Chapter 23

Relevant Costing for Managerial Decisions

1. An opportunity cost is the potential benefit lost by taking a specific action when two or more

alternative choices are available.

2. A sunk cost will change with a future course of action.

3. An out-of-pocket cost requires a future outlay of cash and is relevant for current and future

decision making.

4. Another name for relevant cost is unavoidable cost.

5. Relevant benefits refer to the additional or incremental revenue generated by selecting a

particular course or action over another.

6. Significant sunk costs are relevant to decisions about the future.

7. The concept of incremental cost is the same as the concept of differential cost.

8. Additional business in the form of a special order of goods or services should be accepted

when the incremental revenue equals the incremental costs.

9. In a make or buy decision, management should focus on costs that are the same under the two

alternatives.

10. Part of the decision to accept additional business should be based on a comparison of the

incremental (differential) costs of the added production with the additional revenues to be

received.

11. Incremental costs should be considered in a make or buy decision.

12. If a company has the capacity to produce either 10,000 units of Product A or 10,000 units of

Product B; assuming fixed costs are the same, production restrictions are the same for both

products, and the markets for both products are unlimited; the company should commit 100% of

its capacity to the product that has the higher contribution margin.

13. The decision to accept an additional volume of business should be based on a comparison of

the revenue from the additional business with the sunk costs of producing that revenue.

14. Most financial measures of revenues and costs from accounting systems are based on

historical costs.

15. Wages from a job a student gives up to attend summer school would be a sunk cost.

16. The cost of equipment purchased by a company last year would be an avoidable cost.

17. A special order of goods or services should always be accepted when the incremental revenue

exceeds the normal revenue.

18. The decision to accept additional business should be based on a comparison of the

incremental (differential) costs of the added production with the additional revenues to be

received.

19. The total cost method determines a selling price equal to a product’s total costs plus a desired

profit on the product.

20. A markup percentage equals total costs divided by desired profit.

21. Incremental costs are also called out-of-pocket costs.

22. Additional costs incurred if a company pursues a certain course of action are sunk costs.

23. If accepting additional business would cause existing sales to decline, the offer should always

be declined.

24. Contribution margin lost from a decline in sales is an opportunity cost.

25. Additional power for operating machines, extra supplies, and added cleanup costs are

examples of incremental overhead costs.

26. Employee morale, timeliness of delivery, and the reactions of customers are examples of

nonfinancial factors that should be considered when making a managerial decision.

27. Costs already incurred in manufacturing the units of a product that do not meet quality

standards are relevant costs in a scrap or rework decision.

28. Sales mix refers to the combination of products sold by a company.

29. To maximize profit when a constrained resource exists, management should produce the sales

mix that has the highest contribution margin per unit of scarce resource.

30. An opportunity cost:

A. Is an unavoidable cost because it remains the same regardless of the alternative chosen.

B. Requires a current outlay of cash.

C. Results from past managerial decisions.

D. Is the potential benefit lost by choosing a specific alternative course of action among two or

more.

E. Is irrelevant in decision making because it occurred in the past.

31. The potential benefits lost by taking a specific action when two or more alternative choices

are available is known as a(n):

A. Alternative cost.

B. Sunk cost.

C. Out-of-pocket cost.

D. Differential cost.

E. Opportunity cost.

32. A cost that requires a future outlay of cash, and is relevant for current and future decision

making, is a(n):

A. Out-of-pocket cost.

B. Sunk cost.

C. Opportunity cost.

D. Operating cost.

E. Uncontrollable cost.

33. A cost that cannot be avoided or changed because it arises from a past decision, and is

irrelevant to future decisions, is called a(n):

A. Uncontrollable cost.

B. Incremental cost.

C. Opportunity cost.

D. Out-of-pocket cost.

E. Sunk cost.

34. A company paid $200,000 ten years ago for a specialized machine that has no salvage value

and is being depreciated at the rate of $10,000 per year. The company is considering using the

machine in a new project that will have incremental revenues of $28,000 per year and annual

cash expenses of $20,000. In analyzing the new project, the $200,000 original cost of the

machine is an example of a(n):

A. Incremental cost.

B. Opportunity cost.

C. Variable cost.

D. Sunk cost.

E. Out-of-pocket cost.

35. An additional cost incurred only if a company pursues a particular course of action is a(n):

A. Period cost.

B. Pocket cost.

C. Discount cost.

D. Incremental cost.

E. Sunk cost.

36. A company is considering a new project that will cost $19,000. This project would result in

additional annual revenues of $6,000 for the next 5 years. The $19,000 cost is an example of

a(n):

A. Sunk cost.

B. Fixed cost.

C. Incremental cost.

D. Uncontrollable cost.

E. Opportunity cost.

37. Gordon Corporation inadvertently produced 10,000 defective digital watches. The watches

cost $8 each to produce. A salvage company will purchase the defective units as they are for $3

each. Gordon’s production manager reports that the defects can be corrected for $5 per unit,

enabling them to be sold at their regular market price of $12.50. Gordon should:

A. Sell the watches for $3 per unit.

B. Correct the defects and sell the watches at the regular price.

C. Sell the watches as they are because repairing them will cause their total cost to exceed their

selling price.

D. Sell 5,000 watches to the salvage company and repair the remainder.

E. Throw the watches away.

38. Chang Industries has 2,000 defective units of product that have already cost $14 each to

produce. A salvage company will purchase the defective units as they are for $5 each. Chang’s

production manager reports that the defects can be corrected for $6 per unit, enabling them to be

sold at their regular market price of $21. Chang should:

A. Throw the units away.

B. Sell the units to the salvage company for $5 per unit.

C. Sell the units as they are because repairing them will cause their total cost to exceed their

selling price.

