Chapter 5

INVENTORIES AND COST OF SALES

True / False Questions

1. Goods in transit are automatically included in inventory regardless of whether title has

passed to the buyer.

2. Goods on consignment are goods shipped by their owner, called the consignor, to another

party called the consignee.

3. If obsolete or damaged goods can be sold, they will be included in inventory at their

original cost.

4. If the seller is responsible for paying freight charges, then ownership of inventory passes

when goods arrive at their destination.

5. Net realizable value for damaged or obsolete goods is sales price less the cost of making

the sale.

6. The cost of an inventory item includes its invoice cost plus any added or incidental costs

necessary to put it in a place and condition for sale, and minus any discount..

7. One application of internal control when taking a physical count of inventory is the use of

pre-numbered inventory tickets.

8. Incidental costs for acquiring merchandise inventory, such as import duties, freight, storage,

and insurance, should not be added to the cost of inventory.

9. The Inventory account is a controlling account for the inventory subsidiary ledger that

contains a separate record for each separate product.

10. Most companies do not take a physical count of inventory each year, but rather rely on

inventory records to determine the inventory value.

11. The matching principle is used to determine how much of the cost of goods available for

sale is deducted from sales and how much is carried forward as inventory.

12. The consistency concept allows a company use different accounting methods from period

to period in order to maximize profits.

13. A company must disclose any change in its inventory costing method in its financial

statements.

14. Whether purchase costs are rising or falling, FIFO always will yield the highest gross

profit and net income.

15. An advantage of the weighted average inventory method is that it tends to smooth out

erratic changes in costs.

16. In a period of rising purchase costs, LIFO usually gives a lower taxable income and

therefore, yields a tax advantage.

17. FIFO is preferred when purchase costs are rising and managers have incentives to report

higher income for reasons such as bonus plans, job security, and reputation.

18. The LIFO method of inventory valuation can result in a company’s ending inventory

being valued at less than the inventory’s replacement cost because LIFO inventory leaves the

oldest costs in inventory.

19. The full disclosure principle requires that the notes to the financial statements report any

change in the method of accounting for inventory.

20. An advantage of FIFO is that it assigns the most recent costs to cost of goods sold, and

does a better job of matching current costs with revenues on the income statement.

21. According to IRS guidelines, companies may use FIFO for financial reporting and LIFO

for tax reporting.

22. An error in the period-end inventory balance will cause an error in the calculation of cost

of goods sold.

23. Errors in the period-end inventory balance only affect the current period’s records and

financial statements.

24. An inventory error is sometimes said to be self-correcting because it yields an offsetting

error in the next period.

25. An understatement of the ending inventory balance will overstate cost of goods sold and

understate net income.

26. Overstating beginning inventory will understate cost of goods sold and net income.

27. An understatement of ending inventory will cause an understatement of assets and equity

on the balance sheet.

28. An overstatement of ending inventory will cause an overstatement of assets and an

understatement of equity on the balance sheet.

29. A merchandiser’s ability to pay its short-term obligations depends on many factors

including how quickly it sells its merchandise inventory.

30. The inventory turnover ratio is computed by dividing cost of goods sold by average

merchandise inventory.

31. The days’ sales in inventory ratio is computed by dividing ending inventory by cost of

goods sold and multiplying the result by 365.

32. The simple rule for inventory turnover is that a low ratio is preferable.

33. It can be expected that companies selling perishable goods have a higher inventory

turnover than companies selling nonperishable goods.

34. A company’s cost of goods sold was $15,500 and its average merchandise inventory was

$4,500. Its inventory turnover equals 3.4.

35. Underwood had cost of goods sold of $8 million and its ending inventory was $2 million.

Therefore, its days’ sales in inventory equals 25 days.

36. Determining the unit costs assigned to inventory items is one of the most important

decisions in accounting for inventory.

37. When units are purchased at different costs over time, determining the cost per unit

assigned to inventory items is simple.

38. LIFO assumes that inventory costs flow in the order incurred.

39. The assignment of costs to cost of goods sold and inventory using weighted average

usually yields different results depending on whether a perpetual or periodic system is used.

40. The FIFO inventory method assumes that costs for the latest units purchased are the first

to be charged to the cost of goods sold.

41. The costs of goods purchased will vary under the different inventory methods of specific

identification, FIFO, LIFO, and weighted average.

42. The assignment of costs to the cost of goods sold and to ending inventory using FIFO is

the same for both the perpetual and periodic inventory systems.

43. Under FIFO, the most recent costs are assigned to ending inventory.

44. The choice of an inventory valuation method has little to no impact on gross profit and

cost of sales.

45. In applying the lower of cost or market method to inventory valuation, market is defined

as the current replacement cost.

46. In applying the lower of cost or market method to inventory valuation, market is defined

as the current selling price.

47. A company has inventory with a selling price of $451,000, a market value of $223,000

and a cost of $241,000. According to the lower of cost or market, the inventory should be

written down to $223,000.

48. The lower of cost or market rule for inventory valuation is always applied to individual

units separately rather than to major categories of inventory or to the entire inventory.

49. The conservatism constraint requires that when more than one estimate of the amounts to

be received or paid in the future exists and these estimates are about equally likely, then the

most optimistic amount is used.

50. The lower of cost or market requiring inventory to be reported at market value if it is

lower than cost is an example of applying the conservatism constraint.

51. A company’s total cost of inventory was $329,000 and its current replacement cost is

$307,000. Under the lower cost or market, the amount reported should be $329,000.

52. A company’s cost of inventory was $219,500. Due to phenomenal demand the market

value of its inventory increased to $221,700. This company should write up the value of its

inventory according to the conservatism constraint.

53. When LIFO is used with the periodic inventory system, cost of goods sold is assigned

costs from the most recent purchases at the point of each sale, rather than from the most

recent purchases for the period.

54. The retail inventory method estimates the cost of ending inventory by applying the gross

profit ratio to net sales.

55. The reasoning behind the retail inventory method is that if we can get a good estimate of

the cost-to-retail ratio, we can multiply ending inventory at retail by this ratio to estimate

ending inventory at cost.

56. The reliability of the gross profit method depends on a good estimate of the gross profit

ratio.

57. In the retail inventory method of inventory valuation, the retail amount of inventory refers

to its dollar amount measured using selling prices of inventory items.

58. To avoid the time-consuming process of taking an inventory each year, most companies

use the gross profit method to estimate ending inventory.

59. Using the retail inventory method, if the cost to retail ratio is 70% and ending inventory at

retail is $145,000, then estimated ending inventory at cost is $207,143.

60. Damaged and obsolete goods that can be sold:

A. Are never counted as inventory.

B. Are included in inventory at their full cost.

C. Are included in inventory at their net realizable value.

D. Should be disposed of immediately.

E. Are assigned a value of zero.

61. Merchandise inventory includes:

A. All goods owned by a company and held for sale.

B. All goods in transit.

C. All goods on consignment.

D. Only damaged goods.

E. Only non-damaged goods.

62. Goods in transit are included in a purchaser’s inventory:

A. At any time during transit.

B. When the purchaser is responsible for paying freight charges.

C. When the supplier is responsible for freight charges.

D. If the goods are shipped FOB destination.

E. After the half-way point between the buyer and seller.

63. Consignment goods are:

A. Goods shipped by the owner to the consignee who sells the goods for the owner.

B. Reported in the consignee’s books as inventory.

C. Goods shipped to the consignor who sells the goods for the owner.

D. Not reported in the consignor’s inventory since they do not have possession of the

inventory.

E. Always paid for by the consignee when they take possession.

64. Regardless of the inventory costing system used, cost of goods available for sale must be

allocated at the end of the period between

A. beginning inventory and net purchases during the period.

B. ending inventory and beginning inventory.

C. net purchases during the period and ending inventory.

D. ending inventory and cost of goods sold.

E. beginning inventory and cost of goods sold.

65. On December 31 of the current year, Plunkett Company reported an ending inventory

balance of $215,000. The following additional information is also available:

Plunkett sold and shipped goods costing $38,000 to Savannah Enterprises on

December 28 with shipping terms of FOB shipping point. The goods were not

included in the ending inventory amount of $215,000.

Plunkett purchased goods costing $44,000 on December 29. The goods were shipped

FOB destination and were received by Plunkett on January 2 of the following year.

The shipment was a rush order that was supposed to arrive by December 31. These

goods were included in the ending inventory balance of $215,000.

Plunkett’s ending inventory balance of $215,000 included $15,000 of goods being held

on consignment from Carole Company. (Plunkett Company is the consignee.)

Plunkett’s ending inventory balance of $215,000 did not include goods costing

$95,000 that were shipped to Plunkett on December 27 with shipping terms of FOB

destination and were still in transit at year-end.

