Chapter 22

PERFORMANCE MEASUREMENT AND RESPONSIBILITY

ACCOUNTING

True / False Questions

1. Evaluation of the performance of an investment center involves only financial measures.

2. Profit center managers are evaluated on their ability to generate revenues in excess of

costs.

3. Departmental information is usually distributed to the public as part of the company’s

annual report and footnotes.

4. Investment center is another name for profit center.

5. A department can never be considered to be a profit center.

6. A cost center does not directly generate revenues.

7. A selling department is usually evaluated as a profit center.

8. A profit center generates revenue, incurs costs, and has the authority to make significant

investing decisions.

9. Indirect expenses are allocated to departments based upon the benefits received by each

department.

10. Direct expenses require allocation across departments because they cannot be readily

traced to one department.

11. Departmental salary expenses are direct expenses of that department.

12. The concepts of direct expenses and controllable costs are essentially the same; also,

indirect expenses and uncontrollable costs are essentially the same.

13. The number of hours that a department uses equipment and machinery is a reasonable

basis for allocating depreciation.

14. Advertising expense can be reasonably allocated to departments on the basis of each

department’s proportion of sales.

15. No standard rule identifies the best basis of allocating expenses across departments, so it

is impossible to allocate costs in a manner that will be perceived as fair.

16. A department’s direct expenses are usually considered uncontrollable costs.

17. An example of a controllable cost is equipment depreciation expense.

18. A responsibility accounting performance report usually compares actual costs to budgeted

costs amounts by management level.

19. Joint costs are costs incurred in producing or purchasing a single product.

20. Joint costs can be allocated either using a physical basis or a value basis.

21. A joint cost of producing two products can be allocated between those products on the

basis of the relative physical quantities of each product produced.

22. In producing oat bran, the joint cost of milling the oats into bran, oatmeal, and animal feed

is considered a direct cost to the oat bran, because the oat bran cannot be produced without

incurring the joint cost.

23. Investment center managers are typically evaluated using performance measures that

combine income and assets.

24. Return on investment is a useful measure to evaluate the performance of a cost center

manager.

25. Measures used to evaluate the manager of an investment center include investment

turnover and profit margin.

26. A useful measure used to evaluate the performance of an investment center is investment

center residual income.

27. An example of a service department is the human resources department.

28. Allocating costs to service departments involves accumulating revenues and direct

expenses, allocating indirect expenses, and preparing the department income statement.

29. Since service departments do not generate revenues, it is unnecessary to accumulate and

allocate their costs.

30. The process of preparing departmental income statements begins with allocating service

department expenses.

31. Departmental income statements are prepared for service departments but not operating

departments.

32. Departmental contribution to overhead is the amount of sales for that department less its

direct expenses.

33. Departmental contribution to overhead is the same as gross profit generated by that

department.

34. Decentralization refers to companies that have multiple locations.

35. In a decentralized organization, decisions are made by managers throughout the company

rather than by a few top executives.

36. A cost center is a unit of a business that incurs costs without directly generating revenues.

All of the following are considered cost centers except:

A. Accounting department at Warner Bros.

B. Purchasing department at Best Buy.

C. Research department at Microsoft.

D. Advertising department at Hertz.

E. Juice division at Coca Cola.

37. A unit of a business that generates revenues and incurs costs is called a:

A. Performance center.

B. Profit center.

C. Cost center.

D. Responsibility center.

E. Expense center.

38. The type of department that generates revenues and incurs costs, and its manager is

responsible for the investments made in operating assets is called a:

A. Profit center

B. Cost center

C. Service department

D. Investment center

E. Responsibility center

39. An accounting system that accumulates and reports costs incurred by each service

department for management to evaluate the performance of a department is a:

A. Departmental accounting system.

B. Cost accounting system.

C. Service accounting system.

D. Revenue accounting system.

E. Standard accounting system.

40. A department that incurs costs without directly generating revenues is a:

A. Service center.

B. Production center.

C. Profit center.

D. Cost center.

E. Performance center.

41. The difference between a profit center and an investment center is

A. an investment center incurs costs, but does not directly generate revenues.

B. an investment center incurs no costs but does generate revenues.

C. an investment center is responsible for investments made in operating assets.

D. an investment center provides services to profit centers.

E. There is no difference; investment center and profit center are synonymous.

42. An expense that is readily traced to a department because it is incurred for that

department’s sole benefit is a(n):

A. Common expense.

B. Indirect expense.

C. Direct expense.

D. Administrative expense.

E. Recurring expense.

43. Expenses that are easily traced and assigned to a specific department because they are

incurred for the sole benefit of that department are called:

A. Direct expenses.

B. Indirect expenses.

C. Controllable expenses.

D. Uncontrollable expenses.

E. Fixed expenses.

44. Expenses that are not easily associated with a specific department, and which are incurred

for the joint benefit of more than one department, are:

A. Fixed expenses.

B. Indirect expenses.

C. Direct expenses.

D. Uncontrollable expenses.

E. Variable expenses.

45. Regardless of the system used in departmental cost analysis:

A. Direct costs are allocated, indirect costs are not.

B. Indirect costs are allocated, direct costs are not.

C. Both direct and indirect costs are allocated.

D. Neither direct nor indirect costs are allocated.

E. Total departmental costs will always be the same.

46. The salaries of employees who spend all their time working in one department are:

A. Variable expenses.

B. Indirect expenses.

C. Direct expenses.

D. Responsibility expenses.

E. Unavoidable expenses.

47. A challenge in calculating the total costs and expenses of a department is:

A. Determining the gross profit ratio.

B. Assigning direct costs to the department.

C. Allocating indirect expenses to the department.

D. Determining the amount of sales of the department.

E. Determining the direct expenses of the department.

48. A company has two departments, Y and Z that incur delivery expenses. An analysis of the

total delivery expense of $9,000 indicates that Dept. Y had a direct expense of $1,000 for

deliveries and Dept. Z had no direct expense. The indirect expenses are $8,000. The analysis

also indicates that 40% of regular delivery requests originate in Dept. Y and 60% originate in

Dept. Z. Departmental delivery expenses for Dept. Y and Dept. Z, respectively, are:

A. $4,500; $4,500.

B. $4,200; $4,800.

C. $5,500; $3,500.

D. $4,800; $4,200.

E. $5,400; $3,600.

49. A company has two departments, Y and Z that incur wage expenses. An analysis of the

total wage expense of $19,000 indicates that Dept. Y had a direct wage expense of $2,000 and

Dept. Z had a direct wage expense of $3,500. The remaining expenses are indirect and

analysis indicates they should be allocated evenly between the two departments. Departmental

wage expenses for Dept. Y and Dept. Z, respectively, are:

