Chapter 17

Activity-Based Costing and Analysis

True / False Questions

1. In competitive markets, the price of a given product is established through the forces of supply

and demand.

2. Product costs consist of direct labor, direct materials, manufacturing overhead, and indirect

costs.

3. Distorted product cost information can result in poor decisions.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

4. The cost to heat a manufacturing facility can be directly linked to the number of units

produced.

5. Examples of volume-related measures include direct labor hours, direct labor cost dollars, and

machine hours.

6. Departments are the cost objects when the plantwide overhead rate method is used.

7. The plantwide overhead rate is determined by using volume-related measures.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

8. Data concerning volume-related measures are readily available in most manufacturing

settings.

9. The departmental overhead rate method uses a different overhead rate for each production

department.

10. By definition, costs classified as overhead are consumed in basically the same manner

regardless of the process involved.

11. Products are the first stage cost objects when using a departmental overhead rate method.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

12. The departmental overhead rate method allows each department to have its own overhead

rate and its own allocation base.

13. The premise of ABC is that it takes activities to make products and provide services and

these activities drive costs.

14. Activities are the cost objects of the second stage of ABC.

15. A cost pool is a collection of costs that are related to the same or similar activity.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

16. Activity-based costing first assigns costs to products and then uses these product costs to

assign costs to manufacturing activities.

17. Multiple cost pools are used when allocating overhead using the plantwide overhead rate

method.

18. Management’s pricing and cost decisions for a product are influenced by that product’s cost

assignments.

19. A major disadvantage of using a plantwide overhead rate is the extreme difficulty in

gathering the needed information.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

20. The usefulness of overhead allocations based on a plantwide overhead rate depends on two

crucial assumptions: (1) the overhead cost is correlated with the allocation base; and (2) all

products use overhead cost in dissimilar proportions.

21. Some companies allocate their overhead cost using a plantwide overhead rate largely because

of its simplicity.

22. Allocated overhead costs vary depending upon the allocation methods used.

23. When products differ in batch size and complexity, they usually consume different amounts

of overhead resources.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

24. Overhead costs are often affected by many issues and are frequently too complex to be

explained by any one factor.

25. Compared to the departmental overhead rate method, the plantwide overhead rate method

usually results in more accurate overhead allocations.

26. Because departmental overhead costs are allocated based on measures closely related to

production volume, they accurately assign overhead, such as utility costs.

27. The use of a plantwide overhead rate is not acceptable for external reporting under GAAP .

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

28. ABC allocates overhead costs to products based on input measures rather than output

measures .

29. ABC can be used to assign costs to any cost object that is of management interest.

30. ABC is significantly less costly to implement and maintain than more traditional overhead

costing systems.

31. When using the plantwide overhead rate method, total budgeted overhead costs are combined

into one overhead cost pool.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

32. Kinetic Company estimates that overhead costs for the next year will be $1,600,000 for

indirect labor and $400,000 for factory utilities. The company uses direct labor hours as its

overhead allocation base. If 50,000 direct labor hours are planned for this next year, then the

plantwide overhead rate is $.025 per direct labor hour.

33. A company estimates that costs for the next year will be $500,000 for indirect labor,

$50,000 for factory utilities, and $1,000,000 for the CEO’s salary. The company uses machine

hours as its overhead allocation base. If 25,000 machine hours are planned for this next year,

then the plantwide overhead rate is $22 per machine hour.

34. A company estimates total overhead costs for the next year to be $1,200,000 and wishes to

use direct labor hours as its overhead allocation base. This company makes two products: (1)

Fancy X , which requires three direct labor hours per unit, and (2) Plain X, which requires one

direct labor hour per unit. If the company plans to make 10,000 units of Fancy X and 10,000

units of Plain X, then each unit produced will be allocated the same amount of overhead.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

35. Malone has 33,000 total estimated direct labor hours for next year.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

36. Malone’s plantwide overhead rate will be $20.98 per direct labor hour next year.

37. If the direct labor time estimates are met, Malone will allocate $10.49 of overhead cost to

each unit of Little X.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

38. The first step in using the departmental overhead rate method requires that overhead be

traced to each of the company’s departments.

39. The departmental overhead rate method traces costs to each department and then determines

an allocation base for each department.

40. Turtle Company produces t-shirts that go through two operations, cutting and sewing, before

they are complete. Expected costs and activities for the two departments are shown below. Given

this information, the departmental overhead rate for the cutting department based on direct labor

hours is $2.69 per direct labor hour (rounded to two decimals).

Cutting Sewing

Direct labor hours 250,000

DLH

75,000 DLH

Machine hours 125,000

MH

150,000 MH

Overhead costs $500,000 $375,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

41. A company produces heating elements that go through two operations, casting and

assembling, before they are complete. Expected costs and activities for the two departments are

shown below. Given this information, the departmental overhead rate for the assembling

department based on direct labor hours is $5 per direct labor hour.

Casting Assembling

Direct labor hours 1,875 DLH 7,500 DLH

Machine hours 12,500 MH 3,750 MH

Overhead costs $75,000 $37,500

42. A company produces paint that goes through two operations, operation A and operation B,

before it is complete. Expected costs and activities for the two departments are shown below.

Given this information, the departmental overhead rate for Department B based on machine

hours is $4 per machine hour.

Department

A

Department

B

Machine hours 50,000 MH 60,000 MH

Direct labor hours 78,500 DLH 100,800 DLH

Overhead costs $392,500 $403,200

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

43. A company produces computer chips that go through two operations, operation A1 and

operation B2, before they are complete. Expected costs and activities for the two departments are

shown below. Departmental overhead rates are based on machine hours in department A1 and

direct labor hours in department B2. Therefore, the overhead rates for department A1 and

department B2 are $3.62 per machine hour and $5.73 per direct labor hour, respectively.

Department

A1

Department

B2

Machine hours 40,000 MH 30,000 MH

Direct labor hours 36,200 DLH 28,650 DLH

Overhead costs $144,800 $171,900

44. A company produces garden benches that go through two operations, operation 1A1 and

operation 2B2, before they are complete. Expected costs and activities for the two departments

are shown below. Both departments have departmental overhead rates based on machine hours.

Therefore, the overhead rates for department 1A1 and department 2B2 are the same.

Department

1A1

Department

2B2

Machine hours 70,000 MH 60,000 MH

Direct labor hours 56,350 DLH 50,160 DLH

Overhead costs $225,400 $250,800

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

45. A company produces surgical equipment that goes through threes processes, 1A1, 2B2, and

3C3, before they are complete. Expected costs and activities for the three departments are shown

below. All departments have departmental overhead rates based on direct labor hours. Therefore,

the overhead rate for each department is $5 per direct labor hour.