Based on the above information, the amount that Plunkett should report in ending inventory

on December 31 is:

A. $194,000

B. $209,000

C. $200,000

D. $171,000

E. $156,000

66. Bedrock Company reported a December 31 ending inventory balance of $412,000. The

following additional information is also available:

The ending inventory balance of $412,000 included $72,000 of consigned inventory

for which Bedrock was the consignor.

The ending inventory balance of $412,000 included $22,000 of office supplies that

were stored in the warehouse and were to be used by the company’s supervisors and

managers during the coming year.

Based on this information, the correct balance for ending inventory on December 31 is:

A. $412,000

B. $340,000

C. $318,000

D. $362,000

E. $390,000

67. Buffalo Company reported a December 31 ending inventory balance of $412,000. The

following additional information is also available:

The ending inventory balance of $412,000 did not include goods costing $48,000 that

were purchased by Buffalo on December 28 and shipped FOB destination on that date.

Buffalo did not receive the goods until January 2 of the following year.

The ending inventory balance of $412,000 included damaged goods at their original

cost of $38,000. The net realizable value of the damaged goods was $10,000.

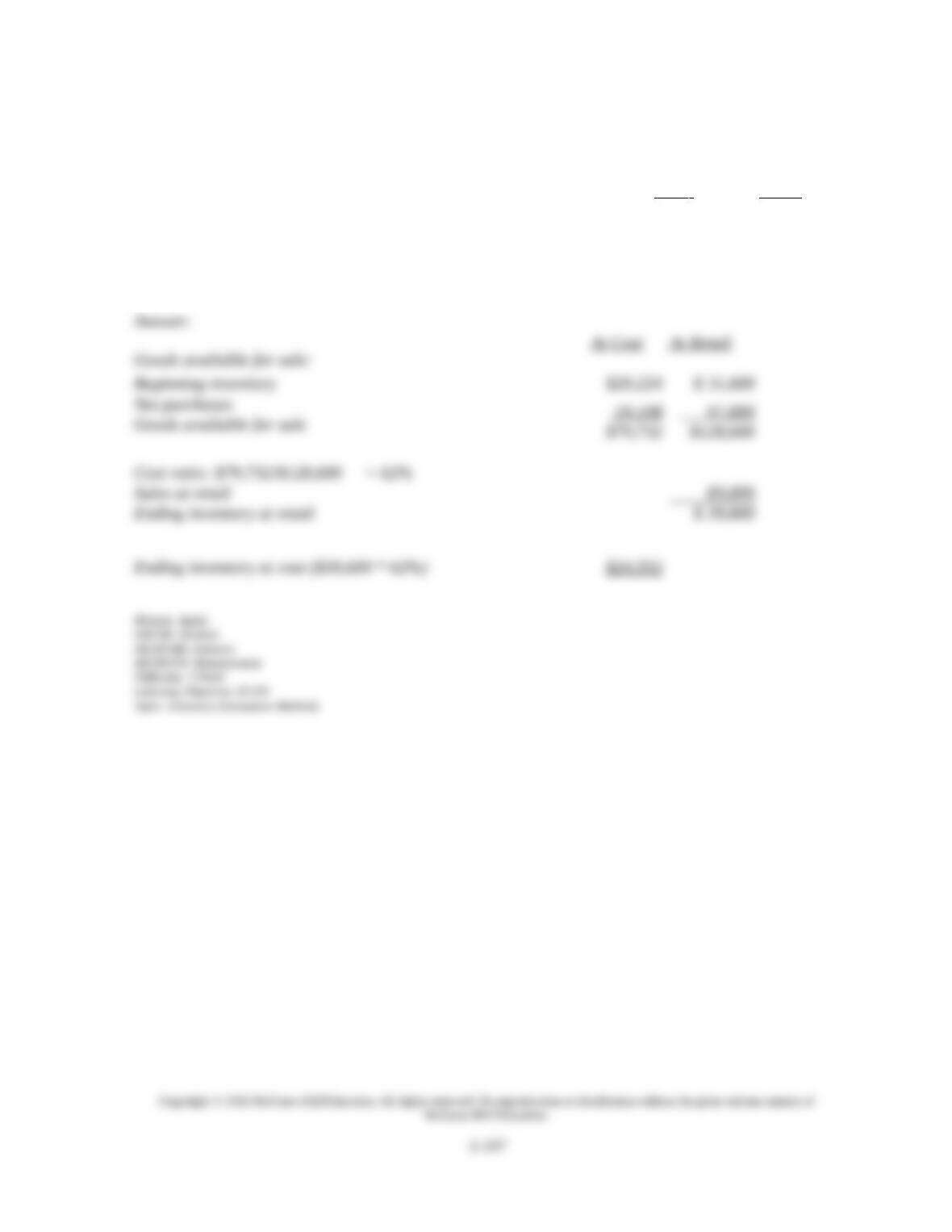

Based on this information, the correct balance for ending inventory on December 31 is:

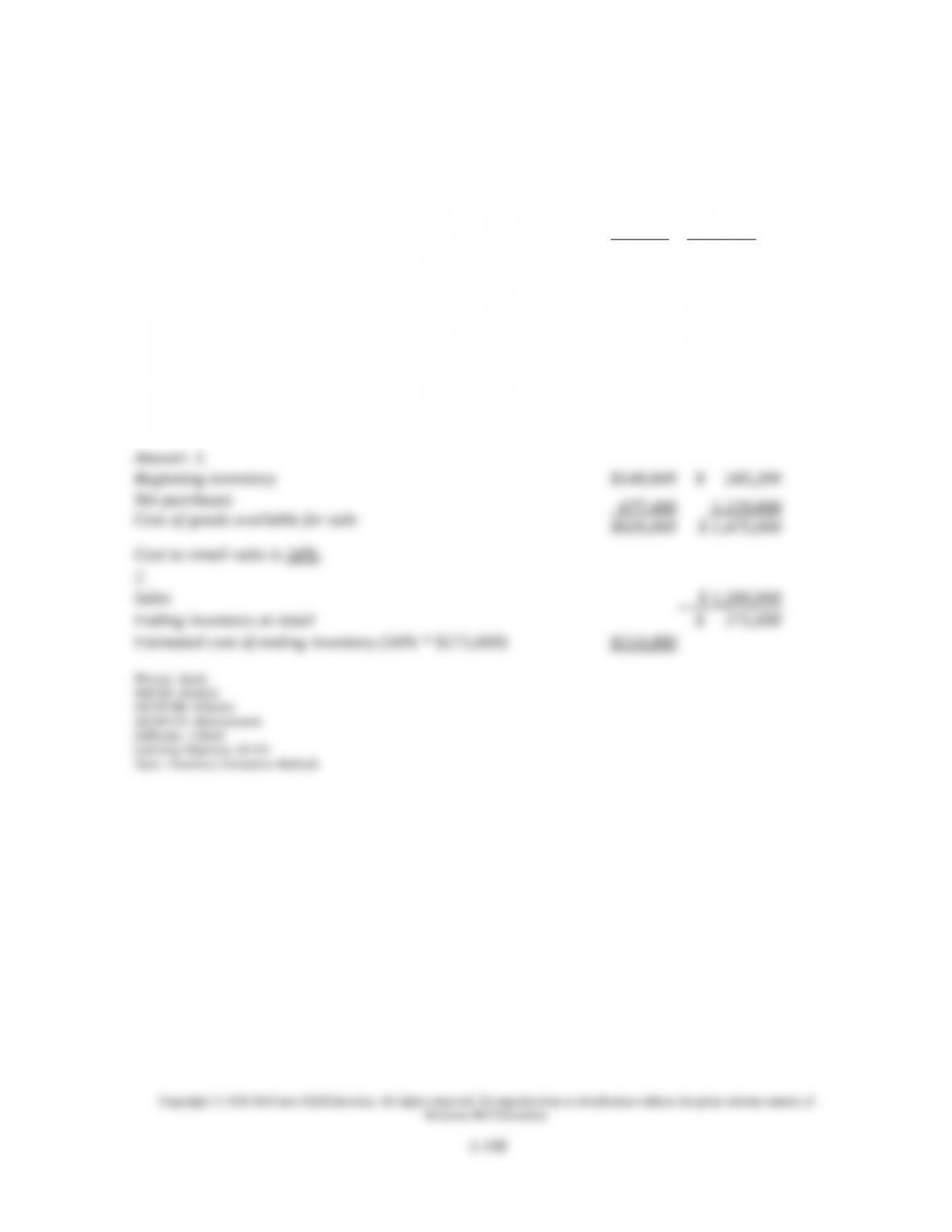

A. $374,000

B. $384,000

C. $460,000

D. $422,000

E. $438,000

68. Costs included in the Merchandise Inventory account can include all of the following

except:

A. Invoice price minus any discount.

B. Transportation-in.

C. Storage.

D. Insurance.

E. Damaged inventory that cannot be sold.

69. Internal controls that should be applied when a business takes a physical count of

inventory should include all of the following except:

A. Prenumbered inventory tickets.

B. A manager confirms that all inventories are ticketed only once.

C. Counters confirm the validity of inventory existence, amounts, and quality.

D. Second counts by a different counter.

E. Counters of inventory should be those who are responsible for the inventory.

70. Physical counts of inventory:

A. Are not necessary under the perpetual system.

B. Are necessary to adjust the Inventory account to the actual inventory available.

C. Must be taken at least once a month.

D. Requires the use of hand-held portable computers.

E. Are not necessary under the cost-to benefit constraint.

71. During a period of steadily rising costs, the inventory valuation method that yields the

highest reported net income is:

A. Specific identification method.

B. Average cost method.

C. Weighted-average method.

D. FIFO method.

E. LIFO method.

72. The inventory valuation method that tends to smooth out erratic changes in costs is:

A. FIFO.

B. Weighted average.

C. LIFO.

D. Specific identification.

E. WIFO.

73. The inventory valuation method that has the advantages of assigning an amount to

inventory on the balance sheet that approximates its current cost, and also mimics the actual

flow of goods for most businesses is:

A. FIFO.

B. Weighted average.

C. LIFO.

D. Specific identification.

E. Lower of cost or market.

74. The inventory valuation method that results in the lowest taxable income in a period of

inflation is:

A. LIFO method.

B. FIFO method.

C. Weighted-average cost method.

D. Specific identification method.

E. Gross profit method.

75. The consistency concept:

A. Prescribes a company use the same accounting method of inventory valuation, an

exception being when a change from one method to another will improve its financial

reporting.

B. Requires a company to use one method of inventory valuation exclusively.

C. Requires that all companies in the same industry use the same accounting methods of

inventory valuation.

D. Is also called the full disclosure principle.

E. Is also called the matching principle.

76. The full disclosure principle:

A. Prescribes that the notes to the financial statements report the change from one inventory

valuation method to another.

B. Requires that companies use the same accounting method for inventory valuation period

after period.

C. Is not subject to the consideration of materiality.

D. Is only applied to retailers and manufacturers.

E. Is also called the consistency principle.

77. Which of the following prescribes the use of the less optimistic amount when more than

one estimate of an amount to be received or paid exists and the estimates are about equally

likely?

A. Full disclosure principle.

B. Consistency concept.

C. FIFO inventory valuation method.

D. Conservatism constraint.

E. Matching principle.

78. Which of the following inventory costing methods will always result in the same values

for ending inventory and cost of goods sold regardless of whether a perpetual or periodic

inventory system is used?

A. FIFO and LIFO

B. LIFO and weighted-average cost

C. Specific identification and FIFO

D. FIFO and weighted-average cost

E. LIFO and specific identification

79. If a period-end inventory amount is reported in error, it can cause a misstatement in all of

the following except:

A. Cost of goods sold.

B. Gross profit.

C. Net sales.

D. Current assets.

E. Net income.

80. Since an error in the period-end inventory causes an offsetting error in the next period:

A. Managers can ignore the error.

B. It is said to be self-correcting.

C. It affects only income statement accounts.

D. If affects only balance sheet accounts.

E. Is immaterial for managerial decision making.

81. The understatement of the ending inventory balance causes:

A. Cost of goods sold to be overstated and net income to be understated.

B. Cost of goods sold to be overstated and net income to be overstated.

C. Cost of goods sold to be understated and net income to be understated.

D. Cost of goods sold to be understated and net income to be overstated.

E. Cost of goods sold to be overstated and net income to be correct.

82. The understatement of the beginning inventory balance causes:

A. Cost of goods sold to be understated and net income to be understated.

B. Cost of goods sold to be understated and net income to be overstated.

C. Cost of goods sold to be overstated and net income to be overstated.

D. Cost of goods sold to be overstated and net income to be understated.

E. Cost of goods sold to be overstated and net income to be correct.

83. Lucia Company reported cost of goods sold for Year 1 and Year 2 as follows:

Year 1 Year 2

Beginning inventory $ 120,000 $ 130,000

Cost of goods purchased 250,000 275,000

Cost of goods available for sale 370,000 405,000

Ending inventory 130,000 135,000

Cost of goods sold $ 240,000 $ 270,000

Lucia Company made two errors: 1) ending inventory at the end of Year 1 was understated by

$15,000 and 2) ending inventory at the end of Year 2 was overstated by $6,000. Given this

information, the correct cost of goods sold figure for Year 2 would be:

A. $291,000

B. $276,000

C. $264,000

D. $285,000

E. $249,000

84. Hull Company reported the following income statement information for 2015:

2015

Sales $410,000

Cost of goods sold:

Beginning inventory $132,000

Cost of goods purchases

273,000

Cost of goods available for sale 405,000

Ending inventory

144,000

Cost of goods sold

261,000

Gross profit

$149,000

The beginning inventory balance for Year 1 is correct. However, the ending inventory figure

for Year 1 was overstated by $20,000. Given this information, the correct gross profit figure

for 2015 would be:

A. $149,000.

B. $169,000.

C. $129,000 .

D. $142,000.

E. $112,000.

85. An understatement of ending inventory will cause

A. An overstatement of assets and equity on the balance sheet.

B. An understatement of assets and equity on the balance sheet.

C. An overstatement of assets and an understatement of equity on the balance sheet.

D. An understatement of assets and an overstatement of equity on the balance sheet.

E. No effect on the balance sheet.

86. The inventory turnover ratio:

A. Is used to analyze profitability.

B. Is used to measure solvency.

C. Reveals how many times a company sells its merchandise inventory during a period.

D. Reveals how many days a company can sell inventory if no new merchandise is purchased.

E. Calculation depends on the company’s inventory valuation method.

87. Days’ sales in inventory:

A. Is also called days’ stock on hand.

B. Focuses on average inventory rather than ending inventory.

C. Is used to measure solvency.

D. Is calculated by dividing cost of goods sold by ending inventory.

E. Is a substitute for the acid-test ratio.

88. The inventory turnover ratio is calculated as:

A. Cost of goods sold divided by average merchandise inventory.

B. Sales divided by cost of goods sold.

C. Ending inventory divided by cost of goods sold.

D. Cost of goods sold divided by ending inventory.

E. Cost of goods sold divided by ending inventory times 365.

89. Days’ sales in inventory is calculated as:

A. Ending inventory divided by cost of goods sold.

B. Cost of goods sold divided by ending inventory.

C. Ending inventory divided by cost of goods sold times 365.

D. Cost of goods sold divided by ending inventory times 365.

E. Ending inventory times cost of goods sold.

90. Giorgio had cost of goods sold of $9,421 million, ending inventory of $2,089 million, and

average inventory of $1,965 million. Its inventory turnover equals:

A. 0.21.

B. 4.51

C. 4.79.

D. 76.1 days.

E. 80.9 days.

91. Perfection Company had cost of goods sold of $853,000, ending inventory of $70,500,

and average inventory of $71,600. Its inventory turnover equals:

A. 11.9.

B. 1.0

C. 6.0.

D. 30.6.

E. 12.0.

92. Beckenworth had cost of goods sold of $9,421 million, ending inventory of $2,089

million, and average inventory of $1,965 million. Its days’ sales in inventory equals:

A. 0.21.

B. 4.51.

C. 4.79.

D. 76.1 days.

E. 80.9.days.

93. Ulrich had cost of goods sold of $6.7 million, ending inventory of $2.2 million, and

average inventory of $1.9 million. Its days’ sales in inventory equals:

A. 120.

B. 104.

C. 60.

D. 35.

E. 180

94. Acceptable methods of assigning specific costs to inventory and cost of goods sold

include all of the following except:

A. LIFO method.

B. FIFO method.

C. Specific identification method.

D. Weighted average method.

E. Retail method.

95. Decisions management must make in accounting for inventory cost include all of the

following except:

A. Costing method.

B. Perpetual or periodic inventory system

C. Customer demand for inventory.

D. Use of market values or other estimates.

E. Items included in inventory and their costs.

96. The inventory valuation method that identifies each item in ending inventory with a

specific purchase and invoice is the:

A. Weighted average inventory method.

B. First-in, first-out method.

C. Last-in, first-out method.

D. Specific identification method

E. Retail inventory method.

97. A company had the following purchases during the current year:

January: 10 units at $120

February: 20 units at $130

May: 15 units at $140

September: 12 units at $150

November: 10 units at $160

On December 31, there were 26 units remaining in ending inventory. These 26 units consisted

of 2 from January, 4 from February, 6 from May, 4 from September, and 10 from November.

