Questions & Answers:

Chapter 1 – Overview of Investment Banking

Q1. What were the two main arguments for rejoining investment banks

and retail deposit-taking banks that led to the passing of the

Gramm-Leach-Bliley Act?

Q2. Describe the three principal businesses of an investment bank.

Q3. Why might a universal bank be better able to compete against a

pure-play investment bank for M&A and other investment banking

engagements?

Q4. Investment bank clients can be categorized into two broad groups

of issuers and investors. These two groups often have competing

objectives (issue equity at highest possible price vs. acquire stock in

companies at lowest possible price). Who within the investment

bank is responsible for balancing these competing interests?

Q5. What is a key consideration in determining the cost and other

parameters of a corporate debt offering and why is it important?

Q6. Why might an investment bank place higher priority on sell-side

M&A engagements over buy-side engagements?

Q7. What is two key considerations for bankers in the debt capital

markets division when working with an issuer on an offering?

Q8. De!ne proprietary trading.

Q9. What conflict might exist between a proprietary trading business

and the rest of the investment bank?

Q10. What conflict might exist as a result of having both an Asset

Management business and a Private Wealth Management business?

Q1. Following the 1929 Stock market crash, Congress passed a series of

Acts to regulate the securities industries. Name four of these Acts

and brie6y describe their purpose.

Q2. A goal of many parts of U.S. regulatory legislation has been to

eliminate/minimize conflict of interest between issuers, investment

banks, and investors. Provide examples of conflict of interest in

the U.S. investment banking industry and the corresponding

regulations that attempted to resolve those issues.

Q3. Disclosure of information to investors is another recurring theme in

U.S. regulation of the securities industry. Provide examples of

disclosure required by U.S. regulations.

Q4. What is the role of states in the U.S. in regulating investment

banks?

Q5. What type of U.S. securities offerings do not need to be registered

with the SEC?

Q6. What is a “Red Herring”?

Q7. Before an SEC registration statement is declared effective,

companies (or their underwriters) that sell stock or are deemed to

be promoting the sale of stock have a securities law problem. What

is this problem called and what are its consequences?

Q8. What are the “Risk Factors” in a prospectus? Why are they

important to the issuer and to the investor?

Q9. What is the signi!cance of the Gramm-Leach-Bliley Act of 1999 in

relation to the securities industry?

Q10. What are some securities regulations in place in the U.K., Japan and

China that mirror U.S. regulations?

Q11. What are some major differences between the regulatory

frameworks of the four countries covered in this chapter?

Q12. Compare the regulatory bodies of the four countries covered in this

chapter.

Q13. What does the Dodd-Frank Act of 2010 mainly focus on?

Q1. What type of securities offerings do not need to be registered with

the SEC?

Q2. List the three types of bank participants in an underwriting

syndicate and their core responsibilities, in order of compensation

received, from high to low.

Q3. What are league tables and why are league tables important in

investment banking?

Q4. Describe the function of the equity capital markets group, including

the two major divisions they directly work with and the two types of

clients they indirectly work with.

Q5. Describe the unique process utilized by Google in its IPO, intended

advantages and potential disadvantages.

Q6. What is a shelf registration statement and what securities can be

included in it?

Q7. Why might a younger high-tech company select equity over debt

when raising capital?

Q8. A BBB-/Baa3 rated company is looking at acquiring a smaller (but

sizeable) competitor. Discuss considerations the company should

take into account when deciding whether to fund the acquisition

with new debt, equity, or convertible securities.

Q9. Suppose a company issues a $180 million convertible bond when its

stock is trading at $30. Assuming it is convertible into 5 million

shares, what is the conversion premium of the convertible?

Q10. How many shares will be issued by a convertible issuer if conversion

occurs for a $200 million convertible with a conversion premium of

20%, which is issued when the issuer’s stock price is $25? (show

your calculation).

Q11. Why did the SEC delay declaring Google’s IPO registration effective?

Q12. Provide seven reasons that an investment bank might give to

support their advice that a private company should “go public”.

Q13. List six characteristics of companies that are good targets for an

equity issuance.

Q14. How does a negotiated (best effort) transaction differ from a

“bought deal”?

Q15. What are some methods used by investment banks to help equity

issuers mitigate price risk during the marketing process?

Q16. Explain what a “green shoe” is.

Q17. When a company has agreed to a green shoe, who does the

underwriter buy shares from if the share price drops? Who do they

buy shares from if the share price increases?

Q18. Calculate the investment bank’s fees and pro!t for a 5 million share

equity offering at $40/share, with a 15% green shoe option (fully

exercised) assuming a 2% gross spread, assuming the issuer’s share

price decreases to $38/share after the offering.

Q19. What is the tradeo1 for having a stabilizing green shoe option in a

common equity offering?

Q1. Provide de!nitions for strategic buyers and !nancial buyers in a

prospective M&A transaction.

Q2. Why have strategic buyers traditionally been able to out bid

!nancial buyers in auctions?

Q3. Why are revenue synergies typically given less weight than cost

synergies when evaluating the combination bene!ts of a

transaction?

Q4. In the U.S., if an M&A transaction is relatively large within its

industry, what is the name of the regulatory !ling that is probably

necessary before the transaction can be consummated? Which

agency is it !led with? How long is the waiting period after a !ling

is made? What is the name of the European regulator that may be

relevant in an M&A transaction?

Q5. Assume an acquiring company’s P/E is 15x and the target

company’s P/E is 11x. Is the acquirer more or less likely to use

stock as the acquisition currency? Why?

Q6. What is a potential risk of trying to complete a stock-based

acquisition during periods of high market volatility?

Q7. Assume an investment bank has provided a fairness opinion on a

proposed M&A transaction. Does this mean the board should go

ahead and approve the transaction?

Q8. Why might a board want to include a “go-shop” provision in the

merger/purchase agreement?

