Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 21

FLEXIBLE BUDGETS AND STANDARD COSTS

True / False Questions

1. Standard costs can be used by management to assess the reasonableness of actual costs

incurred.

2. Standard material costs, standard labor costs, and standard overhead costs can be obtained

from standard cost tables published by the Institute of Management Accountants.

3. Standard costs are preset costs for delivering a product or service under normal conditions.

4. When standard costs are used, factory overhead is assigned to products with a

predetermined standard overhead rate.

5. Companies promoting continuous improvement strive to achieve practical standards rather

than ideal standards.

6. While companies strive to achieve ideal standards, reality implies that some loss of

materials usually occurs with any process.

7. A cost variance is the difference between actual cost and standard cost.

8. A budget performance report shows budgeted amounts, actual amounts, and differences

between budgeted and actual amounts.

9. A cost variance equals the difference between the quantity variance and the price variance.

10. When computing a price variance, the price is held constant.

11. Within the same flexible budget performance report, it is impossible to have both

favorable and unfavorable variances.

12. Cost variances are ignored under management by exception.

13. Management by exception means that managers focus on the most significant differences

between actual costs and standard costs..

14. Variable budget is another name for a flexible budget.

15. Fixed budget performance reports compare actual results with the results expected under a

fixed budget.

16. Another name for a static budget is a variable budget.

17. Fixed budgets are also known as flexible budgets.

18. A flexible budget is based on a single predicted amount of sales or other activity measure.

19. A variable or flexible budget is so named because it only focuses on variable costs.

20. A fixed budget performance report never provides useful information for evaluating

variances.

21. In sales variance analysis, the budgeted amount of unit sales is the predicted activity level

and the budgeted cost of the goods sold can be treated as a “standard” price.

22. The total sales variance can be divided into the sales price variance and the sales volume

variance.

23. A flexible budget expresses all costs on a per unit basis, regardless of cost behavior.

24. Although a fixed budget is only useful over the relevant range of operations, a flexible

budget is useful over all possible production levels.

25. A flexible budget expresses variable costs on a per unit basis and fixed costs on a total

basis.

26. The purchasing department is usually responsible for the price paid for materials.

27. A direct labor cost variance can be divided into price and quantity variances, which are

almost always called controllable and volume variances.

28. When the actual cost of direct materials used exceeds the standard cost, the company must

have experienced an unfavorable direct materials price variance.

29. A favorable direct materials price variance might lead to an unfavorable direct materials

quantity variance because the company purchased inferior materials.

30. One possible explanation for direct labor rate and efficiency variances is the use of

workers with different skill levels.

31. An overhead cost variance is the difference between the total overhead actually incurred

for the period and the standard overhead applied to products.

32. A volume variance is the difference between overhead at maximum volume of production

and the standard volume of production.

33. An unfavorable variance is recorded with a debit because it reflects additional costs higher

than the standard cost.

34. If ending variances account balances are material, they should always be closed directly to

Cost of Goods Sold.

35. Standard costs are:

A. Actual costs incurred to produce a specific product or perform a service.

B. Preset costs for delivering a product or service under normal conditions.

C. Established by the IMA.

D. Rarely achieved.

E. Uniform among companies within an industry.

36. The anticipated costs incurred under normal conditions to produce a specific product or to

perform a specific service are:

A. Variable costs.

B. Fixed costs.

C. Standard costs.

D. Product costs.

E. Period costs.

37. The difference between actual price per unit of input and the standard price per unit of

input results in a:

A. Standard variance.

B. Quantity variance.

C. Volume variance.

D. Controllable variance.

E. Price variance.

38. The difference between actual quantity of input used and the standard quantity of input

used results in a:

A. Controllable variance.

B. Standard variance.

C. Budget variance.

D. Quantity variance.

E. Price variance.

39. The difference between the actual cost incurred and the standard cost is called the:

A. Flexible variance.

B. Price variance.

C. Cost variance.

D. Controllable variance.

E. Volume variance.

40. Which of the following is not part of the flow of events in variance analysis:

A. Preparing a standard cost performance report.

B. Identifying questions and their explanations.

C. Taking corrective and strategic actions.

D. Computing and analyzing variances.

E. Working to ensure that all variances are favorable.

41. Standard costs are used in the calculation of:

A. Price and quantity variances.

B. Price variances only.

C. Quantity variances only.

D. Price, quantity, and sales variances.

E. Quantity and sales variances.

42. A company provided the following direct materials cost information. Compute the cost

variance.

Standard costs assigned:

Direct materials standard cost (405,000 units @ $2/unit) $810,000

Actual costs

Direct Materials costs incurred (403,750 units @ $2.20/unit) $888,250

A. $2,500 Favorable.

B. $78,250 Favorable

C. $78,250 Unfavorable

D. $80,750 Favorable.

E. $80,750 Unfavorable.

43. An analytical technique used by management to focus attention on the most significant

variances and give less attention to the areas where performance is reasonably close to

standard is known as:

A. Controllable management.

B. Management by variance.

C. Performance management.

D. Management by objectives.

E. Management by exception.

44. In this type of control system, the master budget is based on a single prediction for sales

volume, and the budgeted amount for each cost essentially assumes that a specific amount of

sales will occur:

A. Sales budget.

B. Standard budget.

C. Flexible budget.

D. Fixed budget.

E. Variable budget.

45. A budget based on several different levels of activity, often including both a best-case and

worst-case scenario, is called a:

A. Rolling budget.

B. Production budget.

C. Flexible budget.

D. Merchandise purchases budget.

E. Fixed budget.

46. Static budget is another name for:

A. Standard budget.

B. Flexible budget.

C. Variable budget.

D. Fixed budget.

E. Master budget.

47. Variable budget is another name for:

A. Cash budget.

B. Flexible budget.

C. Fixed budget.

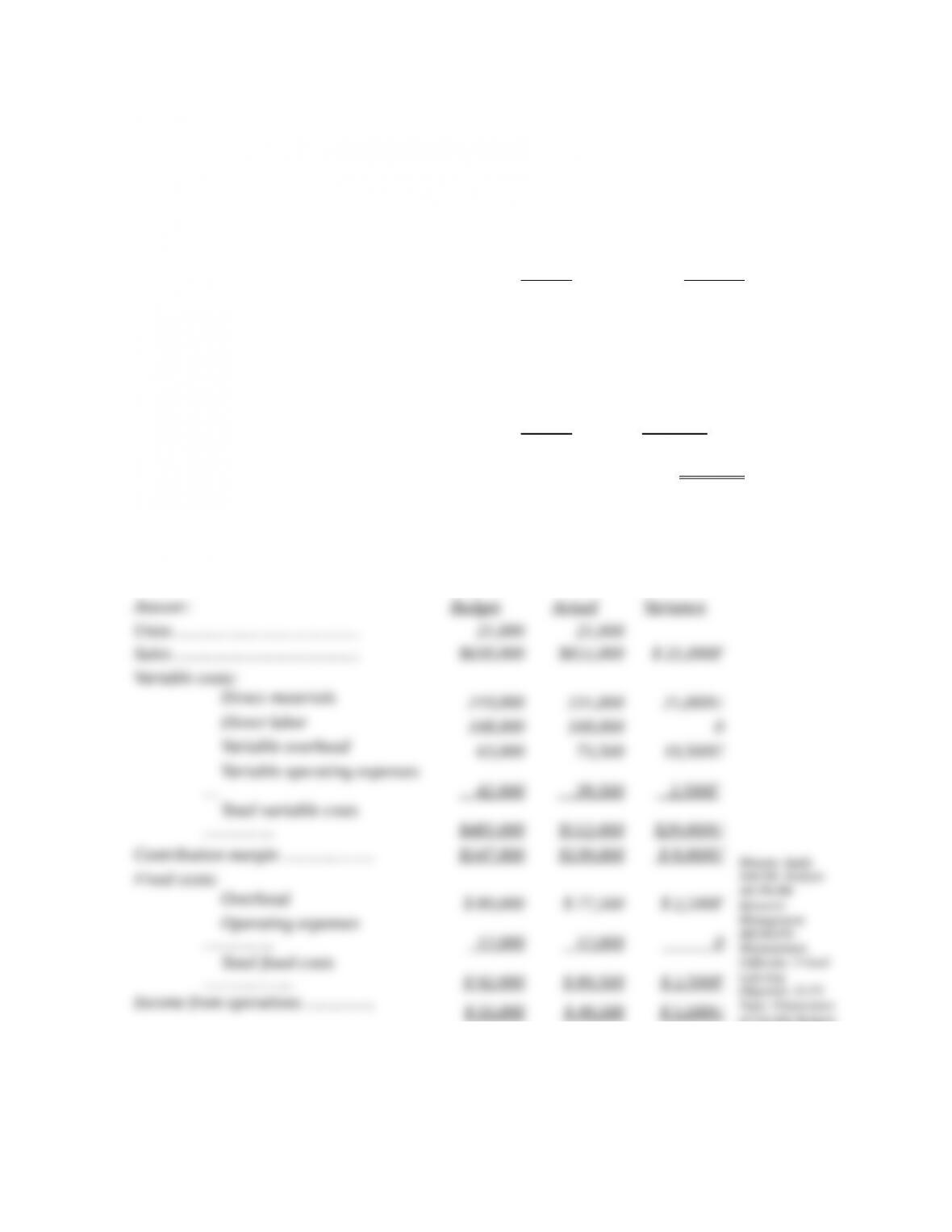

D. Manufacturing budget.

E. Rolling budget.

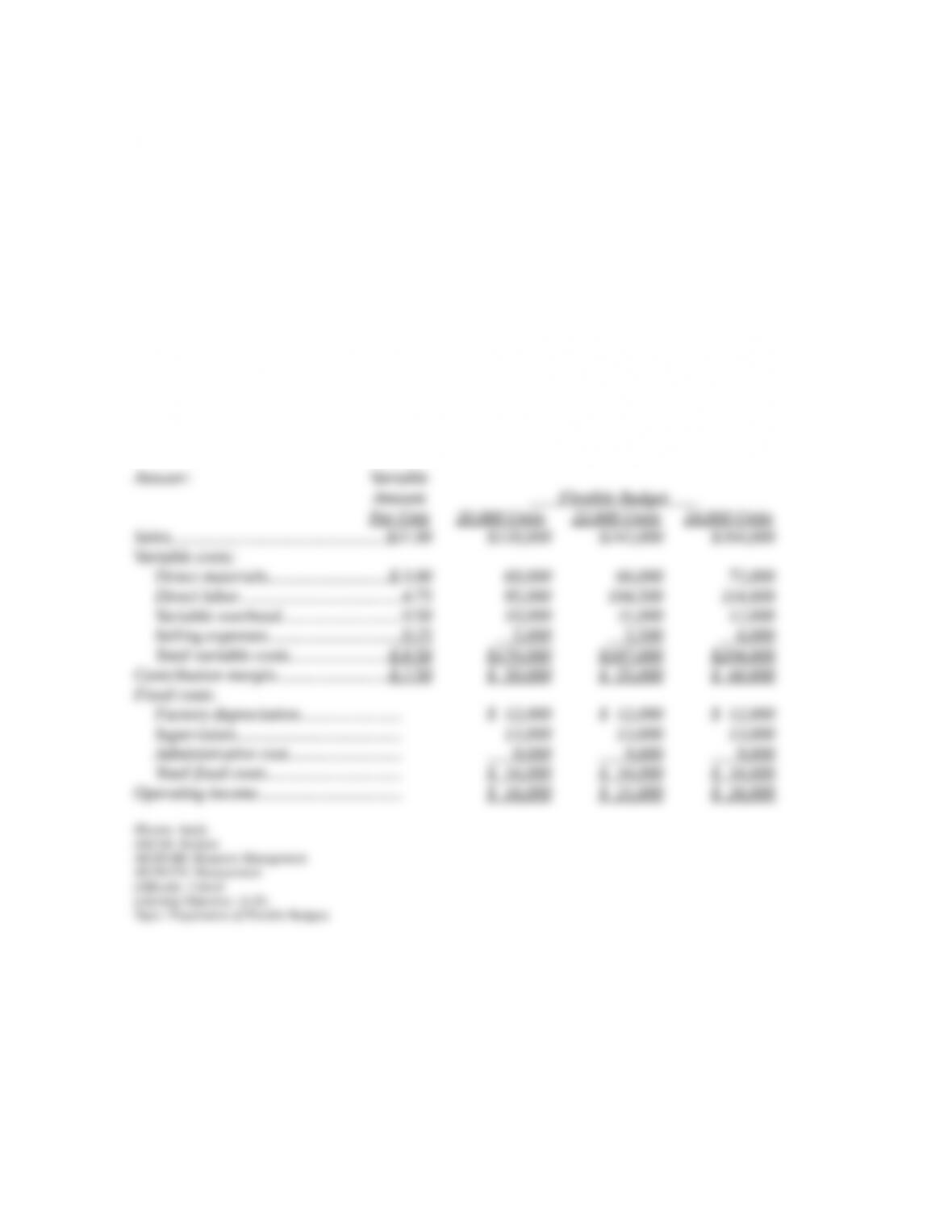

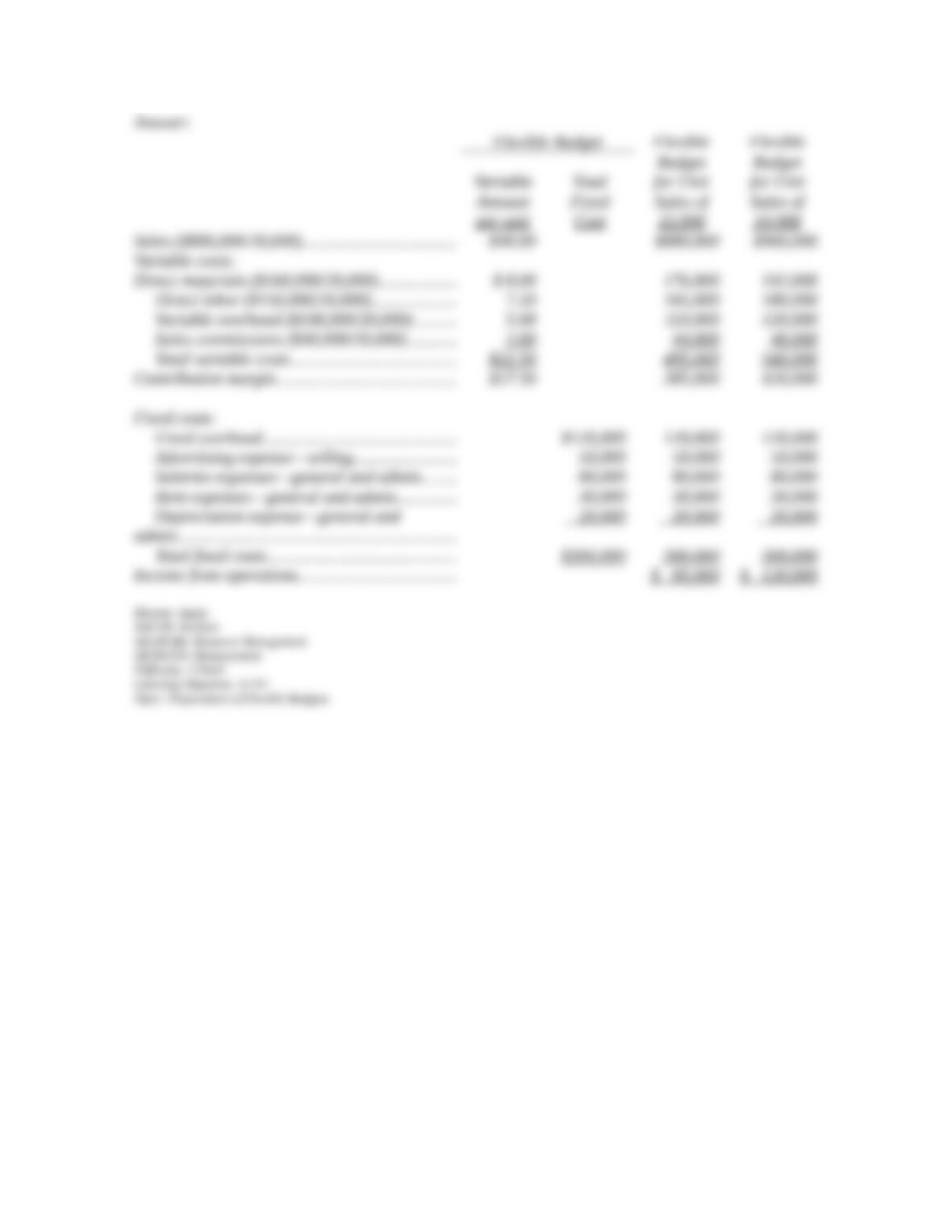

48. Identify the situation below that will result in a favorable variance.

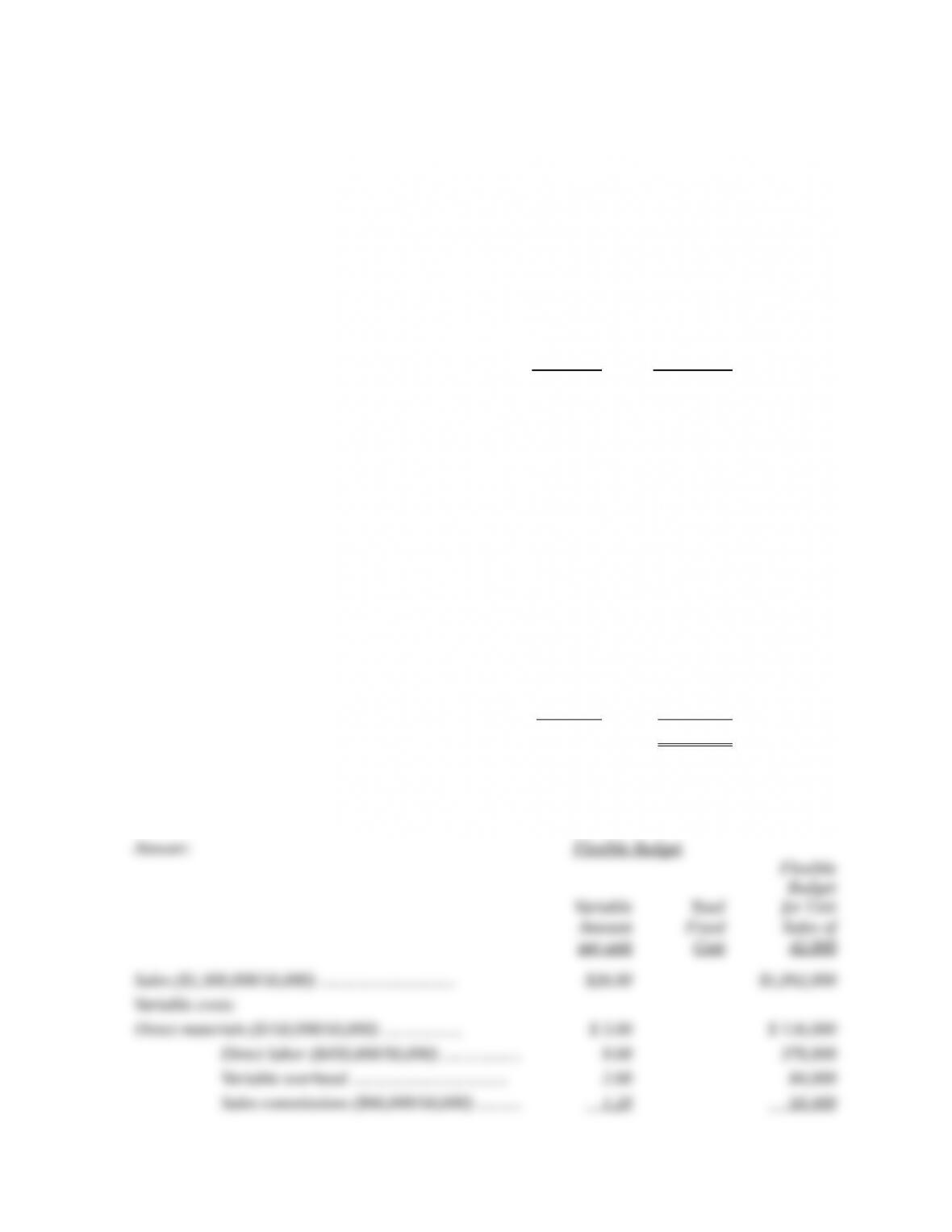

A. Actual revenue is higher than budgeted revenue.

B. Actual revenue is lower than budgeted revenue.

C. Actual income is lower than expected income.

D. Actual costs are higher than budgeted costs.

E. Actual expenses are higher than budgeted expenses.

49. A flexible budget performance report compares the differences between:

A. Actual performance and budgeted performance based on actual sales volume.

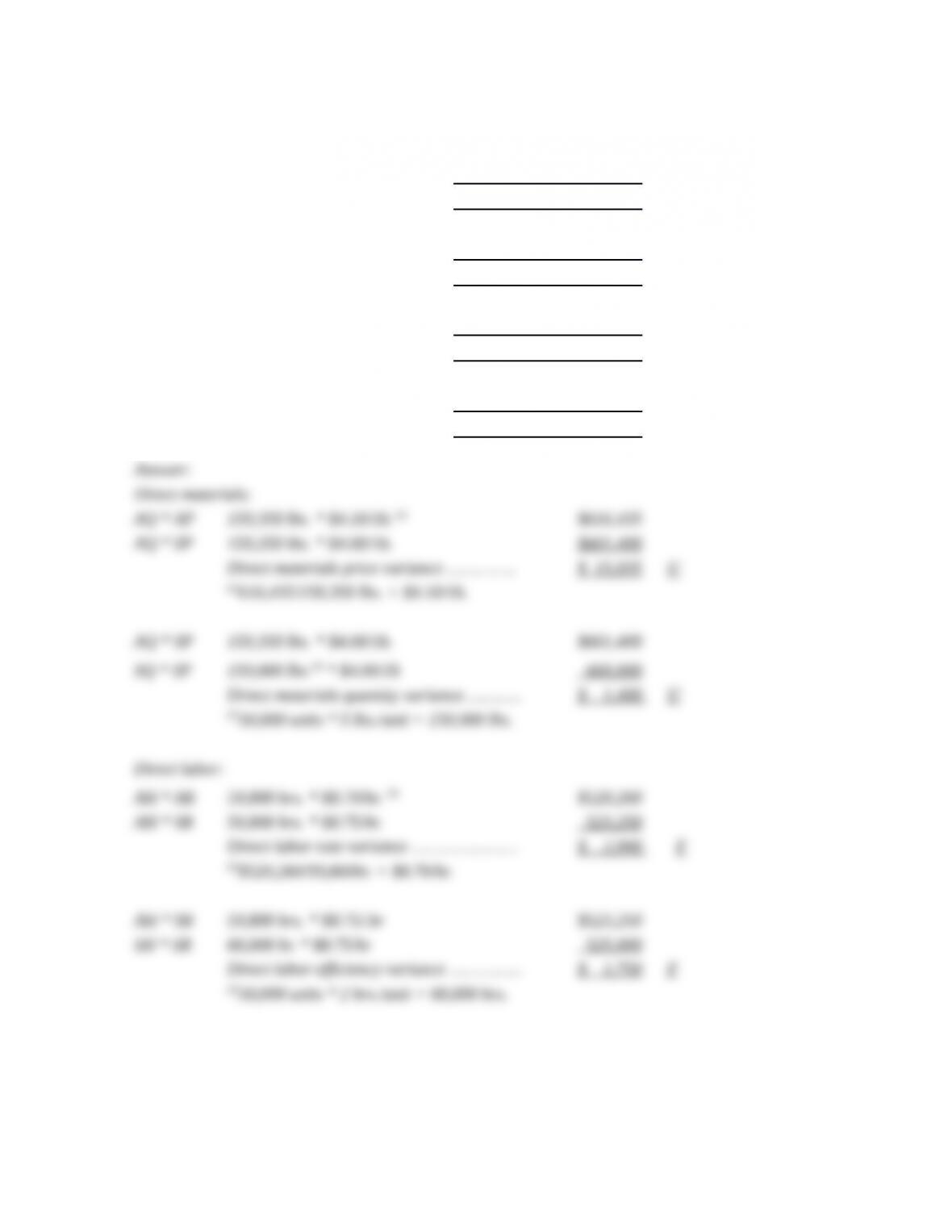

B. Actual performance over several periods.

C. Budgeted performance over several periods.

D. Actual performance and budgeted performance based on budgeted sales volume.

E. Actual performance and standard costs at the budgeted sales volume.

50. Sales variance analysis is used by managers for:

A. Planning purposes only.

B. Budgeting purposes only.

C. Control purposes only.

D. Planning and control purposes.

E. Planning and budgeting purposes.

51. An internal report that helps management analyze the difference between actual

performance and budgeted performance based on the actual sales volume (or other level of

activity) is called a(n):

A. Sales budget performance report.

B. Flexible budget performance report.

C. Master budget performance report.

D. Static budget performance report.

E. Operating budget performance report.

52. A flexible budget may be prepared:

A. Before the operating period only.

B. After the operating period only.

C. During the operating period only.

D. At any time in the planning period.

E. Only when the company encounters excessive costs.

53. A company’s flexible budget for 12,000 units of production showed sales, $48,000;

variable costs, $18,000; and fixed costs, $16,000. The operating income expected if the

company produces and sells 16,000 units is:

A. $ 2,667.

B. $14,000.

C. $18,667.

D. $24,000.

E. $35,000.

54. A company’s flexible budget for 12,000 units of production showed total contribution

margin of $24,000 and fixed costs, $16,000. The operating income expected if the company

produces and sells 15,000 units is:

A. $34,000.

B. $10,000.

C. $18,667.

D. $8,000.

E. $14,000.

55. A company’s flexible budget for 12,000 units of production showed per unit contribution

margin of $3.00 and fixed costs, $20,000. The operating income expected if the company

produces and sells 18,000 units is:

A. $34,000.

B. $10,000.

C. $18,667.

D. $16,000.

E. $24,000.

56. Based on predicted production of 12,000 units, a company anticipates $150,000 of fixed

costs and $123,000 of variable costs. The flexible budget amounts of fixed and variable costs

for 10,000 units are:

A. $125,000 fixed and $102,500 variable.

B. $125,000 fixed and $123,000 variable.

C. $102,500 fixed and $150,000 variable.

D. $150,000 fixed and $123,000 variable.

E. $150,000 fixed and $102,500 variable.

57. Product A has a sales price of $10 per unit. Based on a 10,000-unit production level, the

variable costs are $6 per unit and the fixed costs are $3 per unit. Using a flexible budget for