Department

1A1

Department

2B2

Department

3C3

Machine hours 15,000 MH 25,000 MH 20,000 MH

Direct labor hours 22,830 DLH 10,650 DLH 29,200 DLH

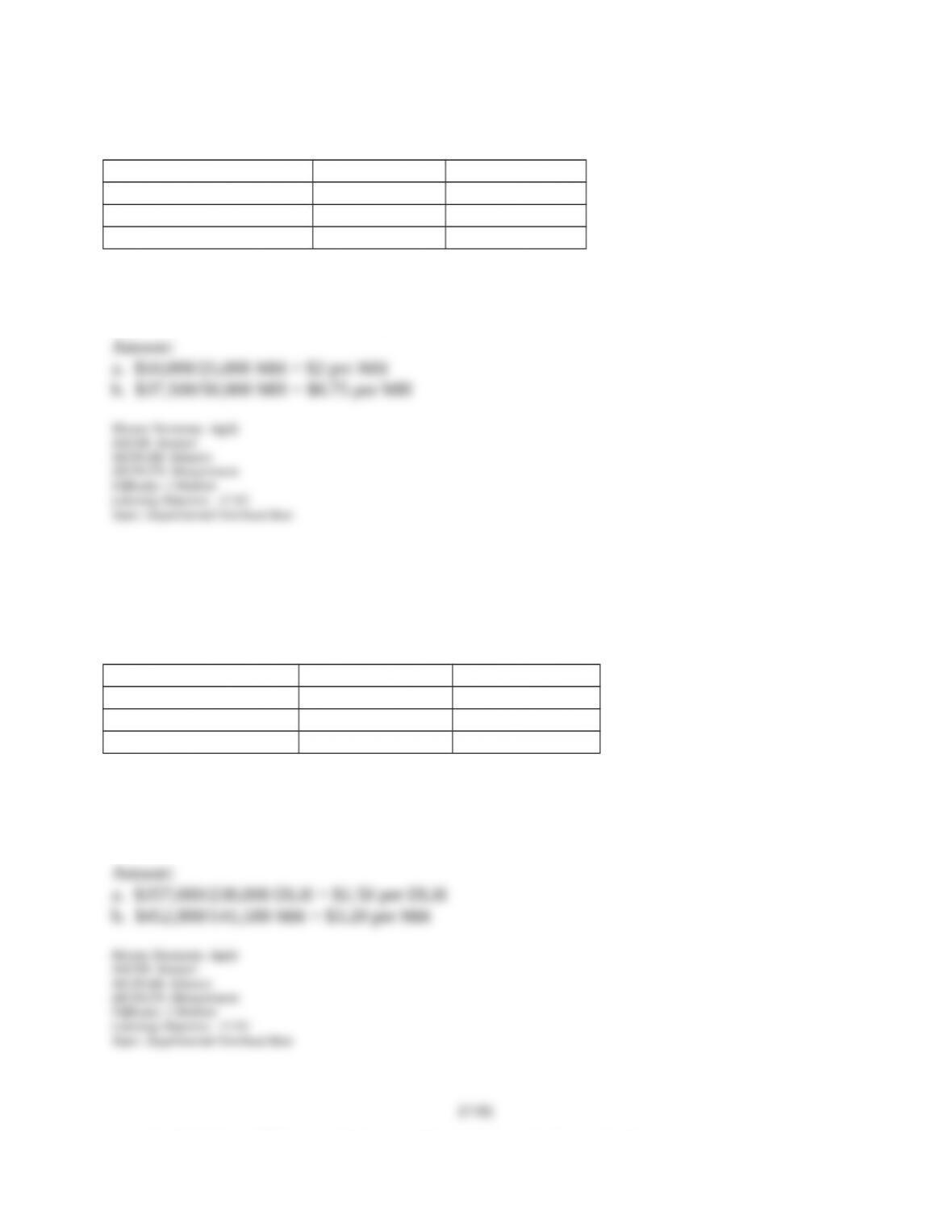

Overhead costs $114,150 $213,000 $73,000

46. Activity-based costing involves four steps: (1) identify activities and the costs they cause, (2)

group similar activities into cost pools, (3) determine an activity rate for each activity cost pool,

and (4) allocate overhead costs to products using those activity rates.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

47. The more activities tracked by activity-based costing, the more accurately overhead costs are

assigned.

48. In activity-based costing, an activity can involve several related tasks.

49. Activities causing overhead cost in an organization are typically separated into four levels:

(1) direct activities, (2) indirect activities, (3) batch level activities, and (4) facility level

activities.

50. Machine setup costs are an example of a batch level activity.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

51. Product design costs are an example of a unit level activity.

52. Facility level costs are not traceable to individual product lines, batches or units.

53. Activity-based costing eliminates the need for overhead allocation rates.

54. Activity-based costing often shifts overhead costs from large volume, standardized products

to low-volume, specialty products that consume disproportionate resources.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

55. The final step of activity-based costing assigns overhead costs to pools rather than to

products.

56. Batch level costs vary with the number of units produced.

57. Product level costs do not vary with the number of units or batches produced.

58. Facility level costs vary with the number of units or batches produced.

59. A quality-inspection cost is an example of unit-level costs.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-18

60. Plantwide overhead rates typically do a better job of matching each department’s overhead

costs to the products using the department’s resources than do departmental overhead rates.

61. Two big benefits of ABC costing are a) more accurate product cost information and b) more

detailed information on costs and the drivers of those costs.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

62. A method of assigning overhead costs to a product using a single overhead rate is:

A. Plantwide overhead rate method.

B. Cost pool overhead rate method.

C. Departmental overhead rate method.

D. Activity-based costing.

E. Overhead cost allocation method.

63. Which types of overhead allocation methods result in the use of more than one overhead rate

during the same time period?

A. Plantwide overhead rate method and departmental overhead rate method.

B. Cost pool overhead rate method and plantwide overhead rate method.

C. Departmental overhead rate method and activity-based costing.

D. Activity-based costing and plantwide overhead rate method.

E. Departmental overhead rate method and cost pool overhead rate method.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

64. Which of the following would not be considered a product cost?

A. Direct labor costs.

B. Factory supervisor’s salary.

C. Factory line worker’s salary.

D. Cost accountant’s salary.

E. Manufacturing overhead costs.

65. Overhead costs:

A. Are directly related to production.

B. Can be traced to units of product in the same way that direct materials can.

C. Cannot be traced to units of product in the same way that direct labor can.

D. Are period costs.

E. Include only fixed costs.

66. The cost object of the plantwide overhead rate method is:

A. The unit of product.

B. The production departments of the company.

C. The production activities of the company.

D. Manufacturing cost pools.

E. the time period.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

67. Which of the following statements is true with regard to the plantwide overhead rate method?

A. The rate is determined using volume-related measures.

B. It is logical to use this method when overhead costs are not closely tied to volume-related

measures.

C. This method uses multiple overhead rates.

D. The rate is determined using measures that are not closely related to volume.

E. The method provides the most accurate means of allocating overhead costs.

68. The cost object(s) of the departmental overhead rate method is:

A. The unit of product.

B. The production departments of the company.

C. The production departments in the first stage and the unit of product in the second stage.

D. The unit of product in the first stage and the production departments in the second stage.

E. The production activities of the company.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

69. Which of the following statements is true with regard to the departmental overhead rate

method?

A. It is logical to use this method when overhead resources are consumed by various products in

substantially the same way throughout multiple departments.

B. It is logical to use this method when overhead resources are consumed by various products in

substantially different ways throughout multiple departments.

C. Each department has the same rate for the same activity pool.

D. It requires one overhead cost pool and one rate.

E. It is synonymous with activity-based costing.

70. The cost object(s) of the activity-based costing method is(are):

A. The unit of product.

B. The production departments of the company.

C. The production activities of the company.

D. The production activities in the first stage and the unit of product in the second stage.

E. The unit of product in the first stage and the production activities in the second stage.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

71. From an ABC perspective, what causes costs to be incurred?

A. Financial transactions.

B. The volume of units produced.

C. Debits and credits.

D. Management decisions.

E. Activities.

72. Which of the following statements is true with regard to activity-based costing rates?

A. The premise of ABC is that activities are what cause costs to be incurred.

B. ABC is another way to refer to a multiple departmental rate situation.

C. There one basic stage to ABC.

D. ABC is simpler and less expensive to implement than other traditional methods of allocating

overhead costs.

