Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 20

MASTER BUDGETS AND PERFORMANCE PLANNING

True / False Questions

1. Personnel who will have performance evaluated according to the budget standards should

not be consulted and involved in preparing the budget.

2. A budget can be an effective means of communicating management's plans to the

employees of a business.

3. Budgets are normally more effective when all levels of management are involved in the

budgeting process.

4. One of the major benefits of formal budgeting is the positive effect it can have on employee

attitudes if applied correctly.

5. Budgeting is an informal plan for future business activities.

6. A budget is a formal statement of future plans, usually expressed in monetary terms.

7. Budgets are long term financial plans that generally cover more than a one-year period.

8. The process of evaluating performance can be improved by using budgets.

9. Continuous budgeting is the practice of revising the entire set of budgets for the periods

remaining and adding new budgets to replace those for the periods that have elapsed.

10. Budget preparation is best determined in a top-down managerial approach.

11. The task of preparing a budget should be the sole task of the most important department in

an organization.

12. The responsibility for coordinating the preparation of a master budget should be assigned

to the Chief Executive Officer.

13. Larger, more complex organizations usually require a longer time to prepare their budgets

than smaller organizations because of the considerable effort to coordinate the different units

within the business.

14. A rolling budget is a specific budget application relevant only to a merchandising

company.

15. The sequence of the budgets within the master budget are dictated by GAAP.

16. The merchandise purchases budget depends on information provided by the sales budget.

17. The master budget is a small component of the comprehensive budget.

18. The merchandise purchases budget is the starting point for preparing the master budget.

19. The master budget includes individual budgets for sales, production or purchases, various

expenses, capital expenditures, and cash.

20. Part of the budgeting process is summarizing the financial statement effects on the

budgeted income statement and the budgeted balance sheet.

21. The budget process rarely coincides with the accounting period.

22. A master budget refers to a company's sales budget that includes all of its segments or

departments.

23. Activity-based budgeting is a budget system based on expected activities and their levels

for the budget period, which helps management plan for the resources required.

24. Traditional budgeting is generally better than activity-based budgeting when attempting to

reduce costs by eliminating non-value-added activities.

25. The sales budget is derived from the production budget.

26. A capital expenditures budget is prepared before the operating budgets.

27. The selling expenses budget is normally prepared before the sales budget because selling

expenses affect the amount of sales.

28. A manufacturing budget shows dollar amounts estimated to be spent to purchase

additional plant assets and amounts expected to be received from plant asset disposals.

29. If budgeted beginning inventory is $8,300, budgeted ending inventory is $9,400, and cost

of goods sold is expected to be $10,260, then budgeted purchases should be $11,360.

30. Part of the cash budget is based on information taken from the capital expenditures

budget.

31. A cash budget shows the expected cash receipts and cash expenditures during the budget

period.

32. The budgeted balance sheet is prepared primarily from data contained in the previously

prepared components of the master budget.

33. The budgeted balance sheet and income statement are normally completed after

preparation of operating and capital expenditure budgets.

34. The financial statement effects of the budgeting process are summarized on the cash

budget and the capital expenditures budget.

35. A company's history indicates that 20% of its sales are for cash and the remaining 80% are

on credit. Collections on credit sales are 30% in the month of the sale and 70% the following

month. Projected sales for January, February, and March are $75,000, $92,000 and $60,000,

respectively. The March expected cash receipts are $80,500.

36. Production budgets always show both budgeted units of product and total costs for the

budgeted units.

37. The manufacturing budgets include the sales budget and the budgeted income statement.

38. A formal statement of future plans, usually expressed in monetary terms, is a:

A. Variance report.

B. Position statement.

C. Budget.

D. Prospectus.

E. Variance analysis.

39. The process of planning future business actions and expressing them as a formal plan is

called:

A. Budgeting.

B. Cost accounting.

C. Managerial accounting.

D. Variance analysis.

E. Standard cost analysis.

40. All of the following are necessary for budgets to be effective except:

A. Goals should be attainable.

B. Employees affected by a budget should be consulted when it is prepared.

C. Evaluations should be made carefully with opportunities to explain differences between

actual and budgeted amounts.

D. Managers must be aware of potential negative outcomes of budgeting, such as budgetary

slack.

E. All budgeted amounts must be spent to ensure that budgets aren’t reduced for the next

period.

41. Which of the following is not a result of following a well-designed budgeting process?

A. Improved decision-making processes.

B. Improved performance evaluations.

C. Improved coordination of business activities.

D. Assurance of future profits.

E. Improved communication of management’s action plans .

42. Which of the following is a benefit derived from budgeting?

A. Budgeting focuses management's attention on past performance.

B. Budgeting avoids needing industry and economic factors in decision making.

C. Budgeting provides a basis for evaluating performance.

D. Budgeting avoids the need for incentives to improve employee performance.

E. Budgeting eliminates the need for coordination across departments .

43. Which of the following statements about budgeting is false?

A. Budgeting is an aid to planning and control.

B. Budgets create standards for performance evaluation.

C. Budgets help coordinate the activities of the entire organization.

D. Budgeting forces managers to think ahead and formalize future objectives.

E. The master budget should only be prepared by top management.

44. A budget is best described as:

A. A formal statement of a company's future plans usually expressed in monetary terms.

B. A master control device.

C. An informal statement of company’s future plans usually expressed in monetary terms.

D. The most crucial component of a company’s evaluation process.

E. The minimum acceptable performance level.

45. The central guidance of the budget process is the responsibility of the:

A. Chief Accounting Officer.

B. Chief Executive Officer (CEO).

C. Chief Financial Officer (CFO).

D. Budget Committee.

E. Board of Directors.

46. Budgets that are periodically revised and have new periods added to replace those that

have lapsed are called:

A. Production budgets.

B. Sales budgets.

C. Cash budgets.

D. Rolling budgets.

E. Capital expenditures budgets.

47. In a company that employs continuous budgeting on a quarterly basis and has an

accounting period that ends December 31 of each year, what period would the first revision

and update to the January through December 2015 budget cover?

A. February 2015–January 2016

B. March 2015–February 2016

C. December 2015–November 2016

D. April 2015–March 2016

E. January 2016–December 2016

48. The most useful budget figures are developed:

A. From the "top-down".

B. From the "bottom-up" following a participatory process.

C. By the budget committee.

D. By the CEO.

E. After the accounting period has begun.

49. The practice of preparing budgets for each of several future periods and revising those

budgets as each period is completed, adding a new budget each period so that the budgets

always cover the same number of future periods, is called:

A. Participatory budgeting.

B. Capital budgeting.

C. Balanced budgeting.

D. Continuous budgeting.

E. Primary budgeting.

50. The usual budget period for most companies is:

A. An annual period of 250 working days.

B. A monthly period separated into daily budgets.

C. A quarterly period separated into weekly budgets.

D. An annual period separated into weekly budgets.

E. An annual period separated into quarterly and monthly budgets.

51. Assuming a bottom-up process of budget development, which of the following should be

initially responsible for developing sales estimates?

A. The budget committee.

B. The accounting department.

C. The sales department.

D. Top management.

E. The marketing department.

52. The master budgeting process typically begins with the sales budget and ends with a cash

budget and:

A. Budgeted financial statements.

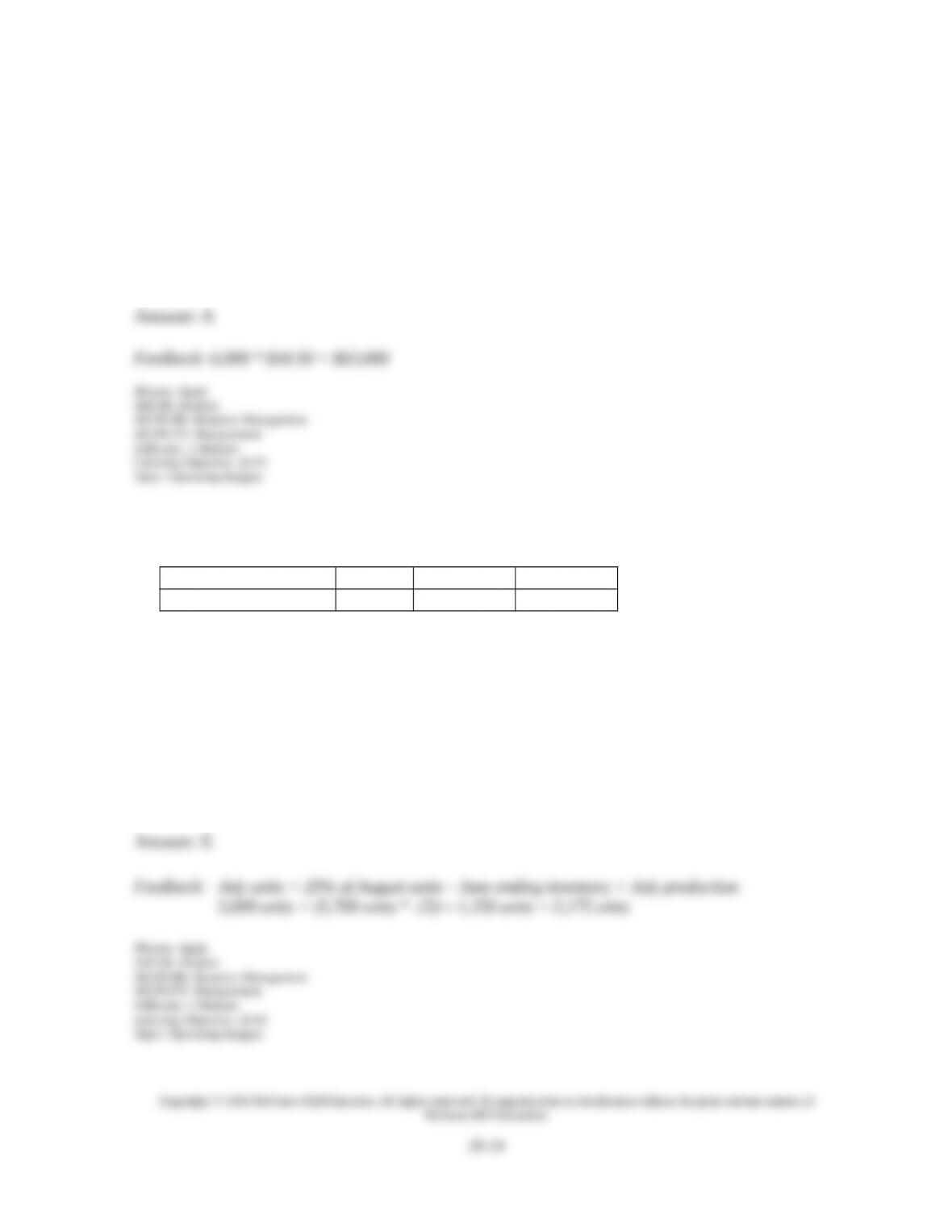

B. Forecast budget.

C. Capital expenditures budget.

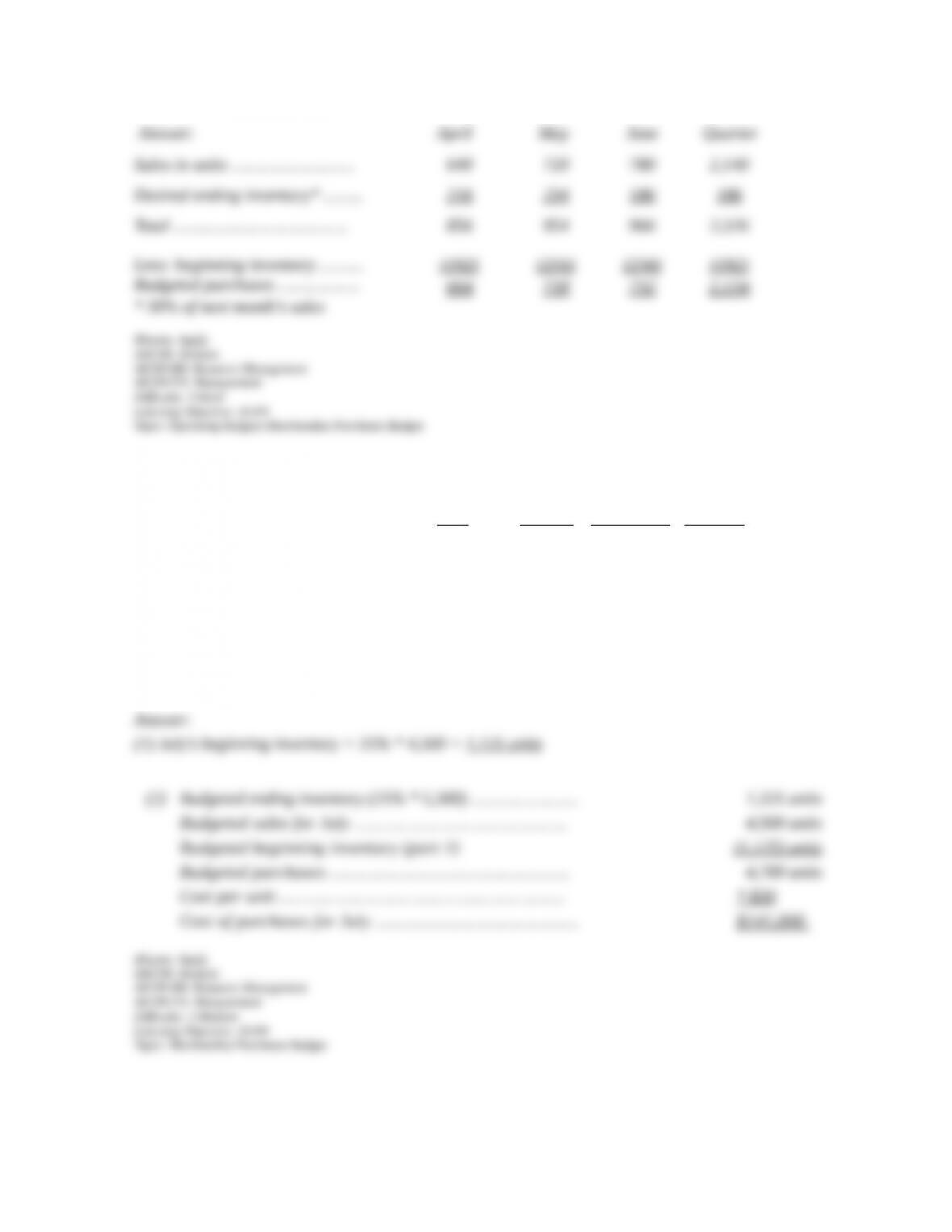

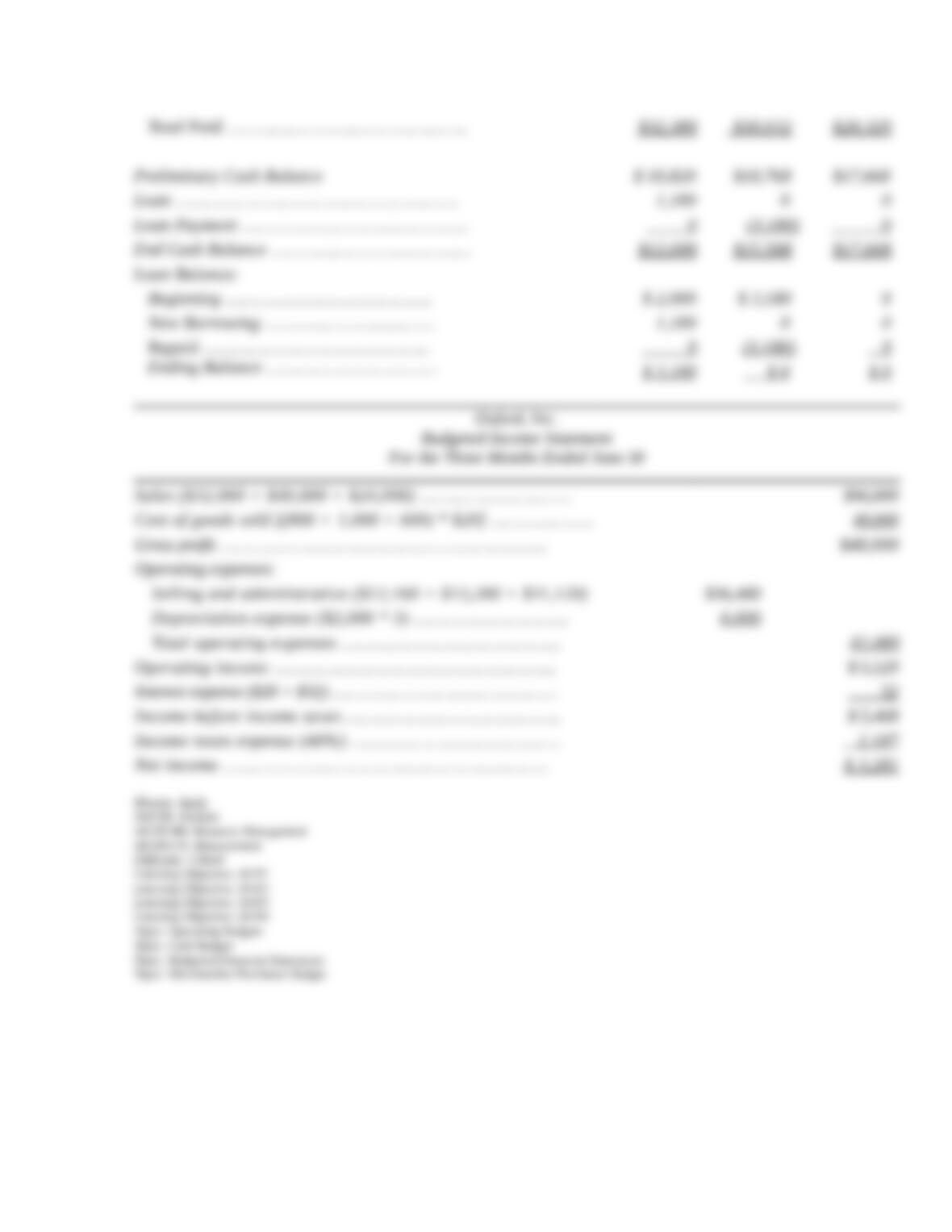

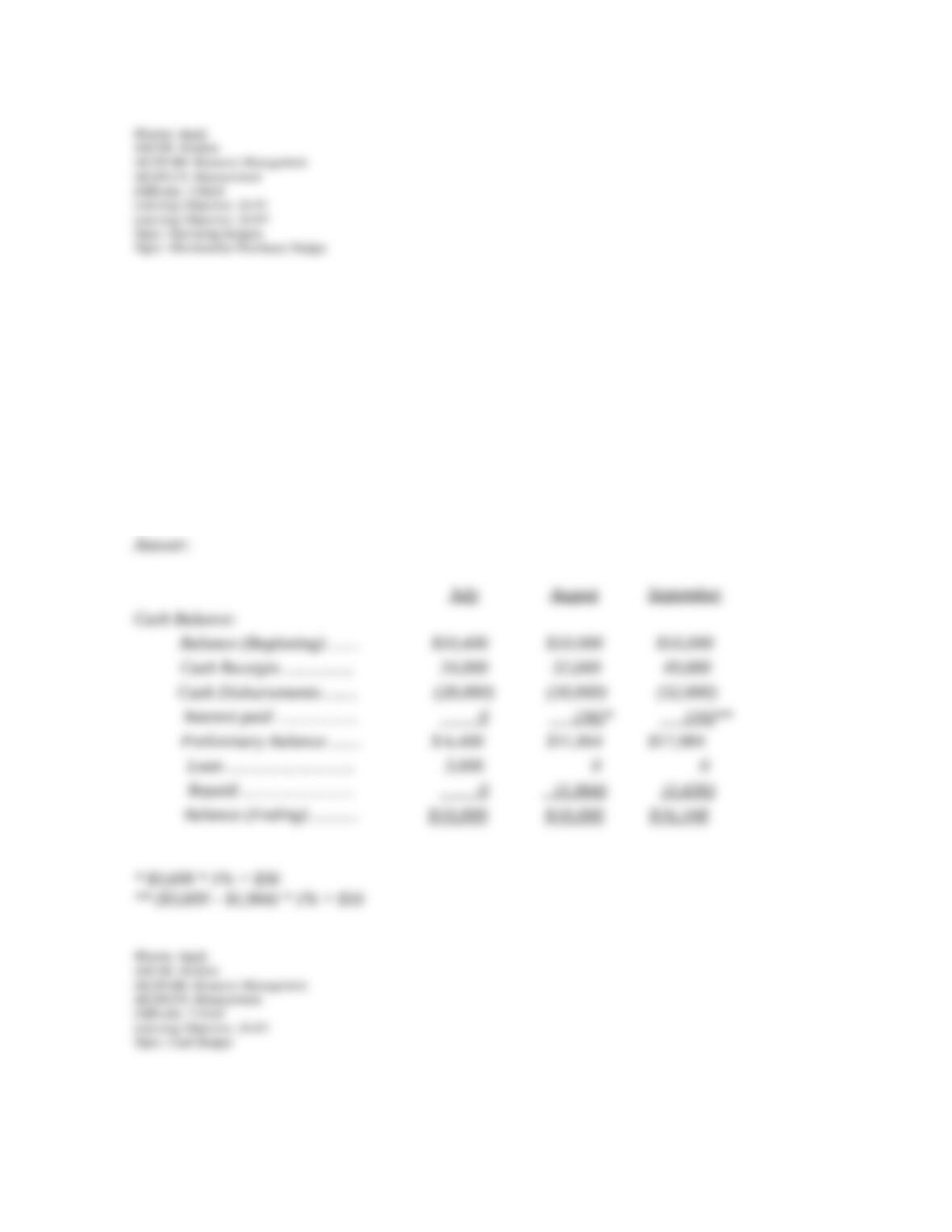

D. Rolling budget.

E. Production budget.

53. Operating budgets include all the following budgets except the:

A. Sales budget.

B. Selling expense budget.

C. Cash budget.

D. Merchandise purchases budget.

E. General and administrative expense budget.

54. Operating budgets include all the following except the:

A. Sales budget.

B. Budgeted balance sheet.

C. Production budget.

D. Selling expense budget.

E. General and administrative expense budget.

55. The master budget of a merchandising company includes a:

A. Production budget.

B. Direct materials budget.

C. Factory overhead budget.

D. Direct materials budget.

E. Purchases budget.

56. The usual starting point for preparing a master budget is forecasting or estimating:

A. Expenditures.

B. Sales.

C. Production.

D. Income.

E. Cash payments.

57. The master budget process usually ends with:

A. The production budget.

B. The sales budget.

C. The selling expense budget.

D. The budgeted balance sheet.

E. The overhead budget.

58. Which of the following budgets is not an operating budget?

A. Sales budget.

B. Cash budget.

C. General and administrative expense budget.

D. Selling expenses budget.

E. Merchandise purchases.

59. A budget system based on expected activities and their levels that enables management to

plan for resources required to perform the activities is:

A. Traditional budgeting.

B. Management budgeting.

C. Master budgeting.

D. Activity-based budgeting.

E. Cash budgeting.

60. A plan that lists the types and amounts of operating expenses expected that are not

included in the selling expenses budget is a:

A. General and administrative expense budget.

B. Sales budget.

C. Cash payments budget.

D. Overhead budget.

E. Selling expense budget.

61. Cameroon Corp. manufactures and sells electric staplers for $16 each. If 10,000 units

were sold in December, and management forecasts 4% growth in sales each month, the dollar

amount of electric stapler sales budgeted for February should be:

A. $187,177

B. $166,400

C. $179,978

D. $173,056

E. $160,000

62. Cameroon Corp. manufactures and sells electric staplers for $16 each. If 10,000 units

were sold in December, and management forecasts 4% growth in sales each month, the

number of electric stapler sales budgeted for March should be:

A. 10,000

B. 11,249

C. 10,400

D. 10,816

E. 11,000

63. A July sales forecast projects that 6,000 units are going to be sold at a price of $10.50 per

unit. The management forecasts 2% growth in sales each month. Total July sales are

anticipated to be:

A. $63,000.

B. $67,500.

C. $61,250.

D. $64,260.

E. $60,000.

64. Bengal Co. provides the following sales forecast for the next three months:

July August September

Sales units 5,000 5,700 5,560

The company wants to end each month with ending finished goods inventory equal to 25% of

the next month’s sales. Finished goods inventory on June 30 is 1,250 units. The budgeted

production units for July are:

A. 6,250 units.

B. 3,750 units.

C. 6,425 units.

D. 2,500 units.

E. 5,175 units.

65. Bengal Co. provides the following sales forecast for the next three months:

July August September

Sales units 5,000 5,700 5,560

The company wants to end each month with ending finished goods inventory equal to 25% of

the next month’s sales. Finished goods inventory on June 30 is 1,250 units. The budgeted

production units for August are:

A. 6,950 units.

B. 4,310 units.

C. 7,090 units.

D. 5,665 units.

E. 4,135 units.

66. A plan that lists dollar amounts to be received from disposing of plant assets and dollar

amounts to be spent on purchasing additional plant assets is called a:

A. Cash budget.

B. Capital expenditures budget.

C. Rolling budget.

D. Sales budget.