12,500 units, what is the budgeted operating income from Product A?

A. $12,500.

B. $25,000.

C. $20,000.

D. $30,000.

E. $35,000.

58. A company’s flexible budget for 10,000 units of production reflects sales of $200,000;

variable costs of $40,000; and fixed costs of $75,000. Calculate the expected level of

operating income if the company produces and sells 13,000 units.

A. $110,500.

B. $85,000.

C. $133,000.

D. $100,000.

E. $50,500.

59. Based on a predicted level of production and sales of 12,000 units, a company anticipates

reporting operating income of $26,000 after deducting variable costs of $72,000 and fixed

costs of $10,000. Based on this information, the budgeted amounts of fixed and variable costs

for 15,000 units would be:

A. $10,000 of fixed costs and $72,000 of variable costs.

B. $10,000 of fixed costs and $90,000 of variable costs.

C. $12,500 of fixed costs and $90,000 of variable costs.

D. $12,500 of fixed costs and $72,000 of variable costs.

E. $10,000 of fixed costs and $81,000 of variable costs.

60. Based on a predicted level of production and sales of 22,000 units, a company anticipates

total variable costs of $99,000, fixed costs of $30,000, and operating income of $36,000.

Based on this information, the budgeted amount of sales for 20,000 units would be:

A. $165,000.

B. $150,000.

C. $117,272.

D. $181,500.

E. $141,900.

61. Based on a predicted level of production and sales of 30,000 units, a company anticipates

total contribution margin of $105,000, fixed costs of $40,000, and operating income of

$52,000. Based on this information, the budgeted operating income for 28,000 units would

be:

A. $52,000.

B. $135,333.

C. $58,000.

D. $72,500.

E. $105,000.

62. Which department is often responsible for the direct materials price variance?

A. The accounting department.

B. The production department.

C. The purchasing department.

D. The finance department.

E. The budgeting department.

63. Georgia, Inc. has collected the following data on one of its products. The actual cost of the

direct materials used is:

Direct materials standard (4 lbs. @ $1/lb.) $4 per finished unit

Total direct materials cost variance—unfavorable $13,750

Actual direct materials used 150,000 lbs.

Actual finished units produced 30,000 units

A. $133,750.

B. $150,000.

C. $106,250.

D. $158,750.

E. $120,000.

64. Georgia, Inc. has collected the following data on one of its products. The direct materials

quantity variance is:

Direct materials standard (4 lbs. @ $1/lb.) $4 per finished unit

Total direct materials cost variance—unfavorable $13,750

Actual direct materials used 150,000 lbs.

Actual finished units produced 30,000 units

A. $30,000 favorable.

B. $13,750 unfavorable.

C. $16,250 favorable.

D. $30,000 unfavorable.

E. $13,750 favorable.

65. Georgia, Inc. has collected the following data on one of its products. The direct materials

price variance is:

Direct materials standard (4 lbs. @ $1/lb.) $4 per finished unit

Total direct materials cost variance—unfavorable $13,750

Actual direct materials used 150,000 lbs.

Actual finished units produced 30,000 units

A. $13,750 unfavorable.

B. $16,250 unfavorable.

C. $16,250 favorable.

D. $30,000 unfavorable.

E. $33,000 favorable.

66. Parallel Enterprises has collected the following data on one of its products. During the

period the company produced 25,000 units. The direct materials price variance is:

Direct materials standard (7 kg. @ $2/kg) $14 per finished unit

Actual cost of materials purchased $322,500

Actual direct materials purchased and used 150,000 lbs.