E. All cost drivers used to determine the rates will be unit-level drivers.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

73. What is the reason for pooling costs?

A. To shift costs from low-volume to high-volume products.

B. It is a budgeting technique designed to accurately track fixed costs.

C. Determining a pool rate for all costs incurred by the same activity reduces the number of cost

assignments required.

D. This procedure helps to determine which costs are directly related to production volume.

E. It simplifies departmental overhead costing procedures.

74. Which of the following are advantages of using the plantwide overhead rate method?

A. The use of cost pools is considerably more accurate than other overhead allocations.

B. The necessary information is readily available.

C. It is more accurate than traditional overhead allocations.

D. Each department has its own overhead rate and its own allocation base.

E. It takes into account that when products differ in batch size and complexity, they usually

consume different amounts of overhead resources.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

75. Which of the following companies would be best served by a plantwide overhead rate?

A. A company that manufactures many different products and whose operations are an equal

mix of labor and mechanized work.

B. A company that manufactures few products and whose operations are labor intensive.

C. A company that manufactures many different products and whose operations are highly

mechanized.

D. A company whose products use overhead resources in very different ways.

E. A company whose products differ in batch size and complexity and consume different

amounts of overhead resources.

76. Which of the following is true?

A. Overhead costs are often affected by many issues and are frequently too complex to be

explained by any one factor.

B. The departmental overhead rate is not usually based on measures closely related to

production volume.

C. The departmental overhead rate is most accurate in assigning overhead costs that are not

driven by production volume.

D. Allocated overhead costs will be the same no matter which allocation method is used.

E. When cost analysts are able to logically trace cost objects to costs, costing accuracy is

improved.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

77. Which of the following is a disadvantage of the departmental overhead rate method?

A. The departmental overhead rate method assigns overhead on the basis of volume-related

measures.

B. The departmental overhead rate method is more refined than the plantwide overhead rate

method.

C. The departmental overhead rate method does not assign overhead on the basis of volume-

related measures.

D. The departmental overhead rate method is simpler and less costly to implement than the

plantwide rate method.

E. There are no disadvantages of the departmental overhead rate method.

78. Which of the following is not true?

A. The departmental overhead method assigns overhead on the basis of volume-related

measures.

B. The departmental overhead rate method is more refined than the plantwide overhead rate

method.

C. Overhead costing accuracy is improved by the use of multiple departmental rates rather than

a single overhead rate.

D. The departmental overhead rate method does not assign overhead on the basis of volume-

related measures.

E. The departmental overhead rate method is more costly to implement than the traditional

overhead rate method.

79. What are three advantages of activity-based costing over traditional volume-based allocation

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-27

methods?

A. Ease of use, more accurate product costing, and more effective cost control.

B. Fewer allocation bases, ease of use, and a direct correlation to production volume.

C. More accurate product costing, more effective cost control, and better focus on the relevant

factors for decision making.

D. More accurate product costing, fewer cost objects, and a direct correlation to production

volume.

E. More accurate product costing, ease of use, less costly to implement.

80. What are the main advantages of traditional volume-based allocation methods compared to

activity-based costing?

A. Traditional volume-based methods are easier to use and less costly to implement and

maintain.

B. Traditional volume-based methods are more accurate and allowed by GAAP.

C. Traditional volume-based methods are less accurate and easier to use.

D. Traditional volume-based methods are harder to use and more costly to implement and

maintain.

E. There are no advantages to using traditional volume-based methods.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

81. K Company estimates that overhead costs for the next year will be $2,900,000 for indirect

labor and $800,000 for factory utilities. The company uses direct labor hours as its overhead

allocation base. If 80,000 direct labor hours are planned for this next year, what is the company’s

plantwide overhead rate?

A. $.02 per direct labor hour.

B. $46.25 per direct labor hour.

C. $36.25 per direct labor hour.

D. $10 per direct labor hour.

E. $.10 per direct labor hour.

82. Peterson Company estimates that overhead costs for the next year will be $6,520,000 for

indirect labor and $550,000 for factory utilities. The company uses machine hours as its

overhead allocation base. If 140,000 machine hours are planned for this next year, what is the

company’s plantwide overhead rate?

A. $.02147 per machine hour.

B. $50.50 per machine hour.

C. $45.75 per machine hour.

D. $3.9286 per machine hour.

E. $.2545 per machine hour.

83. A company estimates that overhead costs for the next year will be $8,320,000 for indirect

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-29

labor and $155,500 for factory utilities. The company uses machine hours as its overhead

allocation base. If 400,000 machine hours are planned for this next year, what is the company’s

plantwide overhead rate? (Round to two decimal places)

A. $0.05 per machine hour.

B. $ 21.19 per machine hour.

C. $ 20.80 per machine hour.

D. $0.39 per machine hour.

E. $2.57 per machine hour.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

84. The following data relates to Spurrier Company’s estimated amounts for next year.

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$1,100,000 $3,300,000

Direct labor hours 540,000 DLH 790,000 DLH

Machine hours 90,000 MH 24,000 MH

What is the company’s plantwide overhead rate if direct labor hours are the allocation base?

(Round to two decimal places)

A. $3.31 per direct labor hour.

B. $3.43 per direct labor hour.

C. $2.04 per direct labor hour.

D. $.30 per direct labor hour.

E. $.50 per direct labor hour.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

85. The following data relates to Black-Out Company’s estimated amounts for next year.

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$300,000 $400,000

Direct labor hours 60,000 DLH 80,000 DLH

Machine hours 1,000 MH 2,000 MH

What is the company’s plantwide overhead rate if machine hours are the allocation base?

(Round to two decimal places.)

A. $233.33 per MH

B. $150.00 per MH

C. $100.00 per MH

D. $4.90 per MH

E. $5.00 per MH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

86. The following data relates to Patterson Company’s estimated amounts for next year.

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$50,000 $60,000

Direct labor hours 180,000 DLH 200,000 DLH

Machine hours 200,000 MH 400,000 MH

What is the company’s plantwide overhead rate if direct labor hours are the allocation base?

(Round to two decimal places.)

A. $3.45 per DLH

B. $5.45 per DLH

C. $0.29 per DLH

D. $0.26 per DLHE. $0.20 per DLH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

87. Lake Erie Company uses a plantwide overhead rate with machine hours as the allocation

base. Next year, 600,000 units are expected to be produced taking .75 machine hours each. How

much overhead will be assigned to each unit produced given the following estimated amounts?

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$3,107,500 $1,520,000

Direct labor hours 150,000 DLH 250,000 DLH

Machine hours 250,000 MH 175,000 MH

A. $11.57 per unit

B. $8.17 per unit

C. $5.61 per unit

D. $12.43 per unit

E. $10.89 per unit

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

88. Red Raider Company uses a plantwide overhead rate with direct labor hours as the

allocation base. Next year, 400,000 units are expected to be produced taking .90 direct-labor

hours each. How much overhead will be assigned to each unit produced given the following

estimated amounts?

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$2,530,000 $900,000

Direct labor hours 168,000 DLH 110,000 DLH

Machine hours 30,000 MH 8,000 MH

A. $63.95 per unit

B. $11.11 per unit

C. $15.06 per unit

D. $7.32 per unit

E. $12.34 per unit

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

89. Western Company allocates $10.00 overhead to each unit produced. The company uses a

plantwide overhead rate with machine hours as the allocation base. Given the amounts below,

how many machine hours does the company expect in department 2?