Q9. When is a break-up fee paid? What is the normal fee as a percent of

equity value?

Q10. Under what circumstances would an investment bank hold a public

auction in an attempt to help sell a company?

Q11. List the four principal alternative methods for establishing value in

an M&A transaction.

Q12. Of the major valuation methods which one(s) are based on relative

values? …on intrinsic values? …on ability to pay?

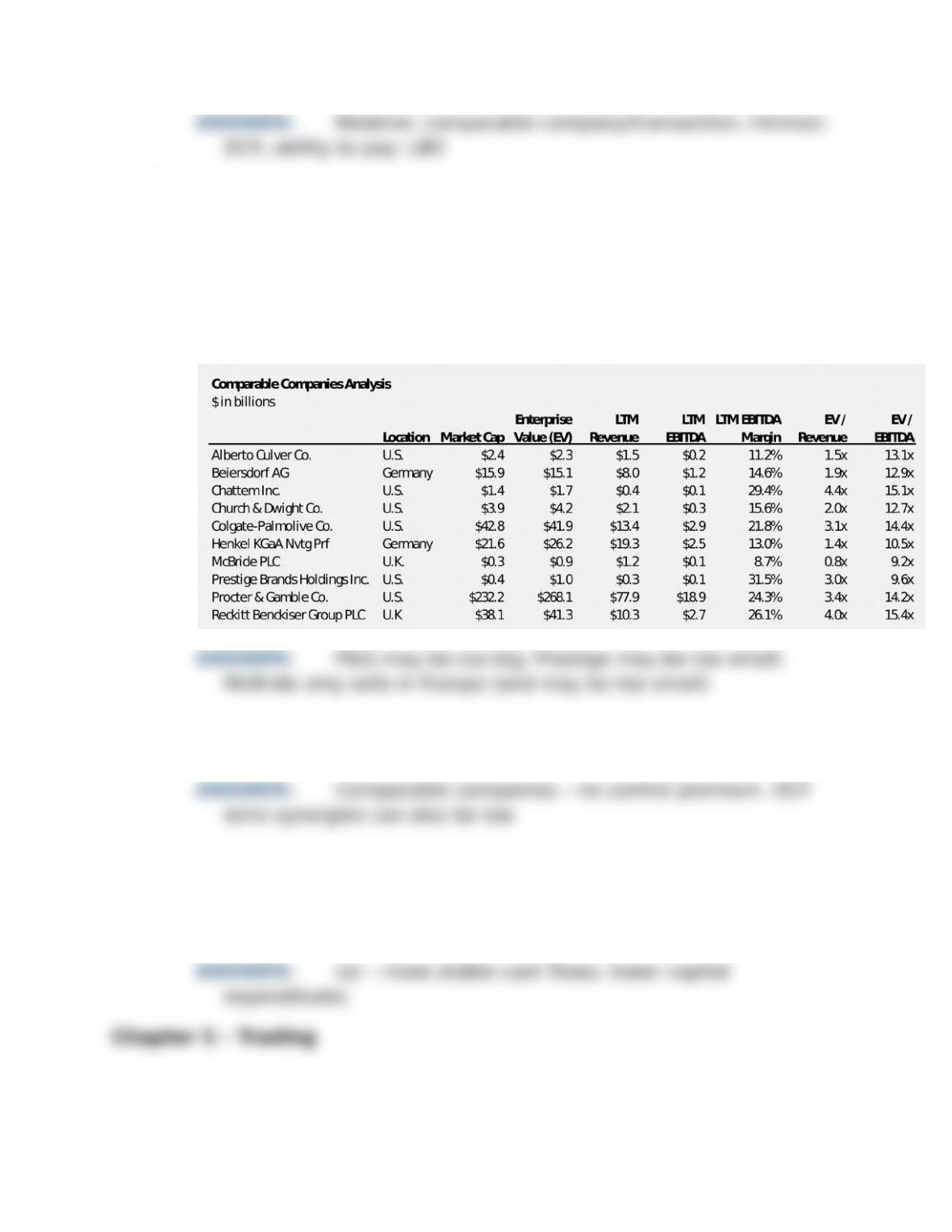

Q13. Suppose you are the sell-side advisor for a multinational household

and personal products manufacturer and marketer that sells

primarily to the mass consumer markets. The analyst on your deal

team prepares the following comparable companies analysis.

Which, if any, of the companies in the list would you potentially

remove from the analysis?

Q14. Which valuation method tends to show the lowest valuation range?

Why?

Q15. Which of the following companies would make a better LBO target,

and why? (a) a diversi!ed manufacturer of consumer snack

products or (b) a manufacturer of factory automation equipment for

car makers, agricultural equipment and other heavy machinery.

Q1. When might an investment bank decline participation in an

underwriting and why?

Q2. How do professionals in sales, trading and research work together?

Q3. Describe what Prime Brokerage is, including four principal products

in this area and the generic name of the !nancial institutions that

are targeted for this business.

Q4. Explain traders’ market-making function.

Q5. Why would a prospective issuer prefer to hire as underwriter an

investment bank that has traders already active in its security?

Q6. FICC is one of the main Divisions in an Investment Bank. What

does FICC stand for? Other than during 2007 and 2008, how does

this division typically rank from a pro!tability point of view,

compared to other Divisions? What happened during these two

years and which part of the FICC Division was most responsible for

this outcome?

Q7. Why might a high short interest ratio be potentially misleading with

respect to the opinions of market participants regarding a particular

stock?

Q8. An investor lends 10,000 shares of ABC for two months when the

stock is at $50 and requires 102% cash collateral. The market

interest on cash collateral is 4.0%. The rebate rate on ABC shares is

2.5%. Calculate the combined pro!t for the stock lender and

investment bank.

Q9. What risks do investors take on when buying on margin?