Using the specific identification method, what is the cost of the ending inventory?

A. $3,500.

B. $3,800.

C. $3,960.

D. $3,280.

E. $3,640.

98. A company had the following purchases during the current year:

January: 10 units at $120

February: 20 units at $125

May: 15 units at $130

September: 12 units at $135

November: 10 units at $140

On December 31, there were 26 units remaining in ending inventory. Using the FIFO

inventory valuation method, what is the cost of the ending inventory?

A. $3,280.

B. $3,200.

C. $3,445.

D. $3,540.

E. $3,640.

99. A company had the following purchases during the current year:

January: 10 units at $120

February: 20 units at $125

May: 15 units at $130

September: 12 units at $135

November: 10 units at $140

On December 31, there were 26 units remaining in ending inventory. Using the LIFO

inventory valuation method, what is the cost of the ending inventory?

A. $3,280.

B. $3,200.

C. $3,445.

D. $3,540.

E. $3,640.

100. A company had inventory on November 1 of 5 units at a cost of $20 each. On November

2, they purchased 10 units at $22 each. On November 6 they purchased 6 units at $25 each.

On November 8, 8 units were sold for $55 each. Using the LIFO perpetual inventory method,

what was the value of the inventory on November 8 after the sale?

A. $304

B. $296

C. $288

D. $280

E. $276

101. Marquis Company uses a weighted-average perpetual inventory system.

August 2 10 units were purchased at $12 per unit.

August 18 15 units were purchased at $14 per unit.

August 29 12 units were sold.

What is the amount of the cost of goods sold for this sale?

A. $148.00

B. $150.50

C. $158.40

D. $210.00

E. $330.00

102. Grays Company has inventory of 10 units at a cost of $10 each on August 1. On August

3, it purchased 20 units at $12 each. 12 units are sold on August 6. Using the FIFO perpetual

inventory method, what amount will be reported in cost of goods sold for the 12 units that

were sold?

A. $120.

B. $124.

C. $128.

D. $130.

E. $140.

103. McCarthy Company has inventory of 8 units at a cost of $200 each on October 1. On

October 2, it purchased 20 units at $205 each. 11 units are sold on October 4. Using the FIFO

perpetual inventory method, what amount will be reported in cost of goods sold for the 11

units that were sold?

A. $2,239.

B. $2,255.

C. $2,200.

D. $2,228.

E. $2,215.

104. McCarthy Company has inventory of 8 units at a cost of $200 each on October 1. On

October 2, it purchased 20 units at $205 each. 11 units are sold on October 4. Using the FIFO

perpetual inventory method, what is the value of inventory after the October 4 sale?

A. $3,485.

B. $3,445.

C. $3,500.

D. $3,472.

E. $3,461.

105. Starlight Company has inventory of 8 units at a cost of $200 each on October 1. On

October 2, it purchased 20 units at $205 each. 11 units are sold on October 4. Using the LIFO

perpetual inventory method, what amount will be reported in cost of goods sold for the 11

units that were sold?

A. $2,239.

B. $2,255.

C. $2,200.

D. $2,228.

E. $2,215.

106. Starlight Company has inventory of 8 units at a cost of $200 each on October 1. On

October 2, it purchased 20 units at $205 each. 11 units are sold on October 4. Using the LIFO

perpetual inventory method, what is the value of inventory after the October 4 sale?

A. $3,485.

B. $3,445.

C. $3,500.

D. $3,472.

E. $3,461.

107. A company’s inventory records report the following:

August 1 Beginning balance 15 units @ $12

August 5 Purchase 10 units @ $13

August 12 Purchase 20 units @ $14

On August 15, it sold 30 units. Using the FIFO perpetual inventory method, what is the value

of the inventory at August 15 after the sale?

A. $140

B. $160

C. $210

D. $380

E. $590

108. A company’s inventory records report the following in November of the current year:

Beginning November 1 5 units @ $20

Purchase November 2 10 units @ $22

Purchase November 6 6 units @ $25

On November 8, it sold 18 units for $54 each. Using the LIFO perpetual inventory method,

what was the amount recorded in the cost of goods sold account for the 18 units sold?

A. $395

B. $410

C. $450

D. $510

E. $520

109. A company’s inventory records report the following in November of the current year:

Beginning November 1 5 units @ $20 .

Purchase November 2 10 @ $22

Purchase November 6 6 @ $25

On November 8, it sold 18 units for $54 each. Using the LIFO perpetual inventory method,

what amount of gross profit was earned from the 18 units sold?

A. $577

B. $452

C. $522

D. $462

E. $562

110. A company sells garden hoses and uses the perpetual inventory system to account for its

merchandise. The beginning balance of the inventory and its transactions during September

were as follows:

September 1: Beginning balance of 18 units at $13 each

September 12: Purchased 30 units at $14 each

September 19: Sold 24 units at $30 selling price each

September 20: Purchased 24 units at $17 each

September 27: Sold 27 units at $30 selling price each

If the ending inventory is reported at $276, what inventory method was used?

A. LIFO method.

B. FIFO method.

C. Weighted average method.

D. Specific identification method.

E. Retail inventory method.

111. Jammer Company uses a weighted average perpetual inventory system and reports the

following:

August 2 Purchase 10 units at $12 per unit.

August 18 Purchase 15 units at $15 per unit.

August 29 Sale 20 units.

August 31 Purchase 14 units at $16 per unit.

What is the per-unit value of ending inventory on August 31?

A. $12.00

B. $13.80

C. $15.42

D. $16.00

E. $17.74

112. Given the following information, determine the cost of the inventory at June 30 using the

LIFO perpetual inventory method.

June 1 Beginning inventory 15 units at $20 each

June 15 Sale of 6 units for $50 each

The cost of the ending inventory is:

A. $200

B. $220

C. $380

D. $275

E. $300

113. In applying the lower of cost or market method to inventory valuation, market is defined

as:

A. Historical cost.

B. Current replacement cost.

C. Current sales price.

D. FIFO.

E. LIFO.

114. Raleigh Co. has the following products in its ending inventory. Compute the lower of

cost or market total for inventory applied separately to each product.

Product Quantity Cost per unit Market per unit

Jelly 150 $2.00 2.15

Jam 370 $2.65 2.50

Marmalade 260 $3.10 3.05

A. $2,040.50.

B. $2,086.50.

C. $2,018.00.

D. $2,109.00.

E. $2,053.50.

115. Generally accepted accounting principles require that the inventory of a company be

reported at:

A. Market value.

B. Historical cost.

C. Lower of cost or market.

D. Replacement cost.

E. Retail value.

116. The conservatism constraint prescribes that:

A. When multiple estimates of amounts to be received or paid in the future are equally likely,

then the least optimistic amount should be used.

B. A company use the same accounting methods period after period.

C. Revenues and expenses are reported in the period in which they are earned or incurred.

D. All items of a material nature are included in financial statements.

E. All inventory items are reported at full cost.

117. A company’s normal selling price for its product is $20 per unit. However, due to market

competition, the selling price has fallen to $15 per unit. This company’s current inventory

consists of 200 units purchased at $16 per unit. Replacement cost has fallen to $13 per unit.

Calculate the value of this company’s inventory at the lower of cost or market.

A. $2,550.

B. $2,600.

C. $2,700.

D. $3,000.

E. $3,200.

118. A company normally sells its product for $20 per unit. However, the selling price has

fallen to $15 per unit. This company’s current inventory consists of 200 units purchased at

$16 per unit. Replacement cost has now fallen to $13 per unit. What is the amount of the

lower cost of market adjustment the company must make as a result of this decline in value?

A. $1,000.

B. $1,400.

C. $400.

D. $600.

E. $800.

119. A company’s current inventory consists of 5,000 units purchased at $6 per unit.

Replacement cost has now fallen to $5 per unit. What is the entry the company must record to

adjust inventory to market?

A. Debit Merchandise Inventory $25,000; credit Cost of Goods Sold $25,000.

B. Debit Cost of Goods Sold $30,000; credit Merchandise Inventory $30,000.

C. Debit Cost of Goods Sold $5,000; credit Merchandise Inventory $5,000.

D. Debit Loss on Inventory $5,000; credit Cost of Goods Sold $5,000.

E. Debit Merchandise Inventory $30,000; credit Cost of Goods Sold $25,000.

120. A company has the following per unit original costs and replacement costs for its

inventory. LCM is applied to individual items.

Part A: 50 units with a cost of $5, and replacement cost of $4.50

Part B: 75 units with a cost of $6, and replacement cost of $6.50

Part C: 160 units with a cost of $3, and replacement cost of $2.50

Under the lower of cost or market method, the total value of this company’s ending inventory

is:

A. $1,180.00.

B. $1,075.00.

C. $1,112.50.

D. $1,217.50.

E. $1,137.50.

121. A company has beginning inventory of 10 units at a cost of $10 each on February 1. On

February 3, it purchases 20 units at $12 each. 12 units are sold on February 5. Using the FIFO

periodic inventory method, what is the cost of the 12 units that are sold?