A. $8,750; $10,250.

B. $10,250; $8,750.

C. $9,500; $9,500.

D. $2,000; $3,500.

E. $6,750; $6,750.

50. Which of the following is not a step in creating operating department income statements?

A. Prepare the departmental income statements.

B. Accumulate revenues and direct expenses by department.

C. Allocate indirect expenses across departments.

D. Allocate service department expenses to operating departments.

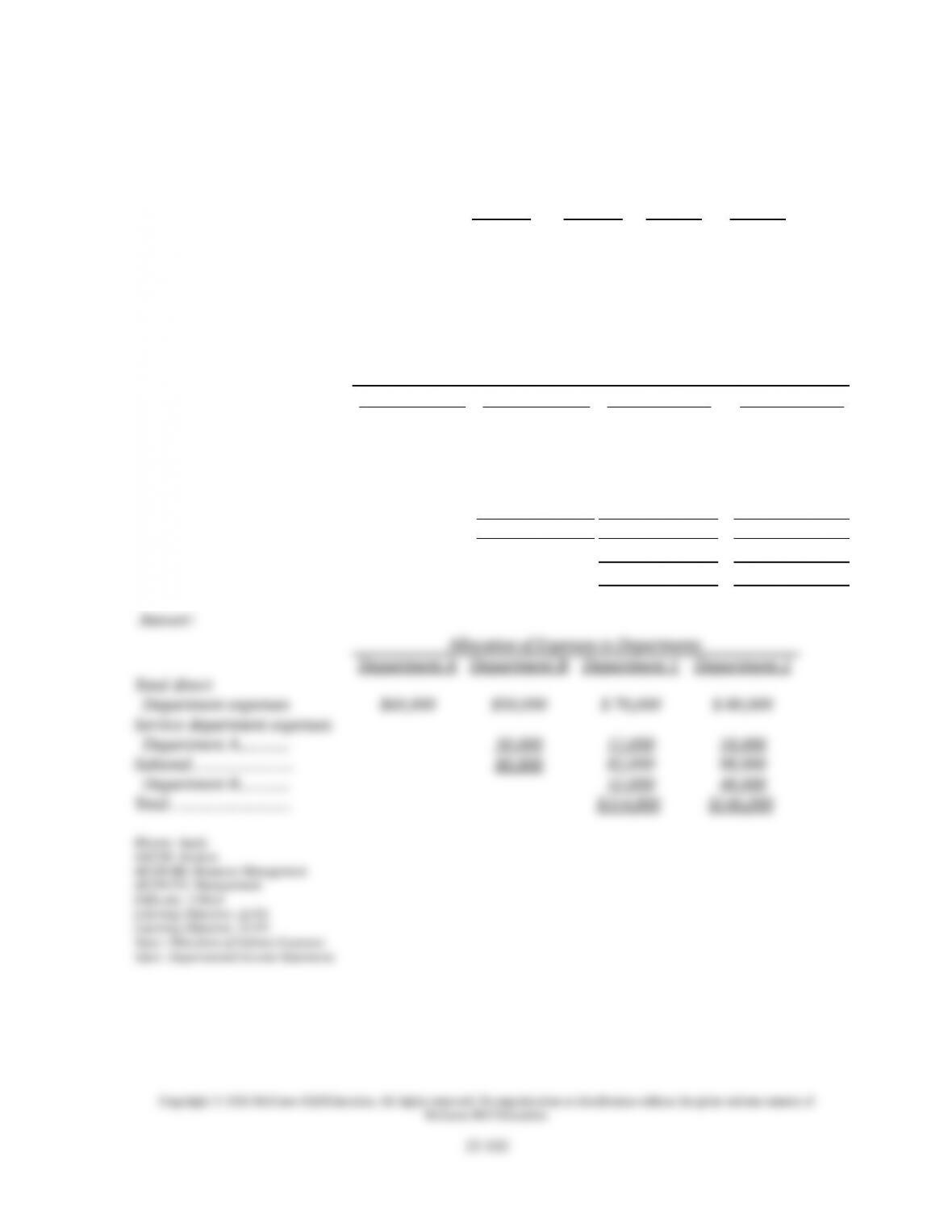

E. Eliminate the uncontrollable costs for each department.

51. The most useful allocation basis for the departmental costs of an advertising campaign for

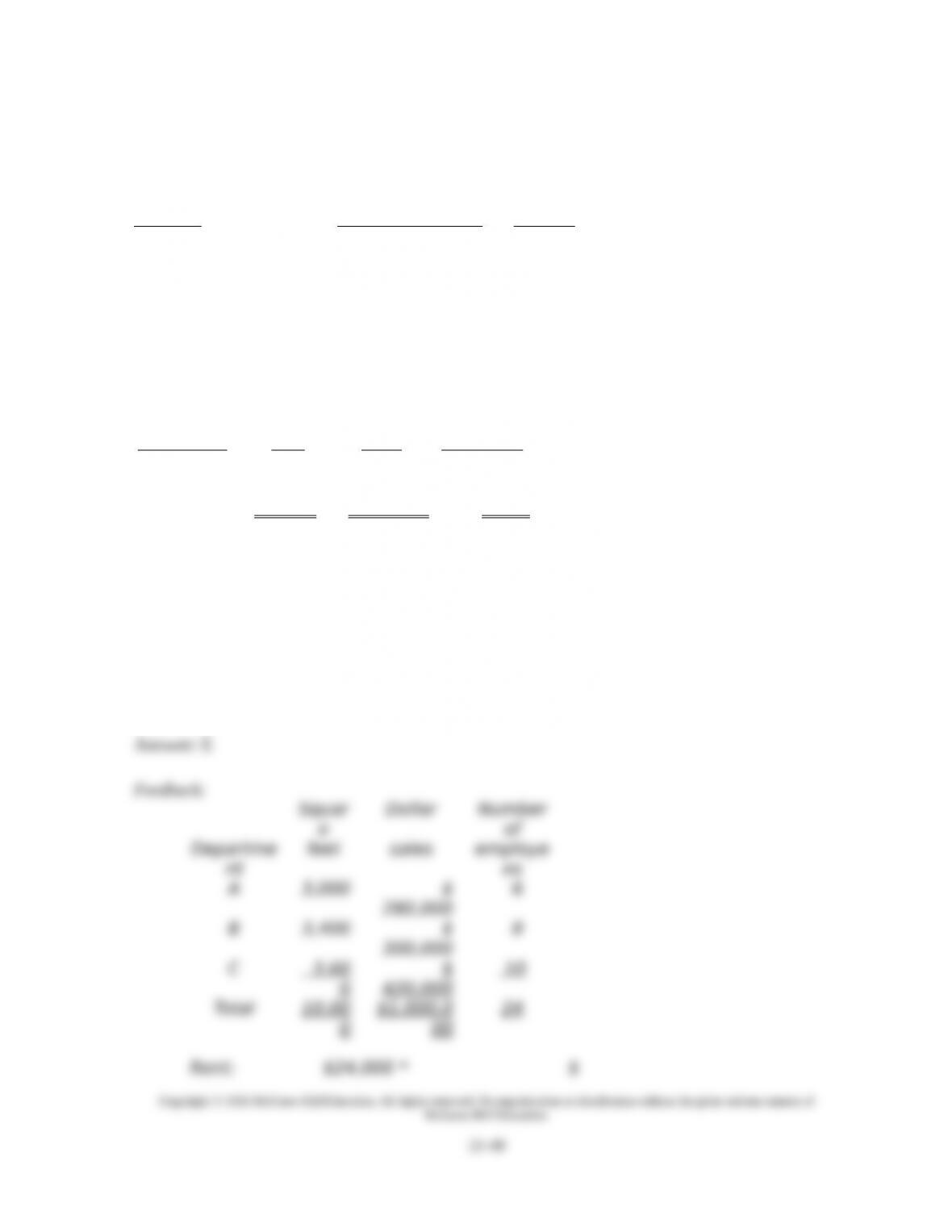

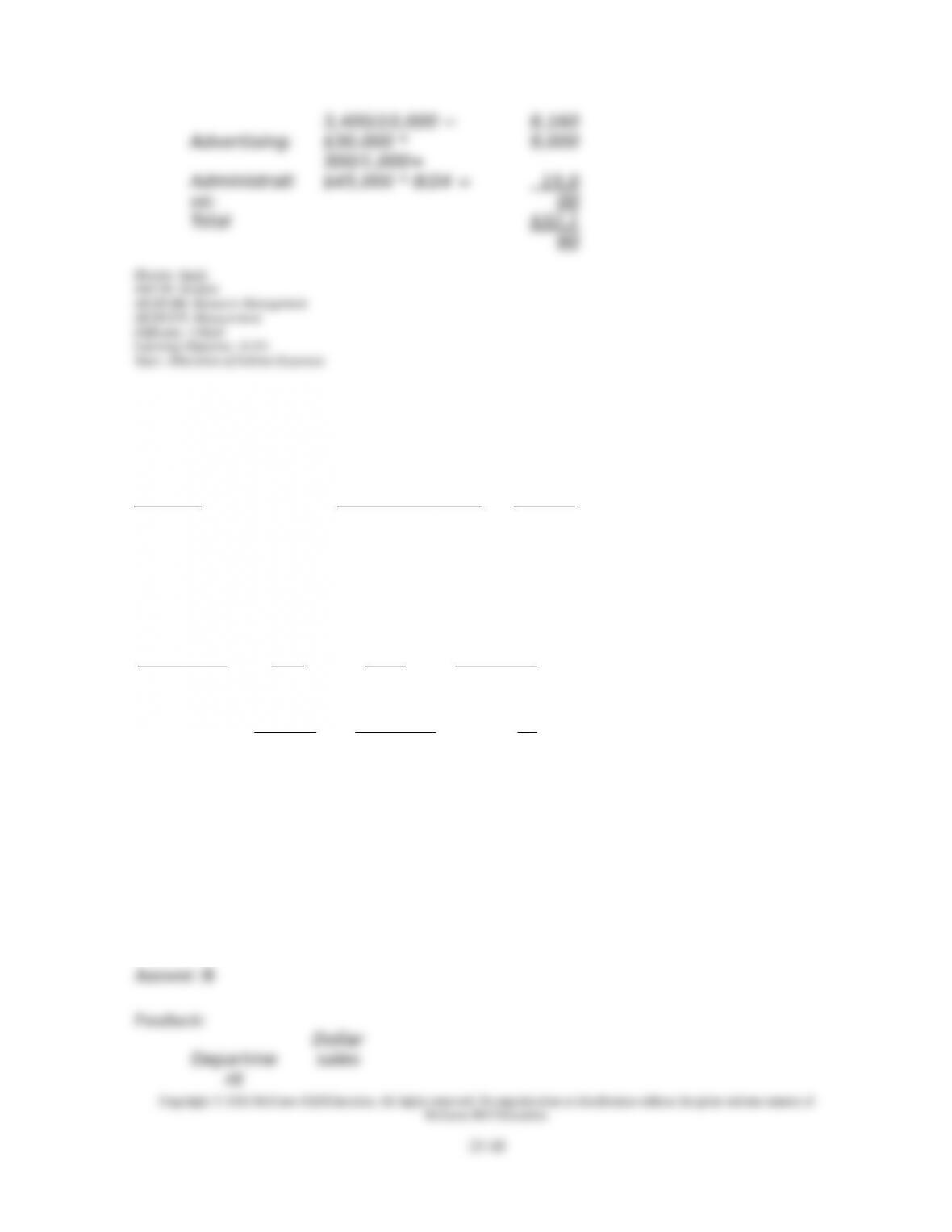

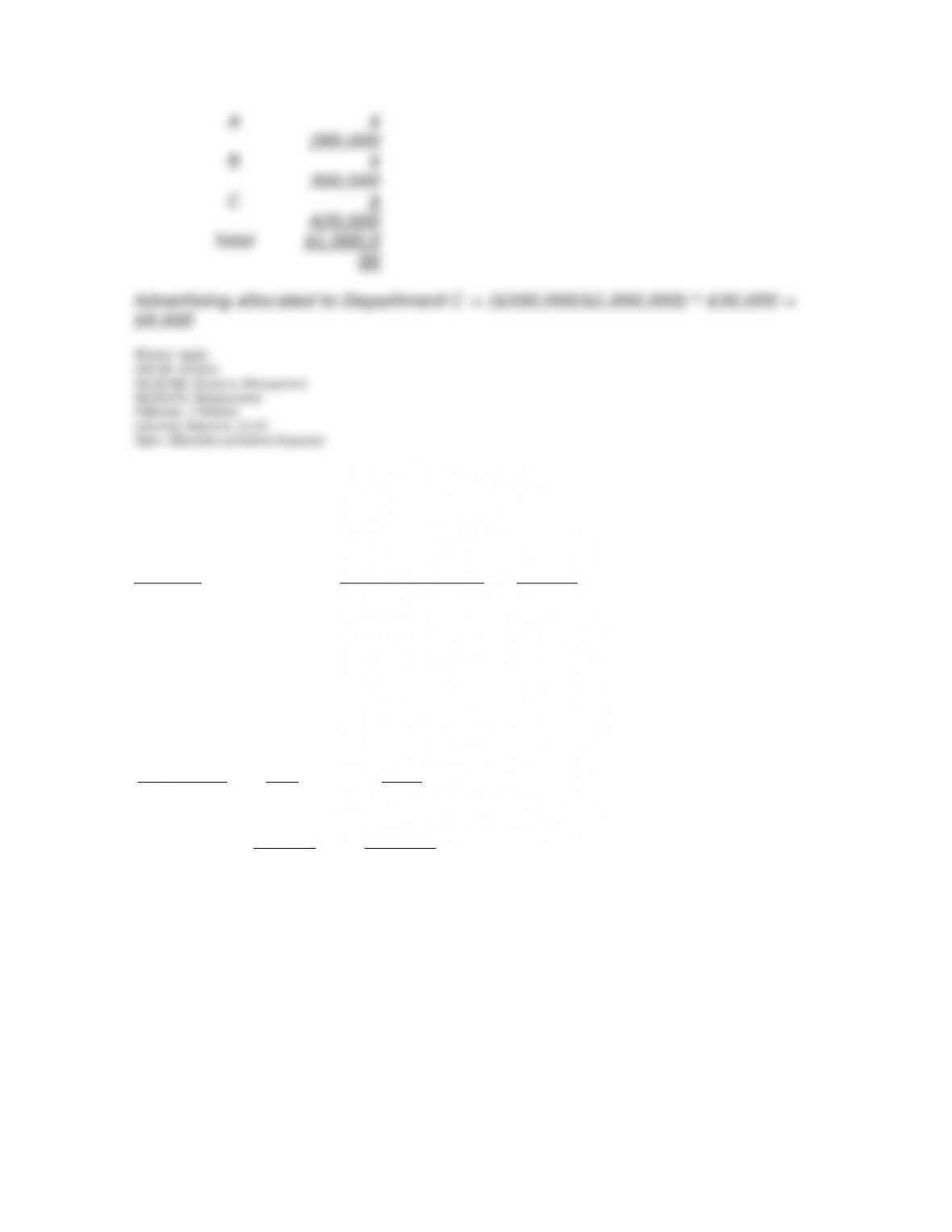

a storewide sale is likely to be:

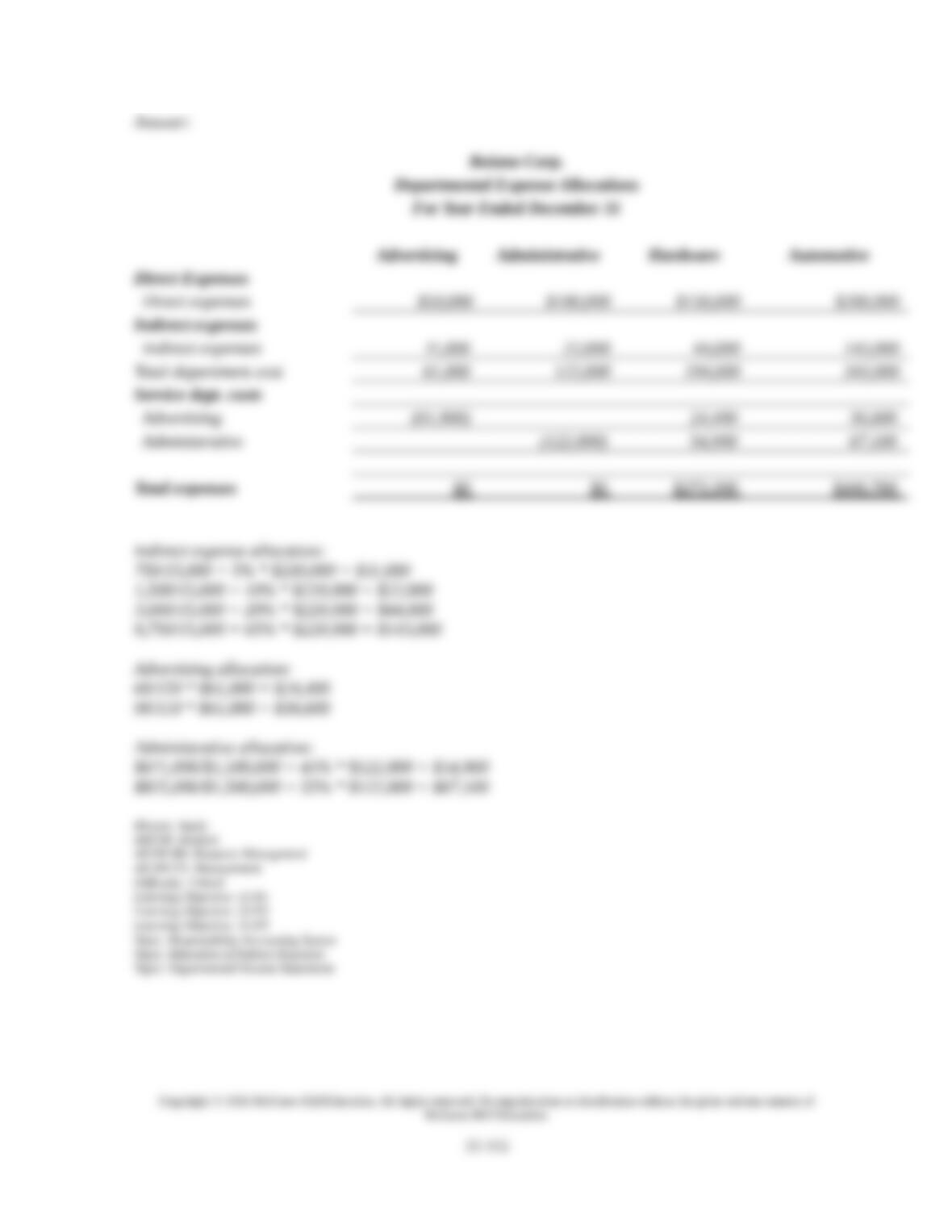

A. Floor space of each department.

B. Relative number of items each department had on sale.

C. Number of customers to enter each department.

D. An equal amount of cost for each department.

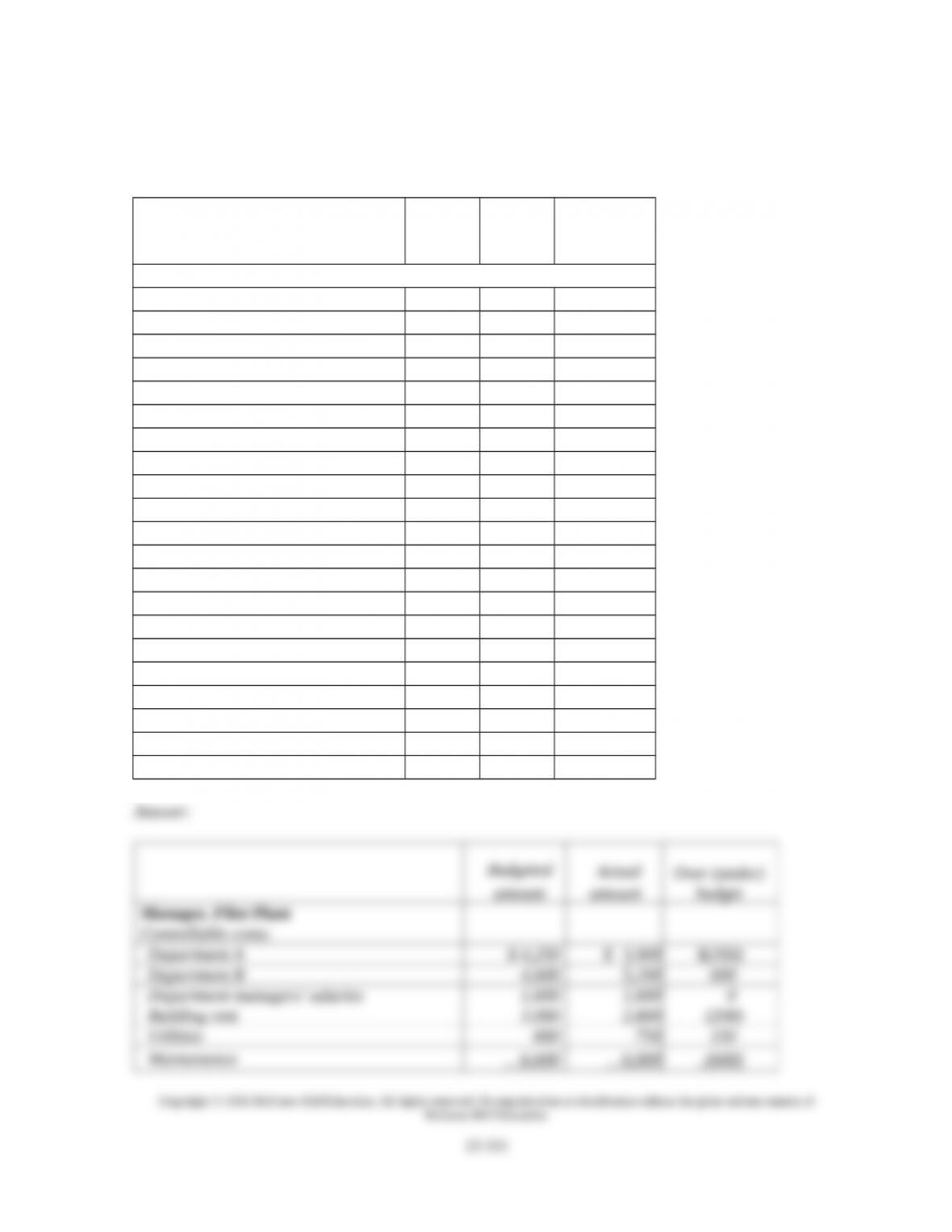

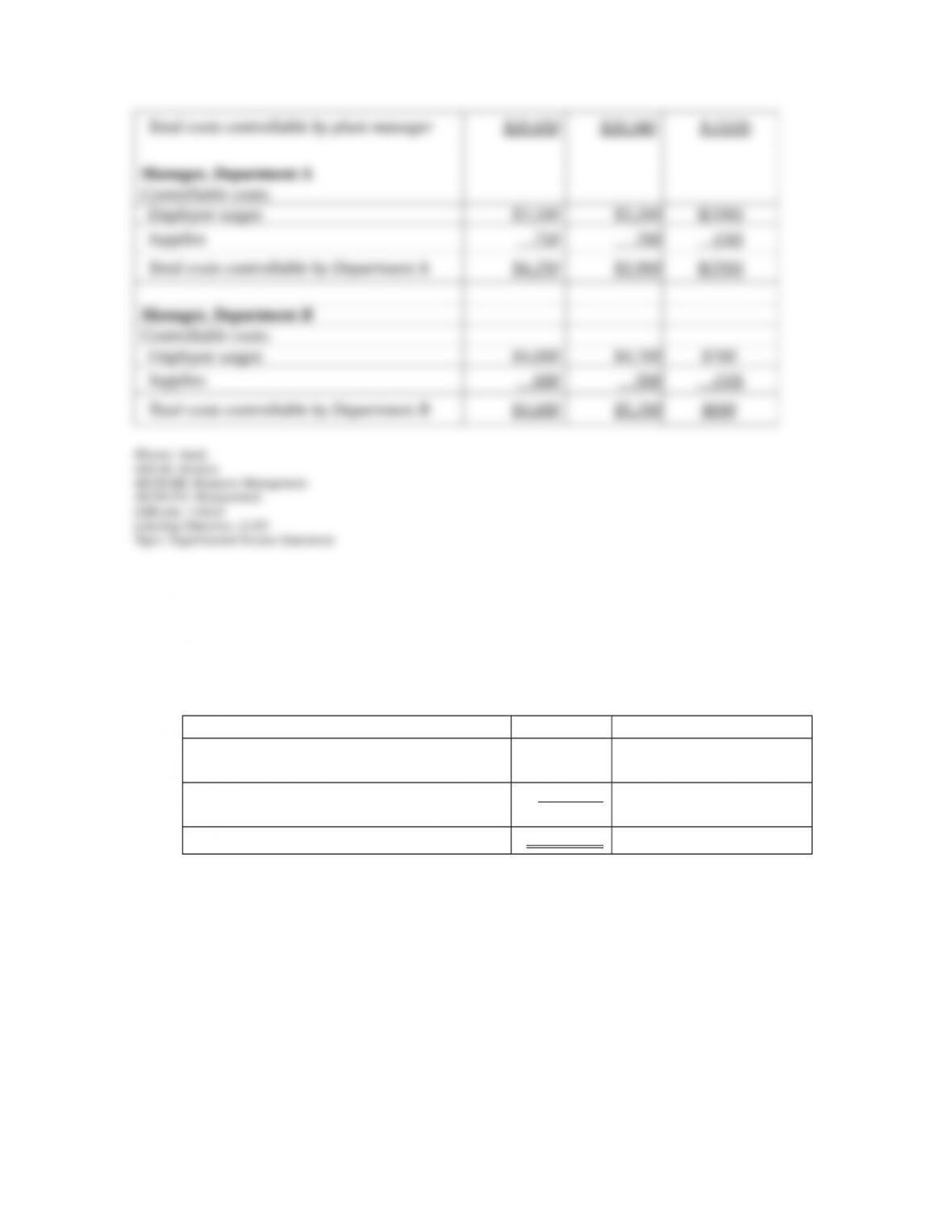

E. Proportion of sales of each department.

52. Costs that the manager has the power to determine or at least significantly affect are

called:

A. Uncontrollable costs.

B. Controllable costs.

C. Joint costs.

D. Direct costs.

E. Indirect costs.

53. A report that accumulates the actual expenses that a manager is responsible for and their

budgeted amounts is a:

A. Segmental accounting report.

B. Managerial cost report.

C. Controllable expense report.

D. Departmental accounting report.

E. Responsibility accounting performance report.

54. An accounting system that is set up to control costs and evaluate managers’ performance

by assigning costs to the managers responsible for controlling them is called a:

A. Cost accounting system.

B. Managerial accounting system.

C. Responsibility accounting system.

D. Financial accounting system.

E. Activity-based accounting system.

55. Costs that the manager does not have the power to determine or at least significantly affect

are:

A. Variable costs.

B. Uncontrollable costs.

C. Indirect costs.

D. Direct costs.

E. Joint costs.

56. Plans that identify costs and expenses under each manager’s control prior to the reporting

period, typically based on the flexible budget approach, are called:

A. Cost accounting systems.

B. Managerial accounting systems.

C. Responsibility accounting systems.

D. Responsibility accounting budgets.

E. Activity-based accounting systems.

57. Within an organizational structure, the person most likely to be evaluated in terms of

controllable costs would be:

A. A payroll clerk.

B. A cost center manager.

C. A production line worker.

D. A maintenance worker.

E. A sales representative.

58. The most useful data for evaluation of a manager’s cost performance is based on:

A. Controllable costs.

B. Contribution percentages.

C. Departmental contributions to overhead.

D. Uncontrollable expenses.

E. Direct costs.

59. In a responsibility accounting system:

A. Managers are responsible for their departments’ controllable costs.

B. Each accounting report contains all items allocated to a responsibility center.

C. Organized and clear lines of authority and responsibility are only incidental.

D. All managers at a given level have equal authority and responsibility.

E. Outputs of the departments are not part of the evaluation process.

60. Responsibility accounting performance reports:

A. Become more detailed at higher levels of management.

B. Are usually summarized at higher levels of management.

C. Are equally detailed at all levels of management.

D. Are useful in any format.

E. Are irrelevant at the highest level of management.

61. A responsibility accounting performance report displays:

A. Only actual costs.

B. Only budgeted costs.

C. Both actual costs and budgeted costs.

D. Only direct costs.

E. Only indirect costs.

62. Which of the following is not true regarding a responsibility accounting system?

A. It is designed to measure the performance of managers in terms of controllable costs.

B. It assigns responsibility for costs to the appropriate managerial level that controls those

costs.

C. It should not hold a manager responsible for costs over which the manager has no

influence.

D. It can be applied at any level of an organization.

E. It is only relevant in manufacturing companies.

63. A cost incurred to produce or purchase two or more products at the same time is a(n):

A. Product cost.

B. Incremental cost.

C. Differential cost.

D. Joint cost.

E. Fixed cost.

64. In regard to joint cost allocation, the “split-off point” is:

A. A physical basis method to allocate costs based on ratio of some physical characteristic.

B. The difference between the actual and market value of joint costs.

C. The point at which some products are sold and some remain in inventory.

D. The point at which separate products can be identified.

E. Not acceptable when using the value basis for allocating joint costs.

65. Allocating joint costs to products using a value basis method is based on their relative:

A. Sales values.

B. Direct costs.

C. Gross margins.

D. Total costs.

E. Variable costs.

66. Differential Chemical produced 10,000 gallons of Preon and 20,000 gallons of Paron.

Joint costs incurred in producing the two products totaled $7,500. At the split-off point, Preon

has a market value of $6.00 per gallon and Paron $2.00 per gallon. Compute the portion of the

joint costs to be allocated to Preon if the value basis is used.

A. $2,500.

B. $3,000.

C. $4,500.

D. $5,625.

E. $1,500.

67. Data pertaining to a company’s joint production for the current period follows:

L M

Quantities produced…………………. 200 lbs. 150 lbs.

Market value at split-off point…..…… $8/lb. $16/lb.

Compute the cost to be allocated to Product L for this period’s $660 of joint costs if the value

basis is used.

A. $264.

B. $396.

C. $330.

D. $1,364.

E. $796.

68. Data pertaining to a company’s joint production for the current period follows:

L M

Quantities produced…………………. 200 lbs. 150 lbs.

Market value at split-off

point………………………………. $8/lb. $16/lb.

Compute the cost to be allocated to Product M for this period’s $660 of joint costs if the value

basis is used.

A. $264.

B. $396.

C. $330.

D. $1,364.

E. $796.

69. A lumber mill bought a shipment of logs for $40,000. When cut, the logs produced a

million board feet of lumber in the following grades. Compute the cost to be allocated to Type

1 and Type 2 lumber, respectively, if the value basis is used.

Type 1—400,000 bd. ft. priced to sell at $0.12 per bd. ft.

Type 2— 400,000 bd. ft. priced to sell at $0.06 per bd. ft.

Type 3— 200,000 bd. ft. priced to sell at $0.04 per bd. ft.

A. $16,000; $16,000.

B. $13,333; $4,444.

C. $40,000; $24,000.

D. $24,000; $12,000.

E. $24,000; $8,000.

70. A lumber mill paid $70,000 for logs that produced 200,000 board feet of lumber in 3

different grades and amounts as follows:

Grade Production Market Price

Structural………… 25,000 board feet $1,350/1,000 bd. ft.

No. 1 Common…. 75,000 board feet $ 750/1,000 bd. ft.

No. 2 Common…. 100,000 board feet $ 300/1,000 bd. ft.

Compute the portion of the $70,000 joint cost to be allocated to No. 2 Common.

A. $ 0.

B. $17,500.

C. $23,333.

D. $35,000.

E. $70,000.

71. A granary allocates the cost of unprocessed wheat to the production of feed, flour, and

starch. For the current period, unprocessed wheat was purchased for $240,000, and the

following quantities of product and sales revenues were produced.

Product Pounds Price per Pound

Feed……….. 100,000 $0.70

Flour.......... 50,000 2.20

Starch........ 20,000 1.00

How much of the $240,000 cost should be allocated to feed?

A. $ 24,500.

B. $ 84,000.

C. $ 90,000.

D. $70,000.

E. $200,000.

72. Wren Pork Company uses the relative market value method of allocating joint costs in its

production of pork products. Relevant information for the current period follows:

Product Pounds Price/lb.

Price/lb.

Loin chops…………. 3,000 $5.00

Ground….. 10,000 2.00

Ribs………. 4,000 4.75

Bacon………… 6,000 3.50

The total joint cost for the current period was $43,000. How much of this cost should Wren

Pork allocate to Loin chops?

A. $ 0.

B. $ 5,909.

C. $ 8,600.

D. $10,750.

E. $43,000.

73. Calculating return on investment for an investment center is defined by the following

formula:

A. Contribution margin/Ending assets.

B. Gross profit/Ending assets.

C. Net income/Ending assets.

D. Income/Average invested assets.

E. Contribution margin/Average invested assets.

74. Investment center managers are usually evaluated using performance measures

A. that combine income and assets.

B. that combine income and capital.

C. based on assets only.

D. based on income only.

E. that combine assets and capital.

75. Two investment centers at Marshman Corporation have the following current-year income

and asset data:

Investment

Center A

Investment

Center B

Investment center income………………………. $415,000 525,000

Investment center average invested assets……… $2,400,000 1,950,000

The return on investment (ROI) for Investment Center A is:

A. 578.3%

B. 24.1%

C. 17.3%

D. 39.2%

E. 19.1%

76. Two investment centers at Marshman Corporation have the following current-year income

and asset data:

Investment

Center A

Investment

Center B

Investment center income………………………. $415,000 $525,000

Investment center average invested assets……… $2,400,000 $1,950,000

The return on investment (ROI) for Investment Center B is:

A. 371.4%

B. 26.9%

C. 24.1%

D. 39.2%

E. 21.7%

77. A retail store has three departments, S, T, and U, and does general advertising that benefits

all departments. Advertising expense totaled $50,000 for the year, and departmental sales

were as follows. Allocate advertising expense to Department T based on departmental sales.

Department S………………………….. $110,000

Department T………………………….. 213,750

Department U………………………….. 151,250

Total $475,000

A. $11,000.

B. $14,000.

C. $16,667.

D. $22,500.

E. $50,000.

78. Riemer, Inc. has four departments. Information about these departments is listed below.

Maintenance is a service department. If allocated maintenance cost is based on floor space

occupied by each of the other departments, compute the amount of maintenance cost allocated

to the Cutting Department.

Maintenance

Cutting

Assembly

Packaging

Direct costs……………………. $18,000 $30,000 $70,000 $45,000

Sq. ft. of space……………….. 500 1,500 2,000 2,500

No. of employees………..….. 2 3 16 4

A. $ 500.

B. $ 4,500.

C. $ 3,724.

D. $ 6,000.

E. $4,153.

79. CakeCo, Inc. has three operating departments. Information about these departments is

listed below. Maintenance is service department at CakeCo that incurred $12,000 of costs

during the period. If allocated maintenance cost is based on floor space occupied by each of

the operating departments, compute the amount of maintenance cost allocated to the Baking

Department.

Mixing Baking Packaging

Direct costs……………………. $21,000 $15,000 $9,000

Sq. ft. of space……………….. 1,000 1,500 500

A. $ 400.

B. $1,200.

C. $4,000.

D. $7,500.

E. $6,000.

80. Marks Corporation has two operating departments, Drilling and Grinding, and an office.

The three categories of office expenses are allocated to the two departments using different

allocation bases. The following information is available for the current period:

Office Expenses Total Allocation Basis

Salaries……………….. $30,000 Number of employees

Depreciation………… 20,000 Cost of goods sold

Advertising………….. 40,000 Net sales

Item Drilling Grinding Total

Number of employees 1,000 1,500 2,500

Net sales………………. $325,000 $475,000 $800,000

Cost of goods sold…. $ 75,000 $125,000 $200,000

The amount of the total office expenses that should be allocated to Grinding for the current

period is:

A. $ 35,750.

B. $ 45,000.

C. $ 54,250.

D. $ 90,000.

E. $600,000.

81. In a firm that manufactures clothing, the department that is responsible for actually

assembling the garments could best be described as a(n):

A. Service department.

B. Operating or production department.

C. Cost center.

D. Department in which all of the costs incurred are direct expenses.

E. Department in which all of the costs incurred are indirect expenses.

82. A company rents a building with a total of 50,000 square feet, which are evenly divided

between two floors. The company allocates the rent for space on the first floor at twice the

rate of space on the second floor. The total monthly rent for the building is $30,000. How

much of the monthly rental expense should be allocated to a department that occupies 10,000

square feet on the first floor?

