Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 24

CAPITAL BUDGETING AND INVESTMENT ANALYSIS

True / False Questions

1. Capital budgeting is the process of analyzing alternative long-term investments and deciding

which assets to acquire or sell.

2. If the internal rate of return (IRR) of an investment is lower than the hurdle rate, the project

should be accepted.

3. Neither the payback period nor the accounting rate of return methods of evaluating

investments considers the time value of money.

4. An advantage of the break-even time (BET) method over the payback period method is that it

recognizes the time value of money.

5. In ranking choices with the break-even time (BET) method, the investment with the longest

BET gets the highest rank.

6. When computing payback period, the year in which a capital investment is made is year 1.

7. The payback period method of evaluating an investment fails to consider cash inflows after the

point where an investment’s costs are fully recovered.

8. The time value of money is considered when calculating the payback period of an investment.

9. Two investments with exactly the same payback periods are not equally valuable to an

investor because the timing of net cash flows may be different.

10. The payback period method, unlike the net present value method, does not ignore cash flows

after the point of cost recovery.

11. If two projects have the same risks, the same payback periods, and the same initial

investments, they are equally attractive.

12. A shorter payback period reduces the company’s ability to respond to unanticipated changes

and increases the risk of having to keep an unprofitable investment.

13. If the straight-line depreciation method is used, the annual average investment amount used

in calculating rate of return is calculated as (beginning book value + ending book value)/2.

14. The accounting rate of return is based on cash flows rather than net income in its calculation.

15. If net present values are used to evaluate two investments that have equal costs and equal

total cash flows, the one with more cash flows in the early years has the higher net present

value.

16. The net present value decision rule is: When an asset’s expected cash flows yield a positive

net present value when discounted at the required rate of return, the asset should be acquired.

17. The internal rate of return equals the rate that yields a net present value of zero for an

investment.

18. The internal rate of return method of evaluating capital investments cannot be used with

uneven cash flows.

19. There is only one method of evaluating capital budgeting decisions.

20. Capital budgeting decisions are risky because the outcome is uncertain, large amounts are

usually involved, the investment involves a long-term commitment, and the decision could be

difficult or impossible to reverse.

21. Capital budgeting decisions are not affected by return on investment considerations.

22. Capital budgeting decisions that relate to investments in technology are not as risky as other

types of capital budgeting decisions.

23. The time value of money concept works on the principle that a dollar today is worth more

than a dollar tomorrow.

24. The time value of money concept works on the principle that a dollar tomorrow is worth

more than a dollar today.

25. The process of restating cash flows in terms of their present values is called discounting.

26. All capital investment evaluation methods use the time value of money concept.

27. A hurdle rate is the minimum acceptable rate of return for an investment.

28. For projects financed from borrowed funds, the hurdle rate must exceed the interest rate paid

on these funds.

29. Lower-risk investments require a higher rate of return compared with higher-risk

investments.

30. Neither the net present value nor the internal rate of return methods of evaluating investments

consider the time value of money.

31. Accounting rate of return is the simplest capital budgeting method. It gives managers an

estimate of how soon they will recover their initial investment.

32. The net present value capital budgeting method considers all estimated cash flows for the

project’s expected life.

33. In ranking choices with the break-even time (BET) method, the investment with the highest

BET measure gets the highest rank.

34. Three widely used methods of comparing investment alternatives are payback period, net

present value, and rate of return on average investment.

35. The payback method of evaluating an investment fails to consider how long the investment

will generate cash inflows beyond the payback period.

36. Two investments with exactly the same payback periods are always equally valuable to an

investor.

37. A disadvantage of an investment with a short payback period is that it will produce revenue

for only a short period of time.

38. In calculating the rate of return on average investment, average investment should be

calculated as (beginning book value + ending book value)/2.

39. The accounting rate of return uses cash flows in its calculation.

40. The payback method, unlike the net present value method, does not ignore cash flows after

the point of cost recovery.

41. The calculation of annual net cash flow from a particular investment project should include

all of the following except:

A. Income taxes.

B. Revenues generated by the investment.

C. Cost of products generated by the investment.

D. Depreciation expense.

E. General and administrative expenses.

42. The process of restating future cash flows in today’s dollars is known as:

A. Budgeting.

B. Annualization.

C. Discounting.

D. Payback period.

E. Capitalizing.

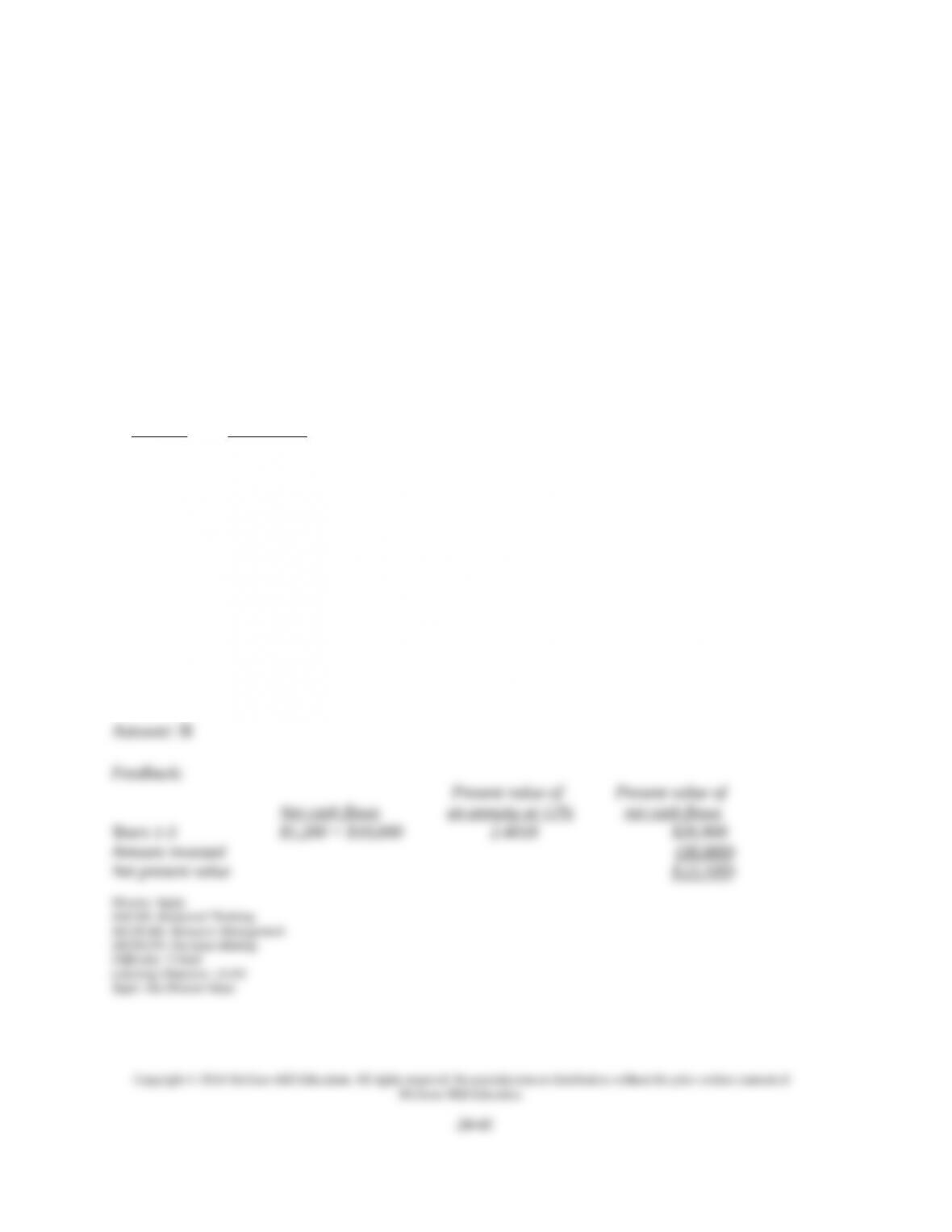

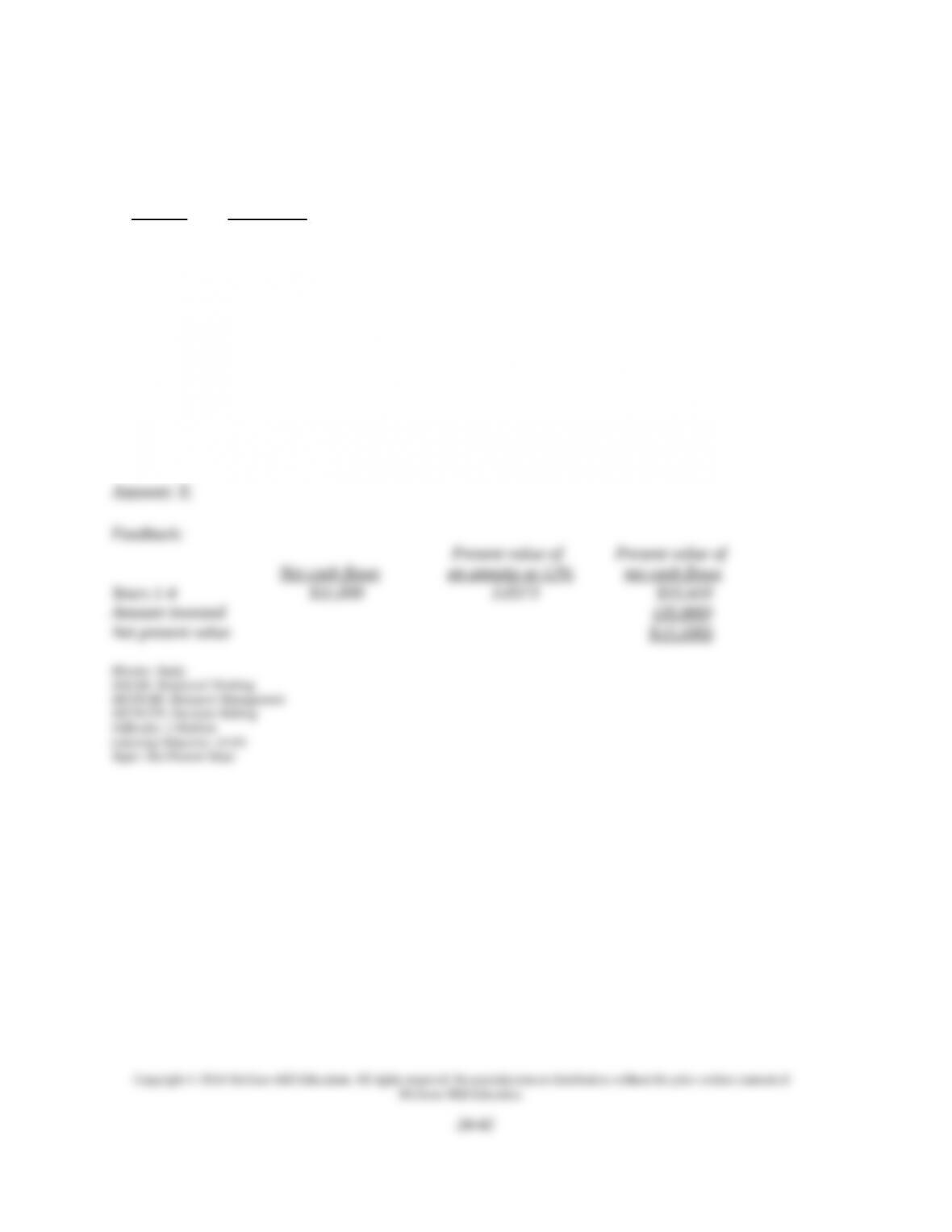

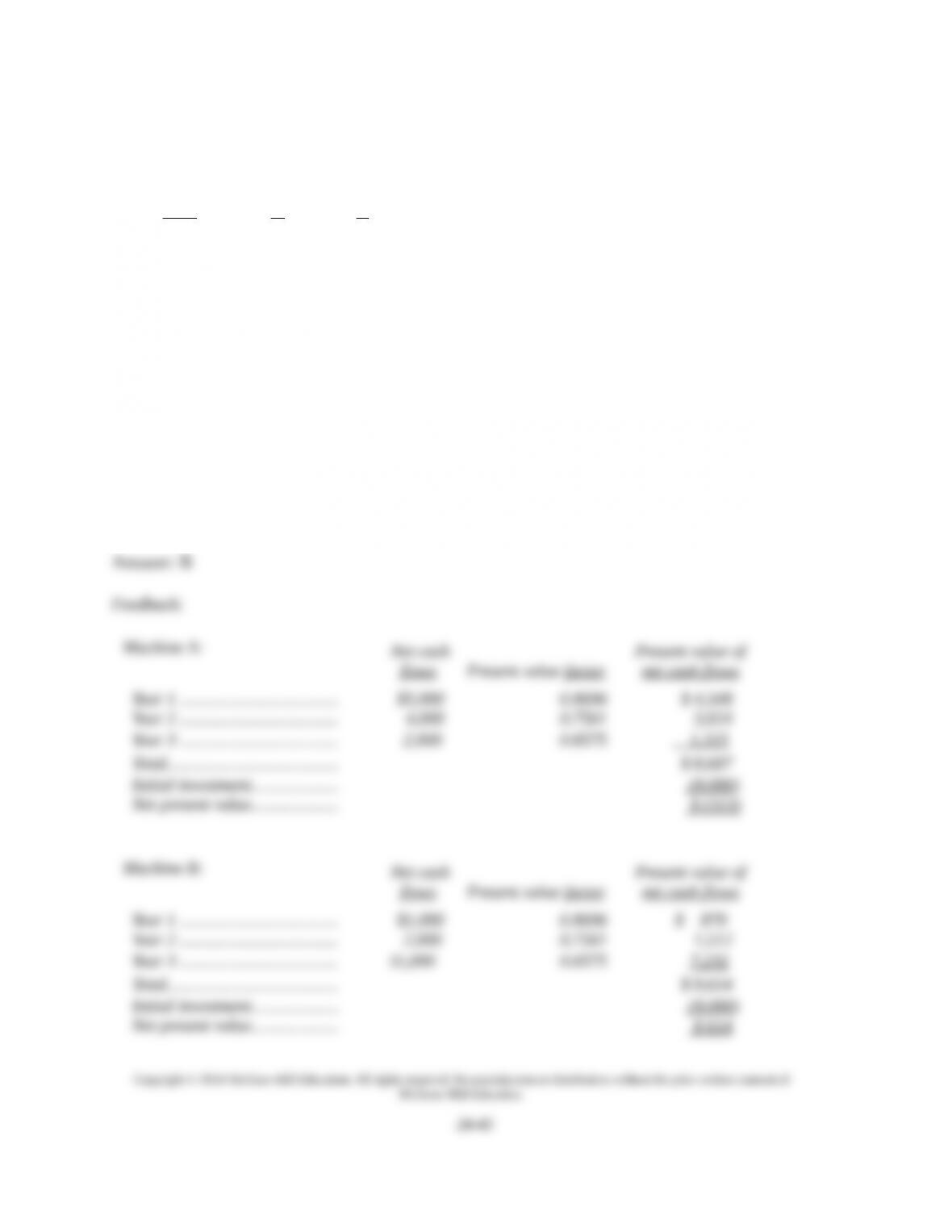

43. A the company’s required rate of return, typically its cost of capital is called the:

A. Internal rate of return.

B. Average rate of return.

C. Hurdle rate.

D. Maximum rate.

E. Payback rate.

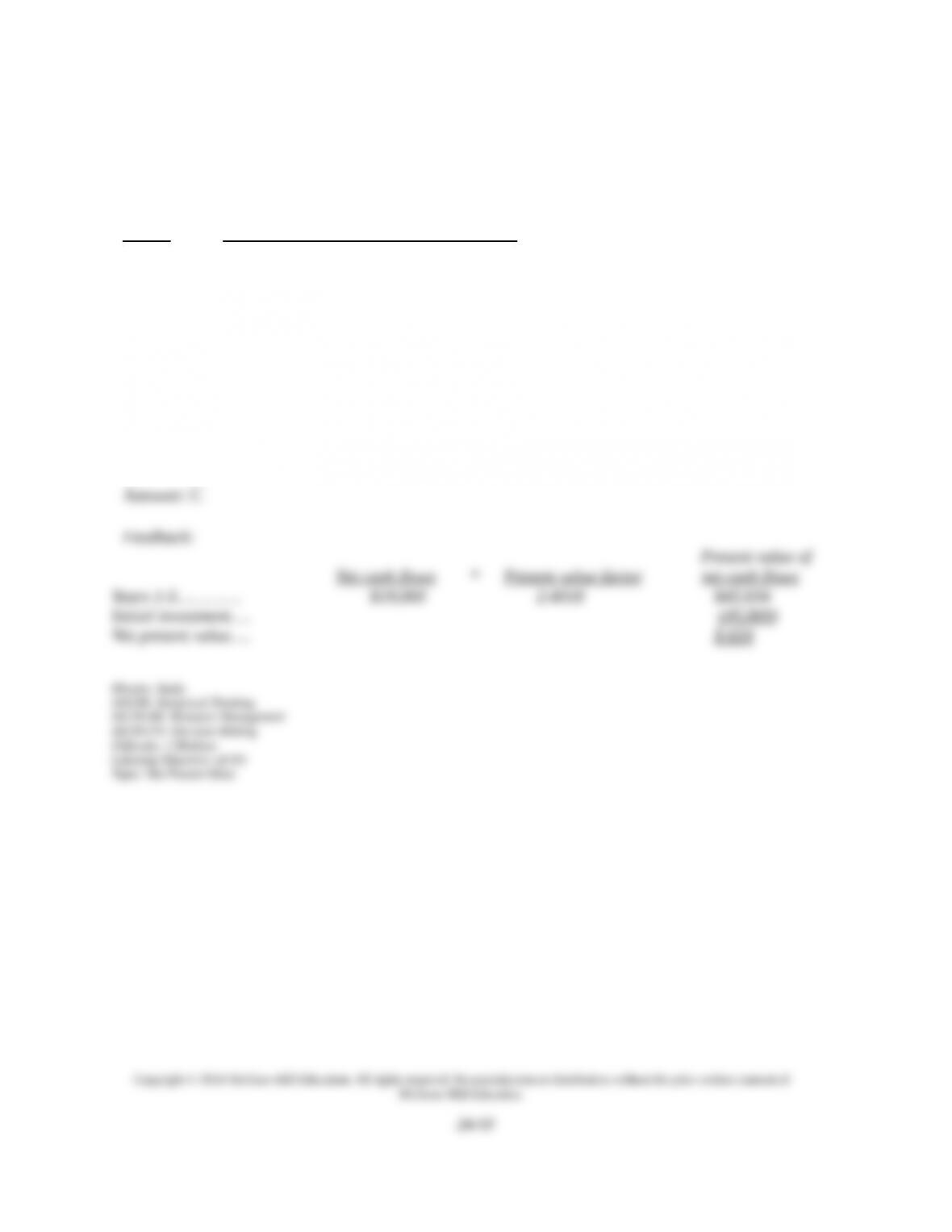

44. In business decision-making, managers typically examine the two fundamental factors of:

A. Risk and capital investment.

B. Risk and return.

C. Capital investment and rate of return.

D. Risk and payback.

E. Payback and rate of return.

45. A limitation of the internal rate of return method is that it:

A. Does not consider the time value of money.

B. Measures results in years.

C. Lacks ability to compare dissimilar projects.

D. Ignores varying risks over the life of a project.

E. Measures net income rather than cash flows.

46. The break-even time (BET) method is a variation of the:

A. Payback method.

B. Internal rate of return method.

C. Accounting rate of return method.

D. Net present value method.

E. Present value method.

47. The calculation of the payback period for an investment when net cash flow is even (equal)

is:

A. Cost of investment/Annual net cash flow

B. Cost of investment/Total net cash flow

C. Annual net cash flow/Cost of investment

D. Total net cash flow/Cost of investment

E. Total net cash flow/Annual net cash flow

48. Capital budgeting decisions usually involve analysis of:

A. Cash outflows only.

B. Short-term investments only.

C. Long-term investments only.

D. Investments with certain outcomes only.

E. Operating revenues.

49. Capital budgeting decisions are generally based on:

A. Tentative predictions of future outcomes.

B. Perfect predictions of future outcomes.

C. Results from past outcomes only.

D. Results from current outcomes only.

E. Speculation of interest rates and economic performance only.

50. The net cash flow of a particular investment project:

A. Does not take income taxes into consideration.

B. Equals the total of the inflows of the project.

C. Equals the total of the outflows of the project.

D. Does not include depreciation.

E. Is equal to operating income each period.

51. Which of the following is an objective of capital budgeting?

A. To eliminate all risk.

B. To discount all future and past cash flows.

C. To earn a satisfactory return on investment.

D. To reverse past decisions.

E. To reduce the number of investment activities.

52. The time value of money concept:

A. Means that a dollar today is worth less than a dollar tomorrow.

B. Means that a dollar tomorrow is worth more than a dollar today.

C. Means that a dollar today is worth more than a dollar tomorrow.

D. Means that “Time is money.”

E. Does not involve the concept of compound interest.

53. A minimum acceptable rate of return for an investment decision is called the:

A. Internal rate of return.

B. Average rate of return.

C. Hurdle rate of return.

D. Maximum rate of return.

E. Payback rate of return.

54. The rate that yields a net present value of zero for an investment is the:

A. Internal rate of return.

B. Accounting rate of return.

C. Net present value rate of return.

D. Zero rate of return.

E. Payback rate of return.

55. Which methods of evaluating a capital investment project ignore the time value of money?

A. Net present value and accounting rate of return.

B. Accounting rate of return and internal rate of return.

C. Internal rate of return and payback period.

D. Payback period and accounting rate of return.

E. Net present value and payback period.

56. Which methods of evaluating a capital investment project use cash flows as a measurement

basis?