D. Sell 1,000 units to the salvage company and repair the remainder.

E. Correct the defects and sell the units at the regular price.

39. Chang Industries has 2,000 defective units of product that have already cost $14 each to

produce. A salvage company will purchase the defective units as they are for $5 each. Chang’s

production manager reports that the defects can be corrected for $6 per unit, enabling them to be

sold at their regular market price of $21. The incremental income or loss on reworking the units

is:

A. $20,000 loss.

B. $20,000 income.

C. $12,000 loss.

D. $32,000 income.

E. $30,000 income.

40. Product A requires 5 machine hours per unit to be produced, Product B requires only 3

machine hours per unit, and the company’s productive capacity is limited to 240,000 machine

hours. Product A sells for $16 per unit and has variable costs of $6 per unit. Product B sells for

$12 per unit and has variable costs of $5 per unit. Assuming the company can sell as many units

of either product as it produces, the company should:

A. Produce only Product A.

B. Produce only Product B.

C. Produce equal amounts of A and B.

D. Produce A and B in the ratio of 62.5% A to 37.5% B.

E. Produce A and B in the ratio of 40% A and 60% B.

41. Epsilon Co. can produce a unit of product for the following costs:

Direct material …………………………………….. $ 8

Direct labor…………………………………………..

24

Overhead………………………….………………….

40

Total costs per unit……………………………….. $72

An outside supplier offers to provide Epsilon with all the units it needs at $60 per unit. If Epsilon

buys from the supplier, the company will still incur 40% of its overhead. Epsilon should choose

to:

A. Buy since the relevant cost to make it is $72.

B. Make since the relevant cost to make it is $56.

C. Buy since the relevant cost to make it is $48.

D. Make since the relevant cost to make it is $48.

E. Buy since the relevant cost to make it is $56.

42. Factor Co. can produce a unit of product for the following costs:

Direct material …………………………………….. $ 8

Direct labor…………………………………………..

24

Overhead………………………….………………….

40

Total costs per unit……………………………….. $72

An outside supplier offers to provide Factor with all the units it needs at $46 per unit. If Factor

buys from the supplier, the company will still incur 60% of its overhead. Factor should choose

to:

A. Buy since the relevant cost to make it is $56.

B. Make since the relevant cost to make it is $48.

C. Buy since the relevant cost to make it is $48.

D. Make since the relevant cost to make it is $32.

E. Buy since the relevant cost to make it is $32.

43. Listmann Corp. processes four different products that can either be sold as is or processed

further.

Listed below are sales and additional cost data:

Sales

Sales

Value

Additional Value after

with no

further

Processing further

Product

Processin

Costs

processing

Premier $1,350 $900 $2,700

Deluxe 450 225 630

Super 900 450 1,800

Basic

90

90

45 180

Which product(s) should not be processed further?

A. Premier.

B. Deluxe.

C. Super.

D. Basic.

E. Premier and Basic.

44. Maxim manufactures a hamster food product called Green Health. Maxim currently has

10,000 bags of Green Health on hand. The variable production costs per bag are $1.80 and total

fixed costs are $10,000. The hamster food can be sold as it is for $9.00 per bag or be processed

further into Premium Green and Green Deluxe at an additional $2,000 cost. The additional

processing will yield 10,000 bags of Premium Green and 3,000 bags of Green Deluxe, which can

be sold for $8 and $6 per bag, respectively. The net advantage (incremental income) of

processing Green Health further into Premium Green and Green Deluxe would be:

A. $98,000.

B. $96,000.

C. $ 8,000.

D. $ 6,000.

E. $ 2,000.

45. Maxim manufactures a cat food product called Green Health. Maxim currently has 10,000

bags of Green Health on hand. The variable production costs per bag are $1.80 and total fixed

costs are $10,000. The cat food can be sold as it is for $9.00 per bag or be processed further into

Premium Green and Green Deluxe at an additional $2,000 cost. The additional processing will

yield 10,000 bags of Premium Green and 3,000 bags of Green Deluxe, which can be sold for $8

and $6 per bag, respectively. If Green Health is processed further into Premium Green and

Green Deluxe, the total gross profit would be:

A. $ 68,000.

B. $ 78,000.

C. $ 96,000.

D. $ 98,000.

E. $100,000.

46. Minor Electric has received a special one-time order for 1,500 light fixtures (units) at $5 per

unit. Minor currently produces and sells 7,500 units at $6.00 each. This level represents 75% of

its capacity. Production costs for these units are $4.50 per unit, which includes $3.00 variable

cost and $1.50 fixed cost. To produce the special order, a new machine needs to be purchased at a

cost of $1,000 with a zero salvage value. Management expects no other changes in costs as a

result of the additional production. Should the company accept the special order?

A. No, because additional production would exceed capacity.

B. No, because incremental costs exceed incremental revenue.

C. Yes, because incremental revenue exceeds incremental costs.

D. Yes, because incremental costs exceed incremental revenues.

E. No, because the incremental revenue is too low.

47. Minor Electric has received a special one-time order for 1,500 light fixtures (units) at $5 per

unit. Minor currently produces and sells 7,500 units at $6.00 each. This level represents 75% of

its capacity. Production costs for these units are $4.50 per unit, which includes $3.00 variable

cost and $1.50 fixed cost. To produce the special order, a new machine needs to be purchased at a

cost of $1,000 with a zero salvage value. Management expects no other changes in costs as a

result of the additional production. If Minor wishes to earn $1,250 on the special order, the size

of the order would need to be:

A. 4,500 units.

B. 2,250 units.

C. 1,125 units.

D. 625 units.

E. 300 units.

48. Bluebird Mfg. has received a special one-time order for 15,000 bird feeders at $3 per unit.

Bluebird currently produces and sells 75,000 units at $7.00 each. This level represents 80% of its

capacity. Production costs for these units are $3.50 per unit, which includes $2.25 variable cost

and $1.25 fixed cost. If Bluebird accepts this additional business, the effect on net income will

be:

A. $45,000 increase.

B. $11,250 increase.

C. $33,750 increase.

D. $7,500 decrease.

E. $33,750 decrease.

49. Bannister Co. is thinking about having one of its products manufactured by a subcontractor.

Currently, the cost of manufacturing 1,000 units follows:

Direct material …………………………..………… $45,000

Direct labor………………………………………….. 30,000

Factory overhead (30% is variable)............ 98,000

If Bannister can buy 1,000 units from a subcontractor for $100,000, it should:

A. Make the product because current factory overhead is less than $100,000.

B. Make the product because the cost of direct material plus direct labor of manufacturing is less

than $100,000.

C. Buy the product because the total incremental costs of manufacturing are greater than

$100,000.

D. Buy the product because total fixed and variable manufacturing costs are greater than

$100,000.

E. Make the product because factory overhead is a sunk cost.

50. Frederick Co. is thinking about having one of its products manufactured by a subcontractor.

Currently, the cost of manufacturing 5,000 units follows:

Direct material …………………………..………… $62,000

Direct labor………………………………………….. 47,000

Variable factory overhead……………….. 38,000

Factory overhead….………………………………. 52,000

If Frederick can buy 5,000 units from a subcontractor for $130,000, it should:

A. Make the product because current factory overhead is less than $130,000.

B. Make the product because the cost of direct material plus direct labor of manufacturing is less

than $130,000.

C. Make the product because factory overhead is a sunk cost.

D. Buy the product because total fixed and variable manufacturing costs are greater than

$130,000.

E. Buy the product because the total incremental costs of manufacturing are greater than

$130,000.

51. A company has the choice of either selling 1,000 defective units as scrap or rebuilding them.

The company could sell the defective units as they are for $4.00 per unit. Alternatively, it could

rebuild them with incremental costs of $1.00 per unit for materials, $2.00 per unit for labor, and

$1.50 per unit for overhead, and then sell the rebuilt units for $8.00 each. What should the

company do?

A. Sell the units as scrap.

B. Rebuild the units.

C. It does not matter because both alternatives have the same result.

D. Neither sell nor rebuild because both alternatives produce a loss. Instead, the company should

store the units permanently.

E. Throw the units away.

52. A company has the choice of either selling 600 defective units as scrap or rebuilding them.

The company could sell the defective units as they are for $2.00 per unit. Alternatively, it could

rebuild them with incremental costs of $0.60 per unit for materials, $1.00 per unit for labor, and

$0.80 per unit for overhead, and then sell the rebuilt units for $5.00 each. What should the

company do?

A. Sell the units as scrap.

B. Rebuild the units.

C. It does not matter because both alternatives have the same result.

D. Since both alternatives produce a loss, store the units in hopes of a better price later.

E. Throw the units away.

53. Ahngram Corp. has 1,000 defective units of a product that cost $3 per unit in direct costs and

$6.50 per unit in indirect cost when produced last year. The units can be sold as scrap for $4 per

unit or reworked at an additional cost of $2.50 and sold at full price of $12. The incremental net

income (loss) from the choice of reworking the units would be:

A. $5,500.

B. $0.

C. ($2,500).

D. $10,500.

E. $2,500.

54. Benjamin Company had the following results of operations for the past year:

Sales (16,000 units at $10)…..……………………… $160,000

Direct materials and direct labor………………….. $96,000

Overhead (20% variable)…..……………………….. 16,000

Selling and administrative expenses (all fixed)

32,000

(144,000

)

Operating income………………………..…………….. $ 16,000

A foreign company (whose sales will not affect Benjamin’s market) offers to buy 4,000 units at

$7.50 per unit. In addition to variable manufacturing costs, selling these units would increase

fixed overhead by $600 and selling and administrative costs by $300. If Benjamin accepts the

offer, its profits will:

A. Increase by $30,000.

B. Increase by $ 6,000.

C. Decrease by $ 6,000.

D. Increase by $ 5,200.

E. Increase by $ 4,300.

55. Lattimer Company had the following results of operations for the past year:

Sales (15,000 units at $12)…..……………………… $180,000

Variable manufacturing costs…………..………….. $97,500

Fixed manufacturing costs…..……………………… 21,000

Selling and administrative expenses (all fixed)

36,000

(154,500

)

Operating income………………………..…………….. $ 25,500

A foreign company whose sales will not affect Lattimer’s market offers to buy 5,000 units at

$7.50 per unit. In addition to existing costs, selling these units would add a $0.25 selling cost for

export fees. If Lattimer accepts this additional business, the special order will yield a:

A. $2,000 loss.

B. $8,250 loss.

C. $3,750 profit.

D. $3,250 loss.

E. $5,000 profit.

56. Markson Company had the following results of operations for the past year:

Sales (8,000 units at $20)………………………… $160,000

Variable manufacturing costs…………………… $86,000

Fixed manufacturing costs……………………….. 15,000

Variable selling and administrative expenses…….

12,000

Fixed selling and administrative expenses ……….

20,000

(133,000

)

Operating income………………………………… $ 27,000

A foreign company whose sales will not affect Markson’s market offers to buy 2,000 units at $14

per unit. In addition to variable manufacturing costs, selling these units would increase fixed

overhead by $1,600 for the purchase of special tools. If Markson accepts this additional business,

its profits will:

A. Increase by $3,500.

B. Decrease by $5,650.

C. Decrease by $1,600.

D. Increase by $ 1,900.

E. Decrease by $5,100.

57. Wheeler Company can produce a product that incurs the following costs per unit: direct

materials, $10; direct labor, $24, and overhead, $16. An outside supplier has offered to sell the

product to Axle for $45. If Wheeler buys from the supplier, it will still incur 45% of its overhead

cost. Compute the net incremental cost or savings of buying.