Q10. How were senior tranches of a CDO able to obtain investment grade

credit ratings when some of the underlying assets were non-

investment grade?

Q11. A domestic airline based in the U.S. has placed a large $10 billion

order for new airplanes with French aircraft manufacturer Airbus.

Delivery is scheduled in four years. Payments are staggered based

on a percentage of completion rate. The U.S. airline believes the

Euro will appreciate against the Dollar during this time frame. How

can the U.S. airline hedge currency risk related to this purchase with

an investment bank?

Q12. What does VaR stand for? What is its de!nition and why is it

important to investment banks? What are some of the criticisms of

VaR?

Q1. What is the difference between asset management and wealth

management?

Q2. Why would a wealth manager choose to allocate some of a client’s

asset to another bank?

Q3. How are the different functions of the sell-side versus the buy-side

manifested through their fee structures?

Q4. What drove the need to separate research and investment banking?

Q5. How have the U.S. enforcement actions against sell-side research in

2003 heightened the issue of declining research revenues?

Q6. What are the objectives of Regulation FD? What are the concerns

about this U.S.-based regulation?

Q1. Compare the different roles provided to the investor community by

credit rating analysts and sell-side research analysts.

Q2. What is the difference between business risk and !nancial risk?

Q3. What are the major criticisms directed at Moody’s, Standard &

Poor’s and Fitch?

Q4. How have recent modernizations by the NYSE helped eliminate the

problem of front running?

Q5. Why might OTC derivatives be considered more risky than

exchange-traded derivatives?

Q6. How is derivatives settlement different from securities settlement?

Q7. What steps have U.S. regulators taken to reduce the systemic risk

associated with OTC derivatives?

Q1. What are the bene!ts of issuing Eurobonds? Investing in

Eurobonds?

Q2. Why are most corporate Eurobond issuers large, multinational

corporations?

Q3. How has recent legislation accelerated the development of the

Japanese M&A market?

Q4. How has the Chinese government’s relaxation of its foreign

exchange controls helped facilitate growth in the Chinese economy?

Q5. In a comparable transactions analysis, what additional

considerations might an investment banker factor in when valuing

an emerging market company?

Q6. Suppose you are a wealth advisor and a client has asked for your

recommendation on which of the BRIC countries poses the least risk

and most opportunity for investment growth. Brie6y compare the

perceived risks and bene!ts of each of the countries and provide

support for your selection.

Q1. After an initial hedge is in place, what do hedge fund investors in

convertible bonds do with shares of the underlying stock when the

stock price increases or decreases?

Q2. True or false (and explain your answer): Convertible arbitrage hedge

funds invest in convertible bonds because the fund managers have

a bullish view on the company’s stock.

Q3. Assume Hedge Fund A purchases a portion of Company B’s

convertible and will execute a delta hedge strategy. Describe the

steps Hedge Fund A will take in the event the price of Company B’s

shares fall, and explain the reasoning behind each action.

Q4. If company A and B are identical in every respect except B has

higher stock price volatility, which company would likely achieve

better convertible pricing? Assuming convertibles issued by A and B

have the same terms except for conversion price, would the

company you selected above have a higher or lower conversion

price?

Q5. WheelCo is raising $200 million via a mandatory convertible bond

issuance. Assuming the company’s share price on the date of

issuance is $20 and the convertible bond carries a 25% conversion

premium, what is the number of shares WheelCo has to deliver to

investors if its share price at maturity is (a) $19; (b) $22, (c) $26,

and (d) $30?

Q6. Suppose you are a current shareholder in a company that is

contemplating capital raising alternatives. Assuming the

transaction would have no negative credit repercussions and you

want minimal EPS dilution, rank the following types of convertibles

from least potential for dilution to most potential for dilution:

coupon-paying convertible, mandatory convertible, zero coupon

convertible.

Q7. A U.S.-based BBB-rated company is looking to make a large

acquisition. Management believes synergies from the acquisition

will create new market opportunities. Unfortunately, these new

opportunities will take a few years to realize and until then, bene!ts

will not be fully re6ected in the company’s stock price. If the

company has rating agency concerns and wants tax deductions

from interest payments, what type of security is this company likely

to issue in support of its acquisition and why?

Q8. Why was the Nikkei Put Warrant program so pro!table for Goldman

Sachs?

Q9. What is ASR an abbreviation for? Describe this transaction and the

principal bene!t for a client? What additional bene!t did IBM

achieve in their ASR?

Q10. Assume a company’s ADTV is 240,000 shares. How many days

would it take to complete a 10.8 million share repurchase program?

The company has 120 million shares outstanding and its estimated

EPS for the current !scal year is $3.40. Assuming the company

meets its earnings estimate, what would year-end EPS be under an

ASR program for the full 10.8 million shares, assuming it is executed

20 business days before the company’s !scal year end? Under an

open market repurchase program?

Q1. What are core differences between Investment Banking and Sales &

Trading career paths?

Q2. Describe what a “Chinese Wall” is, which U.S. regulator would be

concerned with issues involving the wall and what is meant by being

brought “over-the-wall”.

Q3. Describe the bene!ts and risks of mortgage securitization.

Q4. Describe a Credit Default Swap. What are regulators trying to do to

mitigate risk in the CDS market?

Q5. Describe the risks associated with bridge loans extended by

Investment Banks

Q6. Discuss how CDS can be used for hedging and speculative

purposes.

Q7. Describe the areas that !xed income sales focuses on.

Q1. Unlike most mutual funds, why are hedge funds able to charge

performance fees on top of management fees?

Q2. Describe side pockets.

Q3. Where does the name “hedge funds” come from?

Q4. Describe two types of direct leverage employed by hedge funds.

Q5. Describe a margin loan.

Q6. Why is it especially important to adjust hedge fund returns data for

survivorship bias?