E. Production budget.

67. Flack Corporation provides the following information for its December budgeting

process:

The November 30 inventory was 1,800 units.

Budgeted sales for December are 4,000 units.

Desired December 31 inventory is 2,840 units.

Budgeted purchases are:

A. 5,040 units.

B. 1,240 units.

C. 6,840 units.

D. 4,000 units.

E. 5,800 units.

68. A plan that reports the units or costs of merchandise to be purchased by a merchandising

company during the budget period is called a:

A. Selling expenses budget.

B. Merchandise purchases budget.

C. Sales budget.

D. Cash budget.

E. Capital expenditures budget.

69. A plan showing the planned sales units and the revenue to be derived from these sales, and

is the usual starting point in the budgeting process, is called the:

A. Operating budget.

B. Business plan.

C. Income statement budget.

D. Merchandise purchases budget.

E. Sales budget.

70. A plan that lists the types and amounts of selling expenses expected during the budget

period is called a(n):

A. Sales budget.

B. General and administrative budget.

C. Capital expenditures budget.

D. Selling expense budget.

E. Purchases budget.

71. Which of the following factors is least likely to be considered in preparing a sales

budget?

A. Business capacity.

B. Forecasted economic and market conditions.

C. Prediction of unit sales.

D. The capital expenditures budget.

E. Proposed selling expenses, such as advertising.

72. A department store has budgeted sales of 12,000 men's suits in September. Management

wants to have 6,000 suits in inventory at the end of the month to prepare for the winter

season. Beginning inventory for September is expected to be 4,000 suits. What is the dollar

amount of the purchase of suits if each suit has a cost of $75.

A. $ 750,000.

B. $ 900,000.

C. $1,050,000.

D. $1,200,000.

E. $1,350,000.

73. A sporting equipment store expects to purchase $8,000 of ski boots in October. The store

had $2,000 of ski boots in merchandise inventory at the beginning of October, and expects to

have $3,000 of ski boots in merchandise inventory at the end of October to cover part of

anticipated November sales. What is the budgeted cost of goods sold for October?

A. $ 5,000.

B. $ 7,000.

C. $ 8,000.

D. $ 9,000.

E. $10,000.

74. Masterson Company’s budgeted production calls for 56,000 liters in April and 52,000

liters in May of a key raw material that costs $1.85 per liter. Each month’s ending raw

materials inventory should equal 30% of the following month’s budgeted materials. The

January 1 inventory for this material is 16,800 liters. What is the budgeted materials need in

liters for April?

A. 71,600 liters.

B. 39,200 liters.

C. 57,600 liters.

D. 56,000 liters.

E. 54,800 liters.

75. A sporting goods manufacturer budgets production of 45,000 pairs of ski boots in the first

quarter and 30,000 pairs in the second quarter of the upcoming year. Each pair of boots

require 2 kg of a key raw material. The company aims to end each quarter with ending raw

materials inventory equal to 20% of the following quarter’s material needs. Beginning

inventory for this material is 18,000 kg and the cost per kg is $8. What is the budgeted

materials purchases cost for the first quarter?

A. $720,000.

B. $672,000.

C. $576,000.

D. $729,600.

E. $864,000.

76. A quantity of inventory that provides protection against lost sales caused by unfulfilled

demands from customers is called:

A. Just-in-time inventory.

B. Budgeted stock.

C. Continuous inventory.

D. Capital stock.

E. Safety stock.

77. Alliance Company’s budgets production of 24,000 units in January and 28,000 units in the

February. Each finished unit requires 4 pounds of raw material K that costs $2.50 per pound.

Each month’s ending raw materials inventory should equal 40% of the following month’s

budgeted materials. The January 1 inventory for this material is 38,400 pounds. What is the

budgeted materials need in pounds for January?