A. $4.00 savings per unit.

B. $4.00 cost per unit.

C. $2.20 cost per unit.

D. $3.80 cost per unit.

E. $2.20 savings per unit.

58. Paxton Company can produce a component of its product that incurs the following costs per

unit: direct materials, $10; direct labor, $14, variable overhead $3 and fixed overhead, $8. An

outside supplier has offered to sell the product to Axle for $32. Compute the net incremental cost

or savings of buying the component.

A. $5.00 savings per unit.

B. $3.00 cost per unit.

C. $0 cost or savings per unit.

D. $5.00 cost per unit.

E. $3.00 savings per unit.

59. Walters manufactures a specialty food product that can currently be sold for $22 per unit and

has 20,000 units on hand. Alternatively, it can be further processed at a cost of $12,000 and

converted into 12,000 units of Deluxe and 6,000 units of Super. The selling price of Deluxe and

Super are $30 and $20, respectively. The incremental net income of processing further would be:

A. $40,000.

B. $28,000.

C. $18,000.

D. $44,000.

E. $12,000.

60. Cornish Company had the following results of operations for the past year:

Sales (20,000 units at $22)…..….............................. $440,000

Direct materials and direct labor………………………... $200,000

Overhead (40% variable)……………..……………......... 100,000

Selling and administrative expenses (all fixed)…….. 92,000 (392,000)

Operating income…..…..…………………..................... $ 48,000

A foreign company (whose sales will not affect Cornish’s market) offers to buy 3,000 units at

$17.00 per unit. In addition to variable manufacturing costs, selling these units would increase

fixed overhead by $500 and selling and administrative costs by $1,000. If Cornish accepts the

offer, its profits will:

A. Decrease by $4,500.

B. Increase by $4,500.

C. Decrease by $300.

D. Increase by $13,500.

E. Increase by $15,000.

61. Elliot Company can sell all of its products A and Z that it can produce, but it has limited

production capacity. It can produce 8 units of A per hour or 10 units of Z per hour, and it has

20,000 production hours available. Contribution margin per unit is $12 for A and $10 for Z. What

is the most profitable sales mix for Elliot Company?

A. 84,000 units of A and 60,000 units of Z.

B. 48,000 units of A and 80,000 units of Z.

C. 60,000 units of A and 100,000 units of Z.

D. 120,000 units of A and 0 units of Z.

E. 0 units of A and 200,000 units of Z.

62. Soar Incorporated is considering eliminating its mountain bike division, which reported an

operating loss for the recent year of $3,000. The division sales for the year were $1,050,000 and

the variable costs were $860,000. The fixed costs of the division were $193,000. If the mountain

bike division is dropped, 30% of the fixed costs allocated to that division could be eliminated.

The impact on operating income for eliminating this business segment would be:

A. $57,900 decrease

B. $132,100 decrease

C. $54,900 decrease

D. $190,000 increase

E. $190,000 decrease

63. Granfield Company is considering eliminating its backpack division, which reported an

operating loss for the recent year of $42,000. The division sales for the year were $960,000 and

the variable costs were $475,000. The fixed costs of the division were $527,000. If the backpack

division is dropped, 40% of the fixed costs allocated to that division could be eliminated. The

impact on Granfield’s operating income for eliminating this business segment would be:

A. $485,000 decrease

B. $210,800 increase

C. $274,200 decrease

D. $485,000 increase

E. $274,200 increase

64. Granfield Company has a piece of manufacturing equipment with a book value of $40,000

and a remaining useful life of four years. At the end of the four years the equipment will have a

zero salvage value. The market value of the equipment is currently $22,000. Granfield can

purchase a new machine for $120,000 and receive $22,000 in return for trading in its old

machine. The new machine will reduce variable manufacturing costs by $19,000 per year over

the four-year life of the new machine. The total increase or decrease in net income by replacing

the current machine with the new machine (ignoring the time value of money) is:

A. $22,000 decrease

B. $76,000 increase

C. $18,000 decrease

D. $52,000 increase

E. $22,000 increase

65. Beta Inc. can produce a unit of Zed for the following costs:

Direct material $ 10

Direct labor 20

Overhead 50

Total costs per unit $80

An outside supplier offers to provide Beta with all the Zed units it needs at $58 per unit. If Beta

buys from the supplier, it will still incur 40% of its overhead. Beta should:

A. Buy Zed since the relevant cost to make it is $60.

B. Make Zed since the relevant cost to make it is $60.

C. Buy Zed since the relevant cost to make it is $80.

D. Make Zed since the relevant cost to make it is $30.

E. Buy Zed since the relevant cost to make it is $30.

66. To determine a product selling price based on the total cost method, management should

include:

A. Total production and nonproduction costs plus a markup.

B. Total production and nonproduction costs only.

C. Total production costs plus a markup.

D. Total nonproduction costs plus a markup.

E. Only a markup.

67. Assume markup percentage equals desired profit divided by total costs. What is the correct

calculation to determine the dollar amount of the markup per unit?

A. Total cost times markup percentage.

B. Total cost per unit times markup percentage per unit.

C. Total cost per unit divided by markup percentage per unit.

D. Markup percentage per unit divided by total cost per unit.

E. Markup percentage divided by total cost.

68. Wade Company is operating at 75% of its manufacturing capacity of 140,000 product units

per year. A customer has offered to buy an additional 20,000 units at $32 each and sell them

outside the country so as not to compete with Wade. The following data are available:

Costs at 75% capacity: Per

Unit Total

Direct materials $12.00 $1,260,000

Direct labor 9.00 945,000

Overhead (fixed and variable) 15.00 1,575,000

Totals $36.00 $3,780,000

In producing 20,000 additional units, fixed overhead costs would remain at their current level but

incremental variable overhead costs of $6 per unit would be incurred. What is the effect on

income if Wade accepts this order?