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$250,000 $150,000

Direct labor hours 8,000 DLH 12,000 DLH

Machine hours 15,000 MH ? MH

A. 33,000 MH

B. 137,500 MH

C. 82,500 MH

D. 88,000 MH

E. 25,000 MH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

90. A company allocates $7.50 overhead to each unit produced. The company uses a plantwide

overhead rate with direct labor hours as the allocation base. Given the amounts below, how many

direct labor hours does the company expect in department 2?

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$74,358 $49,572

Direct labor hours 6,610 DLH ? DLH

Machine hours 700 MH 800 MH

A. 9,914 DLH

B. 6,612 DLH

C. 3,109 DLH

D. 7,454 DLH

E. 16,254 DLH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

91. Gray Company uses a plantwide overhead rate with machine hours as the allocation base.

Use the following information to solve for the amount of machine hours estimated per unit of

product Q.

Direct material cost per unit of Q $15

Total estimated manufacturing overhead $100,000

Total cost per unit of Q $60

Total estimated machine hours 200,000

MH

Direct labor cost per unit of Q $30

A. 50 MH per unit of Q.

B. .50 MH per unit of Q.

C. .75 MH per unit of Q.

D. 17.5 MH per unit of Q.

E. 30 MH per unit of Q.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

92. Gold Company uses a plantwide overhead rate with machine hours as the allocation base.

Use the following information to solve for the amount of machine hours estimated per unit of

product RST.

Direct material cost per unit of RST $15

Total estimated manufacturing overhead $300,000

Total cost per unit of RST $80

Total estimated machine hours 150,000

MH

Direct labor cost per unit of RST $23

A. 21 MH per unit of RST.

B. 2 MH per unit of RST.

C. 20 MH per unit of RST.

D. 37.5 MH per unit of RST.

E. 38 MH per unit of RST.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

93. Bond Company uses a plantwide overhead rate with direct labor hours as the allocation base. Use the following

information to solve for the amount of direct labor hours estimated per unit of product G2.

Direct material cost per unit of G2 $7

Total estimated manufacturing overhead $787,500

Total cost per unit of G2 $22

Total estimated direct labor hours 450,000

DLH

Direct labor cost per unit of G2 $4.25

A. 1.75 DLH per unit of G2.

B. 6.14 DLH per unit of G2.

C. 9.3 DLH per unit of G2.

D. .66 DLH per unit of G2.

E. 11.25 DLH per unit of G2.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

94. Kamper Company sells two products Big Z and Little Z. Current direct

material and direct labor costs are detailed below. Next year, the company

wishes to use a plantwide overhead rate with direct labor hours as its

allocation base. Next year’s overhead is estimated to be $475,000. The

direct labor and direct materials costs are estimated to be consistent with

the current year. Direct labor costs $20 per hour and the company expects to

manufacture 32,000 units of Big Z and 9,000 units of Little Z next year.

Direct

Material

per Unit

Direct

Labor Dollars

per Unit

Big Z $6 $17

Little Z $12 $8

What are total estimated direct labor hours for this next year?

A. 30,800 total DLH.

B. 616,000 total DLH.

C. 300,000 total DLH.

D. 1,025,000 total DLH.

E. 916,000 total DLH.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

95. Crinkle Cut Clothes Company manufactures two products CC1 and CC2.

Current direct material and direct labor costs are detailed below. Next year

the company wishes to use a plantwide overhead rate with direct labor hours

as its allocation base. Next year’s overhead is estimated to be $338,250. The

direct labor and direct materials costs are estimated to be consistent with

the current year. Direct labor costs $28 per hour and the company expects to

manufacture 22,000 units of CC1 and 91,000 units of CC2 next year.

Direct

Material

per Unit

Direct

Labor Dollars

per Unit

CC1 $37.10 $22.40

CC2 $25.20 $15.40

Compute the plantwide overhead rate for next year.

A. $28.00 per DLH.

B. $37.80 per DLH.

C. $1.35 per DLH.

D. $5.00 per DLH.

E. $.20 per DLH.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

96. Compute Aztec’s departmental overhead rate for the mixing department based on direct labor

hours.

A. $1.50 per DLH.

B. $5.00 per DLH.

C. $0.75 per DLH.

D. $0.50 per DLH.

E. $2.08 per DLH.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

97. Compute Aztec’s departmental overhead rate for the mixing department based on machine

hours.

A. $1.50 per MH.

B. $5.00 per MH.

C. $0.75 per MH.

D. $0.50 per MH.

E. $2.08 per MH.

98. Compute Aztec’s departmental overhead rate for the baking department based on direct labor

hours.

A. $1.50 per DLH

B. $5.00 per DLH

C. $0.75 per DLH

D. $0.50 per DLH

E. $2.08 per DLH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

99. Compute Aztec’s departmental overhead rate for the baking department based on machine

hours.

A. $1.50 per MH

B. $5.00 per MH

C. $0.75 per MH

D. $0.50 per MH

E. $2.08 per MH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

100. Tarnish Industries uses departmental overhead rates and is planning on a $2 per direct labor

hour overhead rate for the molding department. Compute the estimated manufacturing overhead

cost for the molding department given the information shown in the table.

A. $225,000

B. $196,000

C. $150,000

D. $321,000

E. $471,000

101. Tarnish Industries uses departmental overhead rates and is planning on a $1.80 per direct

labor hour overhead rate for the finishing department. Compute the estimated manufacturing

overhead cost for the finishing department given the information shown in the table.

A. $41,667

B. $288,900

C. $256,800

D. $146,700

E. $323,100

102. Tarnish Industries uses departmental overhead rates and is planning on a $2 per machine

hour overhead rate for the molding department. Compute the estimated manufacturing overhead

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-46

cost for the molding department given the information shown in the table.

A. $195,000

B. $196,000

C. $163,000

D. $321,000

E. $471,000

103. Tarnish Industries uses departmental overhead rates and is planning on a $4.10 per

machine hour overhead rate for the finishing department. Compute the estimated manufacturing

overhead cost for the finishing department given the information shown in the table.

A. $307,500

B. $658,050

C. $401,800

D. $334,150

E. $735,950

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

costs

104. Use the data for Wall Nuts, Inc. to compute departmental overhead rates based on machine

hours in Department A and machine hours in Department B.

A. $4.50 per MH in Dept A; $4.50 per MH in Dept B.

B. $7.50 per MH in Dept A; $7.50 per MH in Dept. B.

C. $4.50 per MH in Dept A; $7.50 per MH in Dept B.

D. $2.70 per MH in Dept A; $6.00 per MH in Dept B.

E. $0.60 per MH in Dept A; $0.80 per MH in Dept B.

105. Use the data for Wall Nuts, Inc. to compute the dollar amount of overhead applied to each

unit of oak paneling, assuming the company uses departmental overhead rates based on machine

hours in Department A and machine hours in Department B.

A. $8.70

B. $1.40

C. $14.40

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-48

D. $26.25

E. $41.00

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

106. Use the above data for Wall Nuts, Inc. to compute the total manufacturing cost per unit of

oak paneling assuming the company uses departmental overhead rates based on machine hours in

Department A and machine hours in Department B.

A. $8.70

B. $18.20

C. $21.95

D. $27.30

E. $36.00

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

107. Aurora Corporation produces outdoor security lighting products. All products go through

three processes before completion. Use the expected overhead costs and related data shown

below to compute departmental overhead rates based on machine hours in Department A1A;

based on direct labor hours in Department B2B; and machine hours in Department C3C.