A. Net present value, accounting rate of return, and internal rate of return.

B. Internal rate of return, payback period, and accounting rate of return.

C. Accounting rate of return, net present value, and payback period.

D. Payback period, internal rate of return, and net present value.

E. Net present value, payback period, accounting rate of return, and internal rate of return.

57. The internal rate of return method is not subject to the limitations of the net present value

method when comparing projects with different amounts invested because:

A. The internal rate of return is expressed as a percent rather than the absolute dollar value of

present value.

B. The internal rate of return is expressed as an absolute dollar value rather than the percent of

net present value.

C. The internal rate of return reflects the time value of money rather than the absolute dollar

value of present value.

D. The internal rate of return is expressed as an absolute dollar value rather than the time value

of money used in net present value.

E. The internal rate of return is expressed as a percent rather than the accrual income method

used in net present value.

58. A given project requires a $30,000 investment and is expected to generate end-of-period

annual cash inflows as follows:

Year 1 Year 2 Year 3 Total

$12,000 $8,000 $10,000 $30,000

Assuming a discount rate of 10%, what is the net present value of this investment? Selected

present value factors for a single sum are shown in the table below:

i = 10%

n = 1

i = 10%

n = 2

i = 10%

n = 3

.9091 .8264 .7513

A. $0.00

B. $21,000.00

C. ($7,461.00)

D. $25,033.32

E. ($4,966.68)

59. A given project requires a $28,000 investment and is expected to generate end-of-period

annual cash inflows as follows:

Year 1 Year 2 Year 3

$12,000 $13,000 $12,000

Assuming a discount rate of 10%, what is the net present value of this investment? Selected

present value factors for a single sum are shown in the table below.

i = 10%

n = 1

i = 10%

n = 2

i = 10%

n = 3

.9091 .8264 .7513

A. $0.00

B. $2,668.00

C. ($7,461.00)

D. $30,668.00

E. ($4,966.68)

60. A given project requires a $28,500 investment and is expected to generate end-of-period

annual cash inflows of $12,000 for each of three years. Assuming a discount rate of 10%, what is

the net present value of this investment? Selected present value factors for a single sum are

shown in the table below:

i = 10%

n = 1

i = 10%

n = 2

i = 10%

n = 3

.9091 .8264 .7513

A. $0.00

B. $2,668.00

C. ($7,461.00)

D. $1,341.60

E. $29,841.60

61. The break-even time (BET) method is a variation of the:

A. Payback method.

B. Internal rate of return method.

C. Accounting rate of return method.

D. Net present value method.

E. Present value method.

62. If a manager were concerned with the time value of money, from which two capital

budgeting methods should the manager choose?

A. IRR or Payback.

B. BET or IRR.

C. BET or Payback.

D. NPV or ARR.

E. NPV or Payback.

63. The calculation of the payback period for an investment when net cash flow is even (equal)

is:

A. (Cost of investment)/(Annual net cash flow)

B. (Cost of investment)/(Total net cash flow)

C. (Annual net cash flow)/(Cost of investment)

D. (Total net cash flow)/(Cost of investment)

E. (Total net cash flow)/(Annual net cash flow)

64. Coffer Co. is analyzing two projects for the future. Assume that only one project can be

selected.

Project X Project Y

Cost of

machine

$ 77,000 $55,000

Net cash flow:

Year 1 28,000 2,000

Year 2 28,000 25,000

Year 3 28,000 25,000

Year 4 0 20,000

If the company is using the payback period method and it requires a payback of three years or

less, which project should be selected?

A. Project Y.

B. Project X.

C. Both X and Y are acceptable projects.

D. Neither X nor Y is an acceptable project.

E. Project Y because it has a lower initial investment.

65. A company wishes to buy new equipment for $9,000. The equipment is expected to generate

an additional $2,800 in cash inflows for six years. All cash flows occur at year-end. A bank will

make an $9,000 loan to the company at a 10% interest rate so that the company can purchase the

equipment. Use the table below to determine break-even time for this equipment:

Year

Present Value of

1 at 10%

0 1.0000

1 0.9091

2 0.8264

3 0.7513

4 0.6830

5 0.6209

6 0.5645

A. Break-even time is between two and three years.

B. Break-even time is between three and four years.

C. Break-even time is between four and five years.

D. Break-even time is between five and six years.

E. This project will never break-even.

66. Porter Co. is analyzing two projects for the future. Assume that only one project can be

selected.

Project X Project Y

Cost of machine $68,000 $60,000

Net cash flow:

Year 1 24,000 4,000

Year 2 24,000 26,000

Year 3 24,000 26,000

Year 4

0

20,000

If the company is using the payback period method and it requires a payback of three years or

less, which project should be selected?

A. Project Y.

B. Project X.

C. Both X and Y are acceptable projects.

D. Neither X nor Y is an acceptable project.

E. Project Y because it has a lower initial investment.

67. Porter Co. is analyzing two projects for the future. Assume that only one project can be

selected.

Project X Project Y

Cost of machine $68,000 $60,000

Net cash flow:

Year 1 24,000 4,000

Year 2 24,000 26,000

Year 3 24,000 26,000

Year 4

0

20,000

The payback period in years for Project X is:

A. 2.00.

B. 3.83.

C. 3.50.

D. 2.83.

E. 4.00.

68. The expected amount of time to recover the initial amount of an investment is called the:

A. Amortization period.

B. Payback period.

C. Interest period.

D. Budgeting period.

E. Discounted cash flow period.

69. A company is considering purchasing a machine for $21,000. The machine will generate an

after-tax net income of $2,000 per year. Annual depreciation expense would be $1,500. What is

the payback period for the new machine?

A. 4 years.

B. 6 years.

C. 10.5 years.

D. 14 years.

E. 42 years.

70. A company is considering purchasing a machine for $21,000. The machine will generate an

after-tax net income of $2,000 per year. Annual depreciation expense would be $1,500. What is

the approximate accounting rate of return?

A. 19%

B. 33%

C. 17%

D. 10%

E. 25%

71. A company is considering the purchase of a new piece of equipment for $90,000. Predicted

annual cash inflows from this investment are $36,000 (year 1), $30,000 (year 2), $18,000 (year

3), $12,000 (year 4) and $6,000 (year 5). The payback period is:

A. 4.50 years.

B. 4.25 years.

C. 3.50 years.

D. 3.00 years.

E. 2.50 years.

72. A disadvantage of using the payback period to compare investment alternatives is that:

A. It ignores cash flows beyond the payback period.

B. It includes the time value of money.

C. It cannot be used when cash flows are not uniform.

D. It cannot be used if a company records depreciation.

E. It cannot be used to compare investments with different initial investments.

73. A company is considering the purchase of a new machine for $48,000. Management predicts

that the machine can produce sales of $16,000 each year for the next 10 years. Expenses are

expected to include direct materials, direct labor, and factory overhead totaling $12,000 per year

including depreciation of $3,000 per year. The company’s tax rate is 40%. What is the payback

period for the new machine?