A. Income will decrease by $4 per unit.

B. Income will increase by $4 per unit.

C. Income will increase by $5 per unit.

D. Income will decrease by $5 per unit.

E. Income will increase by $11 per unit.

69. Derby Inc. manufactures a product which contains a small part. The company has always

purchased this motor from a supplier for $125 each. Derby recently upgraded its own

manufacturing capabilities and now has enough excess capacity (including trained workers) to

begin manufacturing the motor instead of buying it. The company prepared the following per

unit cost projections of making the motor, assuming that overhead is allocated to the part at the

normal predetermined overhead rate of 150% of direct labor cost.

The required volume of output to produce the motors will

not require any incremental fixed overhead. Incremental

variable overhead cost is $21 per motor. What is the effect

on income if Derby decides to make the motors?

A. Income will decrease by $16 per unit.

B. Income will increase by $16 per unit.

C. Income will increase by $23 per unit.

D. Income will decrease by $23 per unit.

E. Income will increase by $39 per unit.

70. A company has already incurred a $55,000 cost in partially producing its three products.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

23-41

Direct materials $38

Direct labor 50

Overhead (fixed and

variable)

75

Total $163

Their selling prices when partially and fully processed are shown in the following table with the

additional costs necessary to finish their processing. Based on this information, should any

products be processed further?

Product

Unfinished

Selling Price

Finished

Selling Price

Further

Processing

Costs

A $72 $108 $35

B 83 124 42

C 94 141 45

A. All of these products should be processed further.

B. None of these products should be processed further.

C. Products A and B should be processed further.

D. Products B and C should be processed further.

E. Products A and C should be processed further.

71. Bandy Corporation owns a machine that manufactures lawn games. Production time for the

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

23-42

croquet set is 10 units per hour and for the volley ball game is 8 units per hour. The machine’s

capacity is 1,500 hours per year. Both products are sold to a single customer who has agreed to

buy all of the company’s output up to a maximum of 4,000 croquet sets and 10,000 volleyball

games. Selling prices and variable costs per unit are shown below. Based on this information,

what is Bandy Corporation’s most profitable sales mix?

Croquet Set Volleyball Game

Selling price per unit $75 $62

Variable costs per unit 42 25

A. 15,000 croquet sets.

B. 12,000 volleyball games.

C. 4,000 croquet sets and 10,000 volleyball games.

D. 4,000 croquet sets and 8,800 volleyball games.

E. 2,500 croquet sets and 10,000 volleyball games.

72. The Mad Hatter Company owns a machine that manufactures two types of chimney caps.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

23-43

Production time is .20 hours for cap A and .40 hours for cap B. The machine’s capacity is 2,000

hours per year. Both products are sold to a single customer who has agreed to buy all of the

company’s output up to a maximum of 1,000 units of cap A and 6,000 units of cap B. Selling

prices and variable costs per unit are shown below. Based on this information, what is the Mad

Hatter’s most profitable sales mix?

Cap A Cap B

Selling price per unit $80 $60

Variable costs per unit 53 42

A. 10,000 units of cap A.

B. 5,000 units of cap B.

C. 1,000 units of cap A and 5,000 units of cap B.

D. 1,000 units of cap A and 6,000 units of cap B.

E. 1,000 units of cap A and 4,500 units of cap B.

73. What decision rule should be followed when deciding if a business segment should be

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

23-44

eliminated?

A. Segments generating a net loss should always be eliminated.

B. Segments with revenues that are more than avoidable expenses should be considered for

elimination.

C. Segments with revenues that are more than unavoidable expenses should be considered for

elimination.

D. Segments with revenues that are less than avoidable expenses should be considered for

elimination.

E. Segments with revenues that are less than unavoidable expenses should be considered for

elimination.

74. Rocko Inc. has a machine with a book value of $50,000 and a five-year remaining life. A new

machine is available at a cost of $85,000 and Rocko can also receive $38,000 for trading in the

old machine. The new machine will reduce variable manufacturing costs by $14,000 per year

over its five-year life. Should the machine be replaced?

A. Yes, because income will increase by $14,000 per year.

B. Yes, because income will increase by $23,000 in total.

C. No, because the company will be $23,000 worse off in total.

D. No, because the income will decrease by $14,000 per year.

E. Rocko will be not be better or worse off by replacing the machine.

75. Identify the five steps involved in managerial decision making.

76. Good management accounting indicates that projects be evaluated using relevant data. In

choosing among alternatives, what factors (considerations) are relevant?

77. A company inadvertently produced 6,000 defective portable radios. The radios cost $10 each

to be manufactured. A salvage company will purchase the defective units as they are for $8 each.

The production manager reports that the defects can be corrected for $4.50 per unit, enabling the

company to sell them at the regular price of $15.00. The repair operations would not affect other

production operations. Prepare an analysis that shows which action should be taken.

78. A company manufactures two products. Each unit of product X requires 10 machine hours

and each unit of product Y requires 4 machine hours. The company’s productive capacity is

limited to 180,000 machine hours. Each unit of product X sells for $15 and has variable costs of

$7. Each unit of product Y sells for $8 and has variable costs of $3. If the company can sell all

that it produces of both products, what should the sales mix be?