A. $6,000.

B. $5,000.

C. $3,000.

D. $4,000.

E. $2,000.

83. A company pays $15,000 per period to rent a small building that has 10,000 square feet of

space. This cost is allocated to the company’s three departments on the basis of the amount of

the space occupied by each. Department One occupies 2,000 square feet of floor space,

Department Two occupies 3,000 square feet of -floor space, and Department Three occupies

5,000 square feet of floor space. If the rent is allocated based on the total square footage of the

space, Department One should be charged rent expense for the period of:

A. $4,400.

B. $3,000.

C. $4,000.

D. $2,200.

E. $2,000.

84. Ready Company has two operating (production) departments: Assembly and Painting.

Assembly has 150 employees and occupies 44,000 square feet; Painting has 100 employees

and occupies 36,000 square feet. Indirect factory expenses for the current period are as

follows:

Administration $ 80,000

Maintenance $100,000

Administration is allocated based on workers in each department; maintenance is allocated

based on square footage. The total amount of indirect factory expenses that should be

allocated to the Assembly Department for the current period is:

A. $ 48,000.

B. $ 55,000.

C. $103,000.

D. $104,000.

E. $110,000.

85. Ready Company has two operating (production) departments: Assembly and Painting.

Assembly has 150 employees and occupies 44,000 square feet; Painting has 100 employees

and occupies 36,000 square feet. Indirect factory expenses for the current period are as

follows:

Administration $ 80,000

Maintenance $100,000

Administration is allocated based on workers in each department; maintenance is allocated

based on square footage. The total amount of administration expense that should be allocated

to the Assembly Department for the current period is:

A. $ 48,000.

B. $ 55,000.

C. $103,000.

D. $104,000.

E. $110,000.

86. Canfield Technical School allocates administrative costs to its respective departments

based on the number of students enrolled, while maintenance and utilities are allocated per

square feet of the classrooms. Based on the information below, what is the total amount

allocated to the Welding Department (rounded to the nearest dollar) if administrative costs for

the school were $50,000, maintenance fees were $12,000, and utilities were $6,000?

Department Students Classrooms

Electrical…….….. 120 10,000 sq.

ft.

Welding……..… 70 12,000 sq. ft.

Accounting……. 50 8,000 sq. ft.

Carpentry……… 40

6,000 sq. ft.

Total 280 36,000 sq. ft.

A. $ 0.

B. $17,000.

C. $18,500.

D. $22,667.

E. $30,000.

87. Canfield Technical School allocates administrative costs to its respective departments

based on the number of students enrolled, while maintenance and utilities are allocated per

square feet of the classrooms. Based on the information below, what is the total amount of

administrative cost to the Accounting Department (rounded to the nearest dollar) if

administrative costs for the school were $50,000, maintenance fees were $12,000, and utilities

were $6,000?

Department Students Classrooms

Electrical…….…. 120 10,000 sq.

ft.

Welding……. 70 12,000 sq. ft.

Accounting……… 50 8,000 sq. ft.

Carpentry………. 40

6,000 sq. ft.

Total 280 36,000 sq. ft.

A. $ 8,929.

B. $17,000.

C. $18,500.

D. $22,667.

E. $11,111.

88. Canfield Technical School allocates administrative costs to its respective departments

based on the number of students enrolled, while maintenance and utilities are allocated per

square feet of the classrooms. Based on the information below, what is the total amount of

maintenance cost to the Carpentry Department (rounded to the nearest dollar) if

administrative costs for the school were $50,000, maintenance fees were $12,000, and utilities

were $6,000?

Department Students Classrooms

Electrical…….…. 120 10,000 sq.

ft.

Welding……. 70 12,000 sq. ft.

Accounting……… 50 8,000 sq. ft.

Carpentry………. 40

6,000 sq. ft.

Total 280 36,000 sq. ft.

A. $ 1,714.

B. $12,000.

C. $1,850.

D. $2,000.

E. $1,111.

89. Brownley Company has two service departments and two operating (production)

departments. The Payroll Department services all three of the other departments in proportion

to the number of employees in each. The Maintenance Department costs are allocated to the

two operating departments in proportion to the floor space used by each. Listed below are the

operating data for the current period:

Service Depts. Production Depts.

Payroll Maintenance Cutting Assembly

Direct costs…………… $20,400 $25,500 $76,500 $105,400

No. of personnel……. 15 15 45

Sq. ft. of space……… 10,000 15,000

The total cost of operating the Cutting Department for the current period is:

A. $14,280.

B. $15,912.

C. $76,500.

D. $90,780.

E. $92,412.

90. Brownley Company has two service departments and two operating (production)

departments. The Payroll Department services all three of the other departments in proportion

to the number of employees in each. The Maintenance Department costs are allocated to the

two operating departments in proportion to the floor space used by each. Listed below are the

operating data for the current period:

Service Depts. Production Depts.

Payroll Maintenance Cutting Assembly

Direct costs…………… $20,400 $25,500 $76,500 $105,400

No. of personnel……. 15 15 45

Sq. ft. of space……… 10,000 15,000

The total cost of operating the Maintenance Department for the current period is:

A. $14,280.

B. $15,912.

C. $25,500.

D. $29,580.

E. $22,412.

91. Flamingos, Inc. has four departments. The Administrative Department costs are allocated

to the other three departments based on the number of employees in each and the Maintenance

Department costs are allocated to the Assembly and Packaging Departments based on their

occupied space. Data for these departments follows:

Operating costs……..

No. of employees ….

Sq. ft. of space……...

Admin. Maintenance Assembly Packaging

$30,000 $15,000

2

$70,000

6

2,000

$45,000

4

3,000

The total amount of the Administrative Department’s cost that would eventually be allocated

to the Packaging Department is:

A. $ 4,800.

B. $12,000.

C. $10,000.

D. $18,000.

E. $13,000.

92. Pepper Department store allocates its service department expenses to its various operating

(sales) departments. The following data is available for its service departments:

Expense Basis for allocation Amount

Rent Square feet of floor space $24,000

Advertising Amount of dollar sales $30,000

Administrative Number of employees $45,000

The following information is available for its three operating (sales) departments:

Square Dollar Number of

Department

Feet

Sales

employees

A 3,000 $280,000 6

B 3,400 $300,000 8

C 3,600 $420,000 10

Totals 10,000 $1,000,000 24

What is the total expense allocated to Department B?

A. $29,375.

B. $30,462.

C. $30,500.

D. $30,775.

E. $32,160.

93. Pepper Department store allocates its service department expenses to its various operating

(sales) departments. The following data is available for its service departments:

Expense Basis for allocation Amount

Rent Square feet of floor space $24,000

Advertising Amount of dollar sales $30,000

Administrative Number of employees $45,000

The following information is available for its three operating (sales) departments:

Square Dollar Number of

Department

Feet

Sales

employees

A 3,000 $280,000 6

B 3,400 $300,000 8

C 3,600 $420,000 10

Totals 10,000 $1,000,000 24

What is the total advertising expense allocated to Department C?

A. $30,000.

B. $ 9,000.

C. $12,500.

D. $10,800.

E. $ 7,500.

94. Super Grocery store allocates its service department expenses to its various operating

(sales) departments. The following data is available for its service departments:

Expense Basis for allocation Amount

Administrative Square feet of floor space $15,000

Advertising Amount of dollar sales $ 8,000

The following information is available for its three operating (sales) departments:

Square Dollar

Department

Feet

Sales

Produce 1,000 $80,000

Bakery 800 $30,000

Meats 1,200 $42,000

Totals 3,000 $152,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-51

What is the total administrative expense allocated to the Meats department?

A. $6,000.

B. $9,000.

C. $4,145.

D. $1,200.

E. $3,000.

95. A college uses advisors who work with all students in all divisions of the college. The

most useful allocation basis for the salaries of these employees would likely be:

A. number of classes offered in each division.

B. student graduation rate.

C. square footage of each division.

D. number of students advised from each division.

E. relative salaries of division heads.

96. A firm produces and sells two products, Plus and Max. The following information is

available relating to setup costs (a part of factory overhead):

Plus Max

Units produced……………….. 200 16,000

Batch size (units)…………….. 10 400

Number of setups…………….. 20 40

Direct labor hours per unit... 5 5

Total direct labor hours……. 1,000 80,000

Cost per setup………………….

$ 1,080

Total setup cost………………. $64,800

With traditional two-stage allocation of overhead costs, using direct labor hours as the

allocation base, the setup cost portion of overhead that is allocated to each unit of product for

Plus and Max, respectively is:

A. $.80; $.80.

B. $3.20; $3.20.

C. $4.00; $4.00.

D. $160.00; $12,800.00.

E. $200.00; $16,000.00.

97. A firm produces and sells two products, Plus and Max. The following information is

available relating to setup costs (a part of factory overhead):

Plus Max

Units produced……………….. 200 16,000

Batch size (units)…………….. 10 400

Number of setups…………… 20 40

Direct labor hours per unit... 5 5

Total direct labor hours……. 1,000 80,000

Cost per setup……………….. $ 1,080

Total setup cost……………… $64,800

Using number of setups as the activity base, the amount of setup cost allocated to each unit of

product for Plus and Max, respectively is:

A. $21.60; $.54.

B. $54.00; $27.00.

C. $60.00; $60.00.

D. $108.00; $2.70.

E. $200.00; $16,000.00

98. Rent and maintenance expenses would most likely be allocated based on:

A. Sales volume by department.

B. Square feet of floor space occupied.

C. Number of hours worked.

D. Number of invoices processed.

E. Number of employees in each department.

99. In the preparation of departmental income statements, the preparer completes the

following steps in the following order:

A. Identify direct expenses; allocate indirect expenses; allocate service department expenses.

B. Identify indirect expenses; allocate direct expenses; allocate service department expenses.

C. Identify service department expenses; allocate direct expenses; allocate indirect expenses.

D. Identify direct expenses, allocate service department expenses; allocate indirect expenses.

E. Allocate all expenses.

100. Marian Corporation has two separate divisions that operate as profit centers. The

following information is available for the most recent year:

Black Division Navy Division

Sales (net)……………… $200,000 $400,000

Salary expense……….. 28,000 48,000

Cost of goods sold…… 100,000 159,000

The Black Division occupies 20,000 square feet in the plant. The Navy Division occupies

30,000 square feet. Rent is an indirect expense and is allocated based on square footage. Rent

expense for the year was $50,000. Compute gross profit for the Black and Navy Divisions,

respectively.