A. 20.0 years.

B. 6.0 years.

C. 7.5 years.

D. 12.0 years.

E. 8.9 years.

74. A company is considering the purchase of a new machine for $48,000. Management predicts

that the machine can produce sales of $16,000 each year for the next 10 years. Expenses are

expected to include direct materials, direct labor, and factory overhead totaling $8,000 per year

plus depreciation of $4,000 per year. The company's tax rate is 40%. What is the approximate

accounting rate of return for the machine?

A. 13%.

B. 17%

C. 8%

D. 27%

E. 10%

75. A company is planning to purchase a machine that will cost $24,000, have a six-year life, and

be depreciated over a three-year period with no salvage value. The company expects to sell the

machine’s output of 3,000 units evenly throughout each year. A projected income statement for

each year of the asset’s life appears below. What is the payback period for this machine?

Sales………………………………………… $90,000

Costs:

Manufacturing……………………………… $52,000

Depreciation on machine…………………… 4,000

Selling and administrative expenses……….. 30,000 (86,000)

Income before taxes………………………... $ 4,000

Income tax (50%)…………………………... ( 2,000 )

Net income…………………………………. $ 2,000

A. 24 years.

B. 12 years.

C. 6 years.

D. 4 years.

E. 1 year.

76. A company is planning to purchase a machine that will cost $24,000, have a six-year life,

and be depreciated over a three-year period with no salvage value. The company expects to sell

the machine’s output of 3,000 units evenly throughout each year. A projected income statement

for each year of the asset’s life appears below. What is the accounting rate of return for this

machine?

Sales………………………………………… $90,000

Costs:

Manufacturing……………………………… $52,000

Depreciation on machine…………………… 4,000

Selling and administrative expenses……….. 30,000 (86,000)

Income before taxes………………………... $ 4,000

Income tax (50%)…………………………... (2,000)

Net income…………………………………. $ 2,000

A. 33.3%.

B. 16.7%.

C. 50.0%.

D. 8.3%.

E. 4%.

77. After-tax net income divided by the average amount invested in a project, is the:

A. Net present value rate.

B. Payback rate.

C. Accounting rate of return.

D. Earnings from investment.

E. Profit rate.

78. A company buys a machine for $60,000 that has an expected life of 9 years and no salvage

value. The company anticipates a yearly net income of $2,850 after taxes of 30%, with the cash

flows to be received evenly throughout each year. What is the accounting rate of return?

A. 2.85%.

B. 4.75%.

C. 6.65%.

D. 9.50%.

E. 42.75%.

79. A company buys a machine for $76,000 that has an expected life of 6 years and no salvage

value. The company anticipates a yearly after tax net income of $1,805. What is the accounting

rate of return?

A. 2.85%.

B. 4.75%.

C. 6.65%.

D. 9.50%.

E. 42.75%.

80. Carmel Corporation is considering the purchase of a machine costing $36,000 with a 6-year

useful life and no salvage value. Carmel uses straight-line depreciation and assumes that the

annual cash inflow from the machine will be received uniformly throughout each year. In

calculating the accounting rate of return, what is Carmel’s average investment?

A. $ 6,000.

B. $ 7,000.

C. $18,000.

D. $21,000.

E. $36,000.

81. Watson Corporation is considering buying a machine for $25,000. Its estimated useful life is

5 years, with no salvage value. Watson anticipates annual net income after taxes of $1,500 from

the new machine. What is the accounting rate of return assuming that Watson uses straight-line

depreciation and that income is earned uniformly throughout each year?

A. 6.0%.

B. 8.0%.

C. 8.5%.

D. 10.0%.

E. 12.0%.

82. The accounting rate of return is calculated as:

A. The after-tax income divided by the total investment.

B. The after-tax income divided by the annual average investment.

C. The cash flows divided by the annual average investment.

D. The cash flows divided by the total investment.

E. The annual average investment divided by the after-tax income.

83. The following data concerns a proposed equipment purchase:

Cost........................................................................................ $144,000

Salvage value......................................................................... $ 4,000

Estimated useful life ............................................................ 4 years

Annual net cash flows........................................................... $ 46,100

Depreciation method............................................................. Straight-line

Assuming that net cash flows are received evenly throughout the year, the accounting rate of

return is:

A. 62.3%.

B. 32.0%.

C. 15.0%.

D. 7.7%.

E. 5.0%.

84. The following data concerns a proposed equipment purchase:

Cost........................................................................................ $144,000

Salvage value......................................................................... $ 4,000

Estimated useful life ............................................................ 4 years

Annual net cash flows........................................................... $ 46,100

Depreciation method............................................................. Straight-line

The annual average investment amount used to calculate the accounting rate of return is:

A. $72,000

B. $70,000

C. $37,000

D. $74,000

E. $48,950

85. An estimate of an asset’s value to the company, calculated by discounting the future cash

flows from the investment at the project’s required rate of return and then subtracting the initial

amount of the investment, is known as:

A. Annual net cash flows.

B. Rate of return on investment.

C. Net present value.

D. Payback period.

E. Unamortized carrying value.

86. Which of the following cash flows is not considered when using the net present value

method?

A. Future cash inflows.

B. Future cash outflows.

C. Past cash outflows.

D. Non-uniform cash inflows.

E. Future year-end cash flows.

87. Which one of the following methods considers the time value of money in evaluating

alternative capital expenditures?

A. Accounting rate of return.

B. Net present value.

C. Payback period.

D. Cash flow method.

E. Return on average investment.

88. The hurdle rate is often set at:

A. The rate the company could earn if the investment were placed in the bank.

B. The company’s cost of capital.

C. 10% above the IRR of current projects.

D. 10% above the ARR of current projects.

E. The rate at which the company is taxed on income.

89. Butler Corporation is considering the purchase of new equipment costing $30,000. The

projected annual after-tax net income from the equipment is $1,200, after deducting $10,000 for

depreciation. The revenue is to be received at the end of each year. The machine has a useful life

of 3 years and no salvage value. Butler requires a 12% return on its investments. The present

value of an annuity of 1 for different periods follows:

Periods 12 Percent

1............ 0.8929

2............ 1.6901

3............ 2.4018

4............

3.0373

What is the net present value of the machine?

A. $24,018.

B. $(3,100).

C. $30,000.

D. $26,900.

E. $(29,520).

90. Vextra Corporation is considering the purchase of new equipment costing $35,000. The

projected annual cash inflow is $11,000, to be received at the end of each year. The machine has

a useful life of 4 years and no salvage value. Vextra requires a 12% return on its investments.

The present value of an annuity of $1 for different periods follows:

Periods 12 Percent

1............ 0.8929

2............ 1.6901

3............ 2.4018

4............

3.0373

What is the net present value of the machine (rounded to the nearest whole dollar)?

A. $(33,410).

B. $(3,100).

C. $35,000.

D. $3,410.

E. $(1,590).

91. The following present value factors are provided for use in this problem.

Periods

Present Value Present Value of an

of 1 at 8% Annuity of 1 at 8%

1.................... 0.9259 0.9259

2................... 0.8573 1.7833

3.................... 0.7938 2.5771

4................... 0.7350 3.3121

Cliff Co. wants to purchase a machine for $40,000, but needs to earn an 8% return. The expected

year-end net cash flows are $12,000 in each of the first three years, and $16,000 in the fourth

year. What is the machine’s net present value (round to the nearest whole dollar)?

