Home Depot

Realized

Return

IBM

Realized

Return

2000 20.3% -14.6% 0.2%

2001 72.7% 4.8% -3.2%

2002 -25.7% -58.1% -27.0%

2003 56.3% 71.7% 27.9%

2004 6.7% 17.3% -5.1%

2005 17.9% 0.9% -11.3%

The volatility on Home Depot’s returns is closest to ________.

A) 35%

B) 32%

C) 42%

D) 17%

AACSB Objective: Analytic Skills

Author: JN

Question Status: Revised

21

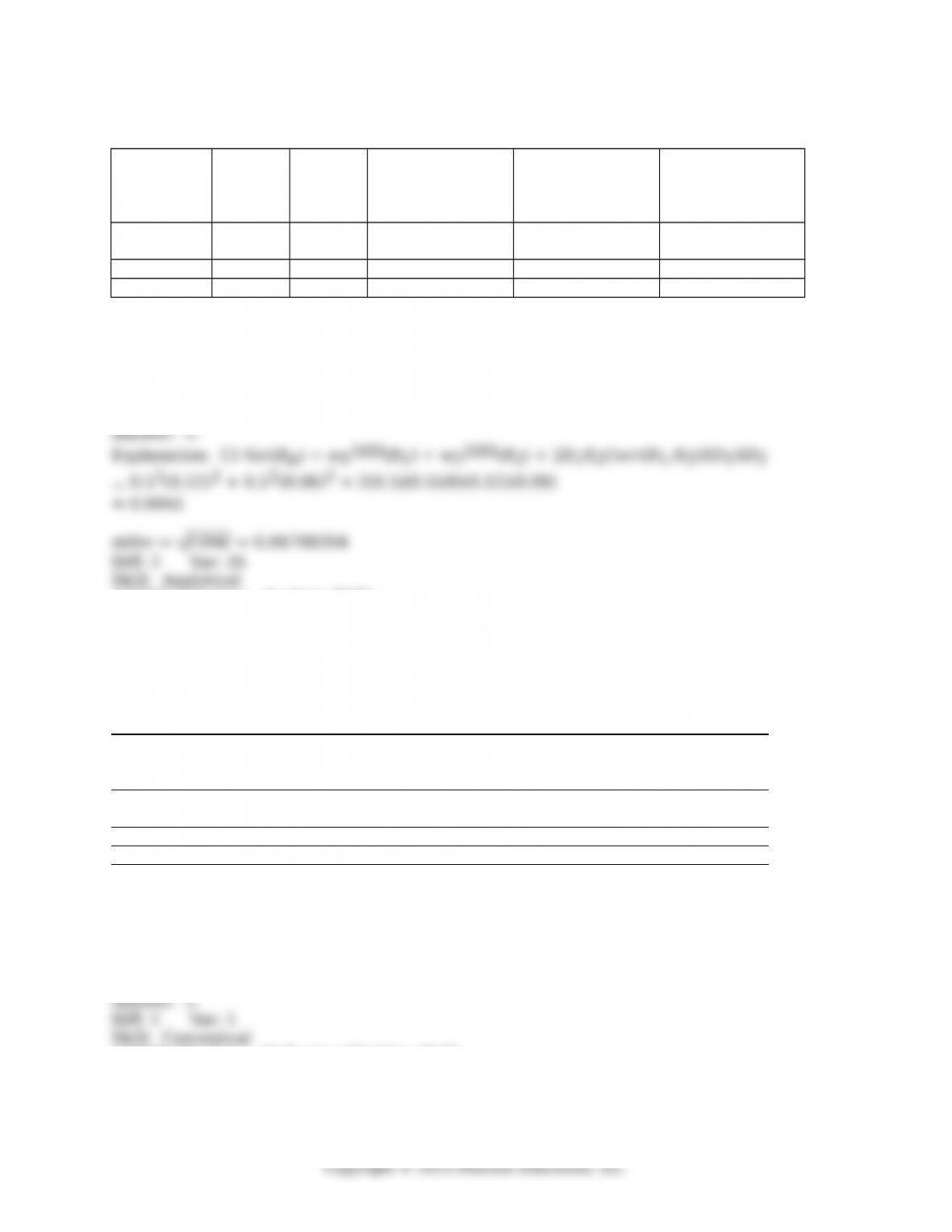

25) Consider the following expected returns, volatilities, and correlations:

Stock

Expecte

d

Return

Standar

d

Deviatio

n

Correlation with

Duke Energy

Correlation with

Microsoft

Correlation with

Wal-Mart

Duke

Energy 14% 6% 1.0 -1.0 0.0

Microsoft 44% 24% -1.0 1.0 0.7

Wal-Mart 23% 14% 0.0 0.7 1.0

The volatility of a portfolio that is equally invested in Duke Energy and Microsoft is closest

to ________.