A. $120

B. $124

C. $128

D. $130

E. $140

122. A company has beginning inventory of 15 units at a cost of $12 each on October 1. On

October 5, it purchases 10 units at $13 per unit. On October 12 it purchases 20 units at $14

per unit. On October 15, it sells 30 units. Using the FIFO periodic inventory method, what is

the value of the inventory at October 15 after the sale?

A. $140

B. $160

C. $210

D. $380

E. $590

123. A company had beginning inventory of 10 units at a cost of $20 each on March 1. On

March 2, it purchased 10 units at $22 each. On March 6 it purchased 6 units at $25 each. On

March 8, it sold 22 units for $54 each. Using the FIFO perpetual inventory method, what was

the cost of the 22 units sold?

A. $470

B. $490

C. $450

D. $570

E. $520

124. A company uses the periodic inventory system and had the following activity during the

current monthly period.

November 1: Beginning inventory of 100 units @ $20

November 5: Purchased 100 units @ $22

November 8: Purchased 50 units @ $23

November 16: Sold 200 units @ $45

November 19: Purchased 50 units @ $25

Using the weighted-average inventory method, the company’s ending inventory would be:

A. $2,000

B. $2,200

C. $2,250

D. $2,400

E. $4,400

125. Health Defense sells first aid kits and uses the periodic inventory system to account for

its merchandise. The beginning balance of the inventory and its transactions during January

were as follows:

January 1: Beginning balance of 18 units at $13 each

January 12: Purchased 30 units at $14 each

January 19: Sold 24 units at a selling price of $30 each

January 20: Purchased 24 units at $17 each

January 27: Sold 27 units at a selling price of $30 each

If the ending inventory is reported at $357, what inventory method was used?

A. LIFO.

B. FIFO.

C. Weighted average.

D. Specific identification.

E. Retail inventory method.

126. A company’s warehouse contents were destroyed by a flood on September 12. The

following information was the only information that was salvaged:

1. Inventory, beginning: $28,000

2. Purchases for the period: $17,000

3. Sales for the period: $55,000

4. Sales returns for the period: $700

The company’s average gross profit ratio is 35%. What is the estimated cost of the lost

inventory?

A. $ 9,705.

B. $25,995.

C. $29,250.

D. $44,000.

E. $45,000.

127. A company reports the following information regarding its inventory.

Beginning inventory: cost is $80,000; retail is $130,000

Net purchases: cost is $65,000; retail is $120,000

Sales at retail: $145,000

The year-end inventory shows $135,000 worth of merchandise available at retail prices. What

is the cost of the ending inventory calculated using the retail inventory method?

A. $ 135,000.

B. $ 73,125.

C. $ 78,300.

D. $ 72,900.

E. $105,000.

128. On March 31 a company needed to estimate its ending inventory to prepare its first

quarter financial statements. The following information is available:

Beginning inventory, January 1: $4,000

Net sales: $80,000

Net purchases: $78,000

The company’s gross margin ratio is 25%. Using the gross profit method, the cost of goods

sold would be:

A. $60,000.

B. $20,000.

C. $58,500.

D. $63,000.

E. $19,500.

129. Big Box Store has operated with a 30% average gross profit ratio for a number of years.

It had $100,000 in sales during the second quarter of this year. If it began the quarter with

$18,000 of inventory at cost and purchased $72,000 of inventory during the quarter, its

estimated ending inventory by the gross profit method is:

A. $30,000.

B. $21,000.

C. $20,000.

D. $18,000.

E. $27,000.

130. On December 31, a company needed to estimate its ending inventory to prepare its

annual financial statements. The following information is currently available:

Inventory as of January 1: $120,500

Net sales for the year: $400,000

Net purchases for the year: $270,500

This company typically achieves a gross profit ratio of 15%. Ending Inventory under the gross

profit method would be:

A. $102,425.

B. $ 10,425.

C. $ 9,000.

D. $ 51,000.

E. $ 51,425.

131. Interim financial statements:

A. Are required by the Congress.

B. Are necessary to achieve full disclosure about a business’s operations.

C. Are statements prepared for periods of less than one year.

D. Require the use of the perpetual method for inventories.

E. Cannot be prepared if the company follows the conservatism principle.

132. Jefferson Company has sales of $300,000 and cost of goods available for sale of

$270,000. If the gross profit ratio is typically 30%, the estimated cost of the ending inventory

under the gross profit method would be:

A. $60,000

B. $180,000

C. $30,000

D. $90,000

E. $120,000.

133. Oxford Packing Company reported net sales in November of the current year of

$1,000,000. At the beginning of November, the company reported beginning inventory of

$368,000. Cost of goods purchased during November amounted to $217,500. The company

reported ending inventory at the end of November of $226,750.

The company’s gross profit rate for November of the current year was:

A. 35.9%

B. 18.8%

C. 81.2%

D. 64.1%

E. 58.6%.

134. On April 24 of the current year, The Memphis Pecan Company experienced a tornado

that destroyed the company’s entire inventory. At the beginning of April, the company

reported beginning inventory of $226,750. Inventory purchased during April (until the date of

the tornado) was $197,800. Sales for the month of April through April 24 were $642,500.

Assuming the company’s typical gross profit ratio is 50%, estimate the amount of inventory

destroyed in the tornado.

A. $212,275

B. $103,300

C. $217,950

D. $321,250

E. $157,788

135. Avanti purchases inventory from overseas and incurs the following costs: the

merchandise cost is $50,000, credit terms 2/10, n/30 that apply only to the $50,000; FOB

shipping point freight charges are $1,500; insurance during transit is $500; and import duties

are $1,000. Avanti paid within the discount period and incurred additional costs of $1,200 for

advertising and $5,000 for sales commissions. Compute the cost that should be assigned to the

inventory.

A. $50,000

B. $53,000

C. $52,000

D. $51,500

E. $53,200

136. Hasham purchases inventory from overseas and incurs the following costs: the

merchandise cost is $80,000, credit terms 1/10, n/30, applicable only to the $80,000; FOB

shipping point freight charges are $2,500; insurance during transit is $300; and import duties

are $1,500. Hasham paid within the discount period. Compute the cost that should be assigned

to the inventory.

A. $83,500

B. $79,200

C. $81,700

D. $84,300

E. $81,000

137. Some companies choose to avoid assigning incidental costs of acquiring merchandise to

inventory by recording them as cost of goods sold when incurred. The principle that supports

this is called:

A. The matching principle.

B. The materiality constraint.

C. The cost principle.

D. The conservation constraint principle.

E. The lower of cost or market principle.

138. All of the following statements related to goods on consignment are true except:

A. Goods on consignment are goods provided by the owner, call the consignor.

B. A consignee sells goods for the owner.

C. The consignor continues to own the consigned goods.

D. The consignee reports the goods in its inventory until sold.

E. The consignor reports the goods in its inventory until sold.

139. When costs to purchase inventory regularly decline, which method of inventory costing

will yield the lowest gross profit and income?

A. FIFO.

B. LIFO.

C. Weighted average.

D. Specific identification.

E. Gross margin.

140. When costs to purchase inventory regularly decline, which method of inventory costing

will yield the lowest cost of goods sold?

A. FIFO.

B. LIFO.

C. Weighted average.

D. Specific identification.

E. Gross margin.

141. IFRS reporting currently does not allow which method of inventory costing?

A. Specific identification.

B. FIFO.

C. LIFO.

D. Weighted average.

E. Lower of cost or market.

142. All of the following statements regarding U.S. GAAP and IFRS are true except:

A. Both U.S. GAAP and IFRS include broad and similar guidance for the items and costs

making up merchandise inventory.

B. For both U.S. GAAP and IFRS, merchandise inventory includes all items that a company

owns and holds for sale.

C. Both U.S. GAAP and IFRS require companies to write down inventory when its value falls

below the cost presently recorded.

D. Both U.S. GAAP and IFRS allow reversals of write downs up to the original acquisition

cost.

E. With limited exceptions, neither U.S. GAAP nor IFRS allow inventory to be adjusted

upward beyond the original cost.

143. Sandoval needs to determine its year-end inventory. The warehouse contains 20,000

units, of which 3,000 were damaged by flood and are not sellable. Another 2,000 units were

purchased from Markor Company, FOB shipping point, and are currently in transit. The

company also consigns goods and has 4,000 units at a consignee’s location. How many units

should Sandoval include in its year-end inventory?