A. $27,500 unfavorable.

B. $50,000 unfavorable.

C. $50,000 favorable.

D. $22,500 unfavorable.

E. $22,500 favorable.

67. Parallel Enterprises has collected the following data on one of its products. During the

period the company produced 25,000 units. The direct materials quantity variance is:

Direct materials standard (7 kg. @ $2/kg) $14 per finished unit

Actual cost of materials purchased $322,500

Actual direct materials purchased and used 150,000 kg

A. $27,500 unfavorable.

B. $50,000 unfavorable.

C. $50,000 favorable.

D. $22,500 unfavorable.

E. $22,500 favorable.

68. Hassock Corp. produces woven wall hangings. It takes 2 hours of direct labor to produce a

single wall hanging. Bartels’ standard labor cost is $12 per hour. During August, Bartels

produced 10,000 units and used 21,040 hours of direct labor at a total cost of $250,376. What

is Bartels’ labor rate variance for August?

A. $2,000 favorable.

B. $2,104 unfavorable.

C. $2,104 favorable.

D. $4,160 favorable.

E. $2,000 unfavorable.

69. Hassock Corp. produces woven wall hangings. It takes 2 hours of direct labor to produce a

single wall hanging. Bartels’ standard labor cost is $12 per hour. During August, Bartels

produced 10,000 units and used 21,040 hours of direct labor at a total cost of $250,376. What

is Bartels’ labor efficiency variance for August?

A. $12,480 favorable.

B. $10,376 unfavorable.

C. $14,584 unfavorable.

D. $4,160 favorable.

E. $12,480 unfavorable.

70. Use the following data to find the total direct labor cost variance if the company produced

3,500 units during the period.

Direct labor standard (4 hrs. @ $7/hr.) $28 per unit

Actual hours worked 12,250

Actual rate per hour $7.50

A. $ 6,125 unfavorable.

B. $ 7,000 unfavorable.

C. $ 7,000 favorable.

D. $12,250 favorable.

E. $ 6,125 favorable.

71. Use the following data to find the direct labor rate variance if the company produced

3,500 units during the period.

Direct labor standard (4 hrs. @ $7/hr.) $28 per unit

Actual hours worked 12,250

Actual rate per hour $7.50

A. $ 6,125 unfavorable.

B. $ 7,000 unfavorable.

C. $ 7,000 favorable.

D. $12,250 favorable.

E. $ 6,125 favorable.

Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 21-P2

Topic: Computing Materials and Labor Variances

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21-33

72. Use the following data to find the direct labor efficiency variance if the company

produced 3,500 units during the period.

Direct labor standard (4 hrs. @ $7/hr.) $28 per unit

Actual hours worked 12,250

Actual rate per hour $7.50

A. $ 6,125 unfavorable.

B. $ 7,000 unfavorable.

C. $ 7,000 favorable.

D. $12,250 favorable.

E. $ 6,125 favorable.

73. Use the following data to find the direct labor rate variance if the company produced

7,000 units of product during the period.

Standard:

Direct labor (3.2 hrs. per unit @ $7/hr.) $22.40 per unit

Actual cost incurred:

Direct labor (24,500 hrs. @ $7.50/hr.) $183,750

A. $12,250 unfavorable.

B. $14,700 unfavorable.

C. $14,700 favorable.

D. $12,250 favorable.

E. $26,950 favorable.

74. The following company information is available for March. The direct materials price

variance is:

Direct materials purchased and used

…………………………………… 2,500 feet @ $55 per foot

Standard costs for direct materials for March production 2,600 feet @ $53 per foot

A. $5,000 favorable.

B. $ 300 favorable.

C. $5,200 unfavorable.

D. $5,000 unfavorable.

E. $5,200 favorable.

75. The following company information is available. The direct materials quantity variance

is:

Direct materials used for production …………………. 36,000 gallons

Standard quantity for units produced ………………… 34,400 gallons

Standard cost per gallon of direct material …………... $6.00

Actual cost per gallon of direct material ……………... $6.10

A. $10,000 unfavorable.

B. $13,200 unfavorable.

C. $ 9,600 unfavorable.

D. $10,000 favorable.

E. $13,200 favorable.

Blooms: Apply

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 21-P2

Topic: Computing Materials and Labor Variances

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21-37

76. Summerlin Company budgeted 4,000 pounds of material costing $5.00 per pound to

produce 2,000 units. The company actually used 4,500 pounds that cost $5.10 per pound to

produce 2,000 units. What is the direct materials quantity variance?

A. $ 400 unfavorable.

B. $ 450 unfavorable.

C. $2,500 unfavorable.

D. $2,550 unfavorable.

E. $2,950 unfavorable.

77. Summerlin Company budgeted 4,000 pounds of material costing $5.00 per pound to

produce 2,000 units. The company actually used 4,500 pounds that cost $5.10 per pound to

produce 2,000 units. What is the direct materials price variance?

A. $ 400 unfavorable.

B. $ 450 unfavorable.

C. $2,500 unfavorable.

D. $2,550 unfavorable.

E. $2,950 unfavorable.

78. A company has established 5 pounds of Material J at $2 per pound as the standard for the

material in its Product Z. The company has just produced 1,000 units of this product, using

5,200 pounds of Material J that cost $9,880. The direct materials quantity variance is:

A. $400 unfavorable.

B. $120 favorable.

C. $400 favorable.

D. $520 favorable.

E. $520 unfavorable.

79. A company has established 5 pounds of Material J at $2 per pound as the standard for the

material in its Product Z. The company has just produced 1,000 units of this product, using

5,200 pounds of Material J that cost $9,880.The direct materials price variance is:

A. $520 unfavorable.

B. $400 unfavorable.

C. $120 favorable.

D. $520 favorable.

E. $400 favorable.

80. A job was budgeted to require 3 hours of labor per unit at $8.00 per hour. The job

consisted of 8,000 units and was completed in 22,000 hours at a total labor cost of $198,000.

What is the total labor cost variance?

A. $2,000 unfavorable.

B. $3,000 unfavorable.

C. $6,000 unfavorable.

D. $8,000 unfavorable.

E. $9,000 unfavorable.

81. The standard materials cost to produce 1 unit of Product R is 6 pounds of material at a

standard price of $50 per pound. In manufacturing 8,000 units, 47,000 pounds of material

were used at a cost of $51 per pound. What is the total direct materials cost variance?

A. $48,000 unfavorable.

B. $51,000 favorable.

C. $51,000 unfavorable.

D. $ 3,000 favorable.

E. $ 3,000 unfavorable.

82. The following information describes a company’s usage of direct labor in a recent period.

The direct labor efficiency variance is:

Actual hours used ………………………………. 45,000

Actual rate per hour …………………………….. $15.00

Standard rate per hour ………………………….. $14.50

Standard hours for units produced …................... 47,000

A. $29,000 unfavorable.

B. $29,000 favorable.

C. $22,500 unfavorable.

D. $52,500 favorable.

E. $52,500 unfavorable.

Blooms: Apply

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 21-P2

Topic: Computing Materials and Labor Variances

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21-42

83. The following information describes a company’s usage of direct labor in a recent period.

The direct labor rate variance is:

Actual hours used ……………………. 45,000

Actual rate per hour ………………….. $15.00

Standard rate per hour ……………….. $14.50

Standard hours for units produced …... 47,000

A. $29,000 favorable.

B. $29,000 unfavorable.

C. $22,500 unfavorable.

D. $52,500 favorable.

E. $52,500 unfavorable.

84. A company uses the following standard costs to produce a single unit of output.

Direct materials 6 pounds at $0.90 per pound = $5.40

Direct labor 0.5 hour at $12.00 per hour = $6.00

Manufacturing overhead 0.5 hour at $4.80 per hour =$2.40

During the latest month, the company purchased and used 58,000 pounds of direct materials

at a price of $1.00 per pound to produce 10,000 units of output. Direct labor costs for the

month totaled $56,350 based on 4,900 direct labor hours worked. Variable manufacturing

overhead costs incurred totaled $15,000 and fixed manufacturing overhead incurred was

$10,400. Based on this information, the direct materials price variance for the month was:

A. $6,000 unfavorable

B. $1,800 favorable

C. $1,000 favorable

D. $5,800 unfavorable

E. $1,800 unfavorable

85. A company uses the following standard costs to produce a single unit of output.

Direct materials 6 pounds at $0.90 per pound = $5.40

Direct labor 0.5 hour at $12.00 per hour = $6.00

Manufacturing overhead 0.5 hour at $4.80 per hour =$2.40

During the latest month, the company purchased and used 58,000 pounds of direct materials

at a price of $1.00 per pound to produce 10,000 units of output. Direct labor costs for the

month totaled $56,350 based on 4,900 direct labor hours worked. Variable manufacturing

overhead costs incurred totaled $15,000 and fixed manufacturing overhead incurred was

$10,400. Based on this information, the direct materials quantity variance for the month was:

A. $1,800 favorable

B. $5,800 unfavorable

C. $5,800 favorable

D. $1,800 unfavorable

E. $1,000 favorable

86. A company uses the following standard costs to produce a single unit of output.

Direct materials 6 pounds at $0.90 per pound = $5.40

Direct labor 0.5 hour at $12.00 per hour = $6.00

Manufacturing overhead 0.5 hour at $4.80 per hour =$2.40

During the latest month, the company purchased and used 58,000 pounds of direct materials

at a price of $1.00 per pound to produce 10,000 units of output. Direct labor costs for the

month totaled $56,350 based on 4,900 direct labor hours worked. Variable manufacturing

overhead costs incurred totaled $15,000 and fixed manufacturing overhead incurred was

$10,400. Based on this information, the direct labor rate variance for the month was:

A. $1,200 favorable

B. $3,650 favorable

C. $2,450 favorable

D. $3,650 unfavorable

E. $1,200 unfavorable

87. A company uses the following standard costs to produce a single unit of output.

Direct materials 6 pounds at $0.90 per pound = $5.40

Direct labor 0.5 hour at $12.00 per hour = $6.00

Manufacturing overhead 0.5 hour at $4.80 per hour =$2.40

During the latest month, the company purchased and used 58,000 pounds of direct materials

at a price of $1.00 per pound to produce 10,000 units of output. Direct labor costs for the

month totaled $56,350 based on 4,900 direct labor hours worked. Variable manufacturing

overhead costs incurred totaled $15,000 and fixed manufacturing overhead incurred was

$10,400. Based on this information, the direct labor efficiency variance for the month was:

A. $3,650 favorable

B. $2,450 favorable

C. $1,200 unfavorable

D. $1,200 favorable

E. $2,450 unfavorable

88. Overhead cost variance is:

A. The difference between the overhead costs actually incurred and the overhead budgeted at

the actual operating level.