A. $72,000; $193,000.

B. $172,000; $352,000.

C. $100,000; $241,000.

D. $52,000; $163,000.

E. $72,000; $163,000.

101. Marian Corporation has two separate divisions that operate as profit centers. The

following information is available for the most recent year:

Black Division Navy Division

Sales (net)……………… $200,000 $400,000

Salary expense……….. 28,000 48,000

Cost of goods sold….. 100,000 159,000

The Black Division occupies 20,000 square feet in the plant. The Navy Division occupies

30,000 square feet. Rent is an indirect expense and is allocated based on square footage. Rent

expense for the year was $50,000. Compute departmental income for the Black and Navy

Divisions, respectively.

A. $52,000; $163,000.

B. $172,000; $352,000.

C. $72,000; $163,000.

D. $72,000; $193,000.

E. $100,000; $241,000.

102. Fallow Corporation has two separate profit centers. The following information is

available for the most recent year:

West Division East Division

Sales (net)……………… $200,000 $350,000

Salary expense……….. 26,000 40,000

Cost of goods sold….. 80,000 175,000

The West Division occupies 5,000 square feet in the plant. The East Division occupies 3,000

square feet. Rent, which was $40,000 for the year, is an indirect expense and is allocated

based on square footage. Compute operating income for the West Division.

A. $120,000.

B. $95,000.

C. $94,000.

D. $69,000.

E. $54,000.

103. The amount by which a department’s sales exceed its direct expenses is:

A. Net sales.

B. Gross profit.

C. Departmental profit.

D. Contribution margin.

E. Departmental contribution to overhead.

104. Departmental contribution to overhead is calculated as the amount of sales of the

department less:

A. Controllable costs.

B. Product and period costs.

C. Direct expenses.

D. Direct and indirect costs.

E. Joint costs.

105. The Menswear Department of Major’s Department Store had sales of $188,000, cost of

goods sold of $132,500, indirect expenses of $13,250, and direct expenses of $27,500 for the

current period. The Menswear Department’s contribution to overhead as a percent of sales is:

A. 7.8%.

B. 14.9%.

C. 29.5%.

D. 66.7%.

E. 85.4%.

106. Ultimo Co. operates three production departments as profit centers. The following

information is available for its most recent year. Department 1’s contribution to overhead as a

percent of sales is:

Cost of Direct Indirect

Dept. Sales Goods Sold Expenses Expenses

1$1,000,000 $700,000 $100,000 $ 80,000

2 400,000 150,000 40,000 100,000

3 700,000 300,000 150,000 20,000

107. Ultimo Co. operates three production departments as profit centers. The following

information is available for its most recent year. Department 2’s contribution to overhead in

dollars is:

Cost of Direct Indirect

Dept. Sales Goods Sold Expenses Expenses

1$1,000,000 $700,000 $100,000 $ 80,000

2 400,000 150,000 40,000 100,000

3 700,000 300,000 150,000 20,000

A. $210,000.

B. $350,000.

C. $ 10,000.

D. $260,000.

E. $150,000.

108. Ultimo Co. operates three production departments as profit centers. The following

information is available for its most recent year. Which department has the greatest

departmental contribution to overhead and what is the amount contributed?

Cost of Direct Indirect

Dept. Sales Goods Sold Expenses Expenses

1$1,000,000 $700,000 $100,000 $ 80,000

2 400,000 150,000 40,000 100,000

3 700,000 300,000 150,000 20,000

A. Dept. 3; $ 400,000.

B. Dept. 1; $1,000,000.

C. Dept. 2; $ 100,000.

D. Dept. 3; $ 250,000.

E. Dept. 2; $ 150,000.

109. A system of performance measures, including nonfinancial measures, used to assess

company and division manager performance is:

A. Hurdle rate.

B. Return on investment.

C. Balanced scorecard.

D. Residual income.

E. Investment turnover.

110. Which of the following is not one of the perspectives used to analyze performance using

the balanced scorecard?

A. Customer

B. Financial/owners

C. Internal process

D. Number of employees

E. Innovation and learning

111. Return on investment can be split into which of the following two measures?

A. Investment center income and profit margin.

B. Profit margin and net income.

C. Investment center average assets and investment turnover.

D. Residual income and operating income.

E. Profit margin and investment turnover.

112. Profit margin for an investment center measures:

A. Investment center income earned per dollar of sales.

B. How efficiently an investment center generates sales from its invested assets.

C. Investment center income compared to target investment center income

D. Departmental contribution to overhead

E. Investment center income generated from its invested assets

113. Carter Company reported the following financial numbers for one of its divisions for the

year; average total assets of $4,100,000; sales of $4,525,000; cost of goods sold of

$2,550,000; and operating expenses of $1,372,000. Compute the division’s return on

investment:

A. 30.3%.

B. 23.6%.

C. 13.3%.

D. 10.4%.

E. 14.7%.

114. Carter Company reported the following financial numbers for one of its divisions for the

year; average total assets of $4,100,000; sales of $4,525,000; cost of goods sold of

$2,550,000; and operating expenses of $1,372,000. Assume a target income of 10% of

average invested assets. Compute residual income for the division:

A. $203,000.

B. $193,000.

C. $150,500.

D. $ 60,300.

E. $197,500.

115. Dartford Company reported the following financial data for one of its divisions for the

year; average investment center total assets of $3,500,000; investment center income

$610,000; a target income of 12% of average invested assets. The residual income for the

division is:

A. $536,800.

B. $1,030,000.

C. $190,000.

D. $683,200.

E. $493,200.

116. Kragle Corporation reported the following financial data for one of its divisions for the

year; average invested assets of $470,000; sales of $930,000; and income of $105,000. The

investment center profit margin is:

A. 22.3%.

B. 50.5%.

C. 197.9%.

D. 447.6%.

E. 11.3%.

117. Kragle Corporation reported the following financial data for one of its divisions for the

year; average invested assets of $470,000; sales of $930,000; and income of $105,000. The

investment turnover is:

A. 22.3.

B. 50.5.

C. 1.98.

D. 447.6.

E. 11.3.

118. If a company reports profit margin of 31.6% and investment turnover of 1.30 for one of

its investment centers, the return on investment must be:

A. 24.3%.

B. 41.1%.

C. 32.9%.

D. 30.3%.

E. 4.11%.

119. Holo Company reported the following financial numbers for one of its divisions for the

year; average total assets of $5,800,000; sales of $5,375,000; cost of goods sold of

$3,225,000; and operating expenses of $1,147,000. Compute the division’s return on

investment:

A. 18.6%.

B. 21.3%.

C. 17.3%.

D. 10.4%.

E. 14.7%.

120. Holo Company reported the following financial numbers for one of its divisions for the

year; average total assets of $5,800,000; sales of $5,375,000; cost of goods sold of

$3,225,000; and operating expenses of $1,147,000. Assume a target income of 15% of

average invested assets. Compute residual income for the division:

A. $150,450.

B. $196,750.

C. $150,500.

D. $133,000.

E. $100,300.

121. Pleasant Hills Properties is developing a golf course subdivision that includes 250 home

lots; 100 lots are golf course lots and will sell for $95,000 each; 150 are street frontage lots

and will sell for $65,000. The developer acquired the land for $1,800,000 and spent another

$1,400,000 on street and utilities improvement. Compute the amount of joint cost to be

allocated to the golf course lots using value basis.

A. $1,920,000.

B. $720,000.

C. $1,620,800.

D. $1,579,200.

E. $1,080,000.

122. Pleasant Hills Properties is developing a golf course subdivision that includes 250 home

lots; 100 lots are golf course lots and will sell for $95,000 each; 150 are street frontage lots

and will sell for $65,000. The developer acquired the land for $1,800,000 and spent another

$1,400,000 on street and utilities improvement. Compute the amount of joint cost to be

allocated to the street frontage lots using value basis.

A. $1,920,000.

B. $720,000.

C. $1,620,800.

D. $1,579,200.

E. $1,080,000.

123. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Brickland. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Purchasing department expense to

be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $17,600.

E. $25,600.

124. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Brickland. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

Required: Compute the amount of Purchasing department expense to be allocated to

Assembly.

A. $6,400.

B. $9,900.

C. $8,100.

D. $14,400.

E. $25,600.

125. The following is a partially completed departmental expense allocation spreadsheet for

Brickland. It reports the total amounts of direct and indirect expenses for its four departments.

Purchasing department expenses are allocated to the operating departments on the basis of

purchase orders. Maintenance department expenses are allocated based on square footage.

Compute the amount of Maintenance department expense to be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $9,000.

E. $25,600.

126. The following is a partially completed lower section of a departmental expense

allocation spreadsheet for Brickland. It reports the total amounts of direct and indirect

expenses for the four departments. Purchasing department expenses are allocated to the

operating departments on the basis of purchase orders. Maintenance department expenses are

allocated based on square footage. Compute the amount of Maintenance department expense

to be allocated to Fabrication.

Purchasing Maintenance Fabrication Assembly

Operating costs $32,000 $18,000 $96,000 $62,000

No. of purchase orders 16 4

Sq. ft. of space 3,300 2,700

A. $6,400.

B. $9,900.

C. $8,100.

D. $9,000.

E. $25,600.

127. Which of the following represents the correct formula for calculating cycle time for a

manufacturer?

A. Process time + inspection time – move time – wait time.

B. Process time – inspection time + move time + wait time.

C. Process time + inspection time + move time + wait time.

D. Process time – inspection time – move time – wait time.

E. Process time + inspection time + move time – wait time.

128. Which of the following statements is correct concerning the elements of cycle time?

A. Move time is the time spent moving (1) raw materials from storage to production and (2)

goods in process from one factory location to another factory location.

B. Inspection time is the time spent producing the product.

C. Process time is considered non-value-added time.

D. Wait time is considered value-added time.

E. Cycle efficiency is the ratio of non-value-added time to total cycle time.

129. Using the information below, compute the manufacturing cycle time:

Process time 6.0 hours

Inspections time .5 hours

Move time .6 hours

Wait time .9 hours

Warehouse storage time 72.0 hours

A. 7.5 hours.

B. 6.5 hours.

C. 8.0 hours.

D. 80.0 hours.

E. 7.1 hours.

130. Using the information below, compute the cycle efficiency:

Process time 6.0 hours

Inspections time .5 hours

Move time .6 hours

Wait time .9 hours

Warehouse storage time 72.0 hours

A. 93.8%.

B. 81.3%.

C. 100.0%.

D. 75.0%.

E. 88.8%.

131. When the selling division in an internal transfer has unsatisfied demand from outside

customers for the product that is being transferred, then the lowest acceptable transfer price as

far as the selling division is concerned is:

A. variable cost of producing a unit of product.

B. the full absorption cost of producing a unit of product.

C. the market price charged to outside customers, less costs saved by transferring internally.

D. the amount that the purchasing division would have to pay an outside seller to acquire a

similar product for its use.