A. 29,000

B. 21,000

C. 23,000

D. 19,000

E. 26,000

144. Salmone Company reported the following purchases and sales of its only product.

Salmone uses a perpetual inventory system. Determine the cost assigned to the ending

inventory using FIFO.

Date Activities Units Acquired at Cost Units Sold at Retail

May 1 Beginning Inventory 150 units @ $10.00

5 Purchase 220 units @ $12.00

10 Sales 140 units @ $20.00

15 Purchase 100 units @ $13.00

24 Sales 150 units @ $21.00

A. $2,260

B. $3,180

C. $1,860

D. $3,580

E. $2,100

145. Salmone Company reported the following purchases and sales of its only product.

Salmone uses a perpetual inventory system. Determine the cost assigned to cost of goods sold

using FIFO.

Date Activities Units Acquired at Cost Units Sold at Retail

May 1 Beginning Inventory 150 units @ $10.00

5 Purchase 220 units @ $12.00

10 Sales 140 units @ $20.00

15 Purchase 100 units @ $13.00

24 Sales 150 units @ $21.00

A. $2,260

B. $3,180

C. $1,860

D. $3,580

E. $2,100

146. Salmone Company reported the following purchases and sales of its only product.

Salmone uses a perpetual inventory system. Determine the cost assigned to ending inventory

using LIFO.

Date Activities Units Acquired at Cost Units Sold at Retail

May 1 Beginning Inventory 150 units @ $10.00

5 Purchase 220 units @ $12.00

10 Sales 140 units @ $20.00

15 Purchase 100 units @ $13.00

24 Sales 150 units @ $21.00

A. $2,260

B. $3,180

C. $1,860

D. $3,580

E. $2,100

147. Salmone Company reported the following purchases and sales for its only product.

Salmone uses a perpetual inventory system. Determine the cost assigned to cost of goods sold

using LIFO.

Date Activities Units Acquired at Cost Units Sold at Retail

May 1 Beginning Inventory 150 units @ $10.00

5 Purchase 220 units @ $12.00

10 Sales 140 units @ $20.00

15 Purchase 100 units @ $13.00

24 Sales 150 units @ $21.00

A. $2,260

B. $3,180

C. $1,860

D. $3,580

E. $2,100

148. On September 1 of the current year, Scots Company experienced a flood that destroyed

the company’s entire inventory. Because the company had not completed its month end

reporting for August, it must estimate the amount of inventory lost using the gross profit

method. At the beginning of August, the company reported beginning inventory of $215,450.

Inventory purchased during August was $192,530. Sales for the month of August were

$542,500. Assuming the company’s typical gross profit ratio is 40%, estimate the amount of

inventory destroyed in the flood.

A. $87,480

B. $134,520

C. $109,980

D. $82,480

E. $81,480

149. Use the following information for Shafer Company to compute inventory turnover for

2015.

2015 2014

Net sales $647,500 $582,000

Cost of goods sold 389,500 360,840

Ending inventory 76,700 79,380

A. 9.98

B. 5.08

C. 4.99

D. 8.30

E. 8.44

150. Use the following information for Davis Company to compute inventory turnover for

2015.

2015 2014

Cost of goods sold 279,500 291,800

Ending inventory 47,700 49,350

A. 5.86

B. 5.76

C. 5.67

D. 11.77

E. 5.89

151. Use the following information for Ephron Company to compute days’ sales in inventory

for 2015.

A. 52. 4

B. 82. 3

C. 50. 5

D. 76.8

E. 79.3

Answer: E

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: 05-A3

Topic: Days’ Sales in Inventory

Feedback: Days’ Sales in Inventory = Ending Inventory/Cost of Goods Sold * 365

Days’ Sales in Inventory = $75,700/$348,500 * 365 = 79.3

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-74

2015 2014

Net sales $547,500 $572,000

Cost of goods sold 348,500 370,840

Ending inventory 75,700 81,400

152. Match each of the following terms a through j with the appropriate definition.

A. Specific identification method F. Interim statements

B. Days’ sales in inventory G. Net realizable value

C. Conservatism constraint H. LIFO method

D. Inventory turnover I. Weighted average inventory method

E. Retail inventory method J. FIFO method

___1. The accounting constraint that aims to select the less optimistic estimate

when two or more estimates are about equally likely.

___2. The expected sales price of an item minus the cost of making the sale.

___3. A method for estimating an ending inventory based on the ratio of the

amount of goods for sale at cost to the amount of goods for sale at retail

price.

___4. An estimate of days needed to convert the inventory at the end of the

period into receivables or cash.

___5. An inventory pricing method that assumes the unit prices of the beginning

inventory and of each purchase are weighted by the number of units of

each in inventory; the calculation occurs at the time of each sale.

____6. Financial statements prepared for periods of less than one year.

____7. An inventory valuation method that assumes costs for the most recent

items purchased are sold first and charged to cost of goods sold.

____8. An inventory valuation method where each item in inventory is identified

with a specific purchase and invoice.

____9. An inventory valuation method that assumes that inventory items are sold

in the order acquired.

____10. The number of times a company’s average inventory is sold during a

period.

153. Match the following terms a through j with the appropriate definition.

A. Inventory turnover

B. Conservatism principle

C. Lower of cost or market

D. Gross profit method

E. Consignor

F. Consistency concept

G. Specific identification method

H. Days’ sales in inventory

I. Consignee

J. Retail inventory method

___1. An owner of goods who ships them to another party who will then sell the goods for

the owner.

___ 2. A procedure for estimating inventory where the past gross profit rate is used to

estimate the cost of goods sold, which is then subtracted from the cost of goods available for

sale to determine the estimated ending inventory.

___ 3. The accounting principle that a company use the same accounting methods period

after period so that the financial statements of succeeding periods will be comparable.

___ 4. An estimate of days needed to convert the inventory available at the end of the period

into receivables or cash.

___ 5. One who receives and holds goods owned by another for purposes of selling the

goods for the owner.

___ 6. The method of assigning costs to inventory where the purchase cost of each item in

inventory is identified and used to determine the cost of inventory.

___ 7. The number of times a company’s average inventory is sold during an accounting

period.

___ 8. The required method of reporting inventory at market when market is lower than cost.

___ 9. A method for estimating inventory based on the ratio of the amount of goods for sale

at cost to the amount of goods for sale at retail prices.

___ 10. The principle that aims to select the less optimistic estimate when two or more

estimates are about equally likely.

1. E; 2. D; 3. F; 4. H; 5. I; 6. G; 7. A; 8. C; 9. J; 10. B

Blooms: Remember

AACSB: Communication

AICPA BB: Industry

AICPA FN: Decision Making

AICPA FN:, Measurement

Difficulty: Easy

Learning Objective: 05-A3

Learning Objective: 05-C1

Learning Objective: 05-P1

Learning Objective: 05-P2

Learning Objective: 05-P4

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-76

Topic: Inventory Turnover and Days’ Sales in Inventory

Topic: Determining Inventory Items

Topic: Inventory Costing

Topic: Inventory Estimation Methods

154. Match the inventory valuation method from the list below that is being described in each

situation in letters a–e. In all cases, assume a period of rising prices.

FIFO First in, first out

LIFO Last in, first out

WA Weighted average

SI Specific identification

_________a. The method that is used if each inventory item can be matched with a specific

purchase and invoice.

_________b. The method that will cause the company to have the lowest income taxes.

_________c. The method that will cause the company to have the lowest cost of goods sold.

_________d. The method that will assign a value to inventory that approximates current cost.

_________e. The method that will tend to smooth out erratic changes in costs.

155. Identify the items that are included in merchandise inventory. (In your answer address

the special situations of goods in transit, consigned goods, and damaged goods.)

156. What specific costs and deductions are used to determine the final cost of merchandise

inventory? Identify all costs including the incidental costs.

157. Describe the internal controls that must be applied when taking a physical count of

inventory.

158. Explain the effects of inventory valuation methods on the cost of ending inventory,

income, and income taxes.

159. How do the consistency concept and the full disclosure principle affect inventory

valuation?

160. What is the effect of an error in the ending inventory balance on the accounts reported in

the income statement?

161. Explain how the inventory turnover ratio and the days’ sales in inventory ratio are used

to evaluate inventory management.

162. Identify and describe the four inventory valuation methods.

163. Explain why the lower of cost or market rule is used to value inventory.

164. Discuss the important accounting features of a periodic inventory system including

accounts and procedures used.

165. Explain the reason a company might use the retail inventory method for valuing

inventory.

166. Explain the reason a company might use gross profit inventory method for valuing

inventory.

167. Sarbanes Oxley (SOX) demands that companies safeguard inventory and properly report

it. List methods that companies should use to safeguard inventory and accounting procedures

that should be used to properly report inventory.