B. The difference between the actual overhead incurred during a period and the standard

overhead applied.

C. The difference between actual and budgeted cost caused by the difference between the

actual price per unit and the budgeted price per unit.

D. The costs that should be incurred under normal conditions to produce a specific product (or

component) or to perform a specific service.

E. The difference between the total overhead cost that would have been expected if the actual

operating volume had been accurately predicted and the amount of overhead cost that was

allocated to products using the standard overhead rate.

89. The difference between actual overhead costs incurred and the budgeted overhead costs

based on a flexible budget is the:

A. Production variance.

B. Quantity variance.

C. Volume variance.

D. Price variance.

E. Controllable variance.

90. When there is a difference between the actual volume of production and the standard

volume of production, which of the following, based solely on fixed overhead, occurs:

A. Production variance.

B. Volume variance.

C. Overhead cost variance.

D. Quantity variance.

E. Controllable variance.

91. A company’s flexible budget for 48,000 units of production showed variable overhead

costs of $72,000 and fixed overhead costs of $64,000. The company incurred overhead costs

of $122,800 while operating at a volume of 40,000 units. The total controllable cost variance

is:

A. $ 1,200 favorable.

B. $ 1,200 unfavorable.

C. $13,200 favorable.

D. $13,200 unfavorable.

E. $15,200 favorable.

92. A company’s flexible budget for the range of 35,000 units to 45,000 units of production

showed variable overhead costs of $2 per unit and fixed overhead costs of $72,000. The

company incurred total overhead costs of $148,800 while operating at a volume of 40,000

units. The total controllable cost variance is:

A. $ 6,800 favorable.

B. 6,800 unfavorable.

C. $3,200 favorable.

D. $3,200 unfavorable.

E. $10,000 favorable.

93. Jefferson Co. uses the following standard to produce a single unit of its product: variable

overhead $6 (2 hrs. per unit @ $3/hr.). Actual data for the month show variable overhead

costs of $150,000, and 24,000 units produced. The total variable overhead variance is:

A. $6,000F.

B. $6,000U.

C. $78,000U.

D. $78,000F.

E. $0.

94. Grant Co. uses the following standard to produce a single unit of its product: Variable

overhead (2 hrs. per unit @ $4/hr.) Actual data for the month show total variable overhead

costs of $190,000, and 23,000 units produced. The total variable overhead variance is:

A. $6,000F.

B. $6,000U.

C. $78,000U.

D. $78,000F.

E. $0.

95. Claymore Corp. has the following information about its standards and production activity

for September. The volume variance is:

Actual total factory overhead incurred……………………. $28,175

Standard factory overhead:

Variable overhead ……………………………………... $3.10 per unit produced

Fixed overhead

($12,000/6,000 estimated units to be produced) $2 per unit

Actual units produced ………………………………….…. 4,800 units

A. $1,295U.

B. $1,295F.

C. $2,400U.

D. $2,400F.

E. $3,695U.

96. Claymore Corp. has the following information about its standards and production activity

for September. The controllable variance is:

Actual total factory overhead incurred …………………… $28,175

Standard factory overhead:

Variable overhead ………………………………………. $3.10 per unit produced

Fixed overhead

($12,000/6,000 estimated units to be produced) $2 per unit

Actual units produced ……………………………….……. 4,800 units

A. $1,295U.

B. $1,295F.

C. $2,400U.

D. $2,400F.

E. $3,695U.

97. Regarding overhead costs, as volume increases:

A. Unit fixed cost increases, unit variable cost decreases.

B. Unit fixed cost decreases, unit variable cost increases.

C. Unit variable cost decreases, unit fixed cost remains constant.

D. Unit fixed cost decreases, unit variable cost remains constant.

E. Both unit fixed cost and unit variable cost remain constant.

98. Regarding overhead costs, as volume increases:

A. Total fixed cost increases, total variable cost remains constant.

B. Total fixed cost remains constant, total variable cost increases.

C. Total variable cost decreases, total fixed cost remains constant.

D. Both total fixed cost and total variable cost increase.

E. Both total fixed cost and total variable cost remain constant.

99. Levelor Company’s flexible budget shows $10,710 of overhead at 75% of capacity, which

was the operating level achieved during May. However, the company applied overhead to

production during May at a rate of $2.00 per direct labor hour based on a budgeted operating

level of 6,120 direct labor hours (90% of capacity). If overhead actually incurred was $11,183

during May, the controllable variance for the month was:

A. $ 473 unfavorable.

B. $ 473 favorable.

C. $1,530 favorable.

D. $1,530 unfavorable.

E. $1,057 favorable.

100. Regent, Inc. uses the following standard to produce a single unit of its product: overhead

$6 (2 hrs. @ $3/hr.). The flexible budget for overhead is $100,000 plus $1 per direct labor

hour. Actual data for the month show overhead costs of $150,000, and 24,000 units produced.

The overhead volume variance is:

A. $10,000 favorable.

B. $12,000 favorable.

C. $ 4,000 unfavorable.

D. $16,000 unfavorable.

E. $36,000 unfavorable.

101. The variable overhead spending variance, the fixed overhead spending variance, and the

variable overhead efficiency variance can be combined to find the:

A. Production variance.

B. Quantity variance.

C. Volume variance.

D. Price variance.

E. Controllable variance.

102. The following information relating to a company’s overhead costs is available.

Budgeted fixed overhead rate per machine hour $0.50

Actual variable overhead $73,000

Budgeted variable overhead rate per machine hour $2.50

Actual fixed overhead $17,000

Budgeted hours allowed for actual output achieved 32,000

Based on this information, the total overhead variance is:

A. $7,000 favorable.

B. $6,000 favorable.

C. $1,000 unfavorable.

D. $6,000 unfavorable.

E. $1,000 favorable.

103. The following information relating to a company’s overhead costs is available.

Actual total variable overhead $73,000

Actual total fixed overhead $17,000

Budgeted variable overhead rate per machine hour $ 2.50

Budgeted total fixed overhead $15,000

Budgeted machine hours allowed for actual output 30,000

Based on this information, the total variable overhead variance is:

A. $2,000 favorable.

B. $6,000 favorable.

C. $2,000 unfavorable.

D. $6,000 unfavorable.

E. $1,000 favorable.

104. When recording variances in a standard cost system:

A. Only unfavorable material variances are debited.

B. Only unfavorable material variances are credited.

C. Both unfavorable material and labor variances are credited.

D. All unfavorable variances are debited.

E. All unfavorable variances are credited.

105. When standard manufacturing costs are recorded in the accounts and the cost variances

are immaterial at the end of the accounting period, the cost variances should be:

A. Carried forward to the next accounting period.

B. Allocated between cost of goods sold, finished goods, and work in process.

C. Closed to cost of goods sold.

D. Written off as a selling expense.

E. Ignored.

106. Seafarer Company established a standard direct materials cost of 1.5 gallons at $2 per

gallon for one unit of its product. During the past month, actual production was 6,500 units.

The material quantity variance was $700 favorable and the material price variance was $470

unfavorable. The entry to charge Work in Process Inventory for the standard material costs

during the month and to record the direct material variances in the accounts would include all

of the following except:

A. A debit to Work in Process for $19,500.

B. A credit to Raw Materials for $19,270.

C. A debit to Direct Material Price Variance for $470.

D. A credit to Direct Material Quantity Variance for $700.

E. A debit to Cost of Goods Sold for $230.

107. When recording the journal entry for labor, the Work in Process Inventory account is

A. Debited for standard labor cost.

B. Debited for actual labor cost.

C. Credited for standard labor cost.

D. Credited for actual labor cost.

E. Not used.

108. Cavern Company’s output for the current period results in a $5,250 unfavorable direct

material price variance. The actual price per pound is $56.50 and the standard price per pound

is $55.00. How many pounds of material are used in the current period?

A. 5,393.

B. 5,110.

C. 3,500.

D. 3,750.

E. 4,000.

109. Sanchez Company’s output for the current period was assigned a $200,000 standard

direct materials cost. The direct materials variances included a $5,000 favorable price

variance and a $3,000 unfavorable quantity variance. What is the actual total direct materials

cost for the current period?

A. $208,000.

B. $198,000.

C. $202,000.

D. $192,000.

E. $205,000.

110. Sanchez Company’s output for the current period was assigned a $400,000 standard

direct labor cost. The direct labor variances included a $10,000 unfavorable direct labor rate

variance and a $4,000 favorable direct labor efficiency variance. What is the actual total direct

labor cost for the current period?

A. $414,000.

B. $386,000.

C. $394,000.

D. $406,000.

E. $410,000.

111. Milltown Company specializes in selling used cars. During the month, the dealership

sold 22 cars at an average price of $15,000 each. The budget for the month was to sell 20 cars

at an average price of $16,000. Compute the dealership’s sales price variance for the month.

A. $22,000 unfavorable.

B. $10,000 favorable.

C. $22,000 favorable.

D. $32,000 unfavorable.

E. $32,000 favorable.

112. Milltown Company specializes in selling used cars. During the month, the dealership

sold 22 cars at an average price of $15,000 each. The budget for the month was to sell 20 cars

at an average price of $16,000. Compute the dealership’s sales volume variance for the month.

A. $22,000 unfavorable.

B. $10,000 favorable.

C. $22,000 favorable.

D. $32,000 unfavorable.

E. $32,000 favorable.

113. Claremont Company specializes in selling refurbished copiers. During the month, the

company sold 180 copiers for total sales of $540,000. The budget for the month was to sell

175 copiers at an average price of $3,200. The sales price variance for the month was.