E. all the costs of producing a unit of product.

132. Division M makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Division O of the same company would like to use the part manufactured by Division M in

one of its products. Division O currently purchases a similar part made by an outside

company for $70 per unit and would substitute the part made by Division M. Division O

requires 5,000 units of the part each period. Division M can sell every unit it produces on the

outside market. What should be the lowest acceptable transfer price from the perspective of

Division O?

A. $75

B. $66

C. $16

D. $50

E. $25

133. Part AR3 costs the Southwestern Division of Luxon Corporation $26 to make-direct

materials are $10, direct labor is $4, variable manufacturing overhead is $9, and fixed

manufacturing overhead is $3. Southwestern Division sells Part AR3 to other companies for

$30. The Northeastern Division of Luxon Corporation can use Part AR3 in one of its products.

The Southwestern Division has enough idle capacity to produce all of the units of Part AR3

that the Northeastern Division would require. What is the lowest transfer price at which the

Southwestern Division should be willing to sell Part AR3 to the Northeastern Division?

A. $30

B. $26

C. $23

D. $27

E. $21

134. Part 7B costs the Midwest Division of Frackle Corporation $30 to make, of which $21 is

variable. Midwest Division sells Part 7B to other companies for $47. The Northern Division

of Frackle Corporation can use Part 7B in one of its products. The Midwest Division has

enough idle capacity to produce all of the units of Part 7B that the Northern Division would

require. What is the lowest transfer price at which the Midwest Division should be willing to

sell Part 7B to the Northern Division?

A. $30

B. $21

C. $47

D. $17

E. $20

135. Division P of Launch Corporation has the capacity for making 75,000 wheel sets per

year and regularly sells 60,000 each year on the outside market. The regular sales price is

$100 per wheel set, and the variable production cost per unit is $65. Division Q of Launch

Corporation currently buys 30,000 wheel sets (of the kind made by Division P) yearly from an

outside supplier at a price of $90 per wheel set. If Division Q were to buy the 30,000 wheel

sets it needs annually from Division P at $87 per wheel set, the change in annual net operating

income for the company as a whole, compared to what it is currently, would be:

A. $600,000

B. $225,000

C. $750,000

D. $135,000

E. $700,000

136. Division X makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Selling price to outside customers…………….…… $50

Variable cost per unit………………………………. $30

Total fixed costs……………………………. ……… $400,000

Capacity in units……………………………………. $25,000

Division Y of the same company would like to use the part manufactured by Division X in

one of its products. Division Y currently purchases a similar part made by an outside company

for $49 per unit and would substitute the part made by Division X. Division Y requires 5,000

units of the part each period. Division X has ample excess capacity to handle all of Division

Y’s needs without any increase in fixed costs and without cutting into outside sales. According

to the formula in the text, what is the lowest acceptable transfer price from the standpoint of

the selling division?

A. $50

B. $49

C. $46

D. $30

E. $20

137. Division A makes a part that it sells to customers outside of the company. Data

concerning this part appear below:

Selling price to outside customers…………….…… $40

Variable cost per unit………………………………. $30

Total fixed costs……………………………. ……… $10,000

Capacity in units……………………………………. $20,000

Division B of the same company would like to use the part manufactured by Division A in one

of its products. Division B currently purchases a similar part made by an outside company for

$38 per unit and would substitute the part made by Division A. Division B requires 5,000

units of the part each period. Division A has ample capacity to produce the units for Division

B without any increase in fixed costs and without cutting into sales to outside customers. If

Division A sells to Division B rather than to outside customers, the variable cost be unit would

be $1 lower. What should be the lowest acceptable transfer price from the perspective of

Division A?

A. $40

B. $38

C. $30

D. $29

E. $10

138. The Mixed Nuts Division of Yummy Snacks, Inc. had the following operating results

last year:

Sales (140,000 pounds of product)…………… $70,000

Variable expenses………………………………. 42,000

Contribution margin…………………………….$28,000

Fixed expenses………………………………… 12,000

Income………………………………………… $16,000

Yummy expects identical operating results in the division this year. The Mixed Nuts Division

has the ability to produce and sell 200,000 pounds of product annually. Assume that the Trail

Mix Division of Yummy wants to purchase an additional 20,000 pounds of nuts from the

Mixed Nuts Division. Mixed Nuts will be able to increase its profit by accepting any transfer

price above:

A. $0.25 per pound

B. $0.08 per pound

C. $0.15 per pound

D. $0.30 per pound

E. $0.10 per pound

139. The Dark Chocolate Division of Yummy Snacks, Inc. had the following operating results

last year:

Sales (150,000 pounds of chocolate)……………$60,000

Variable expenses………………………………. 37,500

Contribution margin……………………………. 22,500

Fixed expenses…………………………………. 12,000

Profit…………………………………………… $10,500

Dark Chocolate expects identical operating results this year. The Dark Chocolate Division has

the ability to produce and sell 200,000 pounds of chocolate annually. Assume that the Peanut

Butter Division of Yummy Snacks wants to purchase an additional 20,000 pounds of

chocolate from the Dark Chocolate Division. Assume that the Dark Chocolate Division is

currently operating at its capacity of 200,000 pounds of chocolate. Also assume again that the

Peanut Butter Division wants to purchase an additional 20,000 pounds of chocolate from Dark

Chocolate. Under these conditions, what amount per pound of chocolate would Dark

Chocolate have to charge Peanut Butter in order to maintain its current profit?

A. $0.40 per pound

B. $0.08 per pound

C. $0.15 per pound

D. $0.25 per pound

E. $0.30 per pound

140. Division X makes a part with the following characteristics:

Production capacity…………….…………………… 25,000 units

Selling price to outside customers…………………… $18

Variable cost per unit…………………………….….. $11

Fixed cost, total……………………………………. … $100,000

Division Y of the same company would like to purchase 10,000 units each period from

Division X. Division Y now purchases the part from an outside supplier at a price of $17 each.

Suppose Division X has ample excess capacity to handle all of Division Y’s needs without any

increase in fixed costs and without cutting into sales to outside customers. If Division X

refuses to accept the $17 price internally and Division Y continues to buy from the outside

supplier, the company as a whole will be:

A. worse off by $70,000 each period.

B. better off by $10,000 each period.

C. worse off by $60,000 each period.

D. worse off by $20,000 each period.

E. better off by $60,000 each period.

141. Division A produces a part with the following characteristics:

Capacity in units…………….…………………… …. 50,000

Selling price per unit…………………… …………… $30

Variable cost per unit…………………………….….. $18

Fixed cost per unit…………………………………… $3

Division B, another division in the company, would like to buy this part from Division A.

Division B is presently purchasing the part from an outside source at $28 per unit. If Division

A sells to Division B, $1 in variable costs can be avoided. Suppose Division A is currently

operating at capacity and can sell all of the units it produces on the outside market for its

usual selling price. From the point of view of Division A, any sales to Division B should be

priced no lower than:

A. $27

B. $29

C. $20

D. $28

E. $21

142. Match the appropriate definition with the following terms:

(a) A department or unit that incurs costs without directly generating revenues.

(b) A department or unit that generates revenues and incurs costs, in which the manager is

also responsible for investments made in operating assets.

(c) Costs that are incurred for the joint benefit of more than one department and cannot be

readily traced to only one department.

(d) Costs readily traced to a specific department because they are incurred for the sole

benefit of that department.

(e) Costs incurred to produce or purchase two or more products at the same time.

(f) Costs for which a manager has the power to determine or at least significantly affect.

(g) A department that generates revenues and incurs costs.

__________ (1) Direct expenses

__________ (2) Profit center

__________ (3) Controllable costs

__________ (4) Indirect expenses

__________ (5) Cost center

__________ (6) Joint cost

__________ (7) Investment center

1. D; 2. G; 3. F; 4. C; 5. A; 6. E; 7. B

Blooms: Remember

AACSB: Communication

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 1 Easy

Learning Objective: 22-A1

Learning Objective: 22-C1

Learning Objective: 22-P1

Topic: Evaluating Investment Center Performance

Topic: Direct and Indirect Expenses

Topic: Responsibility Accounting System

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-87

143. Match the appropriate definition a through h with the following terms:

(a) A department whose manager is judged on the ability to generate revenues in excess of the

department’s costs.

(b) A department or unit that generates revenues and incurs costs, in which the manager is

also responsible for investments made in operating assets.

(c) Set up to control costs and evaluate managers’ performances by assigning costs to the

managers responsible for controlling them.

(d) Compares actual and budgeted costs and expenses under the control of a manager.

(e) A department whose manager is judged on the ability to control costs by keeping them

within a satisfactory range.

(f) A measure of departmental sales less direct expenses.

__________ (1) Investment center

__________ (2) Performance report

__________ (3) Cost center

__________ (4) Departmental contribution to overhead

__________ (5) Profit center

__________ (6) Responsibility accounting system

1. B; 2. D; 3. E; 4. F; 5. A; 6. C

Blooms: Remember

AACSB: Communication

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 1 Easy

Learning Objective: 22-C1

Learning Objective: 22-P1

Learning Objective: 22-P3

Topic: Direct and Indirect Expenses

Topic: Responsibility Accounting System

Topic: Departmental Income Statements

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-88

Short Answer Questions

144. What is a profit center and how is its performance evaluated?

145. What is a cost center and how is its performance evaluated?

146. What is the main difference between a cost center and a profit center?

147. What is the purpose of a departmental accounting system?

148. What is the purpose of a responsibility accounting system?

149. What is an investment center and how is its performance evaluated?

150. Explain the difference between direct and indirect expenses in accounting for

departments.

151. How do companies decide what allocation bases to use to allocate indirect costs to

departments?

152. Describe the information found on a responsibility accounting performance report.

153. Define joint costs and explain how joint costs can be allocated.

154. In the process of preparing department income statements, a company uses there are

three steps before the statements can be completed. Describe those steps.

155. What is the cycle time for a manufacturer? What does it reveal about the manufacturing

process?

156. Riu Corporation has a Parts Division that does work for other Divisions in the company

as well as for outside customers. The company’s Repair Division has asked the Parts Division

to provide it with 2,000 special parts each year. The special parts would require $17.00 per

unit in variable production costs. The Repair Division has a bid from an outside supplier for

the special parts at $28.00 per unit. In order to have time and space to produce the special

part, the Parts Division would have to cut back production of another part-the B83 that it

presently is producing. The B83 sells for $34.00 per unit, and requires $22.00 per unit in

variable production costs. Packaging and shipping costs of the B83 are $4.00 per unit.

Packaging and shipping costs for the new special part would be only $0.50 per unit. The Parts

Division is now producing and selling 10,000 units of the B83 each year. Production and sales

of the B83 would drop by 10% if the new special part is produced for the Repair Division.

Required:

a. What is the range of transfer prices within which both the Divisions’ profits would increase

as a result of agreeing to the transfer of 2,000 special parts per year from the Parts Division to

the Repair Division?

b. Is it in the best interests of Riu Corporation for this transfer to take place? Explain.

