Chapter 13

ANALYSIS OF FINANCIAL STATEMENTS

True / False Questions

1. Financial statement analysis is the application of analytical tools to general-purpose

financial statements and related data for making business decisions.

2. Financial statement analysis lessens the need for expert judgment.

3. Financial statement analysis may be used for personal financial investment decisions.

4. The evaluation of company performance and financial condition includes evaluation of (1)

past and current performance, (2) current financial position, and (3) future performance and

risk.

5. External users of accounting information make the strategic and operating decisions of a

company.

6. One purpose of financial statement analysis for internal users is to provide strategic

information to improve company efficiency and effectiveness in providing products and

services.

7. Evaluation of company performance does not include analysis of (1) past and current

performance, (2) current financial position, and (3) future performance and risk.

8. A company’s board of directors analyzes financial statements to assess future company

prospects for making operating decisions.

9. Financial analysis only refers to the communication of relevant financial information to

decision makers.

10. Profitability is the ability to generate future revenues and meet long-term obligations.

11. Liquidity and efficiency are the ability to meet short-term obligations and to efficiently

generate revenue.

12. Market prospects are the ability to provide financial rewards sufficient to attract and retain

financing.

13. Profitability is the ability to generate positive market expectations.

14. Financial reporting includes not only general purpose financial statements, but also

information from SEC filings, press releases, shareholders’ meetings, forecasts, management

letters, auditor’s reports, and Webcasts.

15. The building blocks of financial statement analysis include (1) liquidity, (2) salability, (3)

solvency, and (4) profitability.

16. General-purpose financial statements include the (1) income statement, (2) balance sheet,

(3) statement of stockholders’ equity (or statement of retained earnings), (4) statement of cash

flows, and (5) notes to these statements.

17. Standards for comparison are not generally necessary when making judgments about a

company’s performance.

18. Standards for comparison when interpreting financial statement analysis include

competitor and industry performance data.

19. Measures taken from a selected competitor or a group of competitors are often excellent

standards of comparison for analysis.

20. Intra-company analysis is based on comparisons with competitors.

21. General standards of comparisons, developed from experience, include the 2:1 level for

the current ratio and 1:1 level for the acid-test ratio.

22. Vertical analysis is the comparison of a company’s financial condition and performance

across time.

23. If a company is comparing its financial condition or performance to a base amount, it is

using vertical analysis.

24. Horizontal analysis is the comparison of a company’s financial condition and performance

to a base amount.

25. If a company is comparing this year’s financial performance to last year’s financial

performance, it is using horizontal analysis.

26. Three of the most common tools of financial analysis include horizontal analysis, vertical

analysis, and ratio analysis.

27. A financial statement analysis report helps to reduce uncertainty in business decisions

through a rigorous and sound evaluation.

28. A good financial report does not link interpretations and conclusions of analysis with the

underlying information.

29. A good financial statement analysis report often includes the following sections: executive

summary, analysis overview, evidential matter, assumptions, key factors, and inferences.

30. Earnings per share are calculated only on income from continuing operations.

31. Analysis of a single financial number is often of limited value.

32. Comparative financial statements are reports that show financial amounts in side by side

columns on a single statement for analysis purposes.

33. Vertical analysis is used to reveal patterns in data covering two or more successive

periods.

34. Trend analysis is a form of horizontal analysis that can reveal patterns in data across

successive periods.

35. Trend analysis of financial statement items can include comparisons of relations between

items on different financial statements.

36. Horizontal analysis is used to reveal patterns in data covering successive periods.

37. A trend percent, or index number, is calculated by dividing the analysis period amount by

the base period amount and multiplying the result by 100.

38. The percent change of a comparative financial statement item is computed by subtracting

the analysis period amount from the base period amount, dividing the result by the base

period amount and multiplying that result by 100.

39. Vertical analysis is a tool to evaluate individual financial statement items or groups of

items in terms of a specific base amount.

40. Horizontal analysis is used to reveal changes in the relative importance of each financial

statement item.