A. 102,400 pounds.

B. 96,000 pounds.

C. 57,600 pounds.

D. 140,800 pounds.

E. 83,200 pounds.

78. Schrank Company is trying to decide how many units of merchandise to order each

month. The company's policy is to have 20% of the next month's sales in inventory at the end

of each month. Projected sales for August, September, and October are 30,000 units, 20,000

units, and 40,000 units, respectively. How many units must be purchased in September?

A. 14,000.

B. 20,000.

C. 22,000.

D. 24,000.

E. 28,000.

79. Masterson Company’s budgeted production calls for 56,000 liters in April and 52,000

liters in May of a key raw material that costs $1.85 per liter. Each month’s ending raw

materials inventory should equal 30% of the following month’s budgeted materials. The

January 1 inventory for this material is 16,800 liters. What is the budgeted cost of materials

purchases for April?

A. $106,560.

B. $101,380.

C. $103,600.

D. $72,520.

E. $132,460.

80. When preparing the cash budget, all of the following should be considered except:

A. Cash receipts from customers.

B. Cash payments for merchandise.

C. Depreciation expense.

D. Cash payments for income taxes.

E. Cash payments for capital expenditures.

81. Bioclean Co. sells a biodegradable cleaning product and has predicted the following sales

for the first four months of the current year:

Jan. Feb. March April

Sales in Units ……….. 1,800 2,000 2,100 1,600

Ending inventory for each month should be 20% of the next month's sales, and the December

31 inventory is consistent with that policy. How many units should be purchased in

February?

A. 2,000.

B. 2,420.

C. 2,020.

D. 1,600

E. 2,820.

82. Garcia Manufacturing’s April sales forecast projects that 5,000 units will sell at a price of

$10.50 per unit. The desired ending inventory is 30% higher than the beginning inventory,

which was 1,000 units. Budgeted purchases of units in April would be:

A. 5,000 units.

B. 6,000 units.

C. 5,300 units.

D. 6,300 units.

E. Some other amount.

83. The sales budget for Modesto Corp. shows that 20,000 units of Product A and 22,000 units

of Product B are going to be sold for prices of $10 and $12, respectively. The desired ending

inventory of Product A is 20% higher than its beginning inventory of 2,000 units. The

beginning inventory of Product B is 2,500 units. The desired ending inventory of B is 3,000

units. Budgeted purchases of Product A for the year would be:

A. 22,400 units.

B. 20,400 units.

C. 20,000 units.

D. 19,500 units.

E. 12,200 units.

84. The sales budget for Modesto Corp. shows that 20,000 units of Product A and 22,000 units

of Product B are going to be sold for prices of $10 and $12, respectively. The desired ending

inventory of Product A is 20% higher than its beginning inventory of 2,000 units. The

beginning inventory of Product B is 2,500 units. The desired ending inventory of B is 3,000

units. Budgeted purchases of Product B for the year would be:

A. 24,500 units.

B. 22,500 units.

C. 16,500 units.

D. 26,500 units.

E. 20,500 units.

85. The sales budget for Modesto Corp. shows that 20,000 units of Product A and 22,000 units

of Product B are going to be sold for prices of $10 and $12, respectively. The desired ending

inventory of Product A is 20% higher than its beginning inventory of 2,000 units. The

beginning inventory of Product B is 2,500 units. The desired ending inventory of B is 3,000

units. Total budgeted sales of both products for the year would be:

A. $ 42,000.

B. $200,000.

C. $264,000.

D. $464,000.

E. $500,000.

86. If budgeted beginning inventory is $8,300, budgeted ending inventory is $9,400, and

budgeted cost of goods sold is $10,260, budgeted purchases should be:

A. $ 860

B. $ 1,100

C. $ 1,960

D. $ 9,160

E. $11,360

87. Coomb’s Fashions forecasts sales of $125,000 for the quarter ended December 31. Its

gross profit rate is 20% of sales, and its September 30 inventory is $32,500. If the December

31 inventory is targeted at $41,500, budgeted purchases for the fourth quarter should be:

A. $134,000.

B. $109,000.

C. $ 91,500.

D. $ 25,000.

E. $ 91,000.

88. A plan that shows the expected cash inflows and cash outflows during the budget period,

including receipts from loans needed to maintain a minimum cash balance and repayments of

such loans, is called a(n):

A. Capital expenditures budget.

B. Operating budget.

C. Rolling budget.

D. Cash budget.

E. Income statement.

89. Which of the following accounts would appear on a budgeted balance sheet?

A. Income tax expense.

B. Accounts receivable.

C. Sales commissions.

D. Depreciation expense.

E. All of the choices are correct.

90. Which of the following budgets is not completed before a cash budget is prepared?

A. Capital expenditures budget.

B. Sales budget.

C. Merchandise purchases budget.

D. General and administrative expense budget.

E. Budgeted income statement.

92. Western Company is preparing a cash budget for June. The company has $12,000 cash at

the beginning of June and anticipates $30,000 in cash receipts and $34,500 in cash

disbursements during June. Western Company has an agreement with its bank to maintain a

minimum cash balance of $10,000. As of May 31, the company owes $15,000 to the bank. To

maintain the $10,000 required balance, during June the company must:

A. Borrow $4,500.

B. Borrow $2,500.

C. Borrow $10,000.

D. Repay $7,500.

E. Repay $2,500.

93. A managerial accounting report that presents predicted amounts of the company's assets,

liabilities, and equity as of the end of the budget period is called a(n):

A. Rolling balance sheet.

B. Continuous balance sheet.

C. Budgeted balance sheet.

D. Cash balance sheet.

E. Operating balance sheet.

94. Southland Company is preparing a cash budget for August. The company has $17,000

cash at the beginning of August and anticipates $120,800 in cash receipts and $134,500 in

cash disbursements during August. Southland Company wants to maintain a minimum cash

balance of $10,000. The preliminary cash balance at the end of August before any loan

activity is:

A. $13,300.

B. $137,800.

C. ($13,700).

D. $3,300.

E. $27,000.

95. Southland Company is preparing a cash budget for August. The company has $17,000

cash at the beginning of August and anticipates $120,800 in cash receipts and $134,500 in

cash disbursements during August. Southland Company wants to maintain a minimum cash

balance of $10,000. To maintain the minimum cash balance of $10,000, the company must

borrow:

A. $0.

B. $. $10,000

C. $6,700.

D. $7,000.

E. $27,700.

96. Frankie’s Chocolate Co. reports the following information from its sales budget:

Expected Sales: July…………………….. $90,000

August…………………. 104,000

September……………… 120,000

Cash sales are normally 25% of total sales and all credit sales are expected to be collected in

the month following the date of sale. The total amount of cash expected to be received from

customers in September is:

A. $ 30,000.

B. $ 78,000.

C. $108,000.

D. $120,000.

E. $130,500.

97. Junior Snacks reports the following information from its sales budget:

Expected Sales: October…………………….. $143,000

November…………………. 151,000

December……………… 187,000

All sales are on credit and are expected to be collected 40% in the month of sale and 60% in

the month following sale. The total amount of cash expected to be received from customers in

November is:

A. $146,200.

B. $ 85,800.

C. $151,000.

D. $236,800.

E. $60,400.

98. A managerial accounting report that presents predicted amounts of the company's

revenues and expenses for the budget period is called a:

A. Budgeted income statement.

B. Budgeted balance sheet.

C. Master plan.

D. Rolling income statement.

E. Continuous profit statement.

99. Justin Company's budget includes the following credit sales for the current year:

September, $25,000; October, $36,000; November, $30,000; December, $32,000. Experience

has shown that payment for the credit sales is received as follows: 15% in the month of sale,

60% in the first month after sale, 20% in the second month after sale, and 5% is uncollectible.

How much cash can Justin Company expect to collect in November as a result of current and

past credit sales?

A. $19,700.

B. $28,500.

C. $30,000.

D. $31,100.

E. $33,900.

100. Funcycle Manufacturing's budget includes the following credit sales for the current year:

September, $145,000; October, $136,000; November, $120,000; December, $157,000.

Experience has shown that payment for the credit sales is received as follows: 15% in the

month of sale, 50% in the first month after sale, and 35% in the second month after sale. What

are the cash collections of credit sales in the month of December?

A. $23,550.

B. $107,600.

C. $83,550.

D. $157,000.

E. $131,150.

101. In preparing a budgeted balance sheet, the amount for Accounts Receivable data can be

derived from:

A. The purchases budget and schedule of cash payments.

B. The sales budget and the schedule of cash receipts.

C. The capital expenditures budget and purchases budget.

D. The budgeted income statement and budgeted balance sheet.

E. The selling expenses budget and the schedule of cash receipts.

102. Long-term liability data for the budgeted balance sheet is derived from:

A. The cash budget and capital expenditures budget.

B. The cash budget and sales budget.

C. The cash budget and budgeted income statement.

D. The sales budget and production budget.

E. The asset budget and debt budget.

103. In preparing financial budgets:

A. The budgeted balance sheet is usually prepared last.

B. The cash budget is usually not prepared.

C. The budgeted income statement is usually not prepared.

D. The capital expenditures budget is usually prepared last.

E. The budgeted income statement is usually prepared last.

104. A company's history indicates that 20% of its sales are for cash and the rest are on credit.

Collections on credit sales are 20% in the month of the sale, 50% in the next month, 25% the

following month, and 5% is uncollectible. Projected sales for December, January, and

February are $60,000, $85,000 and $95,000, respectively. The February expected cash

receipts from all current and prior credit sales is:

A. $57,000

B. $61,200

C. $66,400

D. $80,750

E. $90,250

105. A company's history indicates that 20% of its sales are for cash and the rest are on credit.

Collections on credit sales are 30% in the month of the sale, 50% in the next month, and 15%

the following month. Projected sales for January, February, and March are $60,000, $85,000

and $95,000, respectively. The March expected cash receipts from all current and prior credit

sales is:

A. $57,000

B. $63,080

C. $64,000

D. $80,750

E. $90,250

106. Walter Enterprises expects its September sales to be 20% higher than its August sales of

$150,000. Purchases were $100,000 in August and are expected to be $120,000 in September.