Q7. Discuss why hedge funds may or may not welcome investment by

fund of funds?

Q8. What are some positive consequences resulting from the

proliferation of hedge funds?

Q9. What are some unforeseen consequences resulting from the

proliferation of hedge funds?

Q10. Discuss the dangers of asset/liability mismatch. What are some

strategies hedge funds employ to mitigate this issue?

Q11. What differences between the hedge fund industry and the mutual

fund industry led to the creation of fund of hedge funds, but not

fund of mutual funds?

Q12. Although hedge funds are less regulated than mutual funds, what

type of indirect regulation affects the hedge fund industry?

Q13. What are the three key bene!ts touted by fund of funds? Do you

think that fund of funds usually achieve these bene!ts? Why or why

not?

Q1. During a !nancial crisis, the yield curve 6attens and the yield on the

30-year Treasury bond reached a new low. As a hedge fund

manager, suppose you think the market has overreacted and will

eventually correct itself, leading to a steepening in the yield curve.

What trades might you execute in a long/short strategy to take

advantage of the situation?

Q2. Describe how overall risk is determined in an equity long/short

investing strategy.

Q3. Precious metals such as gold and silver experienced signi!cant

gains during the !nancial crisis as investors purchased tangible

assets that have more perceived value stability. You notice that a

gold/silver precious metals closed end fund is trading at an

historically high premium relative to its net asset value, what trade

might you employ to take advantage of the situation (assuming you

believe the worst is over).

Q4. ABC and DEF operate in the same industry and you have just

attended a trade show where they have unveiled their new product

lines which are coming out this month. ABC‘s offering looks like a

winner whereas you have serious doubts about DEF’s new products.

ABC and DEF both trade at $50 per share. ABC 1 year $50 calls

trade at $3 and DEF 1 year $50 calls trade at $4. ABC 1 year $50

puts trade at $3.50 and DEF 1 year $50 puts trade at $3.50. Interest

rates are 2%. Neither ABC nor DEF pay dividends nor are expected

to pay dividends in the coming years. As a long/short hedge fund

investor, what options trade should you execute in this scenario?

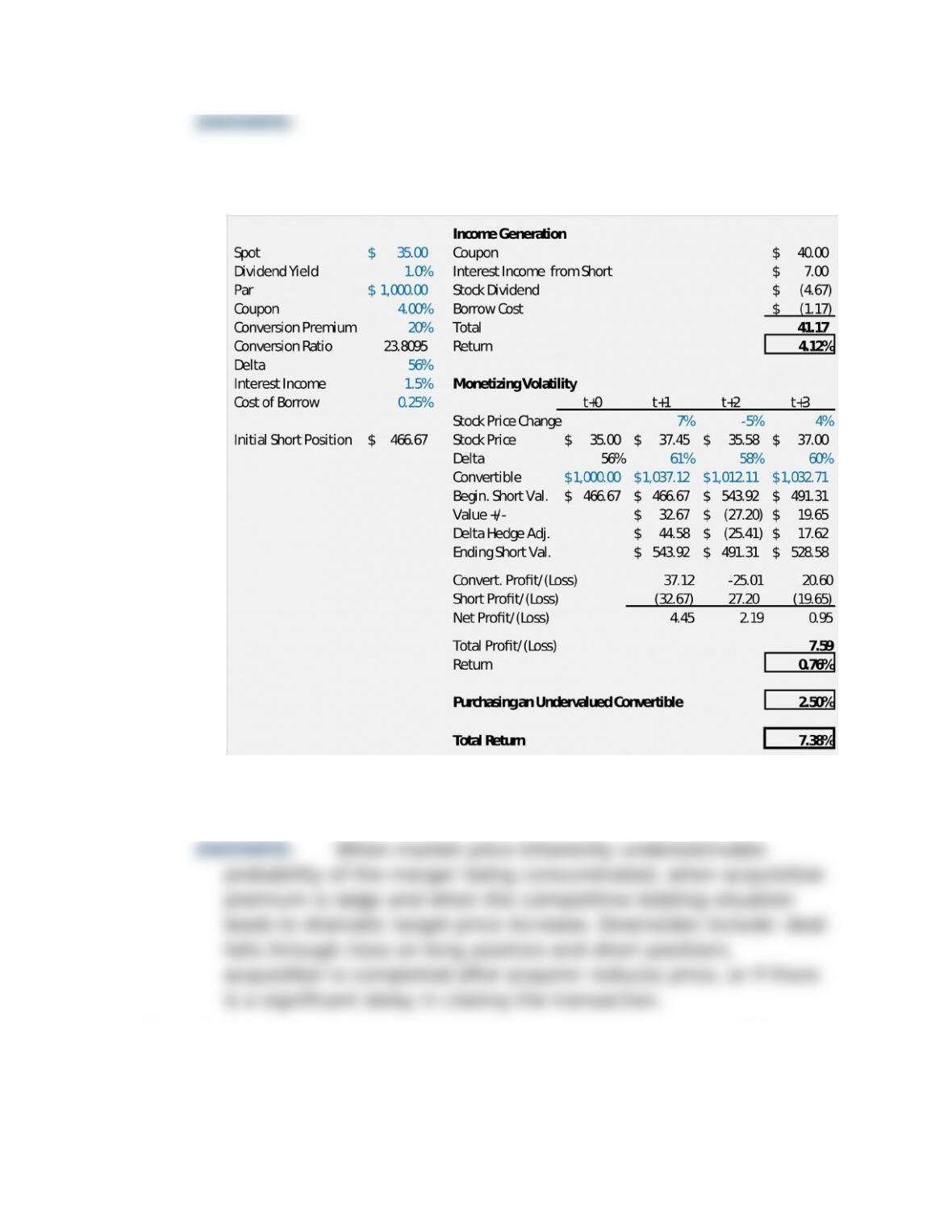

Q5. Assume you buy $1,000 of a convertible bond at par, which was

o1ered at a 2.5% discount to its theoretical value. The stock price

on the day of purchase is $35, and carries a 1% dividend yield. The

convertible bond has a 4% coupon, a conversion premium of 20%,

and a delta of 56%. Interest income from the short position is 1.5%,

and stock borrow cost is 0.25%. During a one-year holding period,

the stock moves 3 times. The percentage change in stock price,

corresponding convertible bond value, and new delta ratio, in

sequential order are as follows: +7% / $1,037.12 / 61%; -5% /

$1,012.11 / 58%; +4% / $1,032.71 / 60%. Calculate the returns

generated from this investment after one year, broken out by

Income Generation, Monetizing Volatility, and Purchasing an

Undervalued Convertible. Ignore transaction costs for the purposes

of this exercise.