A. $20,000 unfavorable.

B. $20,000 favorable.

C. $36,000 unfavorable.

D. $32,000 unfavorable.

E. $36,000 favorable.

114. Claremont Company specializes in selling refurbished copiers. During the month, the

company sold 180 copiers at an average price of $3,000 each. The budget for the month was

to sell 175 copiers at an average price of $3,200. The expected total sales for 180 copiers

were.

A. $540,000.

B. $576,000.

C. $525,000.

D. $560,000.

E. $550,000.

115. Fletcher Company collected the following data regarding production of one of its

products. Compute the total direct materials variance.

Direct materials standard (6 lbs. @ $2/lb.) $12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21-65

A. $6,000 favorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

116. Fletcher Company collected the following data regarding production of one of its

products. Compute the direct materials price variance.

Direct materials standard (6 lbs. @ $2/lb.) $12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

A. $2,430 unfavorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

117. Fletcher Company collected the following data regarding production of one of its

products. Compute the direct materials quantity variance.

Direct materials standard (6 lbs. @ $2/lb.) $12 per finished unit

Actual direct materials used 243,000 lbs.

Actual finished units produced 40,000 units

Actual cost of direct materials used $483,570

A. $2,430 unfavorable.

B. $3,570 unfavorable.

C. $2,430 favorable.

D. $6,000 unfavorable.

E. $3,570 favorable.

118. Fletcher Company collected the following data regarding production of one of its

products. Compute the total direct labor variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished

unit

Actual direct labor hours 81,500 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,100,250

A. $80,250 unfavorable.

B. $80,250 favorable.

C. $61,125 favorable.

D. $61,125 unfavorable.

E. $19,125 favorable.

119. Fletcher Company collected the following data regarding production of one of its

products. Compute the direct labor rate variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished

unit

Actual direct labor hours 81,500 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,100,250

A. $80,250 unfavorable.

B. $80,250 favorable.

C. $61,125 favorable.

D. $61,125 unfavorable.

E. $19,125 unfavorable.

120. Fletcher Company collected the following data regarding production of one of its

products. Compute the direct labor efficiency variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished

unit

Actual direct labor hours 81,500 hrs.

Actual finished units produced 40,000 units

Actual cost of direct labor $1,100,250

A. $19,125 favorable.

B. $80,250 favorable.

C. $61,125 favorable.

D. $19,125 unfavorable.

E. $80,250 unfavorable.

121. Fletcher Company collected the following data regarding production of one of its

products. Compute the variable overhead cost variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished unit

Actual direct labor hours 81,500 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $18,000 favorable.

B. $4,000 favorable.

C. $18,000 unfavorable.

D. $18,300 favorable.

E. $14,300 unfavorable.

122. Fletcher Company collected the following data regarding production of one of its

products. Compute the fixed overhead cost variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished unit

Actual direct labor hours 81,500 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $18,300 favorable.

B. $18,000 favorable.

C. $18,000 unfavorable.

D. $18,300 unfavorable.

E. $14,300 unfavorable.

123. Fletcher Company collected the following data regarding production of one of its

products. Compute the variable overhead spending variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished unit

Actual direct labor hours 81,500 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $25,450 favorable.

B. $4,000 favorable.

C. $4,000 unfavorable.

D. $21,450 unfavorable.

E. $21,450 unfavorable.

124. Fletcher Company collected the following data regarding production of one of its

products. Compute the variable overhead efficiency variance.

Direct labor standard (2 hrs. @ $12.75/hr.) $25.50 per finished unit

Actual direct labor hours 81,500 hrs.

Budgeted units 42,000 units

Actual finished units produced 40,000 units

Standard variable OH rate (2 hrs. @ $14.30/hr.) $28.60 per finished unit

Standard fixed OH rate ($336,000/42,000 units) $8.00 per unit

Actual cost of variable overhead costs incurred $1,140,000

Actual cost of fixed overhead costs incurred $ 338,000

A. $14,300 unfavorable.

B. $21,450 favorable.

C. $4,000 unfavorable.

D. $4,000 unfavorable.

E. $21,450 unfavorable.

125. Janitor Supply produces an industrial cleaning powder that requires 40 grams of material

at $0.10 per gram and .25 direct labor hours at $12.00 per hour. Overhead is assigned at the

rate of $18 per direct labor hour. What is the total standard cost for one unit of product that

would appear on a standard cost card?

A. $7.00.

B. $8.50.

C. $11.50.

D. $7.50.

E. $25.00.

126. ShipCo produces storage crates that require 1.2 meters of material at $.85 per meter and

0.1 direct labor hours at $15.00 per hour. Overhead is assigned at the rate of $9 per direct

labor hour. What is the total standard cost for one unit of product that would appear on a

standard cost card?

A. $25.02.

B. $11.52.

C. $2.40.

D. $2.52.

E. $3.42.

127. Presented below are terms preceded by letters a through j and followed by a list of

definitions 1 through 10. Enter the letter of the term with the definition, using the space

preceding the definition.

(a) Cost variance

(b) Volume variance

(c) Price variance

(d) Quantity variance

(e) Standard costs

(f) Controllable variance

(g) Fixed budget

(h) Flexible budget

(i) Variance analysis

(j) Management by exception

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

21-78

__________ (1) Occurs when there is a difference between the actual and standard volume

of production.

__________ (2) A planning budget based on a single predicted amount of sales or other

activity measure.

__________ (3) Preset costs for delivering a product, or service under normal conditions.

__________ (4) A process of examining differences between actual and budgeted sales or

costs and describing them in terms of the price and quantity differences.

__________ (5) The difference between actual price per unit of input and standard price per

unit of input.

__________ (6) A budget prepared based on several different amounts of sales, often

including a best-case and worst-case scenario.

__________ (7) The difference between actual quantity of input used and standard quantity

of input used.

__________ (8) The difference between actual overhead costs incurred and the budgeted

overhead costs based on a flexible budget.

__________ (9) A management process to focus on significant variances and give less

attention to areas where performance is close to the standard.

__________ (10) The difference between actual and standard cost.

1. B; 2. G; 3. E; 4. I; 5. C; 6. H; 7. D; 8. F; 9. J; 10. A

Blooms: Understand

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 21-C1

Learning Objective: 21-C2

Learning Objective: 21-P1

Learning Objective: 21-P2

Learning Objective: 21- P3

Topic: Standard Costs

Topic: Cost Variances

Topic: Preparation of Flexible Budgets

Topic: Computing Materials and Labor Variances

Topic: Computing Overhead Cost Variances

128. Presented below are terms preceded by letters a through h and followed by a list of

definitions 1 through 8. Enter the letter of the term with the definition, using the space

preceding the definition.

(a) Unfavorable variance

(b) Fixed budget performance report

(c) Overhead cost variance

(d) Budgetary control

(e) Spending variance

(f) Flexible budget performance report

(g) Quantity variance

(h) Favorable variance

__________(1) Results from a comparison of actual cost or revenue to budget that contributes

to a lower income..

__________(2) A report that compares actual results with the results expected under a fixed

budget.

__________(3) The difference between the actual price of an item and its standard price.

__________(4) Results from a comparison of actual cost or revenue to budget that contributes

to higher income.

__________(5) Management’s use of budgets to see that planned objectives are met.

__________(6) Difference between actual quantity of an input and the standard quantity of

the input.

__________(7) Difference between the total overhead cost applied to products and the total

overhead cost actually incurred.

__________(8) A report that compares actual performance and budgeted performance based

on actual sales volume or other activity level.

1. A; 2. B; 3. E; 4. H; 5. D; 6. G; 7. C; 8. F

Blooms: Understand

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 21-C1

Learning Objective: 21-C2

Learning Objective: 21-P1

Learning Objective: 21-P2

Learning Objective: 21-P3

Topic: Standard Costs

Topic: Cost Variances

Topic: Preparation of Flexible Budgets

Topic: Computing Materials and Labor Variances

Topic: Computing Overhead Cost Variances

Short Answer Questions

129. Define standard costs. How do they assist management?

130. Explain variance analysis. Describe how variance analysis assists managers.

131. What are the four steps in the effective management of variance analysis?

132. Should both favorable and unfavorable variances be investigated, or only the unfavorable

ones? Explain.

133. Briefly describe the procedure of management by exception.

134. Identify and explain the primary differences between fixed and flexible budgets.

135. Identify the four steps in the budgetary control process.

136. Flexible budgets may be prepared before or after an actual period of activity. Why would

management prepare such budgets at differing time frames?

137. What are sales variances? How are they used?

138. Wren Company determined that in the production of their products last period; they had

a favorable price variance and an unfavorable quantity variance for direct materials. What

might be the cause(s) of this pattern of variances?

139. What are some causes of direct labor rate and efficiency variances?

140. What is the overhead volume variance? What would be the cause of a favorable volume

variance?

141. How are unfavorable variances recorded? How are favorable variances recorded?

142. Joseph, Inc., provides the following results of June’s operations:

Direct materials price variance ………….. $ 400F

Direct materials quantity variance ………. 2,000U

Direct labor rate variance ……………….. 100U

Direct labor efficiency variance ……….... 1,200F

Variable overhead spending variance …… 400U

Variable overhead efficiency variance ….. 800F

Fixed overhead spending variance ………. 100U

Fixed overhead volume variance ………... 600F

Required:

(a) Determine the total overhead cost variance for June.

(b) Applying the management by exception approach, which of the variances shown are of

greatest concern? Why?

143. Oxford Co. produces and sells two lines of t-shirts, Classic and Mod. Oxford provides

the following data. Compute the sales price and the sales volume variances for each product.

Budget Actual

Unit sales price — Classic …. $15 $16

Unit sales price—Mod ……. $20 $19

Unit sales—Classic ………… 2,400 2,500

Unit sales—Mod ………….. 2,000 1,900

144. A company’s flexible budget for 60,000 units of production showed sales of $96,000,

variable costs of $36,000, and fixed costs of $26,000. What operating income would be

expected if the company produces and sells 70,000 units?

145. A company’s flexible budget for 30,000 units of production showed sales of $90,000,

variable costs of $36,000, and fixed costs of $23,000. Prepare a flexible budget for 25,000

units assuming it is within the same relevant range of production.