All sales are on credit and are collected as follows: 30% in the month of the sale and 70% in

the following month. Merchandise purchases are paid as follows: 25% in the month of

purchase and 75% in the following month. The beginning cash balance on September 1 is

$7,500. The ending cash balance on September 30 would be:

A. $31,500.

B. $67,500.

C. $54,000.

D. $61,500.

E. $136,500.

107. The Ballentine Company expects sales for June, July, and August of $48,000, $54,000,

and $44,000, respectively. Experience suggests that 40% of sales are for cash and 60% are on

credit. The company collects 50% of its credit sales in the month following sale, 45% in the

second month following sale, and 5% are not collected. What are the company's expected

cash receipts for August from its current and past sales?

A. $29,160.

B. $46,760.

C. $61,160.

D. $66,200.

E. $78,800.

108. The Gardner Company expects sales for October of $248,000. Experience suggests that

45% of sales are for cash and 55% are on credit. The company collects 50% of its credit sales

in the month of sale and 50% in the month following sale. Budgeted Accounts Receivable on

September 30 is $67,000. What is the amount of cash expected to be collected in October?

A. $124,000.

B. $178,600.

C. $179,800.

D. $111,600.

E. $246,800.

109. The Gardner Company expects sales for October of $248,000. Experience suggests that

45% of sales are for cash and 55% are on credit. The company collects 50% of its credit sales

in the month of sale and 50% in the month following sale. Budgeted Accounts Receivable on

September 30 is $67,000. What is the amount of Accounted Receivables on the October 31

budgeted balance sheet?

A. $111,600.

B. $124,000.

C. $67,000.

D. $68,200.

E. $136,400.

110. Wichita Industries’ sales are 10% cash and 90% on credit. Credit sales are collected as

follows: 30% in the month of sale, 50% in the next month, and 20% in the following month.

On December 31, the accounts receivable balance includes $12,000 from November sales and

$42,000 from December sales. Assume that total sales for January are budgeted to be $50,000.

What are the expected cash receipts for January from the current and past sales?

A. $18,500.

B. $51,500.

C. $51,900.

D. $55,500.

E. $60,500.

111. Wichita Industries’ sales are 10% for cash and 90% on credit. Credit sales are collected

as follows: 30% in the month of sale, 50% in the next month, and 20% in the following

month. On December 31, the accounts receivable balance includes $12,000 from November

sales and $42,000 from December sales. Assume that total sales for January and February are

budgeted to be $50,000 and $100,000, respectively. What are the expected cash receipts for

February from current and past sales?

A. $80,500.

B. $71,500.

C. $34,500.

D. $61,500.

E. $59,500.

112. Which of the following must be prepared before the direct labor budget?

A. Budgeted income statement.

B. Merchandise purchases budget.

C. Capital expenditures budget.

D. Selling expense budget.

E. Production budget.

113. To determine the production budget for an accounting period, consideration is given to

all of the following except:

A. Budgeted ending inventory.

B. Budgeted beginning inventory.

C. Budgeted sales.

D. Budgeted overhead.

E. Ratio of inventory to future sales.

114. Which of the following budgets is not a budget that a manufacturer would include in its

master budget?

A. Sales budget.

B. Direct materials budget.

C. Production budget.

D. Merchandise purchases budget.

E. Cash budget.

115. A plan that states the number of units to be produced in a future period, based on the

projected unit sales and inventory considerations, is the:

A. Sales budget.

B. Merchandise purchases budget.

C. Production budget.

D. Cash budget.

E. Manufacturing budget.

117. Cahuilla Corporation predicts the following sales in units for the coming four months:

April May June July

Sales in Units ……….. 240 280 300 240

Each month's ending Finished Goods inventory should be 40% of the next month's sales

March 31 Finished Goods inventory is 96 units. A finished unit requires five pounds of direct

material B. The March 31 Raw Materials inventory has 200 pounds of B. Each month's

ending Raw Materials inventory should be 30% of the following month's production needs.

The budgeted purchases of pounds of direct material B during May should be:

A. 1,422 lbs.

B. 288 lbs.

C. 1,854 lbs.

D. 276 lbs.

E. 1,008 lbs.

118. Charm Enterprises’ production budget shows the following units to be produced for the

coming three months:

April May June

Units to be produced ……….. 2,560 2,880 2,760

A finished unit requires four ounces of a key direct material. The March 31 Raw Materials

inventory has 2,560 ounces (oz.) of the material. Each month's ending Raw Materials

inventory should be 35% of the following month's production needs. The materials to be

purchased during May should be:

A. 11,352 oz.

B. 11,520 oz.

C. 7,448 oz.

D. 15,384 oz.

E. 7,616 oz.

119. Fortune Company’s direct materials budget shows the following cost of materials to be

purchased for the coming three months:

January February March

Material purchases ……….. $12,040 14,150 10,970

Payments for purchases are expected to be made 50% in the month of purchase and 50% in

the month following purchase. The December Accounts Payable balance is $6,500. The

budgeted cash payments for materials in January are:

A. $6,500.

B. $9,270.

C. $12,520.

D. $13,095

E. $18,540.

120. Memphis Company’s May sales budget calls for sales of $900,000. The store expects to

begin May with $50,000 of inventory and to end the month with $55,000 of inventory. Gross

margin is typically 45% of sales. Compute the budgeted cost of merchandise purchases for

May.

A. $550,000.

B. $500,000.

C. $495,000.

D. $460,000.

E. $490,000.

121. Fortune Company’s direct materials budget shows the following cost of materials to be

purchased for the coming three months:

January February March

Material purchases ……….. $12,040 14,150 10,970

Payments for purchases are expected to be made 50% in the month of purchase and 50% in

the month following purchase. The December Accounts Payable balance is $6,500. The

expected January 30 Accounts Payable balance is:

A. $6,500.

B. $7,075.

C. $12,040.

D. $6,020

E. $9,270.

122. Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the credit

sales, 30% are collected in the same month as the sale, 65% are collected during the first

month after the sale, and the remaining 5% are not collected. Compute the amount of cash

received from credit sales for May.

A. $561,500.

B. $652,500.

C. $817,500.

D. $592,500.

E. $890,000.

123. Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the credit

sales, 30% are collected in the same month as the sale, 65% are collected during the first

month after the sale, and the remaining 5% are not collected. Compute the amount of cash

received from total sales for May.

A. $561,500.

B. $652,500.

C. $817,500.

D. $592,500.

E. $890,000.

124. Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the credit

sales, 30% are collected in the same month as the sale, 65% are collected during the first

month after the sale, and the remaining 5% are not collected. Compute the amount of cash

received from credit sales for June.

A. $561,500.

B. $652,500.

C. $817,500.

D. $592,500.

E. $890,000.

125. Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the credit

sales, 30% are collected in the same month as the sale, 65% are collected during the first

month after the sale, and the remaining 5% are not collected. Compute the amount of cash

received from total sales for June.

A. $561,500.

B. $652,500.

C. $817,500.

D. $592,500.

E. $890,000.

126. Memphis Company anticipates total sales for April, May, and June of $800,000,

$900,000, and $950,000 respectively. Cash sales are normally 25% of total sales. Of the credit

sales, 30% are collected in the same month as the sale, 65% are collected during the first

month after the sale, and the remaining 5% are collected in the second month. Compute the

amount of accounts receivable reported on the company’s budgeted balance sheet for June

30.

A. $561,500.

B. $712,500.

C. $463,125.

D. $496,875.

E. $617,500.

127. Ratchet Manufacturing’s August sales budget calls for sales of 8,000 units. Each month’s

sales are expected to exceed the prior month’s results by 5%. The product selling price is $25

per unit. The expected total sales dollars for September’s sales budget are:

A. $200,000.

B. $190,000.

C. $210,000.

D. $220,000.

E. $8,400.

128. Ratchet Manufacturing anticipates total sales for August, September, and October of

$200,000, $210,000, and $220,500 respectively. Cash sales are normally 25% of total sales

and the remaining sales are on credit. All credit sales are collected in the first month after the

sale. Compute the amount of cash received for September.

A. $150,000.

B. $202,500.

C. $157,500.

D. $102,500.

E. $307,500.

129. Ratchet Manufacturing anticipates total sales for August, September, and October of

$200,000, $210,000, and $220,500 respectively. Cash sales are normally 25% of total sales

and the remaining sales are on credit. All credit sales are collected in the first month after the

sale. Compute the amount of accounts receivable to be reported on the company’s budgeted

balance sheet for August.

A. $150,000.

B. $50,000.

C. $157,500.

D. $52,500.

E. $200,000.

130. Use the following information to determine the ending cash balance to be reported on the

month ended June 30 cash budget.

a. Beginning cash balance on June 1, $73,000.

b. Cash receipts from sales, $413,000.

c. Budgeted cash disbursements for purchases, $268,000.

d. Budgeted cash disbursements for salaries, $35,000.

e. Other budgeted cash expenses, $57,000.

f. Cash repayment of bank loan, $32,000.

g. Budgeted depreciation expense, $34,000.