168. The company’s inventory manager receives compensation that includes a bonus based on

gross profit. You discover that the inventory manager has knowingly overstated ending

inventory by $2 million. What effect does this error have on the financial statements of the

company and specifically gross profit? Why would the manager knowingly overstate ending

inventory? Would this be considered an ethics violation?

169. Mary’s Antiques does not have its own retail location, instead maintains inventory in its

warehouse and sells merchandise through Oldtime Antique Mall. Oldtime does not assume

responsibility for goods until they are sold to customers at which time it takes a commission

for items sold and sends the sale proceeds to Mary’s. Identify which company has the role of

the consignor and the consignee. Which company should include any unsold goods as part of

its inventory?

170. What advantages does a perpetual inventory system have over periodic inventory

system?

172. Carolina Company uses the LIFO method for valuing its ending inventory. The following

financial statement information is available for its first year of operation:

Carolina Company

Income Statement

For the year ended December 31

Sales…..……………………….. $60,000

Cost of goods sold........... 23,000

Gross profit...................... $37,000

Expenses …….…..…...........

13,000

Income before taxes......... $24,000

Carolina’s ending inventory using the LIFO method was $8,700. Carolina’s accountant

determined that had the company used FIFO, the ending inventory would have been $9,100.

a. Determine what the income before taxes would have been, had Carolina used the FIFO

method of inventory valuation instead of LIFO.

b. What would be the difference in income taxes between LIFO and FIFO, assuming a 30%

tax rate?

c. If Carolina wanted to lower the amount of income taxes to be paid, which method would it

choose?

173. Evaluate each inventory error separately and determine whether it overstates or

understates cost of goods sold and net income.

Inventory error: Cost of goods sold is: Net income is:

Understatement of beginning inventory..............

Understatement of ending inventory...................

Overstatement of beginning inventory................

Overstatement of ending inventory.....................

174. The Community Store reported the following amounts on their financial statements for

Year 1, Year 2, and Year 3:

For the year ended December 31

Year 1 Year 2 Year 3

Cost of goods sold…….…………………. $75,000 $87,000 $77,000

Net income………………………………..… 22,000 25,000 21,000

Total current assets………………………. 155,000 165,000 110,000

Equity…………………………………………. 287,000 295,000 304,000

It was discovered early in Year 4 that the ending inventory on December 31, Year 1 was

overstated by $6,000, and the ending inventory on December 31, Year 2 was understated by

$2,500. The ending inventory on December 31, Year 3 was correct. Ignoring income taxes

determine the correct amounts of cost of goods sold, net income, total current assets, and

equity for each of the years Year 1, Year 2, and Year 3.

175. A company reported the following data:

Year 1 Year 2

Cost of goods sold $317,500 $279,100

Average inventory 72,000 93,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-87

Required:

1. Calculate the company’s merchandise inventory turnover for each year.

2. Comment on the company’s efficiency in managing its inventory.

1. Year 1 $317,500/72,000 = 4.41

Year 2 $279,100/93,000 = 3.00

2. The company’s efficiency in managing its inventory is decreasing as its sales of merchandise

decrease. This is a negative reflection on inventory management.

Blooms: Apply

Blooms: Analyze

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Risk Analysis

Difficulty: 2 Medium

Learning Objective: 05-A3

Topic: Inventory Turnover and Days’ Sales in Inventory

176. A company reported the following data:

Year 1 Year 2

Cost of goods sold $425,000 $486,000

Ending inventory 140,000 175,000

Required:

1. Calculate the days’ sales in inventory for each year.

2. Comment on the trend in inventory management.

1. Year 1 ($140,000/$425,000) * 365 = 120 days

Year 2 (175,000/$486,000) * 365 = 131 days

2. The company has a trend of increasing the number of days it takes to sell its inventory. This is a

negative reflection on inventory management.

Blooms: Apply

Blooms: , Analyze

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Risk Analysis

Difficulty: 3 Hard

Learning Objective: 05-A3

Topic: Inventory Turnover and Days’ Sales in Inventory

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-88

177. A company made the following purchases during the year:

Jan. 10

15 units @ $360 each

Mar. 15 25 units @ $390 each

Apr. 25 10 units @ $420 each

July 30 20 units @ 450 each

Oct. 10 15units @ $480 each

On December 31, there were 28 units in ending inventory. These 28 units consisted of 2 from

the January 10 purchase, 3 from the March 15 purchase, 4 from the April 25 purchase, 11

from the July 30 purchase, and 8 from the October 10 purchase. Using specific identification,

calculate the cost of the ending inventory.

178. A company’s inventory records indicate the following data for the month of July:

July 1 beginning 380 u nits at $ 15 each

July 5 purchased 270 u nits at $ 17 each

July 10 sold 400 units at $50 each

July 20 purchased 300 units at $22 each

July 25 sold 400 units at $50 each

If the company uses the weighted average inventory valuation method and the perpetual

inventory system, what would be the cost of its ending inventory?

179. A company’s inventory records indicate the following data for the month of April:

April 1 beginning 350 units at $18 each

April 5 purchase 290 units at $20 each

April 9 sale 500 units at $55 each

April 14 purchase 250 units at $22 each

April 20 sale 200 units at $55 each

April 30 purchase 240 units at $25 each

If the company uses the first-in, first-out (FIFO) method and the perpetual inventory

system, what would be the cost of the ending inventory?

180. A company’s inventory records indicate the following data for the month of January:

Jan. 1 beginning 180 units at $9 each

Jan. 5 purchased 170 units at $10 each

Jan. 9 sold 300 units at $35 each

Jan. 14 purchased 200 units at $11 each

Jan. 20 sold 150 units at $35 each

Jan. 30 purchased 230 units at $12 each

If the company uses the last-in, first-out perpetual inventory system, what would be the

cost of the ending inventory?

181. A company’s inventory records indicate the following data for the month of January:

Jan. 1 beginning 180 units at $9 each

Jan. 5 purchased 170 units at $10 each

Jan. 9 sold 300 units at $35 each

Jan. 14 purchased 200 units at $11 each

Jan. 20 sold 150 units at $35 each

Jan. 30 purchased 230 units at $12 each

If the company uses the last-in, first-out perpetual inventory system, what is the amount

of cost of goods sold for January?

182. A company’s inventory records indicate the following data for the month of April:

April 1 beginning 350 units at $18 each

April 5 purchase 290 units at $20 each

April 9 sale 500 units at $55 each

April 14 purchase 250 units at $22 each

April 20 sale 200 units at $55 each

April 30 purchase 240 units at $25 each

If the company uses the first-in, first-out (FIFO) method and the perpetual inventory

system, what is the amount of cost of goods sold for April?

183. Calculate the ending inventory using FIFO for a company that uses a perpetual inventory

system, using the information given below.

Units

Unit

Cost

Beginning inventory 100 $10

Aug. 5 purchased 40 12

Aug. 10 sold 60 –

Aug. 15 purchased 70 13

Aug. 25 sold

50

–

Purchases Cost of Goods Sold Inventory

Date Units Unit cost Total Units Unit

cost

Total Units Unit cost Total

8/1 100 $10 $1,000

8/5 40 $12 $480 100 $10

$1,000

40

$12

480

140

$1,480

8/10 60 $10 $600 40 $10 $ 400

40

$12

480

80 $ 880

8/15 70 $13 $910 40 $10 $ 400

40 $12 480

70

$13

910

150 $1,790

8/25 40 $10 $400 30 $12 $ 360

10

$12

120

70

$13

910

100 $1,270

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 05-P1

Topic: Inventory Costing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-95

184. Calculate the ending inventory using LIFO for a company that uses a perpetual inventory

system, using the information given below.

Units

Unit

Cost

Beginning inventory 100 $10

Aug. 5 purchased 40 12

Aug. 10 sold 60 –

Aug. 15 purchased 70 13

Aug. 25 sold

50

185. Using the information given below for a company that uses a perpetual inventory system,

calculate the ending inventory using weighted average.

Units

Unit

Cost

Beginning inventory 100 $10

Jan. 5 purchased 40 12

Jan. 10 sold 60 –

Jan. 15 purchased 70 13

Jan. 25 sold

50

–

186. Use the information below to determine the sales revenue, cost of goods sold and gross

profit that would be reported for the company related to the March 16 sale assuming the

company uses FIFO inventory valuation and a perpetual inventory system.

January 1: Purchased 100 units at $10 per unit.

February 5: Purchased 60 units at $12 per unit.

March 16: Sold 40 units for $16 per unit.

187. Use the information below to determine the sales revenue, cost of goods sold and gross

profit that would be reported for the company related to the March 16 sale assuming the

company uses LIFO inventory valuation and a perpetual inventory system.

January 1: Purchased 100 units at $10 per unit.