146. Based on predicted production of 25,000 units, FreshCo. anticipates $175,000 of fixed

costs and $137,500 of variable costs. What are the flexible budget amounts of total costs for

20,000 and 30,000 units?

147. Based on predicted production of 25,000 units, Marvel Mix Co. anticipates $175,000 of

variable costs and $137,500 of fixed costs. What are the flexible budget amounts of total costs

for 28,000 units?

148. Anniston Co. planned to produce and sell 40,000 units. At that volume level, variable

costs are determined to be $320,000 and fixed costs are $30,000. The planned selling price is

$10 per unit. Anniston actually produced and sold 42,000 units.

Using a contribution margin format:

(a) Prepare a fixed budget income statement for the planned level of sales and production.

(b) Prepare a flexible budget income statement for the actual level of sales and production.

149. Clevenger Co. planned to produce and sell 30,000 units with a selling price of $10 per

unit. Variable costs are expected to be $4 per unit and fixed costs are expected to be $80,000.

Clevenger actually produced and sold 37,000 units.

Using a contribution margin format:

Prepare a fixed budget income statement for the planned level of sales and production.

150. Clevenger Co. planned to produce and sell 30,000 units with a selling price of $10 per

unit. Variable costs are expected to be $4 per unit and fixed costs are expected to be $80,000.

Clevenger actually produced and sold 37,000 units.

Using a contribution margin format:

Prepare a flexible budget income statement for the actual level of sales and production.

151. A product has a sales price of $20. Based on a 15,000-unit production level, the variable

costs are $12 per unit and the fixed costs are $6 per unit. Using a flexible budget for an actual

production and sales level of 18,000 units, what is the budgeted operating income?

152. Engineworks Co. provides the following fixed budget data for the year:

Sales (20,000 units)

……………………………. $600,000

Cost of sales:

Direct materials

…………………………….. $200,000

Direct labor

………………………………… 160,000

Variable overhead

………………………….. 60,000

Fixed overhead

…………………………….. 80,000 500,000

Gross profit

……………………………………. $100,000

Operating expenses:

Fixed

……………………………………….. $12,000

Variable

……………………………………. 40,000 52,000

Income from operations

……………………….. $ 48,000

The company’s actual activity for the year

follows:

Sales (21,000 units)

……………………………. $651,000

Cost of goods sold:

Direct materials

…………………………….. $231,000

Direct labor

………………………………… 168,000

Variable overhead

………………………….. 73,500

Fixed overhead

…………………………….. 77,500 550,000

Gross profit

……………………………………. $101,000

Operating expenses:

Fixed

………………………………………. 12,000

Variable

……………………………………. 39,500 51,500

Income from operations

………………………. $ 49,500

Required:

Prepare a flexible budget performance report for the year using the contribution margin

format.

of Flexible Budgets

153. Zip-up Company provides the following data developed for its master budget:

Sales price ……………………… $11.00 per unit

Costs:

Direct materials ………………. $3.00 per unit

Direct labor …………………… $4.75 per unit

Variable overhead ……………. $0.50 per unit

Factory depreciation …………. $12,000 per month

Supervision …………………… $13,000 per month

Selling expense ……………….. $0.25 per unit

Administrative cost …………… $9,000 per month

Required:

Prepare flexible budgets for sales of 20,000, 22,000 and 24,000 units. Use a contribution

margin format.

154. Jake Co. has prepared the following fixed budget for the year, assuming production and

sales of 30,000 units. This level of production represents 80% of capacity.

Jake Co.

Fixed Budget

For Year Ending December 31

Sales ……………………………………. $1,500,000

Cost of goods sold:

Direct materials ………………… $540,000

Direct labor …………………….. 300,000

Indirect materials (variable) ….... 15,000

Indirect labor (variable) ………... 21,000

Depreciation ……………………. 180,000

Salaries …………………………. 90,000

Utilities (80% fixed) ……………. 54,000

Maintenance (40% variable) …… 33,000 1,233,000

Gross profit ……………………………... $ 267,000

Operating expenses:

Commissions …………………… $ 45,000

Advertising (fixed) ……………... 60,000

Wages (variable) ……………….. 15,000

Rent …………………………….. 30,000

Total operating expenses ………. 150,000

Income from operations ………………... $ 117,000

Calculate the following flexible budget amounts at the indicated levels of capacity:

Operations at

60% of Capacity

Operations at

75% of Capacity

Sales

Total variable costs

Total fixed costs

Income from operations

155. Whidbey Co. fixed budget for the year is shown below:

Sales (50,000 units) …………………………. $1,300,000

Cost of goods sold:

Direct materials

………………………… $150,000

Direct labor

……………………………... 450,000

Overhead (includes $2 per unit

variable

overhead)

………………………………….. 240,000 840,000

Gross profit

……………………………... $ 460,000

Selling expenses:

Sales commissions (all variable)

……….. 60,000

Rent (all fixed)

…………………………. 40,000

Insurance (all fixed)

……………………. 35,000

General and administrative expenses:

Salaries (all fixed)

……………………… 72,000

Rent (all fixed)

…………………………. 54,000

Depreciation (all fixed)

…………………. 31,000 292,000

Net income from operations ………………… $ 168,000

Prepare a flexible budget for Whidbey Co. that shows a detailed budget for its actual sales

volume of 42,000 units. Use the contribution margin format.

156. Lavoie Company planned to use 18,500 pounds of material costing $2.50 per pound to

make 4,000 units of its product. In actually making 4,000 units, the company used 18,800

pounds that cost $2.54 per pound. Calculate the direct materials price variance.

157. Lavoie Company planned to use 18,500 pounds of material costing $2.50 per pound to

make 4,000 units of its product. In actually making 4,000 units, the company used 18,800

pounds that cost $2.54 per pound. Calculate the direct materials quantity variance.

158. Job #411 was budgeted to require 3.5 hours of labor at $11.00 per hour. However, it was

completed in 3 hours by a person who worked for $14.00 per hour. What is the total labor cost

variance for Job #4115?

159. LJ Co. produces picture frames. It takes 3 hours of direct labor to produce a frame. LJ’s

standard labor cost is $11.00 per hour. During March, LJ produced 4,000 frames and used

12,400 hours at a total cost of $133,920. What is LJ’s labor rate variance for March?

160. In producing 700 units of product last period, Azure Company used 5,000 pounds of

Material K, costing $34,250. The company has established the standard of using 7.2 pounds

of Material K per unit of product, at a price of $7.50 per pound. Calculate the materials price

and quantity variances associated with producing the 700 units, and indicate whether they are

favorable or unfavorable:

161. Use the following cost information to calculate the direct labor rate and efficiency

variances and indicate whether they are favorable or unfavorable.

Actual costs and quantities:

Direct labor cost incurred

………….. $360,000

Direct labor hours used

…………….. 20,000 hours

Units produced ………………..…… 45,000 units

Standard costs and quantities:

Direct labor rate per hour

………….. $16.50

Hours to produce one unit

…………. 0.5 hours

162. The following information describes production activities of the Midtown Corp.:

Raw materials used …………………… 16,000 lbs. at $4.05 per lb.

Factory payroll ………………………...

5,545 hours for a total of

$72,085

30,000 units were completed during the year

Budgeted standards for each unit produced:

1/2 lb. of raw material at $4.15 per lb.

10 minutes of direct labor at $12.50 per hour

Compute the direct materials price and quantity and the direct labor rate and efficiency

variances. Indicate whether each variance is favorable or unfavorable.

163. Ransom, Inc. budgets direct materials cost at $1.10/liter and each product requires 4

liters per unit of finished product. April’s activities show usage of 832 liters to complete 196

units at a cost of $798.72. Compute the direct materials price and quantity variances. Indicate

if the variance is favorable or unfavorable.

164. Lionaire, Inc. has developed the following standard cost data based on 60,000 direct

labor hours, which is 75% of capacity.

Per Unit

Direct materials (6 lbs. @ $2.00/lb.) $12.00

Direct labor (1 hrs. @ $8.00/hr.) 8.00

During the last period, the company operated at 80% of capacity and produced 128,000 units.

Actual costs were:

Direct materials (760,000 lbs.) $1,558,000

Direct labor (126,000 hrs.) 1,014,300

Determine the direct materials price and quantity variances and the direct labor rate and

efficiency variances. Indicate whether each variance is favorable or unfavorable.

Direct materials:

Price variance

Quantity variance

Direct labor:

Rate variance

Efficiency variance

165. Maxwell Co. collected the following information about its production activities for the

current year.

a. Compute the direct materials price and quantity variances and indicate whether each is

favorable or unfavorable.

b. Prepare the journal entry to record the issuance of direct materials into production.

Actual costs and quantities:

Direct materials used 95,000 lbs. @ $6.30 per lb.

Units completed during the year, 50,000 units

Standard costs and quantities:

Price per lb. of direct material, $6.05

Two lbs. of direct material per unit

166. Linx Company’s output for a period was assigned the standard direct labor cost of

$17,160. If the company had a favorable direct labor rate variance of $1,000 and an

unfavorable direct labor efficiency variance of $275, what was the total actual cost of direct

labor incurred during the period?

167. Tiger, Inc. budgeted the following overhead costs for the current year assuming

operations at 80% of capacity, or 40,000 units:

Total variable overhead ……………. $240,000

Total fixed overhead ……………….

560,00

0

Total overhead ……………………. $800,000

The standard cost per unit when operating at this same 80% capacity level is:

Direct materials (5 lbs. @ $4/1b.) ………… $20.00

Direct labor (2 hrs. @ $8.75 hr.) …………. 17.50

Variable overhead (2 hrs. @ $3/hr.) ………… 6.00

Fixed overhead (2 hrs. @ $7/hr.) …………. 14.00

Total cost per unit …………………………. $57.50

The actual production achieved in the current year was 60% of capacity, or 30,000 units. The actual

costs were:

Direct materials (150,350 lbs.) …………. $616,435

Direct labor (59,800 hrs.) ………………. 520,260

Variable overhead ………….…………… 192,000

Fixed overhead ………….………….…... 552,000

Calculate the following variances and indicate whether each is favorable or unfavorable.