Department

A1A

Department

B2B

Department

C3C

Direct labor hours 90,000 DLH 80,000 DLH 72,000 DLH

Machine hours 54,000 MH 32,000 MH 54,000 MH

Manufacturing overhead

costs

$540,000 $160,000 $216,000

A. Dept. A: $10 per MH; Dept B: $2 per DLH; Dept C: $4 per MH.

B. Dept. A: $6 per MH; Dept B: $5 per DLH; Dept C: $3 per MH.

C. Dept. A: $10 per MH; Dept B: $5 per DLH; Dept C: $4 per MH.

D. Dept. A: $6 per MH; Dept B: $5 per DLH; Dept C: $4 per MH.

E. Dept. A: $10 per MH; Dept B: $2 per DLH; Dept C: $3 per MH.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

108. Consider the following activities that take place in a veterinary clinic.

(a.) Cleaning cages.

(b.) Heating and air conditioning the clinic.

(c.) Sending blood work to a lab.

(d.) Dispensing medicine.

Which of the following statements is true?

A. Service entities cannot use ABC for overhead allocation.

B. Cleaning cages is a facility level activity.

C. Dispensing medicine is a facility level activity.

D. Heating and air conditioning the clinic is a facility level activity.

E. Sending blood work to a lab is a facility level activity.

109. Consider the following activities that take place in a medical clinic.

(a.) Cleaning exam rooms.

(b.) Heating and air conditioning the clinic.

(c.) Sending blood work to a lab.

(d.) Dispensing medicine.

Which of the following statements is true?

A. Cleaning rooms and heating the clinic are both unit level activities.

B. Sending blood work to the lab is a batch level activity.

C. Sending blood work and dispensing medicine are both batch level activities.

D. Cleaning rooms and dispensing medication are both product or service level activities.

E. Heating the clinic and dispensing medication are both batch level activities.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

110. All of the following are examples of facility sustaining costs except:

A. Costs of cleaning the workplace.

B. Costs of custodial work.

C. Costs of personnel support.

D. Costs of sampling product quality.

E. Costs of employee recreational facilities.

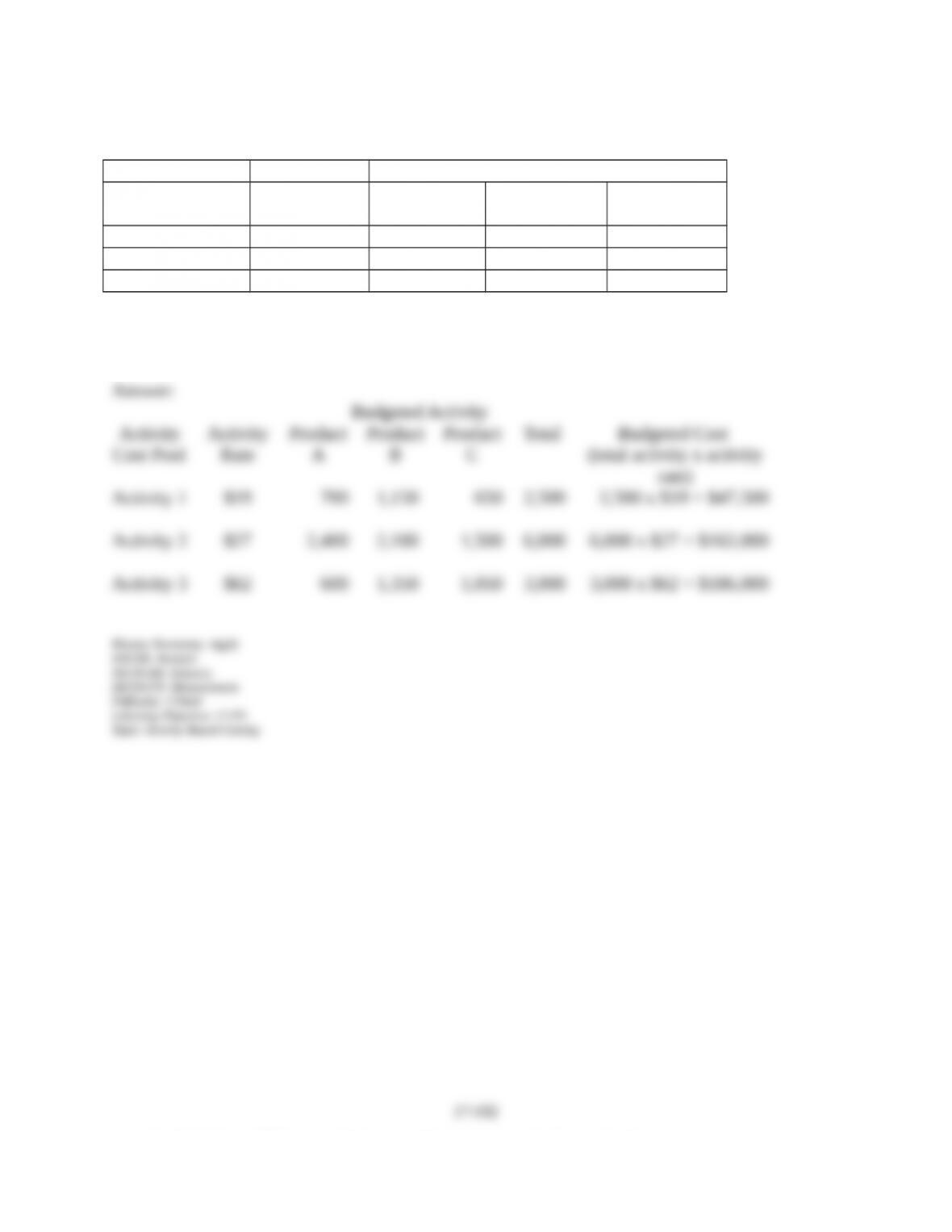

111. A company uses activity-based costing to determine the costs of its three products: A, B,

and C. The budgeted cost and activity for each of the company’s three activity cost pools are

shown in the following table:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A Product B Product C

Activity 1 $70,000 6,000 9,000 20,000

Activity 2 $45,000 7,000 15,000 8,000

Activity 3 $82,000 2,500 1,000 1,625

Which of the following statements is true regarding this company’s activity rates?

A. The activity rate under the activity-based costing system for Activity 2 is

$2.00.

B. The activity rate under the activity-based costing system for Activity 2 is $16.00.

C. The activity rate under the activity-based costing system for Activity 2 is $1.50.

D. The activity rate under the activity-based costing system for Activity 2 is $19.50.

E. The activity rate under the activity-based costing system for Activity 2 is $2.81.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

112. A company uses activity-based costing to determine the costs of its three products: A, B,

and C. The budgeted cost and activity for each of the company’s three activity cost pools are

shown in the following table:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A Product B Product C

Activity 1 $70,000 6,000 9,000 20,000

Activity 2 $45,000 7,000 15,000 8,000

Activity 3 $82,000 2,500 1,000 1,625

What are the activity rates for the three activities under activity based costing?