Q6. When is merger arbitrage an attractive investment strategy? What

are the downside risks of this strategy?

Q7. MNO makes a tender o1er for PRS at 1.5 MNO shares per PRS share.

MNO was trading at $40 per share prior to announcement and fell to

$38 on announcement. PRS was trading at $40 per share prior to

announcement and is now trading at $50. If you are pursuing a

merger arbitrage strategy, what is the position you would set up to

create potential investment value? What derivative transaction

could you use to mitigate your risk?

Q8. Calculate the expected return for the following cash merger

arbitrage transaction: offer per Target share is $30.25. Target’s

share price just prior to the announcement is $20.00, and $28.50

immediately following the announcement. The deal is expected to

close with a 95% certainty. The deal is expected to close in four

months.

Q9. Describe scenarios whereby distressed / restructuring hedge fund

strategies could produce poor results.

Q10. Generally speaking, in which two hedge fund strategies would you

expect to see more volatile returns?

Q11. Merger arbitrage is considered a market-neutral strategy. Under

what conditions would this no longer be the case?

Q12. What are some ways to neutralize market risk in an equity

long/short transaction?

Q1. Which type of company makes an easier target for an activist

investor and why: a company that has adopted a majority voting

standard, or a company with a plurality voting standard?

Q2. Suppose Company A submits a corporate governance proposal to

destagger its board. Under current regulations, would brokers be

permitted to vote their customers’ shares without voting

instructions?

Q3. What’s the bene!t of staggering the election of board of directors?

Q4. Cumulative voting is the practice of allowing shareholders to cast all

of their votes for a single nominee for the board of directors when

the company has multiple openings on its board. Does this practice

help or hinder activists?

Q5. Describe what is meant by a “13D letter”

Q6. If Company A owns Company B’s stock (which is currently trading at

$30) and A purchases a two year put on B’s stock with a strike price

of $25 and sells a two year call on B stock with a strike price of $34,

what is this equity derivative structure called? What are its bene!ts

and disadvantages?

Q7. What timing mismatch issue exists for activist hedge fund

investment strategy?

Q8. Activist funds need to devote more time and resources to

investments compared to most other fund strategies. What added

risk does this produce for activist funds?

Q9. Describe a total return swap (sometimes called an equity swap) and

the bene!ts of this strategy for a hedge fund.

Q10. In the legal battle between CSX, TCI and 3G, the SEC and the

Federal Court judge that presided over the lawsuit held differing

views of the case. Which had a more rules-based approach and

which had a more principles-based approach?

Q1. Which two core hedge fund activities can either create incremental

risk or act as a risk mitigator?

Q2. Explain the importance of hedge funds to investment banks,

including revenue, types of business, and which investment banking

division is most relevant. In addition, with which investment

banking areas do hedge funds principally complete?