157. Regal Furniture Company allocates its indirect salaries of $22,500 on the basis of sales.

Determine the indirect salaries allocated to Departments 1 and 2 using the following

information.

Dept.1 Dept.2 Combined

Revenues from sales…….. $182,000 $78,000 $260,000

Direct Salaries…………….. 42,250 22,750 65,000

Salaries allocated to Dept. 1 _______________

Salaries allocated to Dept. 2 _______________

158. A company rents a small building with 10,000 square feet of space for $100,000 per year.

The rent is allocated to the company’s three departments on the basis of the value of the space

occupied by each. Department One occupies 1,500 square feet of ground-floor space,

Department Two occupies 3,500 square feet of ground-floor space, and Department Three

occupies 5,000 square feet of second-floor space. If rent for comparable floor space in the

neighborhood averages $15.00 per sq. ft. for ground-floor space and $10.00 per sq. ft. for

second-floor space, what annual rent expense should be charged to each department?

159. A retail store has three departments, A, B, and C, each of which has four full-time

employees. The store does general advertising that benefits all departments. Advertising

expense totaled $90,000 for the current year, and departmental sales were:

Department A……………… $308,000

Department B……………… 644,000

Department C……………… 448,000

Total sales…………………………......$1,400,000

Calculate the amount of advertising expense that should be allocated to each department?

160. A company produces two joint products (called 301 and 302) in a single operation that

uses one raw material called Fruge. Four hundred gallons of Fruge were purchased at a cost of

$800 and were used to produce 150 gallons of Product 301, selling for $5 per gallon, and 75

gallons of Product 302, selling for $15 per gallon. How much of the $800 cost should be

allocated to each product, assuming that the company allocates cost based on sales revenue?

161. A company produces two products, XX and YY, from a single raw material called Zub.

Zub is purchased in 55-gallon drums, and the contents of one drum are sufficient to produce

30 gallons of XX and 15 gallons of YY. XX sells for $10.00 per gallon and YY sells for

$30.00 per gallon. During the current period, the company used 400 drums of Zub to produce

XX and YY. The cost of Zub was $90 per drum.

Required:

(1) If the cost of Zub is allocated to the XX and YY products on the basis of the number of

gallons produced, how much of the total cost of the 400 drums should be charged to each

product?

(2) If the cost of Zub is allocated to the XX and YY products in proportion to their market

values, how much of the total cost of the 400 drums should be charged to each product?

(3) Which basis of allocating the cost is most likely to be used by the company?

162. Karl and Grady are managers of two product lines for Brewster Company. One of them

is a candidate for promotion based on performance. Using the data below, determine who had

the better performance using performance measures such as net income, profit margin, and

return on investment. Show your calculations and support your answer.

Karl Grady

Revenue……………….. $412,000 $450,000

Costs…………………… 380,000 411,000

Average Assets..……. 400,000 600,000

163. Use the Hamilton Company’s investment center information below to calculate (a) return

on total investment and (b) investment center residual income.

Net Income…………………… $315,900

Average Invested Assets…….. $2,100,000

Target Net Income…………… 6% of division assets

164. City Park College allocates administrative costs to its teaching departments based on the

number of students enrolled, while maintenance and utilities are allocated based on square

feet of classrooms. Based on the information below, what is the total amount of expenses

allocated to each department (rounded to the nearest dollar) if administrative costs for the

college were $180,000, maintenance expenses were $70,000, and utilities were $85,000?

Teaching Size of

Department

Students

Classroom

Electronics……………. 117 900 sq. ft.

Automotive…………… 156 750 sq. ft.

Computers……………. 429 1,200 sq. ft.

Plumbing…………….. 78 150 sq. ft.

165. Arkansas Toys, a retail store, has three sales departments supported by two service

departments. Cost and operational data for each department follow:

Purch.

Sales Cost of Square Orders

Department

Sales

Goods Sold Footage Issued

1…....

$92,160

$36,864

1,728

1,260

2..….. 69,120 32,832 3,024 1,680

3..….. 80,640 32,256 1,296 2,310

Service

Departments Allocation Basis Cost

Advertising……….. Sales $10,000

Purchasing………… No. of purchase orders issued 12,000

Determine the service department expenses to be allocated to Sales Department 1 for (round

answers to whole dollars):

Advertising ___________________

Purchasing ___________________

166. Chancellor Company is divided into four departments. Departments A and B are service

departments and Departments 1 and 2 are operating (production) departments. The services of

the two service departments are used by the other departments as follows:

Dept. A Dept. B Dept. 1 Dept. 2

Services of:

Department A..………. 50% 20% 30%

Department B…….….. 40% 60%

Direct costs incurred by each department $60,000 $50,000 $70,000 $80,000

Complete the following table:

Allocation of Expenses to Departments

Department A Department B Department 1 Department 2

Total direct

Department

expenses..

$60,000 $50,000 $ 70,000 $ 80,000

Service department expenses

Department A…………

Subtotal……………………

Department B…………

Total………………………..

167. Sturdivant Fasteners, Co. uses a traditional allocation of overhead based on direct labor

hours system. The manager has accumulated the following information on engineering

changes, which are indirect cost of their products, for two of the company’s major products:

Automotive

Fasteners

Computer

Fasteners

Total units produced……………………………… 5,000 2,500

Cost per engineering change………………….. $400 $ 400

Number of engineering changes……………… 5 25

Direct labor hours per unit……………………… 4 4

Compute the cost per unit using: The traditional two-stage allocation of the costs of

engineering changes based on direct labor hours.

168. Nesbit Co. has two operating (production) departments supported by a number of service

departments. The following information was collected for a recent period:

Direct Costs

Indirect

Cost

Machining

Department

Assembly

Department

Salaries………………………….. $122,400 $ 85,700 $36,700

Insurance…..…………………… 20,200 11,000 5,500

Utilities…..……………………… 23,900 13,900 2,000

Depreciation…………………… 20,700 11,500 13,800

Maintenance…………………… 7,000 4,700 29,400

Office expenses….…………… -0- -0- 71,100

Cost of goods sold…………… 327,600 121,200

Indirect costs are allocated as follows: salaries on the basis of sales, office expenses on the

basis of the number of employees, and all other costs on the basis of square footage.

Additional information about the production departments follows:

Square Number of

Footage

Employees

Machining……………….. 14,535 78

Assembly………………… 4,845 52

Sales for the Machining Department are $724,404 and sales for the Assembly Department are

$356,796. Determine the departmental contribution to overhead and the departmental net

income for each production department.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-104

169. Holliday, Inc., operates a retail store with two departments, A and B. Its departmental

income statement for the current year follows:

Holliday, Inc.

Departmental Income Statement

For Year Ended December 31

Dept. A Dept. B Combined

Sales….………………………………………………… $180,000 $200,000 $380,000

Direct expenses………………………………….….

129,900

142,870

272,770

Contributions to overhead……………………… $ 50,100 $ 57,130 $107,230

Indirect expenses:

Depreciation–Building …………………… 10,000 11,760 21,760

Maintenance…………………………………… 1,600 1,700 3,300

Utilities…..……………………………………… 6,200 6,320 12,520

Office expenses………………..…….……….

1,800

2,000

3,800

Total indirect expenses …..……………….. $ 19,600 $ 21,780 $ 41,380

Net income………………………………………..…. $ 30,500 $ 35,350 $ 65,850

Holliday allocates building depreciation, maintenance, and utilities on the basis of square

footage. Office expenses are allocated on the basis of sales.

Management is considering an expansion to a three-department operation. The proposed

Department C would generate $120,000 in additional sales and have a 17.5% contribution to

overhead. The company owns its building. Opening Department C would redistribute the

square footage to each department as follows: A, 19,040; B, 21,760 sq. ft.; C, 13,600.

Increases in indirect expenses would include: maintenance, $500; utilities, $3,800; and office

expenses, $1,200.

Complete the following departmental income statements, showing projected results of

operations for the three sales departments. (Round amounts to the nearest whole dollar.)

Dept. A Dept. B Dept. C Combined

Sales………………………………………………………………. $180,000 $200,000

Direct expenses………………………………………………. 129,900 142,870

Contributions to overhead……………………………….. $ 50,100 $ 57,130

Indirect expenses………………………………………………

Depreciation—building………………………………..

Maintenance……………………………………………….

Utilities……………………………………………………..

Office expenses…………………………………………..

Total indirect expenses………………………………..

Net income………………………………………………………

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-106

170. Williams Co. operates three separate departments (R, S, T). The data below is provided

for the current year:

Total Sales…………………… $120,000 ($40,000 from each department)

Cost of Goods Sold…………. $ 80,000 (50% from R; 25% from S; 25% from T)

Direct Expense……………… $ 26,000 ($6,000 from R; $12,000 from S; $8,000 from T)

Indirect Expenses……………… $ 9,000

Required:

Prepare an income statement showing the departmental contributions to overhead for the

current year.

171. The following data is available for the Janitorial Services Department of Glitterol Co.

Revenues………………………..…….…….………. $216,000

Cost of Sales ………………………………….……. 168,000

Expenses:

Supplies-Direct………………………… 12,000

Salaries-Indirect Allocated

……………………………………..............

34,000

Rent-Direct………………………………. 8,000

Rent-Indirect Allocated.…….......... 4,500

Required: Calculate departmental contribution to overhead for the Janitorial Services

Department, including the department’s contribution as a percentage of revenues.

172. The Linens Department of the Krafton Department Store had sales of $282,000, cost of

goods sold of $173,500, indirect expenses of $19,875, and direct expenses of $41,250 for the

current period. What is the Linens Department’s contribution to overhead as a percent of

sales?

173. Marsha Hansen, the manager of the Flint Plant of the Michigan Company is responsible

for all of the plant’s costs except her own salary. There are two operating departments within

the plant, Departments A and B. Each department has its own manager. There is also a

maintenance department that provides services equally to the two operating departments. The

following information is available.

A

Budget

B

Total A

Actual

B

Total

Employee wages

$3,500

$4,000

$7,500

$3,200

$4,700

$7,900

Department

Manager’s salary

800

800

1,600

800

800

1,600

Supplies

750

600

1,350

700

590

1,290

Building rent

1,500

1,500

3,000

1,400

1,400

2,800

Utilities

300

300

600

375

375

750

Maintenance 3,300 3,300 6,600 3,000 3,000 6,000

Totals $10,150 $10,500 $20,650 $9,475 $10,865 $20,340

Department managers are responsible for the wages and supplies in their department. They are

not responsible for their own salary. Building rent, utilities, and maintenance are allocated to

each department based on square footage.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

22-110

Required: Complete the responsibility accounting performance reports below that list costs

controllable by the manager of Department A, the manager of Department B, and the manager

of the Flint plant.

Budgeted

amount

Actual

amount

Over (under)

budget

Manager, Flint Plant

Controllable costs:

Manager, Department A