February 5: Purchased 60 units at $12 per unit.

March 16: Sold 40 units for $16 per unit.

188. Use the information below to determine the sales revenue, cost of goods sold and gross

profit that would be reported for the company related to the March 16 sale assuming the

company uses LIFO inventory valuation and a perpetual inventory system.

January 1: Purchased 100 units at $10 per unit.

February 5: Purchased 60 units at $12 per unit.

March 16: Sold 40 units for $16 per unit.

189. A company reported the following data related to its ending inventory:

Product

849

Units Available

100

Cost

$10

Market

$11

842 75 16 14

847 60 14 13

860 40 16 20

Calculate the lower-of-cost-or-market on the inventory applied separately to each product.

190. A company had the following ending inventory costs:

Product Units of Hand Unit Cost Market Value

A 10 $ 5 $ 6

B 50 8 7

C 35 10 11

Required: Calculate the lower of cost or market (LCM) value for each individual item.

1. Product Total Cost Total LCM

Market

A..…....... $ 50 $ 60

$50

B………. 400 350 350

C………. 350

385 350

TOTAL 800

$750

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 05-P2

Topic: Lower or Cost or Market

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-101

191. A company uses the periodic inventory system, and the following information is

available. All purchases and sales are on credit. The selling price for the merchandise is $11

per unit.

Units

Unit

Cost

$3

Total

Cost

$ 90

6/01 Inventory Balance…………………………………. 30

6/06 Purchase………………………………………………. 70 4 280

6/11 Purchase…………………………………….………… 45 5 225

6/16

Purchase……………………………………………….

50

6

300

Goods available…………………………………….

195

$895

6/12 Sale……………………………………………….…….. 100

6/20

Sale………………………………………………………

60

Goods sold………………………….………………..

160

6/31 Inventory Balance………………………………….

35

Required: Determine the cost of the ending inventory and the cost of goods sold for June

using the LIFO method.

192. A company made the following merchandise purchases and sales during the month of

May:

May 1 Purchased 380 units at $15 each

May 5 Purchased 270 units at $17 each

May 10 Sold 400 units at $50 each

May 20 Purchased 300 units at $22 each

May 25 Sold 400 units at $50 each

There was no beginning inventory. If the company uses the weighted average periodic

method, what would be the cost of the ending inventory?

193. A company made the following merchandise purchases and sales during the month of

May:

May 1 Purchased 380 units at $15 each

May 5 Purchased 270 units at $17 each

May 10 Sold 400 units at $50 each

May 20 Purchased 300 units at $22 each

May 25 Sold 400 units at $50 each

There was no beginning inventory. If the company uses the LIFO periodic inventory method,

what would be the cost of the ending inventory?

194. A company made the following merchandise purchases and sales during the month of

May:

May 1 Purchased 380 units at $15 each

May 5 Purchased 270 units at $17 each

May 10 Sold 400 units at $50 each

May 20 Purchased 300 units at $22 each

May 25 Sold 400 units at $50 each

There was no beginning inventory. If the company uses the FIFO periodic inventory method,

what would be the cost of the ending inventory?

195. A company’s store was destroyed by an earthquake on February 10 of the current year.

The only information for the current period that could be salvaged included the following:

Beginning inventory, January 1: $44,000

Purchases to date: $198,000

Sales to date: $310,000

Historically, the company’s gross profit ratio has been 30%. Estimate the value of the

destroyed inventory using the gross profit method.

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: 05-P4

Topic: Inventory Estimation Methods

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-106

196. Apply the retail method to the following company information to calculate the cost of the

ending inventory for the current period.

Cost

Retail

Beginning inventory…………………………………………… $20,224 $31,600

Net purchases………………………………………………….. 59,508 97,000

Sales…………………………………………………………… 89,000

197. A company uses the retail inventory method and has the following information available

concerning its most recent accounting period:

At Cost At Retail

Beginning-of-period inventory $148,600 $ 245,200

Net purchases 677,400 1,229,800

Sales 1,200,000

1. What is the cost-to-retail ratio using the retail method?

2. What is the estimated cost of the ending inventory?

198. Forever Young Game Stores (FYG) has taken a physical count of its inventory at March

31, its fiscal year-end. After reviewing the accounting records and documentation, the

following items have been discovered:

(a) An invoice from Shreck Co. indicates that $30,000 of games were shipped to FYG on

March 27, terms FOB shipping point. The games and invoice did not arrive at FYG until

February 2 and were not included in the physical count.

(b) An invoice from Gamers, Inc. indicates that $8,000 of games were shipped to FYG on

March 29, terms FOB destination. The games and invoice did not arrive at FYG until

February 2 and were not included in the physical count.

The physical count and cost assignment on March 31 prior to these two items is $440,000.

The cost of goods sold for FYG is $2,100,000.

1. Calculate the amount that should be reported as ending inventory for FYG.

2. Calculate the days’ sales in inventory before and after the appropriate adjustments for

inventory.

1. The ending inventory should be adjusted to $470,000. Only the $30,000 invoice needs to be added

since it was shipped FOB shipping point, the owner (FYG) should include the inventory in the ending

balance. ($440,000 + $30,000 = $470,000)

2. Before adjustment: $440,000/$2,100,000 * 365 = 76.5 days

After adjustment: $470,000/$2,100,000 * 365 = 81.7 days

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

AICPA FN: Risk Analysis

Difficulty: 3 Hard

Learning Objective: 05-A3

Learning Objective: 05-C1

Topic: Inventory Turnover and Days’ Sales in Inventory

Topic: Determining Inventory Items

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-109

199. A company reported the current month purchase and sales data for its only product and

uses the perpetual inventory system. Determine the cost assigned to ending inventory and cost

of goods sold using FIFO.

Date Activities Units Acquired at Cost Units Sold at

Retail

April 1 Beginning Inventory 175 units @ $15.00

4 Purchase 150 units @ $16.00

7 Sales 160 units @ $30.00

10 Purchase 200 units @ $17.00

16 Sales 250 units @ $30.00

25 Purchase 160 units @ $18.00

28 Sales 150 units @ $32.00

200. A company reported the current month purchase and sales data for its only product and

uses the perpetual inventory system. Determine the cost assigned to ending inventory and cost

of goods sold using LIFO.

Date Activities Units Acquired at Cost Units Sold at

Retail

April 1 Beginning Inventory 175 units @ $15.00

4 Purchase 150 units @ $16.00

7 Sales 160 units @ $30.00

10 Purchase 200 units @ $17.00

16 Sales 250 units @ $30.00

25 Purchase 160 units @ $18.00

28 Sales 150 units @ $32.00

201. A company uses the retail inventory method and has the following information available

concerning its most recent accounting period:

At Cost At Retail

January 1 beginning inventory $167,340 $304,240

Cost of goods purchased 561,850 1,021,560

Sales 940,400

Sales returns 40,200

1. Use the retail inventory method to estimate the company’s year-end inventory at cost.

2. A year-end physical count at retail prices yields a total inventory of $404,800. Prepare a

calculation showing the company’s loss from shrinkage at cost and at retail.

1. $729,190/1,325,800 = .55

$1,325,800 – $900,200 = $425,600

$425,600 * .55 = $234,080

2. $425,600 – $404,800 = $20,800 inventory shrinkage at retail

$20,800 * .55 = $11,440 inventory shrinkage at cost

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: 05-P4

Topic: Inventory Estimation Methods

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-112

Fill in the Blank Questions

202. Goods that are in transit and were shipped FOB shipping point should be included in the

inventory records of the _______________________.

203. Goods that are in transit and were shipped FOB destination should be included in the

inventory records of the _______________________.

204. Goods on consignment are goods that are shipped by the owner, called the

_______________, to another party called the ______________________ that will sell the

goods for the owner.

205. _______________________ is the estimated sales price of damaged goods minus the

cost of making the sale.

206. Some companies use the __________________ constraint to avoid assigning incidental

costs of acquiring merchandise to inventory.

207. The cost of an inventory item includes the _____________, plus ______________ costs

necessary to put it in a place and condition for sale.

208. When purchase costs regularly rise, the ___________________ method of inventory

valuation yields the highest gross profit and net income.

209. When purchase costs regularly rise, the ___________________ method of inventory

valuation yields the lowest gross profit and net income, providing a tax advantage.

210. An advantage of the _________________ method of inventory valuation is that it tends

to smooth out the effect of erratic changes in costs.

211. An overstated beginning inventory will ______________ cost of goods sold and

_____________ net income.

212. The ________________________ratio reflects how much inventory is available in terms

of days’ sales.

213. The _____________________ is a measure of how quickly a merchandiser sells its

merchandise inventory.

214. The ______________________ method of assigning costs to inventory and cost of

goods sold exactly matches the costs of particular items with the revenues they generate and