79. Goodfellow Company had the following results of operations for the past year:

Sales (8,000 units at $6.80)………………..…. $ 54,400

Materials and direct labor…………….……….. (20,000)

Overhead (40% variable)……………………... (10,000)

Selling and administrative expenses (all fixed)

(6,000

)

Operating income………………………………… $ 18,400

A foreign company (whose sales will not affect Goodfellow’s regular sales) offers to buy 2,000

units at $5.00 per unit. In addition to variable manufacturing costs, there would be shipping costs

of $1,200 in total on these units. Prepare an analysis of this additional business to show whether

Goodfellow should take this order.

80. Variations Company had the following results of operations for the past year:

Sales (8,000 units at $7.00)………………..…. $ 56,000

Variable manufacturing costs..…………....... (30,000)

Fixed manufacturing costs………………….… (6,000)

Fixed selling and administrative expenses

(4,500

)

Operating income………………………………… $ 15,500

A foreign company (whose sales will not affect Variations’ regular sales) offers to buy 700 units

at $4.00 per unit. In addition to variable manufacturing costs, there would be an export cost of

$0.30 per unit. Prepare an analysis of this additional business to show whether Variations should

take this order.

81. A company produces three different products that all require processing on the same

machines. There are only 27,000 machine hours available in each year. Production information

for each product is:

A B C

Sales price per unit…………………..…………… $20.00 $38.00 $35.00

Variable costs per unit ………………………….. $12.00 $26.00 $17.00

Machine hours necessary to produce one unit 2.5 4.0 4.50

Required:

(1) Determine the preferred sales mix if there are no market constraints on any of the products.

(2) Determine the preferred sales mix if the demand is limited to 5,000 units for each product.

(3) Determine the preferred sales mix if the demand is limited to 3,000 units for each product.

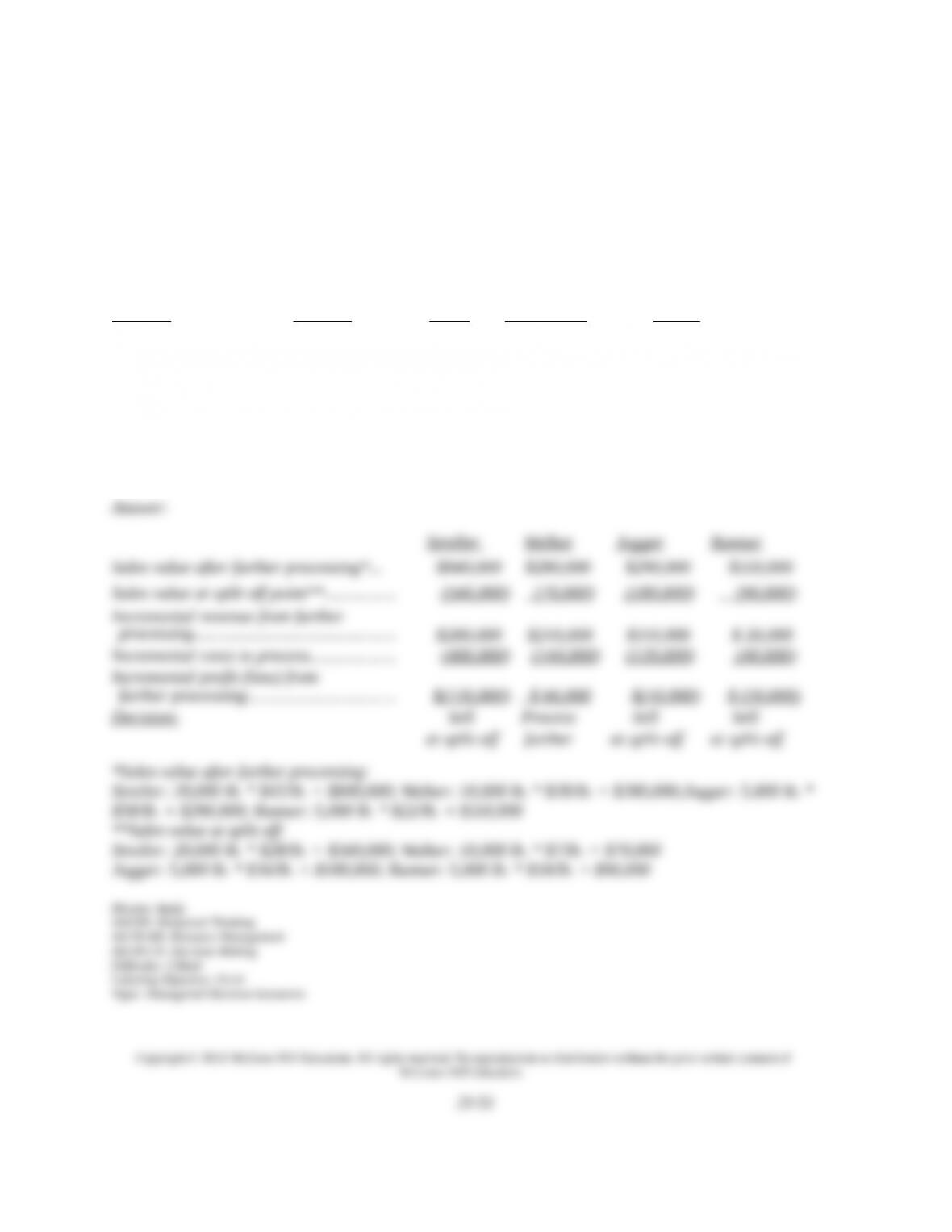

82. A company puts four products through a common production process. This process costs

$100,000 each year. The four products can be sold when they emerge from this process at the

“split-off point,” or processed further and then sold. Data about the four products for the coming

period are:

Unit Sales Unit Sales

Price per Price per

unit at unit after Additional

Split-Off Further Processing

Product

Volume

Point

Processing

Costs

Stroller 20,000 lb. $28.00 $42.00 $400,000

Walker 10,000 lb. 7.00 28.00 144,000

Jogger 5,000 lb. 36.00 58.00 120,000

Runner

5,000 lb.