A. (1) $2.00; (2) $3.00; (3) $3.50.

B. (1) $3.50; (2) $1.50; (3) $32,80.

C. (1) $3.50; (2) $3.00; (3) $16.00.

D. (1) $2.00; (2) $1.50; (3) $16.00.

E. (1) $2.00; (2) $1.50; (3) $32.80.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

113. A company uses activity-based costing to determine the costs of its three products: A, B and

C. The budgeted cost and activity for each of the company’s three activity cost pools are shown

in the following table:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A Product B Product C

Activity 1 $70,000 6,000 9,000 20,000

Activity 2 $45,000 7,000 15,000 8,000

Activity 3 $82,000 2,500 1,000 1,625

How much overhead will be assigned to Product B using activity-based costing?

A. $56,500

B. $78,000

C. $62,500

D. $197,000

E. $70,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

114. A company has two products: A and B. It uses activity-based costing and has prepared the

following analysis showing budgeted cost and activity for each of its three activity cost pools:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A Product B

Activity 1 $87,000 3,000 2,800

Activity 2 $62,000 4,500 5,500

Activity 3 $93,000 2,500 5,250

Annual production and sales level of Product A is 34,300 units, and the annual production and

sales level of Product B is 69,550 units. What is the approximate overhead cost per unit of

Product B under activity-based costing?

A. $3.00

B. $2.00

C. $10.28

D. $15.00

E. $2.33

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

115. A company has two products: A and B. It uses activity-based costing and has prepared the

following analysis showing budgeted cost and activity for each of its three activity cost pools:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A Product B

Activity 1 $87,000 3,000 2,800

Activity 2 $62,000 4,500 5,500

Activity 3 $93,000 2,500 5,250

Annual production and sales level of Product A is 34,300 units, and the annual production and

sales level of Product B is 69,550 units. What is the approximate overhead cost per unit of

Product A under activity-based costing?

A. $3.00

B. $2.00

C. $10.28

D. $15.00

E. $2.33

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

116. A company has two products: A1 and B2. It uses activity-based costing and has prepared the

following analysis showing budgeted cost and activity for each of its three activity cost pools:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A1 Product B2

Activity 1 $48,000 1,200 4,800

Activity 2 $63,000 2,240 4,760

Activity 3 $80,000 7,200 800

Annual production and sales level of Product A1 is 8,480 units, and the annual production and

sales level of Product B2 is 22,310 units. What is the approximate overhead cost per unit of

Product A1 under activity-based costing?

A. $8.00

B. $9.00

C. $10.00

D. $12.00

E. $4.00

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

117. A company has two products: A1 and B2. It uses activity-based costing and has prepared the

following analysis showing budgeted cost and activity for each of its three activity cost pools:

Budgeted Activity

Activity Cost

Pool

Budgeted

Cost Product A1 Product B2

Activity 1 $48,000 1,200 4,800

Activity 2 $63,000 2,240 4,760

Activity 3 $80,000 7,200 800

Annual production and sales level of Product A1 is 8,480 units, and the annual production and

sales level of Product B2 is 22,310 units. What is the approximate overhead cost per unit of

Product B2 under activity-based costing?

A. $8.00

B. $9.00

C. $10.00

D. $12.00

E. $4.00

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

118. Refer to the data above. What are the overhead rates used to apply material handling (MH)

and storage costs (SC. using activity-based costing?

A. MH $300/batch; SC $2.73/unit.

B. MH $300/batch; SC $.20/lb.

C. MH $525/batch; SC $.205/unit.

D. MH $700/batch; SC $.205/lb.

E. MH $700/batch; SC $8.20/lb.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

119. Refer to the data in the preceding tables. How much overhead cost will be assigned to each

product line using activity-based costing (ABC.?

A. Dog food: $462,500; cat food: $462,500.

B. Dog food: $860,000; cat food: $65,000.

C. Dog food: $60,000; cat food: $45,000.

D. Dog food: $800,000; cat food: $20,000.

E. Dog food: $320; cat food: $320.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

120. Refer to the data above. How much overhead cost will be assigned to each unit of product

using activity-based costing (ABC.?

A. Dog food: $4.62; cat food: $4.62.

B. Dog food: $2.64; cat food: $2.64.

C. Dog food: $8.60; cat food: $0.33.

D. Dog food: $0.26; cat food: $8.60.

E. Dog food: $0.12; cat food: $3.85.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

121. Refer to the data in the preceding tables. How much overhead cost will be assigned to the

ice cream sandwich product line using activity-based costing (ABC.?

A. $340,000

B. $368,000

C. $28,000

D. $850.08

E. $433,682

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

122. Refer to the data above. How much overhead cost will be assigned to the dessert bar

product line using activity-based costing (ABC.?

A. 340,750

B. $247,818

C. $16,000

D. $297,500

E. $313,500

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

123. A company identified the following partial list of activities, costs, and activity drivers

expected for the next year:

Activity Expected Costs Cost Driver

Extrusion costs $83,600 Number batches made

Handling costs $8,800 Number of orders filled

Packaging costs $40,500 Number of units made

Product A Product B

Production volume 750,000 units 600,000 units

Batches made 200 batches 750 batches

Orders filled 75 200

Calculate activity rates for each of the three activities using activity-based costing (ABC).

A. Extrusion: $304 per batch; handling: $32 per unit; packaging: $.03 per unit.

B. Extrusion: $88 per batch; handling: $32 per order; packaging: $.03 per unit.

C. Extrusion: $88 per order; handling: $32 per unit; packaging: $.03 per batch.

D. Extrusion: $418 per batch; handling: $117.33 per order; packaging: $.054 per unit.

E. Extrusion: $118.13 per batch; handling: $44 per order; packaging: $.0675 per unit.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

124. A company identified the following partial list of activities, costs, and activity drivers

expected for the next year:

Activity Expected Costs Cost Driver

Extrusion costs $83,600 Number batches made

Handling costs $8,800 Number of orders filled

Packaging costs $40,500 Number of units made

Product A Product B

Production volume 750,000 units 600,000 units

Batches made 200 batches 750 batches

Orders filled 75 200

How much overhead in total will be assigned to the Product A line using activity based costing?

A. $42,500.

B. $132,900.

C. $90,400.

D. $66,000.

E. $66,450.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

125. Which of the following would not be considered a product cost?

A. Direct material costs.

B. Factory supervisor’s salary.

C. Direct labor costs.

D. Budget accountant’s salary.

E. Manufacturing overhead costs.

126. The use of which of the following costing systems is most likely to reduce over- or

undercosting, and keep it to a minimum?

A. Departmental overhead allocation rates

B. Plantwide overhead rate

C. Activity-based costing

D. Traditional costing system

127. Which of the following statements is true of activity-based costing?

A. ABC ignores the allocation of marketing costs.

B. ABC classifies some indirect costs as direct costs.

C. ABC is more likely to result in big differences from a traditional costing system if the

business makes only one product rather than multiple products.

D. Activities are the cost objects of the second stage of ABC.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

128. ABC assumes all costs are ________ because over the long run the company can adjust the

amount of assets utilized.

A. variable

B. fixed

C. direct

D. nondiscretionary

E. committed

129. Put the following ABC implementation steps in order ________.

A Use the activity overhead rates to assign overhead costs to cost objects.

B Compute the allocation rates.

C Trace overhead costs to cost pools.

D Identify the activities and the overhead costs they cause.

A. DACB

B. DBCA

C. BADC

D. CDAB

E. DCBA

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

130. ________ is considered while choosing a cost allocation base for activity costs in ABC

costing.

A. The marketing strategy of the products being produced

B. The product sales price

C. The availability of reliable data and metrics

D. The number of employees in direct labor

131. Would the following activities at a manufacturer of shampoo be best classified as unit-level,

batch-level, product-level, or facility level activities?