A. $94,000.

B. $60,000.

C. $126,000.

D. $149,000.

E. $21,000.

131. Trago Company manufactures a single product and has a JIT policy that ending

inventory must equal 5% of the next month’s sales. It estimates that May’s ending inventory

will consist of 14,000 units. June and July sales are estimated to be 280,000 and 290,000

units, respectively. Compute the number of units to be produced that would appear on the

company’s production budget for the month of June.

A. 290,000.

B. 294,500.

C. 280,500.

D. 280,000.

E. 266,000.

132. Trago Company manufactures a single product and has a JIT policy that ending

inventory must equal 5% of the next month’s sales. It estimates that May’s ending inventory

will consist of 14,000 units. June and July sales are estimated to be 280,000 and 290,000

units, respectively. Trago assigns variable overhead at a rate of $1.80 per unit of production.

Fixed overhead equals $400,000 per month. Compute the number of units to be produced and

use this amount to compute the total budgeted overhead that would appear on the factory

overhead budget for month of June.

A. $920,200.

B. $904,900.

C. $930,100.

D. $922,000.

E. $878,800

133. Glaston Company manufactures a single product using a JIT inventory system. The

production budget indicates that the number of units expected to be produced are 193,000 in

October, 201,500 in November, and 198,000 in December. Glaston assigns variable overhead

at a rate of $0.75 per unit of production. Fixed overhead equals $150,000 per month. Compute

the total budgeted overhead that would appear on the factory overhead budget for month of

October.

A. $343,000.

B. $150,000.

C. $144,750.

D. $301,125.

E. $294,750.

134. Zhang Industries sells a product for $700. Unit sales for May were 400 and each month’s

sales are expected to exceed the prior month’s results by 3%. Compute the total sales dollars

to be reported on the sales budget for month ended June 30.

A. $280,000.

B. $297,000.

C. $271,600.

D. $288,400.

E. $364,000.

135. Zhang Industries sells a product for $700. Unit sales for May were 400 and each month’s

sales are expected to exceed the prior month’s results by 3%. Zhang pays a sales manager a

monthly salary of $3,000 and a commission of 2% of sales. Compute the projected selling

expense to be reported on the selling expense budget for the manager for month ended June

30.

A. $8,600.

B. $11,652.

C. $8,652.

D. $5,768.

E. $8,768.

136. Zhang Industries sells a product for $700. Unit sales for May were 400 and each month’s

sales are expected to exceed the prior month’s results by 3%. Zhang pays a sales manager a

monthly salary of $3,000 and a commission of 2% of sales in dollars. Assume 30% of Zhang’s

sales are for cash. The remaining 70% are credit sales; these customers pay in the month

following the sale. Compute the budgeted cash receipts for June.

A. $282,520.

B. $196,000.

C. $201,880.

D. $280,000.

E. $285,880.

137. Zhang Industries budgets production of 300 units in June and 310 units in July. Each

finished unit requires 4 pounds of raw material K, which costs $5 per pound. Each month’s

ending inventory of raw materials should be 30% of the following month’s budgeted

production. The June 1 raw materials inventory has 360 pounds of raw material K. Compute

budgeted purchases for raw material K for June.

A. 1,200 lbs.

B. 1,240 lbs.

C. 1,212 lbs.

D. 1,220 lbs.

E. 880 lbs.

138. Zhang Industries budgets production of 300 units in June and 310 units in July. Each unit

requires 1.5 hours of direct labor. The direct labor rate if $14 per hour. The indirect labor rate

is $21.00 per hour. Compute the budgeted direct labor cost for July.

A. $6,300.

B. $6,510.

C. $9,450.

D. $9,765.

E. $16,275.

139. Zhang Industries is preparing a cash budget for June. The company has $25,000 cash at

the beginning of June and anticipates $95,000 in cash receipts and $111,290 in cash

disbursements during June. The company has no loans outstanding on June 1. Compute the

amount the company must borrow, if any, to maintain a $20,000 cash balance.

A. $28,710.

B. $12,290.

C. $16,290.

D. $11,290

E. $6,290.

140. Webster Corporation’s budgeted sales for February are $325,000. Webster pays sales

representatives a commission of 6% of sales dollars. The company pays a sales manager a

monthly salary of $4,400 and expects advertising expense of $2,000 per month. Compute the

total selling expenses to be reported on the selling expense budget for the month of February.

A. $19,500.

B. $6,400.

C. $23,900.

D. $25,900.

E. $21,500.

141. Webster Corporation is preparing a master budget for the first quarter of the year. The

company budgets production of 2,680 units in January, 2,600 units in February and 2,740

units in March. Each unit requires 0.6 hours of direct labor. The direct labor rate is $12 per

hour. Compute the budgeted direct labor cost for the first quarter budget.

A. $56,160.

B. $57,744.

C. $96,240.

D. $93,600.

E. $48,120.

142. Webster Corporation’s monthly projected general and administrative expenses include

$5,000 administrative salaries, $2,400 of other cash administrative expenses, $1,350 of

depreciation expense, and 0.5% monthly interest on an outstanding bank loan of $10,000.

Compute the total general and administrative expenses to be reported on the general and

administrative expense budget per month.

A. $17,400.

B. $7,400.

C. $7,450.

D. $5,050.

E. $8,800.

143. Webster Corporation is preparing its cash budget for April. The March 31 cash balance

is $36,400. Cash receipts are expected to be $641,000 and cash payments for purchases are

expected to be $608,500. Other cash expenses expected are $27,000 selling and $33,500

general and administrative. The company desires a minimum cash balance at the end of each

month of $30,000. If necessary, the company borrows enough cash to meet the minimum

using a short-term note. Webster’s preliminary cash balance before loan activity for April is

expected to be:

A. $8,400.

B. $21,600.

C. $30,000.

D. ($28,000).

E. $68,900.

144. Flagstaff Company has budgeted production units for July of 7,900 units. Variable

factory overhead is $1.20 per unit. Budgeted fixed factory overhead is $19,000, which

includes $3,000 of factory equipment depreciation. Compute the total budgeted overhead to

be reported on the factory overhead budget for the month.

A. $25,480.

B. $19,000.

C. $23,900.

D. $28,480.

E. $9,480.

145. Flagstaff Company has budgeted production units of 7,900 for July and 8,100 for

August. The direct materials requirement per unit is 2 ounces. The company has determined

that it wants to have safety stock of direct materials on hand at the end of each month to

complete 20% of the units budgeted in the following month. There was 3,160 ounces of direct

material in inventory at the start of July. The total amount direct materials in ounces to be

purchased in July is.

A. 15,800.

B. 16,200.

C. 19,040.

D. 15,880.

E. 15,720.

146. Flagstaff Company has budgeted production units of 7,900 for July and 8,100 for

August. The direct materials requirement per unit is 2 ounces. The company has determined

that it wants to have safety stock of direct materials on hand at the end of each month to

complete 20% of the units budgeted in the following month. There was 3,160 ounces of direct

material in inventory at the start of July. The total cost of direct materials purchases for the

July direct materials budget, assuming the materials cost $1.15 per ounce, is:

A. $18,262.

B. $21,896.

C. $14,536.

D. $18,078.

E. $18,170.

147. Flagstaff Company has budgeted production units of 7,900 for July and 8,100 for

August. The direct labor requirement per unit is 0.50 hours. Labor is paid at the rate of $21

per hour. The total cost of direct labor for the month of August is:

A. $82,950.

B. $4,050.

C. $85,050.

D. $3,950.

E. $168,000.

148. On its December 31, 2014, balance sheet, Calgary Industries reports equipment of

$370,000 and accumulated depreciation of $74,000. During 2015, the company plans to

purchase additional equipment costing $80,000 and expects depreciation expense of $30,000.

Additionally, it plans to dispose of equipment that originally cost $42,000 and had

accumulated depreciation of $5,600. The balances for equipment and accumulated

depreciation, respectively, on the December 31, 2015 budgeted balance sheet are:

A. $328,000; $74,000.

B. $450,000; $98,400.

C. $450,000; $104,000

D. $408,000; $104,000.

E. $408,000; $98,400.

149. Calgary Industries is preparing a budgeted income statement for 2015 and has

accumulated the following information. Predicted sales for the year are $730,000 and cost of

goods sold is 40% of sales. The expected selling expenses are $81,000 and the expected

general and administrative expenses are $90,000, which includes $23,000 of depreciation. The

companies income tax rate is 30%. The budgeted net income for 2015 is:

A. $438,000.

B. $186,900.

C. $267,000

D. $84,700.

E. $80,100.

150. Grason Corporation is preparing a budgeted balance sheet for 2015. The retained

earnings balance at December 31, 2014 was $533,500. The 2015 budgeted income statement

shows expected net income of $112,000. The company expects to declare dividends during

2015 amounting to $40,000. The expected balance in retained earnings on the 2015 budgeted

balance sheet is:

A. $533,500.

B. $605,500.

C. $645,500

D. $493,500.

E. $685,500.

151. Match the definitions 1 through 9 with the correct term or phrase a through i.

(a) Master budget

(b) General and administrative expense budget

(c) Budget

(d) Safety stock

(e) Budgeted income statement

(f) Budgeted balance sheet

(g) Sales budget

(h) Cash budget

(i) Merchandise purchases budget

______(1) A plan that shows the units and dollars of merchandise to be purchased during the

budget period.

______(2) A managerial accounting report that shows predicted amounts of the company's

assets, liabilities, and balances as of the end of the budget period.

______(3) A plan that shows the expected sales units and the dollars from these sales.

______(4) A managerial accounting report that shows predicted amounts of sales and

expenses for the budget period.

______(5) A quantity of inventory that provides protection against lost sales caused by

unfulfilled demand from customers or delays in shipments from suppliers.

______(6) A formal, comprehensive plan for a company’s future that includes several

individual budgets that are linked with each other to form a coordinated plan.

______(7) A formal statement of a company's future plans, usually expressed in monetary

terms.