18.00

22.00

40,000

Determine which products should be sold at the split-off point and which should be processed

further.

83. A company has just received a special, one-time order for 1,000 units. Producing the order

will have no effect on the production and sales of other units. The buyer’s name will be stamped

on each unit, at a cost of $1.50 per unit. Normal cost data, excluding stamping, follows:

Direct materials…………………………… $ 10 per unit

Direct labor……………………………….. 16 per unit

Variable overhead………………………… 4 per unit

Allocated fixed overhead…………………. 12 per unit

Allocated fixed selling expense…………… 8 per unit

Prepare an analysis that indicates the selling price per unit this company will require to earn

$3,000 on the order.

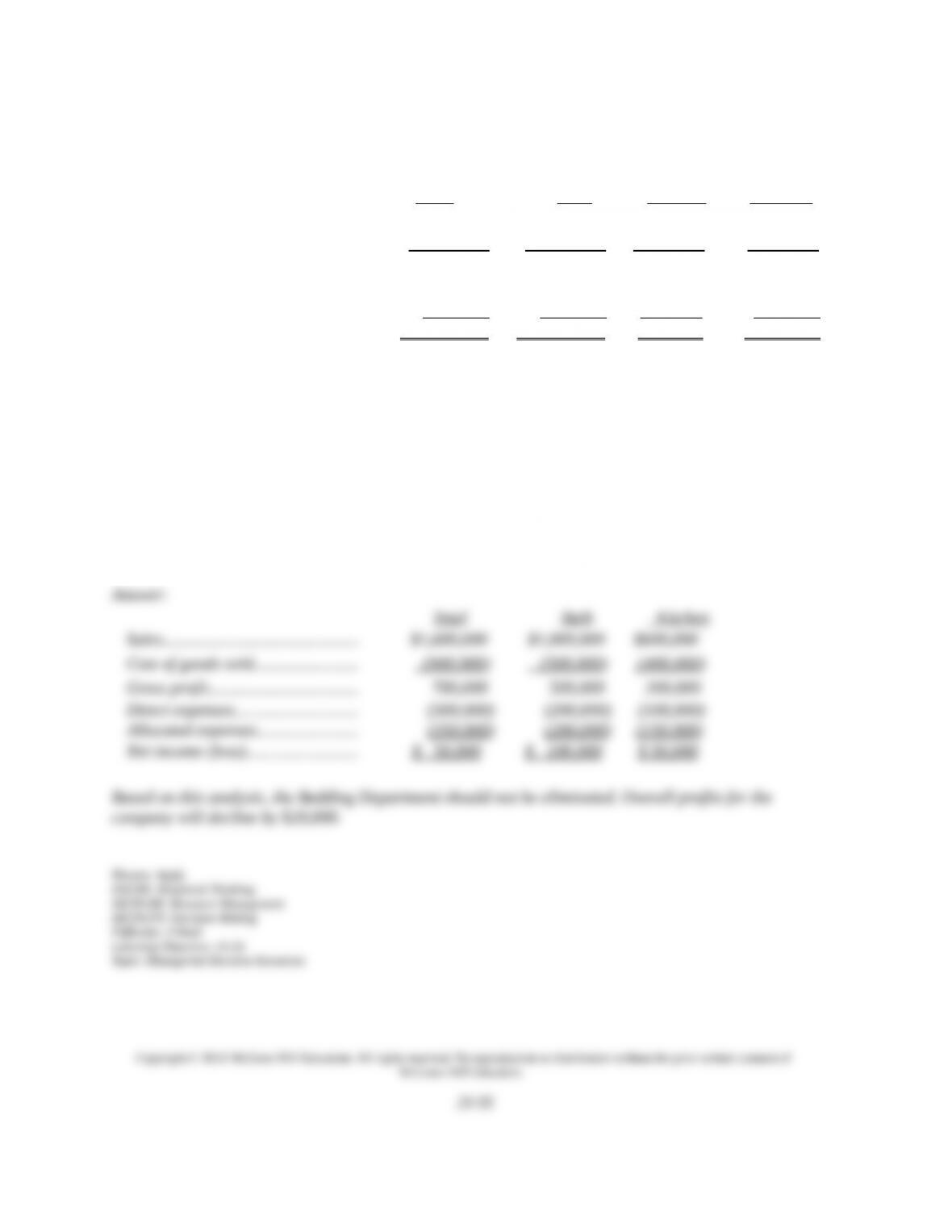

84. Spilker Linens Store has three departments: Bath, Kitchen, and Bedding. The most recent

income statement, showing the total operating profit and departmental results is shown below:

Total Bath Kitchen Bedding

Sales…………………….……………. $2,100,000 $1,000,000 $600,000 $500,000

Cost of goods sold…..…........... (1,260,000) (500,000) (400,000) (360,000)

Gross profit………………………… 840,000 500,000 200,000 140,000

Direct expenses………..………….

(420,000)

(200,000)

(100,000)

(120,000)

Allocated expenses…...............

(350,000)

(100,000)

(75,000)

(175,000)

Net income (loss)……..…………. $ 70,000 $ 200,000 $ 25,000 $(155,000)

Based on this income statement, management is planning on eliminating the Bedding

department, as it is generating a net loss. If the Bedding department is eliminated, the Kitchen

department will expand to fill the space, but sales will not change in total, nor will direct

expenses. None of Bedding’s allocated expenses will be avoided, but they will be reallocated to

Bath and Kitchen. Bath will be allocated $100,000 additional expenses, and Kitchen will be

allocated $75,000 additional expenses. Prepare a new income statement for Spilker Linens

Store, showing the results if the Bedding Department is eliminated and indicate whether

eliminating the department is advisable.