Direct materials:

Price variance

Quantity variance

Direct labor:

Rate variance

Efficiency variance

Variable overhead:

Spending variance

Efficiency variance

Fixed overhead:

Spending variance

Volume variance

168. Beluga Corp. has developed standard costs based on a predicted operating level of

352,000 units of production, which is 80% of capacity. Variable overhead is $281,600 at this

level of activity, or $0.80 per unit. Fixed overhead is $440,000. The standard costs per unit

are:

Direct materials (0.5 lbs. @ $1/1b.) …… $0.50 per unit

Direct labor (1 hour @ $6/hour) ………. $6.00 per unit

Overhead (1 hour @ $2.05/hour) ……… $2.05 per unit

Beluga actually produced 330,000 units at 75% of capacity and actual costs for the period

were:

Direct materials (162,000 lbs.) ………. $ 170,100

Direct labor (329,500 hours) …………. $2,042,900

Fixed overhead ………………………… $ 438,000

Variable overhead …………………….

$

262,000

Calculate the following variances and indicate whether each variance is favorable or

unfavorable:

(1) Direct labor efficiency variance: $__________________

(2) Direct materials price variance: $__________________

(3) Controllable overhead variance: $__________________

169. The following information comes from the records of Barney Co. for the current period.

a. Compute the direct materials price and quantity variances, direct labor rate and efficiency

variances and state whether the variance is favorable or unfavorable.

b. Prepare the journal entries to charge direct materials and direct labor costs to work in

process and the materials and labor variances to their proper accounts.

Actual costs and quantities:

Direct materials used ………………… 37,000 feet @ $6.20 per foot

Direct labor hours used ……………… 50,660 hours

Direct labor rate per hour ……………. $16.50

25,000 units were produced during the period.

Standard costs and quantities per unit:

Direct materials ……………………… 1.5 ft. @ $6.10 per ft.

Direct labor …………………………... 2 hours @ $17 per hour

170. The following information comes from the flexible budget performance report of Jackal

Corp. for the current period. Prepare the journal entries to charge direct materials and direct

labor costs to work in process and the materials and labor variances to their proper accounts.

Direct materials actual cost………………………… $237,400

Direct materials standard cost …………………… $238,750

Materials price variance…………………………. $11,700 U

Materials quantity variance………………………… $13,050 F

171. The following information comes from the records of Magno Co. for the current period.

a. Compute the overhead controllable and volume variances. In each case, state whether the

variance is favorable or unfavorable.

b. Prepare the journal entries to charge overhead costs to work in process and the overhead

variances to their proper accounts.

Actual costs and quantities:

Direct materials used ………………………... 38,000 feet @ $6.20 per foot

Direct labor hours used ……………………… 50,660 hours

Direct labor rate per hour ……………………. $16

Factory overhead ……………………………. $211,600

25,000 units were produced during the period.

Standard costs and quantities per unit:

Direct materials ………………………………. 1.5 ft. @ $6.10 per ft.

Direct labor …………………………………… 2 hours @ $17 per hour

Factory overhead (based on budgeted production of 24,500 units)

Variable overhead $2.25/direct labor hour

Fixed overhead $1.95/direct labor hour

172. If Mercury Company’s actual overhead incurred during a period was $32,700 and the

company reported a favorable overhead controllable variance of $1,200 and an unfavorable

overhead volume variance of $900, how much standard overhead cost was assigned to the

products produced during the period?

173. A company’s flexible budget for 36,000 units of production showed variable overhead

costs of $54,000 and fixed overhead costs of $50,000. The company actually incurred total

overhead costs of $95,300 while operating at a volume of 32,000 units. What is the

controllable variance?

174. During November, Gliem Company allocated overhead to products at the rate of $26.00

per direct labor hour. This figure was based on 80% of capacity or 1,600 direct labor hours.

However, Gliem Company operated at only 70% of capacity, or 1,400 direct labor hours.

Budgeted overhead at 70% of capacity is $38,900, and overhead actually incurred was

$38,000. What is the company’s volume variance for November? (Indicate whether the

variance is favorable or unfavorable)

175. Selected information from Richards Company’s flexible budget is presented below:

Operating Levels

80% 90% 100%

Budgeted production in units 4,800 5,400 6,000

Budgeted labor (standard hours) 9,600 10,800 12,000

Budgeted overhead:

Variable overhead $86,400 $97,200 $108,000

Fixed overhead 63,600 63,600 63,600

Richards Company applies overhead to production at a rate of $31.25 per unit based on a

normal operating level of 80% of capacity. For the current period, Richards Company

produced 5,400 units and incurred $62,000 of fixed overhead costs and $96,000 of variable

overhead costs. The company used 11,000 labor hours to produce the 5,400 units. Calculate

the variable overhead spending and efficiency variances, and the fixed overhead spending and

volume variances. Indicate whether each variance is favorable or unfavorable.

176. Hatter, Inc. allocates fixed overhead at a rate of $17 per direct labor hour. This amount is

based on 90% of capacity or 3,600 direct labor hours for 6,000 units. During July, Hatter

produced 5,500 units. Budgeted fixed overhead is $66,000, and overhead incurred was

$67,000.

Required: Determine the volume variance for July.

177. Gleason Company has developed the following standard cost data based on 60,000 direct

labor hours, which is 75% of capacity. Fixed overhead is $360,000 and variable overhead is

$180,000 at this level of activity.

Per Unit

Direct material (3 lbs. @ $2.00/1b.) ………… $ 6.00

Direct labor (0.5 hrs. @ $8.00/hr. ) …………. 4.00

Variable overhead (0.5 hrs. @ $3.00/hr.) …… 1.50

Fixed overhead (0.5 hrs. @ $6.00/hr.) ……… 3.00

Total standard cost ………...………...……… $14.50

During the current period, the company operated at 80% of capacity and produced 128,000

units. Actual costs were:

Direct material (380,000 lbs.) ……………. $779,000

Direct labor (63,000 hrs.) …………………. 507,150

Fixed overhead …………….……………… 365,000

Variable overhead ………………………… 220,000

Calculate the variable overhead spending and efficiency variance and the fixed overhead

spending and volume variances. Indicate whether each is favorable or unfavorable.

178. Naches Co. assigned direct labor cost to its products in May for 1,300 standard hours of

direct labor at the standard $8 per hour rate. The direct labor rate variance for the month was

$200 favorable and the direct labor efficiency variance was $150 favorable. Prepare the

journal entry to charge Work in Process Inventory for the standard labor cost of the goods

manufactured in May and to record the direct labor variances. Assuming that the direct labor

variances are immaterial, prepare the journal entry that Naches would make to close the

variance accounts.

179. Firenze Company’s fixed budget for the first quarter of the calendar year appears below.

Prepare flexible budgets that show variable costs per unit, fixed costs and two different

flexible budgets for sales volumes of 22,000 and 24,000.

Sales (20,000 units)........................................... $800,000

Cost of goods sold:

Direct materials............................................ $160,000

Direct labor.................................................. 150,000

Variable overhead......................................... 100,000

Fixed overhead............................................. 120,000 530,000

Gross profit.................................................. $ 270,000

Selling expenses:

Sales commissions(all variable)................... 40,000

Advertising (all fixed).................................. 50,000

General and administrative expenses:

Salaries (all fixed)........................................ 80,000

Rent (all fixed) ............................................ 30,000

Depreciation (all fixed)................................ 20,000 220,000

Net income from operations............................. $ 50,000

180. Gala Enterprises reports the following information regarding the production of one of its

products for the month. Compute the direct materials cost variance, the direct materials price

variance, the direct materials quantity variance and identify each as either favorable or

unfavorable.

Direct materials standard (6 lbs. @ $3/lb.) $18 per finished unit

Actual direct materials used 179,000 lbs.

Actual finished units produced 30,000 units

Actual cost of direct materials used $554,900

181. Gala Enterprises reports the following information regarding the production on one of its

products for the month. Compute the direct labor cost variance, the direct labor rate variance,

the direct labor efficiency variance and identify each as either favorable or unfavorable.

Direct labor standard (2 hrs. @ $15/hr.) $30 per finished unit

Actual direct labor hours 60,800 hrs.

Actual finished units produced 30,000 units

Actual cost of direct labor $905,920

182. Gala Enterprises collected the following data regarding production of one of its products.

Compute the variable overhead cost variance, the variable overhead spending variance, the

variable overhead efficiency variance, the fixed overhead cost variance, the fixed overhead

spending variance, and the fixed overhead volume variance.

Direct labor standard (2 hrs. @ $15/hr.) $30.00 per finished unit

Actual direct labor hours 60,800 hrs.

Budgeted units 31,000 units

Actual finished units produced 30,000 units

Standard variable OH rate (2 hrs. @ $14.00/hr.) $28.00 per finished unit

Standard fixed OH rate ($310,000/31,000 units) $10.00 per unit

Actual variable overhead costs incurred $857,600

Actual fixed overhead costs incurred $312,000

183. __________ are preset costs for delivering a product or service under normal conditions.

184. Companies promoting continuous improvement strive to achieve _____________

standards by eliminating inefficiencies and waste.

185. A standard that takes into account the reality that some loss usually occurs with any

process under normal application of the process is known as a _______________ standard.

186. Differences between actual costs and standard costs are known as _______________.

These differences may be subdivided into ______________ and _________________.

187. Direct materials variances are called price and quantity variances. However, when

referring to direct labor, these variances are usually called _________________ and

_____________ variances.

188. In the analysis of variances, management commonly focuses on four categories of

production costs: __________________ cost, ___________________ cost; _____________

cost; and _________________ cost.

189. A management approach that focuses attention on significant differences from plans and

gives less attention to areas where performance is reasonably close to standards is known as

___________________.

190. A fixed budget is also called a _____________ budget.

191. A favorable variance for a cost means that when compared to the budget, the actual cost

is ____________________ than the budgeted cost.

192. A flexible budget is also called a _______________ budget.

193. A _______________________ contains relevant information that compares actual results

to planned activities.

194. The difference between the actual sales and the flexible budget sales is called the

______________________ variance.

195. The difference between the flexible budget sales and the fixed budget sales is called the

__________________________ variance.

196. In preparing flexible budgets, the costs that remain constant in total are