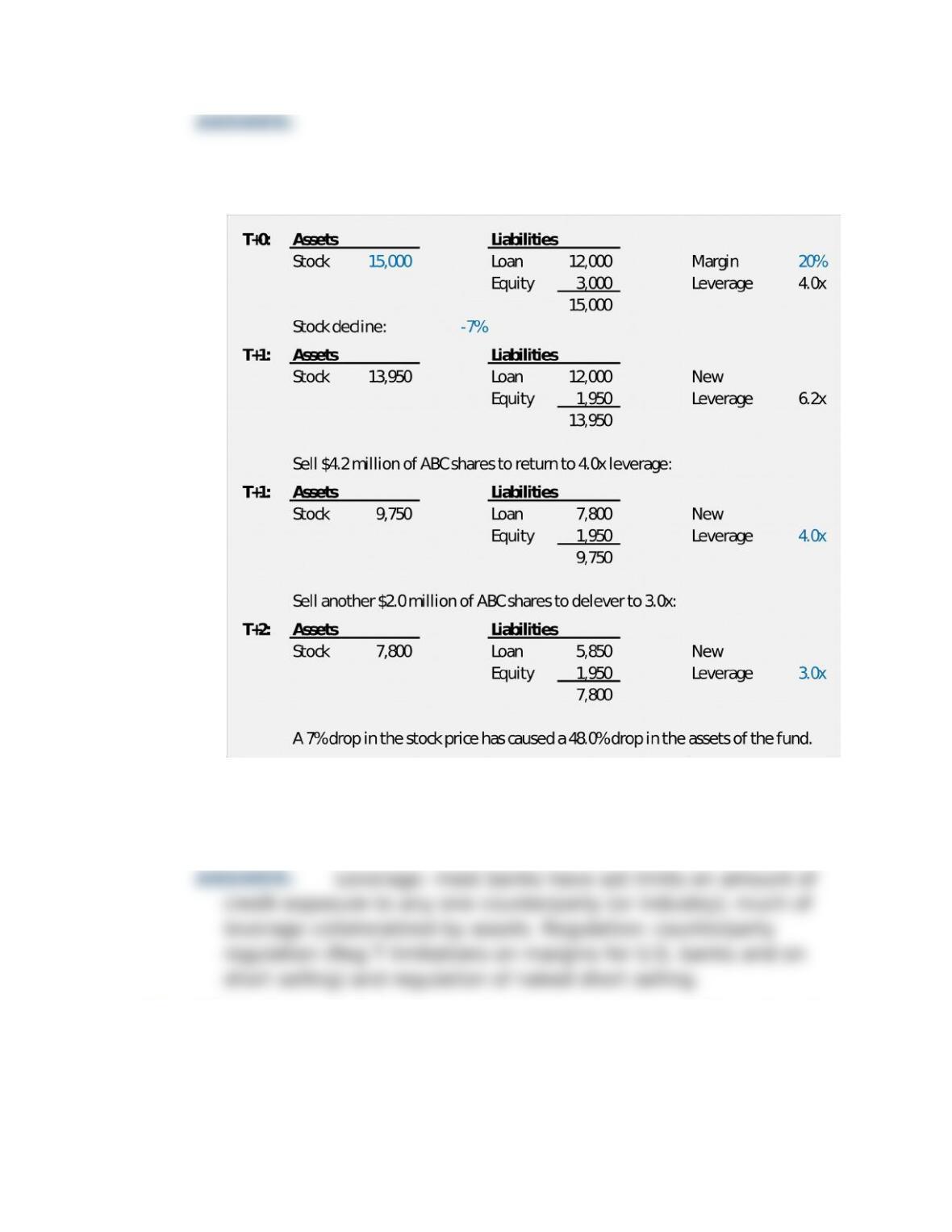

Q3. Suppose a hedge fund manager buys $15 million of ABC shares on

20% margin. The maximum allowable leverage ratio is 4.0x. The

next day, unexpected negative news about ABC is released and its

stock closes down 7%. One day later, the hedge fund’s prime

broker noti!es the manager that leverage ratios now need to come

down to 3.0x. What percentage of the original balance of ABC

shares is left in the investment fund at the end of the day after

selling shares to comply with the new leverage requirement?

(assume the fund’s sales of ABC stock does not further depress its

share price)

Q4. What are two of the key checks and balances in place to help

manage the incremental risks associated with the hedge fund

industry?

Q5. What are some of the major market events in the last three decades

that have raised the issue of systemic risk?

Q6. Under historical U.S. laws, when did a fund (and its advisors) need

to register with the SEC? What is the regulatory requirement under

the Dodd-Frank Act?

Q1. Describe the key characteristics and bene!ts of hedge funds

Q2. How has the perception of hedge funds changed since the !nancial

crisis?

Q3. Describe the problems associated with the high-water mark fee

structure often employed by hedge funds.

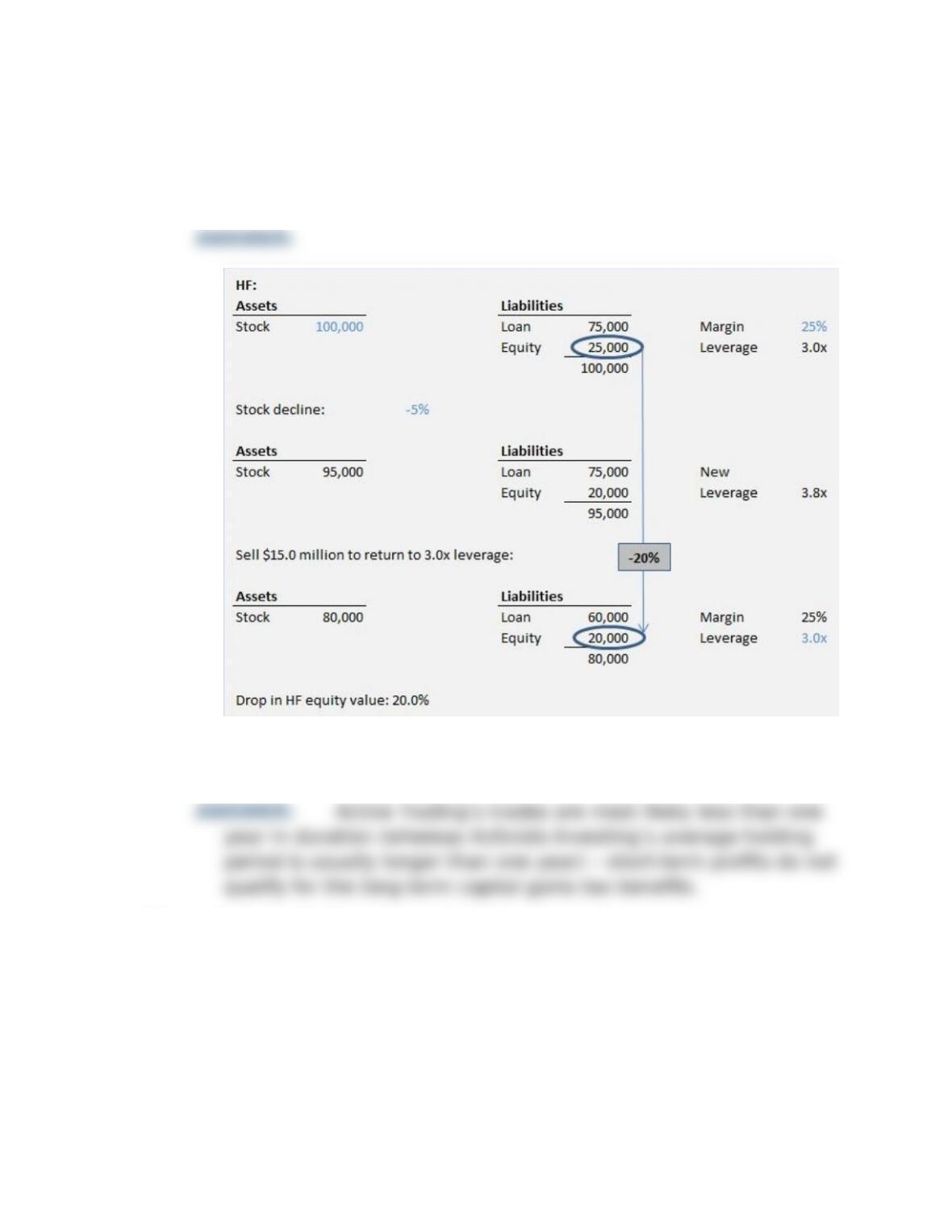

Q4. Assume an investor invests in a hedge funds that employs 25%

margin / 3.0x leverage. What happens to the investor’s money (%

change) if investments in the hedge fund’s portfolio drop 5% in

value?