Researching new formulas Shipping orders to stores

A. Batch Batch

B. Unit Unit

C. Product Batch

D. Product Unit

A. Choice A

B. Choice B

C. Choice C

D. Choice D

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

132. All of the following are examples of facility level costs except:

A. Costs of cleaning the workplace.

B. Costs of custodial work.

C. Costs of personnel support.

D. Costs of receiving shipments.

E. Costs of providing electricity.

133. _____________ costs support the company as a whole.

A. Batch-level

B. Product-level

C. Unit-level

D. Facility-level

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

134. Which of the following is a disadvantage of the departmental overhead rate method?

A) It may fail to accurately assign many overhead costs that are not driven by production

volume.

B) Allows each department to have its own overhead rate.

C) Allows each department to have its own allocation base.

D) The departmental overhead rate is usually more accurate in overhead allocations than the

plantwide overhead rate.

135. The use of departmental overhead rates will generally result in:

A) The use of a single cost allocation base

B) The use of a single overhead cost pool for the shop

C) The use of a separate cost allocation base for each department in the shop

D) The use of a separate cost allocation base for each activity in the shop

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

136. ABC systems ________.

A. usually will undercost complicated or complex products

B. will limit cost drivers to units of output

C. highlight the different levels of activities

D. will allocate costs based on the overall level of activity

137. ABC costing might lead to:

A. increasing the sales price of low-volume products

B. increasing the sales price of high-volume products

C. increasing low-volume products that appear to be profitable

D. decreasing high-volume products that appear to be unprofitable

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

138. Costs incurred in detecting poor quality products are referred to as:

A. appraisal costs

B. external failure costs

C. internal failure costs

D. prevention costs

139. West Company estimates that overhead costs for the next year will be $5,240,000 for

indirect labor and $550,000 for factory utilities. The company uses machine hours as its

overhead allocation base. If 150,000 machine hours are planned for this next year, what is the

company’s plantwide overhead rate?

A. $.0259 per machine hour.

B. $34.93 per machine hour.

C. $38.60 per machine hour.

D. $3.67 per machine hour.

E. $.2727 per machine hour.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

140. The following data relates to Mangini Company’s estimated amounts for next year.

Estimated: Department 1 Department 2

Manufacturing overhead

costs

$320,000 $400,000

Direct labor hours 65,000 DLH 75,000 DLH

Machine hours 2,000 MH 2,500 MH

What is the company’s plantwide overhead rate if machine hours are the allocation base?

(Round to two decimal places.)

A. $200.00 per MH

B. $150.00 per MH

C. $160.00 per MH

D. $31.11 per MH

E. $5.14 per MH

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

141. Compute Tasty’s departmental overhead rate for the mixing department based on direct

labor hours.

A. $1.50 per DLH.

B. $5.00 per DLH.

C. $0.75 per DLH.

D. $0.60 per DLH.

E. $1.67 per DLH.

142. Compute Tasty’s departmental overhead rate for the mixing department based on machine

hours.

A. $1.50 per MH.

B. $3.33 per MH.

C. $0.60 per MH.

D. $0.50 per MH.

E. $2.00 per MH.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

143. When calculating the departmental overhead rate, the numerator should be?

A) The total estimated departmental overhead cost

B) The total amount of departmental allocation base

C) The total budgeted overhead cost

D) The actual quantity of the departmental allocation base used by the job

144. Cleveland Choppers manufactures two types of motorcycles, a Base and a Loaded model. The following

activity and costs have been gathered:

Number of Number of Number of

Product Components Setups Direct Labor Hrs

Base 15 20 700

Loaded 25 40 600

Overhead costs $27,000 $22,500

The number of components and number of setups are chosen as activity-cost drivers for

overhead. Assuming an ABC costing system is being used, what is the total overhead cost

assigned to the Base model?

A) $15,450

B) $21,375

C) $13,500

D) $17,625

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

145. The number of components and number of setups are chosen as activity-cost drivers for

overhead. Assuming an ABC costing system is being used, what is the total overhead cost

assigned to the Loaded model?

A) $31,875

B) $36,000

C) $28,125

D) $34,050

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

146. Match each of the following terms a through j with the appropriate definitions 1 through 10.

(a) Cost object

(b) Activity

(c) Cost driver

(d) Activity-based costing

(e) Batch level activities

(f) Activity-based management

(g) Pool rate

(h) Activity cost driver

(i) Activity driver

(j) Cost pool

_____ (1) A measure of activity level.

_____ (2) Actions which cause resources to be used.

_____ (3) A collection of costs that are related to the same or similar activity.

_____ (4) An outgrowth of ABC that draws on the link between activities and cost incurrence

for better management.

_____ (5) The target of a cost assignment.

_____ (6) Actions performed only on groups of units.

_____ (7) Variable that causes an activity’s cost to go up or down.

_____ (8) An allocation rate used to assign a collection of related costs to a cost object.

_____ (9) A cost allocation method that focuses on activities performed.

_____(10) Variable that causes a cost to go up or down.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

147. Identify each of the following activities as unit level (U), batch level (B., product level (P),

or facility level (F) to indicate the way each is incurred with respect to production.

_____ (1) Providing electricity

_____ (2) Sampling product quality

_____ (3) Cutting parts

_____ (4) Receiving shipments

_____ (5) Organizing production

_____ (6) Printing checks

_____ (7) Providing personnel support

_____ (8) Calibrating machines

_____ (9) Cleaning workplace

_____ (10) Assembling components

148. Direct labor, direct materials, and manufacturing overhead are all product costs. Why is

overhead more difficult to account for than either direct labor or direct materials?

149. Name and briefly describe three overhead rate methods.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-79

150. Explain cost flows for the plantwide overhead rate method.

151. Explain cost flows for the departmental overhead rate method.

152. Explain cost flows for activity-based costing.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-80

153. What is the basic principle underlying activity-based costing?

154. How does ABC differ from using multiple departmental rates?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

155. What are the major advantages of using a plantwide overhead rate?

156. Explain some of the disadvantages of the departmental overhead rate method.

157. Why is overhead allocation under ABC usually more accurate than either the plantwide

overhead allocation method or the departmental overhead allocation method?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

158. Identify and explain the four control levels associated with activity-based costing.

159. A company estimates that overhead costs for the next year will be $7,200,000 for indirect

labor, $400,000 for factory utilities, and $43,000 for depreciation on factory machinery. The

company uses direct labor hours as its overhead allocation base. If 955,375 direct labor hours are

planned for this next year, what is the company’s plantwide overhead rate?

160. A company estimates that overhead costs for the next year will be $3,600,000 for indirect

labor, $200,000 for factory utilities, and $21,500 for depreciation on factory machinery. The

company uses machine hours as its overhead allocation base. If 764,300 machine hours are

planned for this next year, what is the company’s plantwide overhead rate?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

161. A company has two products: A and B. It uses a plantwide overhead allocation method

based on activity 2 and has prepared the following analysis showing budgeted costs and

activities. Use this information to compute (a) the company’s plantwide overhead rate and (b) the

amount of overhead allocated to Product A.

Activity Cost Pool

Budgeted

Overhead Cost

Budgeted Activity

Product A Product B Total

Activity 1 $160,000 400 1,600 2,000

Activity 2 $110,000 2,000 1,000 3,000

Activity 3 $180,000 1,200 10,800 12,000

Total budgeted

overhead

$450,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

162. A company has two products: A and B. It uses activity-based costing and has prepared the

following analysis showing budgeted costs and activities. Use this information to compute (a) the

company’s overhead rates for each of the three activities and (b) the amount of overhead allocated to Product

A.