______(8) A plan that plans the predicted operating expenses not included in the selling

expenses or manufacturing budgets.

______(9) A plan that shows the expected cash inflows and cash outflows during the budget

period.

1. I; 2. F; 3. G; 4. E; 5. D; 6. A; 7. C; 8. B; 9. H

Blooms: Remember

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 1 Easy

Learning Objective: 20-C1

Learning Objective: 20-C2

Learning Objective: 20-P1

Learning Objective: 20-P2

Learning Objective: 20-P3

Learning Objective: 20-P4

Topic: Budget Process and Administration

Topic: The Master Budget

Topic: Operating Budgets

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

20-85

Topic: Cash Budget

Topic: Budgeted Financial Statements

Topic: Merchandise Purchases Budget

152. Presented below are terms or phrases preceded by letters a through j and followed by a

list of definitions 1 through 10. Match the correct definitions with the terms or phrases by

placing the letter of the term or phrase in the answer space provided at the beginning of the

definition.

(a) Budget

(b) Capital expenditures budget

(c) Activity-based budgeting

(d) Sales budget

(e) Production budget

(f) Cash budget

(g) Budgeted balance sheet

(h) Continuous budgeting

(i) Selling expense budget

(j) Rolling budgets

_____ (1) A plan that lists the types and amounts of selling expenses expected during the

budget period.

_____ (2) A plan that shows expected activities and their levels for the budget period used to

estimate resources required to perform the activities.

_____ (3) A managerial accounting report that presents predicted amounts of the company's

assets, liabilities, and equity as of the end of the budget period.

_____ (4) A formal statement of future plans, usually expressed in monetary terms.

_____ (5) A plan showing the expected sales units and dollars from the sales; the starting

point in the budgeting process.

_____ (6) A plan that lists dollar amounts estimated to be received from disposing of plant

assets and spent on purchasing additional plant assets to carry out the budgeted

business activities.

______(7) The practice of preparing budgets for a selected number of several periods and

revising those budgets as each period is completed.

______(8) A plan showing the number of units to be produced each period, based on the units

projected in the sales budget, along with inventory considerations.

______ 9) A plan that shows the expected cash inflows and outflows during the budget period,

including receipts from loans needed to maintain a minimum cash balance and

repayments of such loans.

______(10) Additional monthly or quarterly budgets to replace the ones that have lapsed as

each budget period goes by.

1. I; 2. C; 3. G; 4. A; 5. D; 6. B; 7. H; 8. E; 9. F; 10. J

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

20-86

Blooms: Remember

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 1 Easy

Learning Objective: 20-C1

Learning Objective: 20-C2

Learning Objective: 20-P1

Learning Objective: 20-P2

Learning Objective: 20-P3

Topic: Budget Process and Administration

Topic: The Master Budget

Topic: Operating Budgets

Topic: Cash Budget

Topic: Budgeted Financial Statements

Short Answer Questions

153. Describe at least five benefits of budgeting.

154. List the three important guidelines that should be followed in the budgeting process.

155. What are rolling budgets? Why are rolling budgets prepared?

156. Briefly describe the process by which budgets are developed and administered.

157. Briefly describe a master budget and the sequence in which the individual budgets within

the master budget are prepared.

158. What is activity-based budgeting?

159. Why is the sales budget usually prepared first?

160. What is a sales budget? How is the sales budget prepared?

161. What is a merchandise purchases budget? How is the merchandise purchases budget

constructed?

162. What is a capital expenditures budget?

163. What is a cash budget? How can management use a cash budget?

164. What is a production budget?

165. A department store has budgeted cost of goods sold for March of $60,000 for its

women's shorts. Management wants to have $12,000 of shorts in inventory at the end of the

month to prepare for the summer season. Beginning inventory in March was $8,000. What

dollar amount of shorts should be purchased to meet the above plans?

166. A sporting goods store budgeted August purchases of ski jackets at $140,000. The store

had ski jackets costing $12,000 in its inventory at the beginning of August; and to cover part

of anticipated September sales, they expect to have $25,000 of ski jackets in inventory at the

end of the month of August. What is the budgeted cost of goods sold for August?

167. In preparing a budget for the last three months of the current year, Country Cozy

Company is planning the units of merchandise it must order each month. The company's

policy is to have 15% of the next month's sales in its inventory at the end of each month.

Projected sales for October, November, and December are 27,000 units, 29,500 units, and

31,000 units, respectively. How many units must be ordered in November?

168. Dado, Inc. is preparing its budget for the second quarter. The following sales data have

been forecasted:

April May June July August

Unit sales……………….. 640 720 780 620 660

Additional information follows:

Inventory on March 31: 192 Units

Desired ending inventory each month:

30% of next month's

sales

Prepare a merchandise purchases budget for the total units to be purchased in the months of

April, May, and June, as well as the total unit purchases for entire the quarter.

169. Greco Company has prepared the following forecasts of monthly sales:

July August September October

Sales (in Units) ……….. 4,500 5,300 4,000 3,700

Greco has decided that the number of units in its inventory at the end of each month should

equal 25% of the next month's sales. The budgeted cost per unit is $30.

(1) How many units should be in July's beginning inventory?

(2) What amount should be budgeted for the cost of merchandise purchases in July?

170. Hammerly Corporation is preparing its master budget for the quarter ending March 31. It

sells a single product for $25 a unit. Budgeted sales are 40% cash and 60% on credit. All

credit sales are collected in the month following the sales. Budgeted sales for the next four

months follow:

January February March April

Sales in Units ………………. 1,200 1,000 1,600 1,400

At December 31, the balance in accounts receivable is $10,000, which represents the

uncollected portion of December sales. The company desires merchandise inventory equal to

30% of the next month's sales in units. The December 31 balance of merchandise inventory is

340 units, and inventory cost is $10 per unit. Forty percent of the purchases are paid in the

month of purchase and 60% are paid in the following month. At December 31, the balance of

Accounts Payable is $8,000, which represents the unpaid portion of December's purchases.

Operating expenses are paid in the month incurred and consist of:

· Sales commissions (10% of sales)

· Freight (2% of sales)

· Office salaries ($2,400 per month)

· Rent ($4,800 per month)

Depreciation expense is $4,000 per month. The income tax rate is 40%, and income taxes will

be paid on April 1. A minimum cash balance of $10,000 is required, and the cash balance at

December 31 is $10,200. Loans are obtained at the end of a month in which a cash shortage

occurs. Interest is 1% per month, based on the beginning of the month loan balance, and must

be paid each month. If the ending cash balance exceeds the minimum, the excess will be

applied to repaying any outstanding loan balance. At December 31, the loan balance is $0.

Prepare a master budget (round all dollar amounts to the nearest whole dollar) for each of the

months of January, February, and March that includes the:

· Sales budget

· Schedule of cash receipts

· Merchandise purchases budget

· Schedule of cash disbursements for merchandise purchases

· Schedule of cash disbursements for selling and administrative expenses (combined)

· Cash budget, including information on the loan balance

· Budgeted income statement for the quarter

171. Oxford, Inc., is preparing its master budget for the quarter ended June 30. It sells a single

product for $40 each. Sales are 60% cash and 40% on credit. All credit sales are collected in

the month following the sale. At March 31, the balance in accounts receivable is $12,000,

which represents the uncollected balance on March sales. Budgeted sales for the next four

months follow:

April May June July

Sales in Units ……….. 800 1,000 600 1,200

The product cost is $20 per unit, and desired ending inventory is 60% of the following

month's sales in units. Inventory at March 31 is 480 units. Purchases are paid 50% in the

month of purchase and 50% in the following month. At March 31, the balance in accounts

payable is $11,000, which represents the unpaid purchases from March. Operating expenses

are paid in the month incurred and consist of:

· Commissions (10% of sales)

· Shipping (3% of sales)

· Office salaries ($3,000 per month)

· Rent ($5,000 per month)

Depreciation is $2,000 per month. Income taxes are 40%, and will be paid on July 1. There

are no taxes payable at March 31. A minimum cash balance of $12,000 is required, and the

beginning cash balance is $12,000. Loans are obtained at the end of any month when a cash

shortage occurs. Interest is 1% per month based on the beginning of the month loan balance

and is paid at each month end. If the ending cash balance exceeds the minimum, the excess

will be applied to repaying any outstanding loan balance. At March 31, the loan balance is

$2,000. Prepare a master budget (round all dollar amounts to the nearest whole dollar) for

each of the months of April, May, and June that includes the:

· Sales budget

· Schedule of cash receipts

· Merchandise purchases budget

· Schedule of cash disbursements for purchases of merchandise

· Schedule of cash disbursements for selling and administrative expenses (combined)

· Cash budget, including information on the loan balance

· Budgeted income statement for the quarter

172. Stanley Company is preparing a cash budget for February. The company has $30,000

cash at the beginning of February and anticipates $75,000 in cash receipts and $96,250 in cash

disbursements during February. Stanley Company has an agreement with its bank to maintain

a cash balance of $10,000. What amount, if any, must the company borrow during February to

maintain a $10,000 cash balance?

173. Groundworks Company budgeted the following credit sales during the current year:

September, $90,000; October, $123,000; November, $105,000; December, $111,000.

Experience has shown that cash from credit sales is received as follows: 10% in the month of

sale, 50% in the first month after sale, 35% in the second month after sale, and 5% is

uncollectible. How much cash should Groundworks Company expect to collect in November

from all current and past credit sales?

174. The Ewing Company budgeted sales for January, February, and March of $96,000,

$88,000, and $72,000, respectively. Seventy percent of sales are on credit. The company

collects 60% of its credit sales in the month following sale, and 40% in the second month

following sale. What are Ewing’s expected cash receipts for March related to all current and

past sales?