A. $(9,075).

B. $2,685.

C. $42,685.

D. $(28,240).

E. $52,000.

92. The following present value factors are provided for use in this problem.

Periods

Present Value Present Value of an

of $1 at 8% Annuity of $1 at 8%

1.................... 0.9259 0.9259

2................... 0.8573 1.7833

3.................... 0.7938 2.5771

4................... 0.7350 3.3121

Xavier Co. wants to purchase a machine for $37,000 with a four year life and a $1,000 salvage

value. Xavier requires an 8% return on investment. The expected year-end net cash flows are

$12,000 in each of the four years. What is the machine’s net present value (round to the nearest

whole dollar)?

A. $3,480

B. $2,745.

C. $40,480.

D. $(3,480).

E. $(2,745).

93. Turk Manufacturing is considering purchasing two machines. Each machine costs $9,000 and

will produce cash flows as follows:

End of Machine

Year A B

1.................. $5,000 $1,000

2................. 4,000 2,000

3.................. 2,000 11,000

Turk Manufacturing uses the net present value method to make the decision, and it requires a

15% annual return on its investments. The present value factors of 1 at 15% are: 1 year, 0.8696;

2 years, 0.7561; 3 years, 0.6575. Which machine should Turk purchase?

A. Only Machine A is acceptable.

B. Only Machine B is acceptable.

C. Both machines are acceptable, but A should be selected because it has the greater net present

value.

D. Both machines are acceptable, but B should be selected because it has the greater net present

value.

E. Neither machine is acceptable.

94. Alfarsi Industries uses the net present value method to make investment decisions and

requires a 15% annual return on all investments. The company is considering two different

investments. Each require an initial investment of $15,000 and will produce cash flows as

follows:

End of Investment

Year A B

1.................. $8,000 $0

2................. 8,000 0

3.................. 8,000 24,000

The present value factors of $1 each year at 15% are:

1 ……………..0.8696

2 ……………. 0.7561

3 ……………. 0.6575

The present value of an annuity of $1for 3 years at 15% is 2.2832

Which investment should Alfarsi choose?

A. Only Investment A is acceptable.

B. Only Investment B is acceptable.

C. Both investments are acceptable, but A should be selected because it has the greater net

present value.

D. Both investments are acceptable, but B should be selected because it has the greater net

present value.

E. Neither machine is acceptable.

95. Alfarsi Industries uses the net present value method to make investment decisions and

requires a 15% annual return on all investments. The company is considering two different

investments. Each require an initial investment of $15,000 and will produce cash flows as

follows:

End of Investment

Year A B

1.................. $8,000 $0

2................. 8,000 0

3.................. 8,000 24,000

The present value factors of $1 each year at 15% are:

1 ……………..0.8696

2 ……………. 0.7561

3 ……………. 0.6575

The present value of an annuity of $1 for 3 years at 15% is 2.2832

The net present value of Investment A is:

A. $18,266.

B. $(15,000).

C. $9,000.

D. $(20,549).

E. $3,266.

96. Alfarsi Industries uses the net present value method to make investment decisions and

requires a 15% annual return on all investments. The company is considering two different

investments. Each require an initial investment of $15,000 and will produce cash flows as

follows:

End of Investment

Year A B

1.................. $8,000 $0

2................. 8,000 0

3.................. 8,000 24,000

The present value factors of $1 each year at 15% are:

1 ……………..0.8696

2 ……………. 0.7561

3 ……………. 0.6575

The present value of an annuity of $1for 3 years at 15% is 2.2832

The net present value of Investment B is:

A. $780.

B. $(15,780).

C. $9,000.

D. $39,797

E. $(5,918).

97. A company is considering the purchase of new equipment for $45,000. The projected annual

net cash flows are $19,000. The machine has a useful life of 3 years and no salvage value.

Management of the company requires a 12% return on investment. The present value of an

annuity of 1 for various periods follows:

Period Present value of an annuity of 1 at 12%

1……. 0.8929

2……. 1.6901

3……. 2.4018

What is the net present value of this machine assuming all cash flows occur at year-end?

A. $(1,768)

B. $3,000

C. $634

D. $19,000

E. $45,634

98. A company can buy a machine that is expected to have a three-year life and a $30,000

salvage value. The machine will cost $1,800,000 and is expected to produce a $200,000 after-tax

net income to be received at the end of each year. If a table of present values of 1 at 12% shows

values of 0.8929 for one year, 0.7972 for two years, and 0.7118 for three years, what is the net

present value of the cash flows from the investment, discounted at 12%?

A. $ 118,855

B. $ 583,676

C. $ 629,788

D. $ 705,391

E. $1,918,855

99. A company is considering a 5-year project. The company plans to invest $60,000 now and it

forecasts cash flows for each year of $16,200. The company requires a hurdle rate of 12%.

Calculate the internal rate of return to determine whether it should accept this project. Selected

factors for a present value of an annuity of 1 for five years are shown below:

Present value of an annuity

Interest rate of $1 factor for year 5

10% 3.7908

12% 3.6048

14% 3.4331

A. The project should be accepted.

B. The project should be rejected because it earns less than 10%.

C. The project earns more than 10% but less than 12%. At a hurdle rate of 12%, the project

should be rejected.

D. Only 9% is acceptable.

E. Only 10% is acceptable.

100. Tressor Company is considering a 5-year project. The company plans to invest $90,000 now

and it forecasts cash flows for each year of $27,000. The company requires that investments

yield a discount rate of at least 14%. Selected factors for a present value of an annuity of 1 for

five years are shown below:

Present value of an annuity

Interest rate of $1 factor for year 5

10% 3.7908

12% 3.6048

14% 3.4331

Calculate the internal rate of return to determine whether it should accept this project.

A. The project should be accepted because it will earn more than 14%.

B. The project should be accepted because it will earn more than 10%.

C. The project will earn more than 12% but less than 14%. At a hurdle rate of 14%, the project

should be rejected.

D. The project should be rejected because it will earn less than 14%.

E. The project should be rejected because it will not earn exactly 14%.

101. A new manufacturing machine is expected to cost $278,000, have an eight-year life, and a

$30,000 salvage value. The machine will yield an annual incremental after-tax income of

$35,000 after deducting the straight-line depreciation. Compute the payback period for the

purchase.

A. 8.7 years.

B. 3.8 years.

C. 4.2 years.

D. 7.3 years.

E. 5.4 years.

102. A new manufacturing machine is expected to cost $278,000, have an eight-year life, and a

$30,000 salvage value. The machine will yield an annual incremental after-tax income of

$35,000 after deducting the straight-line depreciation. Compute the accounting rate of return for

the investment.

A. 22.7%.

B. 23.4%.

C. 46.9%.

D. 12.2%.

E. 24.5%.

103. Nestor Company is considering the purchase of an asset for $100,000. It is expected to

produce the following net cash flows. The cash flows occur evenly throughout each year.

Annual Net

Cash Flows

Year 1 $40,000

Year 2 $40,000

Year 3 $35,000

Year 4 $35,000

Year 5 $30,000

Compute the payback period for this investment. (Round to two decimal places.)