85. Luxury Linens has three departments: Bath, Kitchen, and Bedding. The most recent income

statement, showing the total operating profit and departmental results is shown below:

Total Bath Kitchen Bedding

Sales…………………….……………. $2,100,000 $1,000,000 $500,000 $600,000

Cost of goods sold…..…........... (1,260,000) (500,000) (360,000) (400,000)

Gross profit………………………… 840,000 500,000 140,000 200,000

Direct expenses………..………….

(420,000)

(200,000)

(120,000)

(100,000)

Allocated expenses…...............

(325,000)

(100,000)

(150,000)

(75,000)

Net income (loss)……..…………. $ 95,000 $ 200,000 $(130,000) $25,000

Based on this income statement, management is considering eliminating the Kitchen

department. If the Kitchen department is eliminated, the other departments will expand to fill the

space but sales are not expected to change. Twenty percent of Kitchen’s allocated expenses will

be avoided due to restructuring and the remainder reallocated equally to Bath and Bedding.

Show an analysis indicating whether the Kitchen department should be eliminated.

86. Generalware, Inc. sells a single product and reports the following results from sales of

100,000 units:

Sales ($45 unit) …………..…………….… $4,500,000

Less costs and expenses:

Direct materials ($16/unit)………….… $1,600,000

Direct labor ($9/unit)…………….….… 900,000

Variable overhead ($3/unit)…….…….. 300,000

Fixed overhead ($8.10/unit)……………. 810,000

Variable administrative ($4.50/unit)…. 450,000

Fixed administrative ($4/unit)………… 400,000

Total costs and expenses……………… $(4,460,000)

Operating income………………………… $ 40,000

A foreign company wants to purchase 15,000 units. However, they are willing to pay only $36

per unit for this one-time order. They also agree to pay all freight costs. To fill the order,

Generalware will incur normal production costs. Total fixed overhead will have to be increased

by $60,000 to pay for equipment rentals and insurance. No additional administrative costs

(variable or fixed) will be incurred in association with this special order.

Required:

(1) Should Generalware accept the order if it does not affect regular sales? Explain.

(2) Assume that Generalware can accept the special order only by giving up 5,000 units of its

normal sales. Should the company accept the special order under these circumstances?

87. A company is planning to introduce a new portable computer to its existing product line.

Management must decide whether to make the computer case or buy it from an outside supplier.

The lowest outside price is $90. If the case is produced internally, the company will have to

purchase new equipment that will yield annual depreciation of $130,000. The company will also

need to rent a new production facility at $200,000 a year. At 20,000 cases per year, a preliminary

analysis of production costs shows the following:

Per Case

Direct materials……………………………..……………….. $ 40.00

Direct labor……………………………………………………… 32.00

Variable overhead…………………………………………….. 10.00

Equipment depreciation……………..…………………….. 6.50

Building rental ………………………………………………… 10.00

Allocated fixed overhead………………………………….. 7.50

Total cost………………………………………………………… $106.00

Required:

(1) Determine whether the company should make the cases or buy them from the outside

supplier.

(2) What other factors, besides cost, should the company consider?

88. A company must decide between scrapping or rebuilding units that do not pass inspection.

The company has 15,000 such units that cost $6 per unit to manufacture. The units were built to

satisfy a special order, which must still be satisfied if the defective units are scrapped. The units

can be sold as scrap for $2.50 each or they can be reworked for $4.50 each and sold for the full

price of $9.00 each. If the units are sold as scrap, the company will have to build 15,000

replacement units and sell them at the full price.

Required:

(1) What is the net return from selling the units as scrap?

(2) What is the net return from reworking and selling the units?

(3) Should the company sell the units as scrap or rework them?

89. A company inadvertently produced 3,000 defective products. The product cost $15 each to be

manufactured and normally sells for $35 each. A salvage company will purchase the defective

units as they are for $13 each. The production manager reports that the defects can be corrected

for $5 per unit, enabling the company to sell them at a discounted price of $22.00. The repair

operations would not affect other production operations. Prepare an analysis that shows which

action should be taken.

90. Mays Company can sell all of product A that it produces but only 160,000 units of Z and it

has limited production capacity. It can produce 6 units of A per hour or 10 units of Z per hour,

and it has 30,000 production hours available. Contribution margin per unit is $12 for A and $10

for Z. What is the most profitable sales mix for this company?

91. Marshall Company currently manufactures one of its parts at a cost of $3.25 per unit. This

cost is based on a normal production rate of 50,000 units. Variable costs are $2.10 per unit, fixed

costs related to making this part are $40,000 per year, and allocated fixed costs are $45,000 per

year. Allocated fixed costs are unavoidable whether the company makes or buys the part.

Marshall is considering buying the part from a supplier for a quoted price of $2.80 per unit

guaranteed for a three-year period. Should the company continue to manufacture the part, or

should it buy the part from the outside supplier? Support your answer with analyses.

92. Relevant costs are also known as ___________________.

93. A(n) ________________________ requires a future outlay of cash and is relevant for current

and future decision making.

94. A(n) _____________________ is the potential benefit lost by taking a specific action when

two or more alternative choices are available.

95. A(n) _____________________ arises from a past decision and cannot be avoided or

changed; it is irrelevant to future decisions.

96. __________________________ costs are amounts that will continue even if a segment is

eliminated.

97. Costs already incurred in manufacturing the units of a product that do not meet quality

standards are _________________________ costs.

98. A _______________________________ is the combination of products sold by a company.

99. In this chapter, you examined several short-term managerial decision tasks. Identify (list) any

three of these types of decision tasks:

_________________________; _________________________; _________________________