175. Lafayette Company's experience shows that 20% of its sales are for cash and 80% are on

credit. An analysis of credit sales shows that 50% are collected in the month following the

sale, 45% are collected in the second month, and 5% prove to be uncollectible. Calculate the

following.

August September October November

Sales ……….. $500,000 $525,000 $535,000 $550,000

October November

Receipts from cash sales ……………... (1) (6)

Collections from August credit sales … (2) (7)

Collections from September credit

sales (3) (8)

Collections from October credit sales ... (4) (9)

Total cash collections during the month (5) (10)

176. Use the following data to determine the company's cash disbursements for August and

September:

July August September

Sales……………….. $24,000 $32,000 $36,000

Purchases…………. 14,400 $19,200 $21,600

Payments for purchases……….. One month after purchase

Selling expenses………………… 15% of sales, paid in the month of sale

Administrative expenses……….. 10% of sales, paid in the month of sale

Rent expense……………………. $2,400 per month

Equipment depreciation………… $1,300 per month

177. Widmer Corp. requires a minimum $10,000 cash balance. If necessary, loans are taken to

meet this requirement at a cost of 1% interest per month (paid monthly). If the ending cash

balance exceeds the minimum, the excess will be applied to repaying any outstanding loan

balance. The cash balance on July 1 is $10,400. Cash receipts other than for loans received for

July, August, and September are forecasted as $24,000, $32,000, and $40,000, respectively.

Payments other than for loan or interest payments for the same period are planned at $28,000,

$30,000, and $32,000, respectively at July 1, there are no outstanding loans.

Required:

Prepare a cash budget for July, August, and September.

178. The following information is available for Jergenson Company:

a. The Cash Budget for March shows a bank loan of $10,000 and an ending cash balance of

$48,000.

b. The Sales Budget for March indicates sales of $120,000. Accounts receivable is expected to

be 70% of the current-month sales.

c. The Merchandise Purchases Budget indicates that $90,000 in merchandise will be

purchased in March on account and ending inventory for March is predicted to be 600 units @

$35. Purchases on account are paid 100% in the month following the purchase.

d. The Budgeted Income Statement shows a net income of $48,000 and $21,000 in income tax

expense for the quarter ended March 31. Accrued taxes will be paid in April.

e. The Balance Sheet for February shows equipment of $77,000 with accumulated

depreciation of $28,000, common stock of $25,000 and retained earnings of $8,000. There are

no changes budgeted in the equipment or common stock accounts.

Prepare a budgeted balance sheet for March.

179. Diego, Inc., sells two products, Baubles and Charms. The sales forecast in units for the

first quarter of the coming year is:

Baubles Charms

January….. 20,000 36,000

February… 28,000 60,000

March…… 36,000 64,000

Cash sales are 30% of each product's monthly sales. The remaining sales are credit sales

which are collected as follows: 70% in the month of sale, 20% the next month, and 10% in the

following month. Unit sale prices are $30 and $20 for Baubles and Charms, respectively.

Determine the company's cash receipts for March from its current and past sales.

180. Todd Enterprises is preparing a cash budget for the second quarter of the coming year.

The following data have been forecasted:

April May

Sales ………………………………………………. $150,000 $157,500

Merchandise purchases …………………………… 107,000 112,400

Operating expenses:

Payroll …………………………………………. 13,600 14,280

Advertising ……………………………………. 5,400 5,700

Rent ……………………………………………. 2,500 2,500

Depreciation …………………………………… 7,500 7,500

End of April balances:

Cash ……………………………………………. 30,000

Bank loan payable ……………………………… 26,000

Additional data:

(1) Sales are 40% cash and 60% credit. The collection pattern for credit sales is 50% in the

month following the sale and 50% in the month thereafter. Total sales in March were

$125,000.

(2) Purchases are all on credit, with 40% paid in the month of purchase and the balance paid

in the following month.

(3) Operating expenses are paid in the month they are incurred.

(4) A minimum cash balance of $25,000 is required at the end of each month.

(5) Loans are used to maintain the minimum cash balance. At the end of each month, interest

of 1% per month is paid on the outstanding loan balance as of the beginning of the month.

Repayments are made whenever excess cash is available.

Prepare the company's cash budget for May. Show the ending loan balance at May 31.

181. Argenta, Inc. is preparing its master budget for the first quarter of its calendar year. The

following forecasted data relate to the first quarter:

Unit sales:

January …………………………….. 40,000

February …………………………… 55,000

March ……………………………… 50,000

Unit sales price ………………………. $25

Cost of goods sold per unit …………... $13

Expenses:

Commissions ……………………… 10% of sales

Rent ……………………………….. $20,000/month

Advertising ……………………….. 15% of sales

Office salaries …………………….. $75,000/month

Depreciation ………………………. $50,000/month

Interest …………………………….. 15% annually on a $250,000 note payable

Tax rate 40%

Prepare a budgeted income statement for this first quarter.

182. The production budget for Greski Company revealed the following production volume

for the months of July–September. Each unit produced requires 2.5 hours of direct labor. The

direct labor rate is predicted to be $16 per hour in all months. Prepare a direct labor budget for

Greski Company for July–September.

July Aug Sept

Units to be produced 620 680 540

183. Addams, Inc., is preparing its master budget for the second quarter. The following sales

and production data have been forecasted:

April May June July August

Unit sales …… 400 500 520 480 540

Finished goods inventory on March 31: 120 units

Raw materials inventory on March 31: 450 pounds

Desired ending inventory each month:

Finished goods: 30% of next month's sales

Raw materials: 25% of next month's production needs

Number of pounds of raw material required per finished unit: 4 lbs.

How many pounds of raw materials should be purchased in April?

184. Snap, Inc., provides the following data for the next four months:

April May June

Budgeted production units 442 570 544

Ending Raw Materials Inventory ……. 663 lbs.

Ending Finished Goods Inventory …... 174 Units

Desired Ending Inventory:

Raw Materials = 30% of next month's production needs

Pounds of raw material required for each finished Unit = 5 lbs.

Required:

Calculate the amount of purchases of raw materials in pounds for April and May.

185. Use the following information to prepare the June cash budget for Springer Company. It

should show expected cash receipts and cash disbursement for the month and the cash balance

expected on June 30.

a. Beginning cash balance on June 1 is $52,000.

b. Cash receipts from sales are expected to be $1,625,000.

c. Cash payments for direct materials and direct labor are expected to be $246,500 and

573,100, respectively.

d. Budgeted cash payments for variable overhead is $340,000.

e. Budgeted depreciation, the only fixed overhead estimated for June: $24,000.

f. Cash selling and administrative expenses budgeted for June are $282,000.

g. Bank loan interest due in June: $8,000.

i. Loan payment of $50,000 should be made if the preliminary cash balance is greater than

$200,000.

186. Use the following information to prepare a budgeted income statement for Stellar

Company for the month of June.

a. Beginning cash balance on June 1 is $52,000.

b. Sales amounts are: April (actual), $1,450,000, May (actual), $1,600,000, and June

(budgeted), $1,700,000.

c. Cost of goods sold is 53% of sales.

d. Budgeted cash disbursements for salaries in June: $260,000. Salaries payable on May 31

are $60,000 and are expected to be $50,000 on June 30.

e. Budgeted depreciation expense for June: $24,000.

f. Other cash expenses budgeted for June: $282,000.

g. Accrued income taxes due in June: $48,000.

h. Bank loan interest due in June: $8,000 which represents the 1% monthly expense on a bank

loan of $800,000.

i. The income tax rate applicable to the company is 30%.

187. Use the following information to prepare a budgeted balance sheet for Grover Company

for the month of June.

a. The budgeted net income for the month of June is $236,000.

b. The beginning cash balance is $62,000; total budgeted cash receipts are $1,660,000; total

budgeted cash disbursements are $1,580,000.

c. Budgeted sales for June are $1,700,000. Collections are 40% in the month of sale and 60%

in the month following.

d. The projected inventory balance is 10% of the following month’s sales. Sales for July are

projected to be $1,750,000.

e. Budgeted purchases for June are $900,000 to be paid 80% in the month of purchase and

20% in the month following.

f. The equipment account balance is $1,400,000 on May 31. No equipment purchases or

disposals were made during June. On May 31, the accumulated depreciation is $276,000.

Depreciation expense for June is estimated to be $24,000.

g. There is an outstanding loan balance of $800,000.

h. Accrued income taxes payable for June 30 are $71,000; and salaries payable are $50,000.

i. The only other balance sheet accounts are: Common Stock, with a balance of $800,000 on

May 31, and Retained Earnings with a balance of $300,000 on May 31. No additional

common stock was issued and no dividends were paid during June.

188. There are at least five benefits from budgeting. Identify two of these benefits:

(1) _______________________________________

(2) _______________________________________

189. Guidance for the budget process is usually supplied by a _____________________ of

department heads and other executives responsible for seeing that budgeted amounts are

realistic and coordinated.

190. A ________________________ is a continuously revised budget that adds future months

or quarters to replace months or quarters that have lapsed.

191. The master budget process nearly always begins with the preparation of the

___________________ and usually finishes with the preparation of the

______________________, the ________________, and the ______________________.

192. ___________________________ is a budget system based on expected activities and

their levels that enables management to plan for resources required to perform the activities.

193. The budget that lists the dollar amounts to be both received from plant asset disposals

and spent to purchase additional plant assets to carry out the budgeted business activities is

the __________________________.

194. The ___________ shows expected cash inflows and outflows during the budget period.

195. The ___________________________ , prepared by manufacturing firms, shows the

number of units to be produced in a period based on the unit sales projected in the sales

budget, along with inventory considerations.

196. The ___________________________ shows the budgeted costs for factory overhead