A) 8.1%

B) 9.0%

C) 10.8%

D) 5.4%

AACSB Objective: Analytic Skills

Author: JN

Question Status: Previous Edition

26) Consider the following expected returns, volatilities, and correlations:

Stock

Expecte

d

Return

Standar

d

Deviatio

n

Correlation with

Duke Energy

Correlation with

Microsoft

Correlation with

Wal-Mart

Duke

Energy 13% 6% 1.0 -1.0 0.0

Microsoft 47% 24% -1.0 1.0 0.7

Wal-Mart 23% 14% 0.0 0.7 1.0

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is

closest to ________.

A) 15%

B) 14%

C) 30%

D) 45%

AACSB Objective: Analytic Skills

Author: JP

Question Status: New

22

27) Consider the following expected returns, volatilities, and correlations:

Stock

Expecte

d

Return

Standar

d

Deviatio

n

Correlation with

Duke Energy

Correlation with

Microsoft

Correlation with

Wal-Mart

Duke

Energy 14% 6% 1.0 -1.0 0.0

Microsoft 44% 24% -1.0 1.0 0.7

Wal-Mart 23% 12% 0.0 0.7 1.0

The volatility of a portfolio that is equally invested in Wal-Mart and Duke Energy is closest

to ________.

A) 4.0%

B) 0.7%

C) 6.7%

D) 20.1%

AACSB Objective: Analytic Skills

Author: JP

Question Status: Revised

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

Stock

Expected

Return

Standard

Deviation

Correlation

with Duke

Energy

Correlation

with

Microsoft

Correlation

with Wal-Mart

Duke

Energy 14% 6% 1.0 -1.0 0.0

Microsoft 44% 24% -1.0 1.0 0.7

Wal-Mart 23% 14% 0.0 0.7 1.0

28) Which of the following combinations of two stocks would give you the biggest reduction

in risk?

A) Duke Energy and Wal-Mart

B) Wal-Mart and Microsoft

C) Microsoft and Duke Energy

D) No combination will reduce risk.

AACSB Objective: Relective Thinking Skills

Author: JP

Question Status: New

29) What diversiication, if any, is achieved if two stocks in a portfolio are perfectly

23

positively correlated?

AACSB Objective: Analytic Skills

Author: SS

Question Status: Previous Edition

30) What is the lowest risk possible by selecting two stocks that are perfectly negatively

correlated?

AACSB Objective: Relective Thinking Skills

Author: SS

Question Status: Previous Edition

12.3 Measuring Systematic Risk

1) If you build a large enough portfolio, you can diversify away all the risks of a portfolio.

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

2) A stock market comprises 4600 shares of stock A and 2000 shares of stock B. Assume

the share prices for stocks A and B are $25 and $35, respectively. What is the capitalization

of the market portfolio?

A) $185,000

B) $157,250

C) $175,750

D) $203,500

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

24

3) A stock market comprises 4700 shares of stock A and 2300 shares of stock B. Assume

the share prices for stocks A and B are $25 and $30, respectively. What proportion of the

market portfolio is comprised of stock A?

A) 63.0%

B) 62.0%

C) 61.3%

D) 79%

AACSB Objective: Analytic Skills

Author: JP

Question Status: Revised

4) A stock market comprises 2400 shares of stock A and 2400 shares of stock B. The share

prices for stocks A and B are $15 and $5, respectively. What is the capitalization of the

market portfolio?

A) $43,200

B) $48,000

C) $55,200

D) $52,800

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

25

5) A stock market comprises 2100 shares of stock A and 2100 shares of stock B. The share

prices for stocks A and B are $25 and $15, respectively. What proportion of the market

portfolio is comprised of each stock?

A) Stock A is 62.5% and Stock B is 37.5%.

B) Stock A is 37.5% and Stock B is 62.5%.

C) Stock A is 50% and Stock B is 50%.

D) Stock A is 200% and Stock B is 100%.

AACSB Objective: Analytic Skills

Author: JP

Question Status: Previous Edition

6) A stock market comprises 1500 shares of stock A and 3000 shares of stock B. The share

prices for stocks A and B are $24 and $34, respectively. What is the capitalization of the

market portfolio?