A. 2.85 years.

B. 2.57 years.

C. 3.00 years.

D. 2.50 years.

E. 3.62 years.

104. A machine costs $180,000 and will have an eight-year life, a $20,000 salvage value, and

straight-line depreciation is used. Management estimates the machine will yield an after-tax net

income of $12,500 each year.. Compute the accounting rate of return for the investment.

A. 12.5%.

B. 26.8%.

C. 11.8%.

D. 10.8%.

E. 22.5%.

105. Poe Company is considering the purchase of new equipment costing $80,000. The projected

annual cash inflows are $30,200, to be received at the end of each year. The machine has a useful

life of 4 years and no salvage value. Poe requires a 10% return on its investments. The present

value of an annuity of 1 and present value of an annuity for different periods is presented below.

Compute the net present value of the machine.

Present Value Present Value of an

Periods of 1 at 10% Annuity of 1 at 10%

1................... 0.9091 0.9091

2................... 0.8264 1.7355

3................... 0.7513 2.4869

4................... 0.6830 3.1699

A. $(15,731).

B. $(4,896).

C. $15,731.

D. $4,896.

E. $32,334.

106. Poe Company is considering the purchase of new equipment costing $80,000. The projected

net cash flows are $35,000 for the first two years and $30,000 for years three and four. The

revenue is to be received at the end of each year. The machine has a useful life of 4 years and no

salvage value. Poe requires a 10% return on its investments. The present value of an annuity of

1 and present value of an annuity for different periods is presented below. Compute the net

present value of the machine.

Present Value Present Value of an

Periods of 1 at 10% Annuity of 1 at 10%

1................... 0.9091 0.9091

2................... 0.8264 1.7355

3................... 0.7513 2.4869

4................... 0.6830 3.1699

A. $(15,731).

B. $(4,896).

C. $15,731.

D. $4,896.

E. $23,775.

107. Nestor Company is considering the purchase of an asset for $100,000. It is expected to

produce the following net cash flows. The cash flows occur evenly throughout each year.

Compute the break-even time (BET) period for this investment. (Round to two decimal places.)

Annual Net

Cash Flows

Present

Value of 1

at 10%

Year 0 1.0000

Year 1 $40,000 .9091

Year 2 $40,000 .8264

Year 3 $35,000 .7513

Year 4 $35,000 .6830

Year 5 $30,000 .6209

A. 2.85 years.

B. 2.57 years.

C. 3.17 years.

D. 2.98 years.

E. 3.62 years.

108. Capital budgeting is the process of analyzing:

A. Cash outflows only.

B. Short-term investments.

C. Long-term investments.

D. Investments with certain outcomes only.

E. Operating revenues.

109. The process of analyzing alternative long-term investments and deciding which assets to

acquire or sell is known as:

A. Planning and control.

B. Capital budgeting.

C. Variance analysis.

D. Master budgeting.

E. Managerial accounting.

110. Capital budgeting decisions are risky because all of the following are true except:

A. The outcome is uncertain.

B. Large amounts of money are usually involved.

C. The investment involves a long-term commitment.

D. The decision could be difficult or impossible to reverse.

E. They rarely produce net cash flows.

113. Presented below are terms preceded by letters a through g and followed by a list of

definitions 1 through 7. Match the letter of the term with the definition. Use the space provided

preceding each definition.

(a) Internal Rate of Return

(b) Hurdle Rate

(c) Accounting Rate of Return

(d) Net Cash Flow

(e) Capital Budgeting

(f) Payback Period

(g) Net Present Value

______ (1) Equals the discount rate that results in a net present value of zero.

______ (2) Cash inflows minus cash outflows for the period.

______ (3) A minimum acceptable rate of return.

______ (4) The time expected to pass before the net cash flows from an investment equals its

initial cost.

______ (5) Annual after-tax net income divided by annual average investment.

______ (6) A process of analyzing alternative long-term investments and deciding which assets

to acquire or sell.

______ (7) Initial cost of an investment subtracted from discounted future cash flows from the

investment.

1. A; 2. D; 3. B; 4. F; 5. C; 6. E; 7. G

Blooms: Remember

AACSB: Analytical Thinking

AICPA BB: Resource Management

AICPA FN: Decision Making

Difficulty: 1 Easy

Learning Objective: 24-P1

Learning Objective: 24-P2

Learning Objective: 24-P3

Learning Objective: 24-P4

Topic: Payback Period

Topic: Accounting Rate of Return

Topic: Net Present Value

Topic: Internal Rate of Return

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

24-62

114. Presented below are terms preceded by letters a through f and followed by a list of

definitions 1 through 6. Match the letter of the terms with the definitions. Use the space provided

preceding each definition.

(a) Sunk cost

(b) Opportunity cost

(c) Out-of-pocket cost

(d) Net present value

(e) Incremental cost

(f) Annuity

______ (1) A cost that requires a future outlay of cash and is relevant for current and future

decision making.

______ (2) A series of cash flows of equal dollar amount over equal time periods.

______ (3) An estimate of an asset’s value to the company; computed by discounting the future

net cash flows from the investment the project’s required rate of return and then subtracting the

initial amount invested.

______ (4) A cost that cannot be avoided or changed because it arises from past decision;

irrelevant to future decisions.

______ (5) An additional cost incurred if a company pursues a certain course of action.

______ (6) The potential benefits lost by taking a specific action when two or more alternative

choices are available.

1. C; 2. F; 3. D; 4. A; 5. E; 6. B

Blooms: Remember

AACSB: Analytical Thinking

AICPA BB: Resource Management

AICPA FN: Decision Making

Difficulty: 1 Easy

Learning Objective: 24-P2

Learning Objective: 24-P3

Topic: Accounting Rate of Return

Topic: Net Present Value

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

24-63

Short Answer Questions

115. What is capital budgeting? Why are capital budgeting decisions often difficult and risky?

116. Briefly describe the time value of money. Why is the time value of money important in

capital budgeting?

117. In using a capital budgeting method that takes the time value of money into consideration,

management must consider a hurdle rate in making its decisions. What is a hurdle rate? What

factors does management have to consider in selecting a hurdle rate?

118. How does the calculation of break-even time (BET) differ from the calculation of payback

period (PBP)?

119. Briefly describe both the payback period method and the net present value method of

comparing investment alternatives.

120. When making capital budgeting decisions, companies usually prefer shorter payback

periods. Explain why shorter payback periods are desirable.

121. What is one advantage and one disadvantage of using the accounting rate of return to

evaluate investment alternatives?

122. You have evaluated three projects of similar investment amount and risk using the net

present value (NPV) method. How would you decide which one of the projects to select?

123. When the amount invested differs substantially across projects, NPV is of limited value for

comparison purposes. You have evaluated three projects of substantially different investment

amounts using the net present value (NPV) method. How would you decide which one of the

projects to select?

124. Identify at least three reasons for managers to favor the internal rate of return (IRR) over

other capital budgeting approaches.

125. For each of the capital budgeting methods listed below, place an X in the correct column,

indicating the measurement basis of each, the ability to make comparison among projects, and

whether each method reflects or ignores the time value of money.

Measurement Basis

Comparison among

projects Time value of money

Cash

flows

Accrual

income

Allows

comparison

Difficult

to

compare

Reflects

time value

of money

Ignores

time value

of money

Payback period

Accounting rate of

return

Net present value

_

Internal rate of

return

126. Nebraska Co. is reviewing a capital investment of $100,000. This project’s projected cash

flows over a five-year period are estimated at $35,000 each year.