Q5. Assuming same size and pro!tability, which fund would you expect

to have more in tax liabilities: Active Trading or Activist Investing?

Q6. Hedge fund AlphaBeta has a NAV of $1 million and a zero balance in

its cumulative loss account on January 1, 2016. Now suppose

AlphaBeta’s annual performance (net of management fees) is +

13.9% in 2016, +12.6% in 2017, and -19.1% in 2018. AlphaBeta

charges a 20% performance fee. Based on the high water mark

reached in 2017, what minimum percentage gain the does the fund

need to achieve in 2019 before performance fees can be taken

again?

NA

V

Gain/

(Loss)

Perf.

Fee

Cumulati

ve

Loss

Account

1/1/20

06

1,000,0

00

12/31/20

06

13.90

%

1,139,0

00

139,0

00

27,8

00

0

1/1/20

07

1,111,2

00

12/31/20

07

12.60

%

1,251,2

11

140,0

11

28,0

02

0

1/1/20

08

1,223,2

09

12/31/20

08

–

19.10

%

989,5

76

(233,63

3)

0 (233,63

3)

1/1/20

09

989,5

76

12/31/20

09

23.61

%

1,223,2

09

233,6

33

46,7

27

0

Q7. Classifying some of the largest hedge funds as Tier 1 !nancial

holding companies would subject these funds to requirements

regarding capital, liquidity, and risk management. The rationale for

this is that a large hedge fund, on its own, could pose systemic risk

to the !nancial system. Discuss the merits of this argument.

Q8. How have the investment pro!les of hedge funds changed in recent

years as hedge funds have tried to differentiate themselves from

traditional fund managers?

Q9. What is the bene!t of a hedge fund like Citadel expanding into the

hedge fund services business such as market making and fund

administration?

Q1. Are private equity !rms !nancial buyers or strategic buyers and

why? Which type of buyer should generally be able to pay more in

an M&A auction and why? Why might that not always be the case?

Q2. Provide two examples: one of a publicly traded company that would

be a good LBO target, and one that would not be an ideal candidate.

Explain your choices.

Q3. What type of management is generally needed to run a portfolio

company owned by a private equity !rm (describe the

characteristics of these managers)?

Q4. What are the !ve principal !nancing sources for an LBO transaction?

Q5. How is the commitment and redemption of capital different in

private equity compared to hedge funds?

Q6. Why would a proposal to eliminate the tax bene!ts of carried

interest (performance fees) have a greater impact on the private

equity industry?

Q7. Why are general partners typically only allowed to make

investments in new companies during the !rst !ve years of a fund’s

life?