A) $138,000

B) $117,300

C) $110,400

D) $151,800

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

7) You expect General Motors (GM) to have a beta of 1.3 over the next year and the beta of

Exxon Mobil (XOM) to be 0.9 over the next year. Also, you expect the volatility of General

Motors to be 40% and that of Exxon Mobil to be 30% over the next year. Which stock has

more systematic risk? Which stock has more total risk?

A) XOM, GM

B) XOM, XOM

C) GM, XOM

D) GM, GM

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

26

8) You expect General Motors (GM) to have a beta of 1 over the next year and the beta of

Exxon Mobil (XOM) to be 1.2 over the next year. Also, you expect the volatility of General

Motors to be 30% and that of Exxon Mobil to be 40% over the next year. Which stock has

more systematic risk? Which stock has more total risk?

A) GM, GM

B) GM, XOM

C) XOM, XOM

D) XOM, GM

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

9) You expect General Motors (GM) to have a beta of 1.5 over the next year and the beta of

Exxon Mobil (XOM) to be 1.9 over the next year. Also, you expect the volatility of General

Motors to be 50% and that of Exxon Mobil to be 35% over the next year. Which stock has

more systematic risk? Which stock has more total risk?

A) XOM, GM

B) GM, XOM

C) GM, GM

D) XOM, XOM

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

10) The amount of a stock’s risk that is diversiied away ________.

A) is independent of the portfolio that you add it to

B) depends on market risk premium

C) depends on risk-free rate of interest

D) depends on the portfolio that you add it to

AACSB Objective: Analytic Skills

Author: KB

Question Status: Revised

27

11) If you build a large enough portfolio, you can diversify away all ________ risk, but you

will be left with ________ risk.

A) diversiiable, unsystematic

B) unsystematic, systematic

C) systematic, undiversiiable

D) undiversiiable, diversiiable

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

12) The market portfolio is the portfolio of all risky investments held ________.

A) in descending weights

B) in ascending weights

C) in proportion to their value

D) based on previous year performance

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

13) The S&P 500 index traditionally is a(n) ________ portfolio of the 500 largest U.S. stocks.

A) value weighted

B) equally weighted

C) chain weighted

D) price weighted

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

28

14) For each 1% change in the market portfolio’s excess return, the investment’s excess

return is expected to change by ________ due to risks that it has in common with the

market.

A) beta

B) alpha

C) 0%

D) 1%

AACSB Objective: Analytic Skills

Author: KB

Question Status: Revised

15) The beta of the market portfolio is ________.

A) 0

B) -1

C) 2

D) 1

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

16) Companies that sell household products and food have very little relation to the state of

the economy because such basic needs do not go away. These stocks tend to have ________

betas.

A) high

B) low

C) negative

D) ininite

AACSB Objective: Analytic Skills

Author: KB

Question Status: Revised

29

17) A linear regression to estimate the relation between General Motors’ stock returns and

the market’s return gives the best itting line that represents the relation between the

stock and the market. The slope of this line is our estimate of ________.

A) alpha

B) beta

C) risk-free rate

D) volatility

AACSB Objective: Analytic Skills

Author: KB

Question Status: Previous Edition

18) A linear regression was done to estimate the relation between Sprint’s stock returns

and the market’s return. The intercept of the line was found to be 0.23 and the slope was

1.47. Which of the following statements is true regarding Sprint’s stock?

A) Sprint’s beta is 0.23.

B) Sprint’s beta is 1.47.

C) The risk-free rate is 1.47%.

D) The standard deviation of Sprint’s excess returns is 23%.

AACSB Objective: Analytic Skills

Author: JP

Question Status: Previous Edition

19) You observe that AT&T stock and the S&P 500 have the following weekly returns:

Week AT&T return S&P 500 return

1 0.005 0.001

2 0.010 0.005

3 -0.003 -0.005

4 -0.005 -0.001

If this pattern of stock returns is typical of AT&T stock, and you calculated a beta against

the S&P 500, which of the following is true?

A) AT&T’s beta is negative.

B) AT&T’s beta is zero.

C) AT&T’s beta is positive.

D) Cannot be determined from information given.

AACSB Objective: Analytic Skills

Author: JP

Question Status: Previous Edition

20) Which of the following statements is FALSE?

A) We say a portfolio is an eicient portfolio whenever it is possible to ind another portfolio

that is better in terms of both expected return and volatility.

B) We can rule out ineicient portfolios because they represent inferior investment choices.

C) The volatility of the portfolio will difer, depending on the correlation between the

securities in the portfolio.

D) Correlation has no efect on the expected return on a portfolio.