Activity Cost Pool

Budgeted

Overhead Cost

Budgeted Activity

Product A Product B Total

Activity 1 $160,000 400 1,600 2,000

Activity 2 $110,000 2,000 1,000 3,000

Activity 3 $180,000 1,200 10,800 12,000

Total budgeted

overhead

$450,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

163. A company has two products: AA and BB. It uses a plantwide overhead allocation method

based on activity 33 and has prepared the following analysis showing budgeted costs and

activities. Use this information to compute the company’s plantwide overhead rate.

Activity Cost Pool

Budgeted

Overhead Cost

Budgeted Activity

Product

AA

Product

BB Total

Activity 11 $40,000 100 400 500

Activity 22 $55,000 500 250 750

Activity 33 $90,000 300 1,700 2,000

Total budgeted

overhead

$185,000

164. A company expects next year’s overhead costs to be $400,000. During this time, the

company also expects to produce 1,000,000 units, have 200,000 direct labor hours, and 800,000

machine hours.

Make the following independent calculations.

a. Compute a plantwide overhead rate using units of production as the allocation base.

b. Compute a plantwide overhead rate using direct labor hours as the allocation base.

c. Compute a plantwide overhead rate using machine hours as the allocation base.

165. Superior Products Manufacturing identified the following data in its two production

departments.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

17-86

Assembly Finishing

Manufacturing overhead costs $225,000 $420,000

Direct labor hours worked 6,600 DLH 9,000 DLH

Machine hours used 2,400 MH 5,200 MH

Make the following independent calculations (Round to two decimals).

a. Compute a plantwide overhead rate using machine hours as the allocation base.

b. Compute a plantwide overhead rate using direct labor hours as the allocation base.

166. Superior Products Manufacturing identified the following data in its two production

departments:

Assembly Finishing

Manufacturing overhead costs $225,000 $420,000

Direct labor hours worked 6,600 DLH 10,000 DLH

Machine hours used 2,400 MH 5,200 MH

Compute departmental overhead rates assuming the Assembly rate is based on machine hours

and the Finishing rate is based on direct labor hours.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

167. Fischer Company identified the following activities, costs, and activity drivers:

Activity Expected Costs Expected Activity

Handling parts $425,000 25,000 parts in

stock

Inspecting product $390,000 940 batches

Processing purchase

orders

$220,000 440 orders

Designing packaging $230,000 5 models

a. Compute a plantwide overhead rate assuming the company assigns overhead based on 70,000

budgeted direct labor hours (Round to two decimals).

b. Compute separate rates for each of the four activities using the activity based costing.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

168. Assume New Belgium Brewing Company manufactures and distributes three types of beer

and that estimated per unit product costs and related information for the next year are shown in

the following table:

Blue

Paddle Somersault

Cocoa

Mole Ale

Cost data per unit:

Direct materials $100,000 $500,000 $750,000

Direct labor $3,600 $4,800 $6,000

Overhead $12,000 $16,000 $20,000

Total product cost per unit $115,600 $520,800 $776,000

Machine hours per unit 30 MH 40 MH 50 MH

Number of units produced per year 30 units 20 units 10 units

a. If New Belgium Brewing Company uses a plantwide overhead rate based on machine hours,

what is the total product cost per unit of Cocoa Mole Ale?

b. Blue Paddle is a traditional brew made in large quantities with long production runs.

Somersault is a seasonal beer made in small batches. Cocoa Mole Ale is a specialty beer also

made in small batches. Which of the overhead allocation methods studied in this chapter would

you recommend that New Belgium Brewing Company use and why?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

169. Time Bender Company makes watches and clocks. The following estimated data are

available for the company’s next fiscal year:

Total direct labor costs: $1,700,000

Total setup costs: $190,000

Watches Clocks

Expected production 800,000 100,000

Direct labor hours needed 68,000 DLH 17,000 DLH

Machine setups needed 1,000 setups 1,000 setups

Determine the setup cost per unit for the watches and the clocks if setup costs are assigned using

a plantwide overhead rate based on direct labor hours. (Round to two decimal places.)

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

170. Base Runner, Inc. manufactures baseball bats that go through two operations, cutting and

sanding, before they are complete. Expected costs and activities for the two departments are

shown in the following table:

Cutting Sanding

Direct labor hours 50,000 DLH 5,000 DLH

Machine hours 25,000 MH 50,000 MH

Overhead costs $50,000 $37,500

a. Compute a departmental overhead rate for the cutting department based on machine hours.

b. Compute a departmental overhead rate for the sanding department based on machine hours.

171. Blast Rocket Company manufactures candy-coated popcorn treats that go through two

operations, popping and baking, before they are complete. Expected costs and activities for the

two departments are shown in the following table:

Popping Baking

Direct labor hours 238,000 DLH 50,000 DLH

Machine hours 25,000 MH 141,500 MH

Overhead costs $357,000 $452,800

a. Compute a departmental overhead rate for the popping department based on direct labor

hours.

b. Compute a departmental overhead rate for the baking department based on machine hours.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

172. Freeze Frame, Inc. produces cameras that require three processes, A, B, and C, to complete.

Digital camera model #789 is the best-selling of all the many types of cameras produced.

Information related to the 550,000 units of digital camera model #789 produced annually is

shown below.

Direct materials $450,000

Direct labor

Department A (7,000 DLH x $21 per DLH) $147,000

Department B (25,000 DLH x $19 per DLH) $475,000

Department C (10,000 DLH x $26 per DLH) $260,000

Machine Hours

Department A 42,000 MH

Department B 23,000 MH

Department C 38,000 MH

Freeze Frame’s total expected overhead costs and related overhead data are shown below:

Department A Department

B

Department

C

Direct labor hours 90,000 DLH 75,000 DLH 42,000 DLH

Machine hours 67,500 MH 135,000 MH 53,200 MH

Manufacturing overhead

costs

$540,000 $675,000 $399,000

a. Compute a departmental overhead rate for department A based on direct labor hours.

b. How much overhead is associated with model 789 from department A?

c. Compute a departmental overhead rate for department B based on direct labor hours.

d. How much overhead is associated with model 789 from department B?

e. Compute a departmental overhead rate for department C based on direct labor hours.

f. How much overhead is associated with model 789 from department C?

g. What is the per unit cost of the 550,000 units of model 789?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

173. Freeze Frame, Inc. produces cameras that require three processes, A, B, and C, to complete.

Digital camera model #789 is the best-selling of all the many types of cameras produced.

Information related to the 550,000 units of digital camera model #789 produced annually is

shown below:

Direct materials $450,000

Direct Labor

Department A (7,000 DLH x $21 per DLH) $147,000

Department B (25,000 DLH x $19 per DLH) $475,000

Department C (10,000 DLH x $26 per DLH) $260,000

Machine Hours

Department A 42,000 MH

Department B 23,000 MH

Department C 38,000 MH

Freeze Frame’s total expected overhead costs and related overhead data are shown in the

following table:

Department A Department B Department C

Direct labor hours 90,000 DLH 75,000 DLH 42,000 DLH

Machine hours 67,500 MH 135,000 MH 53,200 MH

Manufacturing overhead

costs

$540,000 $675,000 $399,000

a. Compute a departmental overhead rate for department A based on machine hours.

b. How much overhead is associated with model 789 from department A?

c. Compute a departmental overhead rate for department B based on direct labor hours.