Required:

(a) Calculate the payback period.

(b) Calculate the break-even time. Assume a 12% hurdle rate and use the table below:

Present Value

Periods of 1 at 12%

1…… 0.8929

2…… 0.7972

3…… 0.7118

4…… 0.6355

5…… 0.5674

(c) Using the results in (a) and (b), make a recommendation for the project.

127. A company is considering purchasing a machine for $85,000. The machine is expected to

generate a net after-tax income of $11,250 per year. Depreciation expense would be $8,500.

What is the payback period for this machine?

128. A company is trying to decide which of two new product lines to introduce in the coming

year. The predicted revenue and cost data for each product line follows:

Product A Product B

Sales............................................................. $80,000 $96,000

Direct materials........................................... 3,000 6,000

Direct labor.................................................. 30,000 45,000

Other cash operating expenses................... 7,500 9,000

New equipment costs.................................. 75,000 100,000

Estimated useful life (no salvage).............. 5 years 5 years

The company has a 30% tax rate, it uses the straight-line depreciation method, and it predicts that

cash flows will be spread evenly throughout each year. Calculate each product’s payback period.

If the company requires a payback period of three years or less, which, if either, product should

be chosen?

129. A company is considering a proposal to invest $40,000 in a project that would provide the

following net cash flows:

Year 1............................................... $ 6,500

Year 2.................................................. 12,700

Year 3.................................................. 15,000

Year 4.................................................. 12,800

Compute the project’s payback period.

131. A company is evaluating the purchase of a machine for $750,000 with a six-year useful life

and no salvage value. The company uses straight-line depreciation and it assumes that the annual

net cash flow from using the machine will be received uniformly throughout each year. In

calculating the accounting rate of return, what is the company’s average investment?

132. A company purchases a machine for $800,000. The machine has an expected life of 9 years

and no salvage value. The company anticipates a yearly after-tax net income of $60,000 to be

received uniformly throughout each year. What is the accounting rate of return?

133. A company is considering two projects, Project A and Project B. The following information

is available for each project:

Project A Project B

Investment.............................................. $500,000 $2,000,000

Net present value of cash flows …… $600,000 $800,000

Calculate the profitability index for each project. Based on the profitability index, which project,

if any, should the company pursue and why?

135. A company is considering the purchase of new equipment for $42,000. The projected annual

cash inflow is $18,000. The machine has a useful life of 3 years and no salvage value.

Management of the company requires a 12% return on investment. The present value of an

annuity of $1 for various periods follows:

Period

Present value of an annuity of 1 at 12%

1.......

0.8929

2....... 1.6901

3.......

2.4018

What is the net present value of this machine assuming all cash flows occur at year-end?

136. A company is trying to decide which of two new product lines to introduce in the coming

year. The company requires a 12% return on investment. The predicted revenue and cost data for

each product line follows:

Product A Product B

Unit sales..................................................... 25,000 20,000

Unit sales price............................................ $ 30 $ 30

Direct materials........................................... $ 15,000 $ 8,000

Direct labor.................................................. $ 120,000 $ 80,000

Other cash operating expenses................... $ 30,000 $ 25,000

New equipment costs.................................. $2,500,000 $1,500,000

Estimated useful life (no salvage).............. 5 years 5 years

The company has a 30% tax rate and it uses the straight-line depreciation method. The present

value of an annuity of 1 for 5 years at 12% is 3.6048. Compute the net present value for each

piece of equipment under each of the two product lines. Which, if either of these two investments

is acceptable?

137. A company is considering two alternative investment opportunities, each of which requires

an initial cash outlay of $110,000. The expected net cash flows from the two projects follow:

Project A Project Z

Year 1 ……………… $ 30,000 $ 44,000

Year 2 ……………… 44,000 70,000

Year 3 ……………… 70,000

30,000

Totals ………………....... $144 ,000 $144,000

Required:

(1) Based on a comparison of their net present values, and assuming the same discount rate

(greater than zero) is required for both projects, which project is the better investment? (2) Use

the table values below to find the net present value of the cash flows associated with Project A,

discounted at 12%:

Periods Present value of 1 at 12%

1………………. 0.8929

2………………. 0.7972

3………………. 0.7118

138. A company has a decision to make between two investment alternatives. The company

requires a 10% return on investment. Predicted data is provided below:

Investment A Investment Z

Projected after-tax net income.................................... $ 40,000 $ 42,000

Investment costs.......................................................... $600,000 $675,000

Estimated life .............................................................. 6 years 6 years

The present value of an annuity for 6 years at 10% is 4.3553. This company uses straight-line

depreciation.

Required:

(a) Calculate the net present value for each investment.

(b) Which investment should this company select? Explain.

139. A company is considering a 5-year project. It plans to invest $62,000 now and it forecasts

cash flows for each year of $16,200. The company requires a hurdle rate of 12%. Calculate the

internal rate of return to determine whether it should accept this project. Selected factors for a

present value of an annuity of 1 for five years are shown below:

Interest rate

Present value of an annuity of 1 factor

10%

3.7908

12% 3.6048

14%

3.4331

140. Dracor Company is considering the purchase of equipment that would allow the company to

add a new product to its line. The equipment is expected to cost $280,000 with a 7-year life, no

salvage value, and will be depreciated using straight-line depreciation. The expected annual

income related to this equipment follows. Compute the (a) payback period and (b) accounting

rate of return for this equipment.

Sales............................................................. $900,000

Costs:

Manufacturing............................................. $545,000

Depreciation on machine............................. 40,000

Selling and administrative expenses............ 249,000 (834,000)

Income before taxes..................................... 66,000

Income tax (30%)........................................ ( 19,800)

Net income................................................... $ 46,200

141. Trevoline Company is deciding between two projects. Each project requires an initial

investment of $350,000. The projected net cash flows for the two projects are listed below. The

revenue is to be received at the end of each year. Trevoline requires a 10% return on its

investments. The present value of an annuity of 1 and present value of an annuity factors for

10% are presented below. Use net present value to determine which project should be pursued

and explain why.

Project A Project B Present Value Present Value of an

Periods Cash Flows Cash Flows of 1 at 10% Annuity of 1 at 10%

1................... $50,000 $160,000 0.9091 0.9091

2................... $200,000 $175,000 0.8264 1.7355

3................... $250,000 $175,000 0.7513 2.4869

142. _____________________ is the process of analyzing alternative long-term investments and

deciding which assets to acquire or sell.

143. The minimum acceptable rate of return on an investment, often the company’s cost of

capital, is called the _________________.

144. A capital budgeting method that considers how quickly a project recovers costs is known as

______________. An enhancement to this method that also considers the time value of money

is called ____________.

145. In evaluating capital budgeting alternatives, there are two primary methods that do not

consider the time value of money. These methods are _______________ and

__________________. There are also two primary methods that consider the time value of

money; these are ___________________ and _______________________.

146. The ____________________ is computed by dividing a project’s annual after-tax net

income by the annual average amount invested.

147. The ___________ is computed by discounting the future net cash flows from the investment

at the project’s required rate of return and then subtracting the initial amount invested.

148. The net present value decision rule requires that when an asset’s expected cash flows are

discounted at the required rate and yield a positive net present value, the project should be

____________________.

149. The __________________________ is the rate that yields a net present value of zero for an

investment.