Q8. Suppose a private equity fund has $100 million in committed capital

and its base rate for management fees is 2%. The fund invested in

10 companies during the !rst 5 years and begins to exit its

investments in year 6 at a pace of two exits per year until the end

of year 10, when all investments have been exited. Assume the

original cost basis for each investment is $10 million. Also assume

fees calculated on net invested capital is based on year-end

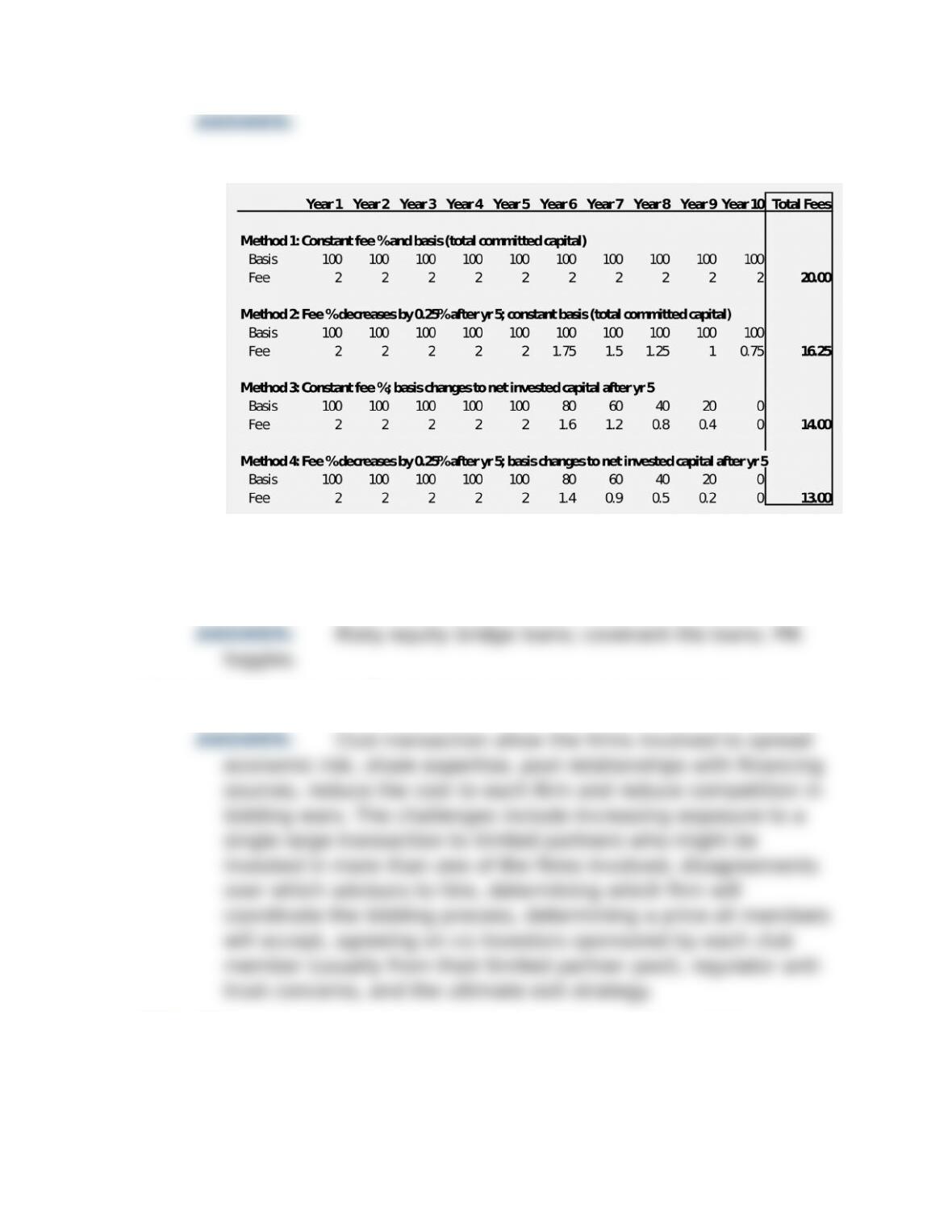

balances. How much in lifetime management fees does the !rm

earn, based on each of the four methods described in Exhibit 16.2?

Q9. What type of concessions were private equity !rms able to get from

investment banks during 2006 and the !rst half of 2007 that

normally would not be possible?

Q10. Describe the bene!ts and challenges of club transactions.

Q11. When a private equity fund teams up with management for a

potential buyout, why would they want to avoid having early

disclosure of the transaction?

Q12. Why do you think more companies don’t recapitalize their balance

sheets by adding more debt in order to replicate the returns

achieved by private equity fund portfolio companies? Do

investment banks ever recommend a leveraged recapitalization of

public companies? Why or why not?

Q13. Since private equity !rms seek to minimize their equity contribution

in a deal in order to maximize returns, the amount of debt used to

!nance transactions should (wishing away !nancial risk) be the

maximum amount of leverage for the company that debt providers

will accept. Why then, are these companies allowed to take on even

more debt for leveraged recapitalizations?

Q1. What does an LBO analysis include, what does it solve for and what

question is answered by the analysis?

Q2. What are the three ways to create returns through an LBO

transaction?

Q3. What is the formula for determining cash 6ow available for debt

service?

Q4. What are the key credit statistics in an LBO !nancing?

Q1. What are some measurable bene!ts from private equity ownership

of corporations?

Q2. What were the World Economic Forum’s principal conclusions

regarding private equity !rms?

Q3. What were the principal perceived bene!ts for the PE consortium’s

acquisition of TXU?

Q4. In hindsight, what were some of the errors committed by the buyout

group for TXU?

Q5. What were the principal risks faced by the PE consortium when they

made their bid to acquire HCA?

Q6. What aspect of Harrah’s business makes it not a good buyout

target?

Q7. What is the impact of highly leveraged deals on the portfolio

companies’ ability to compete in their industries?

Q8. Describe the three main areas where private equity investments

may bring value to corporations.

Q9. Which of the three private equity value propositions for corporations

has become most problematic in recent years?

Q10. What is a bene!t of having a !nancial buyer versus a strategic

buyer in an M&A transaction?

Q11. Describe the bene!ts of the private-equity ownership model versus

public ownership and family-ownership.

Q12. Based on the description of the ideal buyout target in the beginning

of the section titled Corporate Rationale for Private Equity

Transaction, which of the companies described in the section

“Private Equity Portfolio Companies Purchased During 2006-2007”

were the most suitable buyout targets?

Q1. What is a difference between the organizational structure of private

equity funds and hedge funds?

Q2. What are similarities and differences in the compensation structure

for private equity funds and hedge funds?

Q3. What are the primary exit strategies considered by private equity

!rms?

Q4. Discuss whether or not the tax rates applicable to private equity

!rms should be changed?

Q5. In the U.S., what provisions have private equity funds historically

relied on to avoid registration with the SEC? How has the Dodd-

Frank Act changed regulation of private equity funds?

Q6. Why is there a secondary market for private equity funds, but not

hedge funds?

Q7. Based on HCA buyout Exhibits in Chapter 19, calculate the value of

the !nancial sponsors’ equity stake in HCA, based on FASB 157’s fair

value determination requirements. Assume HCA’s EBITDA dropped

by 20% from its LTM EBITDA at the time of the transaction, no debt

has been paid down, and valuation multiples have decreased to

6.5x.

Q1. Describe the bene!ts and risks of an equity buyout compared to a

leveraged buyout.

Q2. Why were LBO funds so successful from 2002 through July 2007?

Describe what has happened since then.

Q3. What is a possible negative consequence of investing during private

equity boom cycles?

Q4. From the perspective of existing LPs in a private equity fund, what

are the bene!ts and considerations of annex funds?

Q5. Explain the advantages of private equity funds partnering with

strategic buyers.

Q6. After initially !nding success in M&A advisory businesses, what

issues have arisen for private equity !rms in this arena?

Q7. Annex funds attempt to address which of the principal risks outlined

in Blackstone’s IPO prospectus (Exhibit 20.10)?

Q8. Discuss “multiple expansion” in the context of value creation for

private equity investments made following a !nancial crisis.

Q9. How have limited partners utilized the secondary market to

participate in private equity?