41. The base amount for a common-size balance sheet is usually total assets.

42. An advantage of common-size statements is that they reflect the dollar magnitude (size) of

the different companies under analysis.

43. Graphical analysis of the balance sheet can be useful in assessing sources of financing.

44. A corporation reported cash of $14,000 and total assets of $178,300. Its common-size

percent for cash equals 7.85%.

45. A ratio expresses a mathematical relation between two quantities and can be expressed as

a percent, rate, or proportion.

46. Ratios must refer to economically important relationships, such as a sale price compared

to its cost.

47. Liquidity refers to the availability of resources to meet short-term cash requirements.

48. Working capital is computed as current liabilities minus current assets.

49. The current ratio is calculated as current liabilities divided by current assets.

50. Total asset turnover reflects a company’s ability to use its assets to generate sales and is an

important indication of operating efficiency.

51. Capital structure refers to a company’s long-run financial viability and its ability to cover

long-term obligations.

52. The use of debt is sometimes described as financial leverage because debt can have the

effect of increasing the return on equity.

53. The greater the times interest earned ratio, the greater the risk a company is exposed to.

54. Efficiency refers to how productive a company is in using its assets, and is usually

measured relative to how much revenue is generated from a certain level of assets.

55. The higher the accounts receivable turnover, the less quickly accounts receivable are

collected.

56. A company with a high inventory turnover requires a smaller investment in inventory than

one producing the same sales with a lower turnover.

57. A rough guideline states that for a company with no discounts offered, days’ sales

uncollected should not exceed 1 1/3 times the days in its credit period.

58. A company that has days’ sales uncollected of 30 days and days’ sales in inventory of 18

days implies that inventory will be converted to cash in about 12 days.

59. The return on total assets can be calculated as profit margin times total asset turnover.

60. The return on common stockholder’s equity measures a company’s success in earning net

income for its owners.

61. A high level of expected risk suggests a low price-earnings (PE) ratio.

62. The return on total assets ratio is a profitability measure.

63. A company reports basic earnings per share of $3.50, cash dividends per share of $0.75,

and a market price per share of $64.75. The company’s dividend yield equals 21.4%.

64. Financial statement analysis involves all of the following except:

A. The application of analytical tools to general-purpose financial statements and related data

for making business decisions.

B. Transforming accounting data into useful information for decision-making.

C. Helping users to make better decisions.

D. Helping to reduce uncertainty in decision-making.

E. Assuring that the company will be more profitable in the future.

65. Evaluation of company performance can include comparison and/or assessment of all but

which of the following:

A. Past performance.

B. Current performance.

C. Current financial position.

D. Future performance and risk.

E. External user needs and demands.

66. External users of financial information:

A. Are those individuals involved in managing and operating the company.

B. Include internal auditors and consultants.

C. Are not directly involved in operating the company.

D. Make strategic decisions for a company.

E. Make operating decisions for a company.

67. Internal users of financial information:

A. Are not directly involved in operating a company.

B. Are those individuals involved in managing and operating the company.

C. Include shareholders and lenders.

D. Include directors and customers.

E. Include suppliers, regulators, and the press.

68. The building blocks of financial statement analysis do not include:

A. External analyst services.

B. Solvency.

C. Profitability.

D. Market prospects.

E. Liquidity and efficiency.

69. Financial reporting refers to:

A. The application of analytical tools to general-purpose financial statements.

B. The communication of financial information useful for decision making.

C. General-purpose financial statements only.

D. Ratio analysis only.

E. Profitability.

70. The ability to meet short-term obligations and to efficiently generate revenues is called:

A. Liquidity and efficiency.

B. Solvency.

C. Profitability.

D. Market prospects.

E. Creditworthiness.

71. The ability to generate future revenues and meet long-term obligations is referred to as:

A. Liquidity and efficiency.

B. Solvency.

C. Profitability.

D. Market prospects.

E. Creditworthiness.

72. The ability to provide financial rewards sufficient to attract and retain financing is called:

A. Liquidity and efficiency.

B. Solvency.

C. Profitability.

D. Market prospects.

E. Creditworthiness.

73. The ability to generate positive market expectations is called:

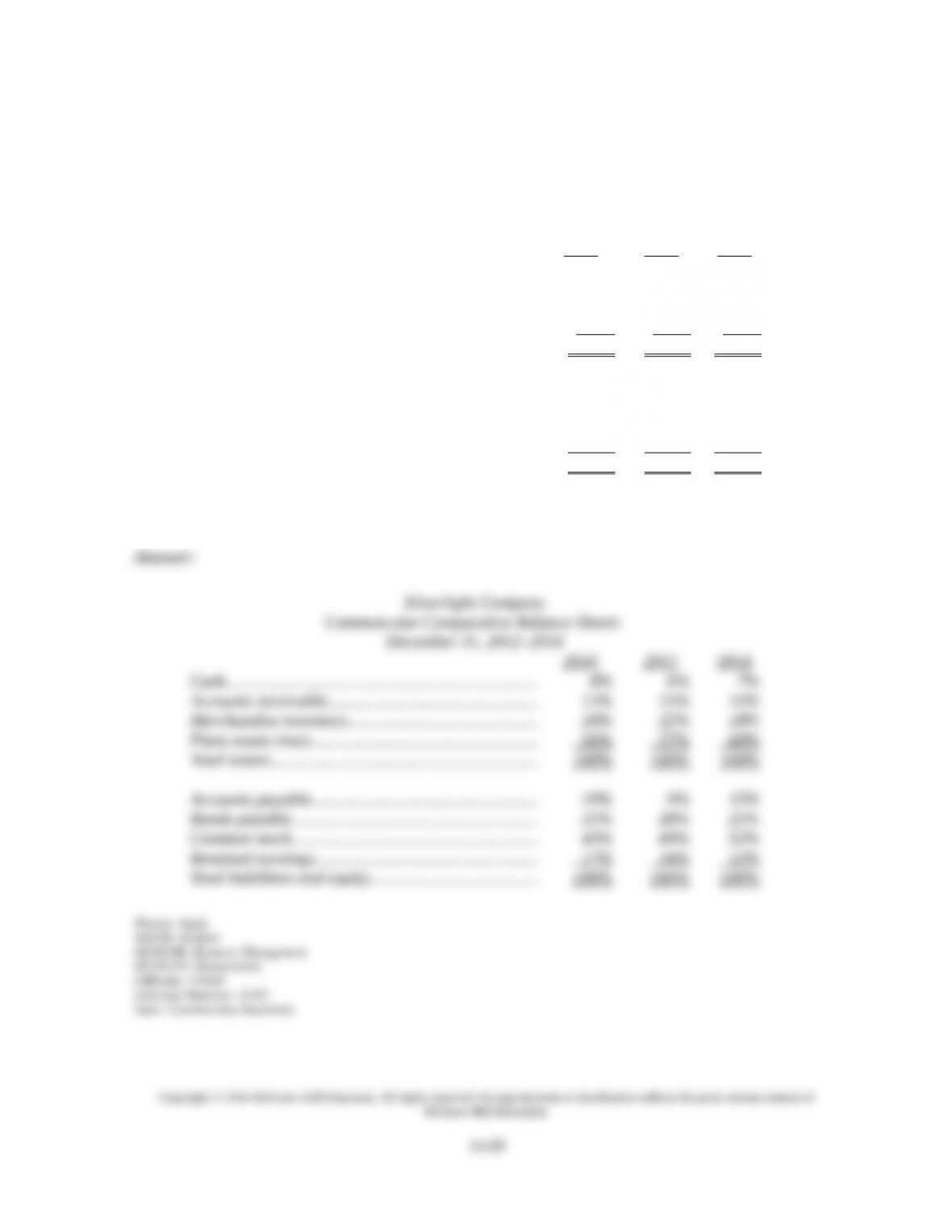

A. Liquidity and efficiency.

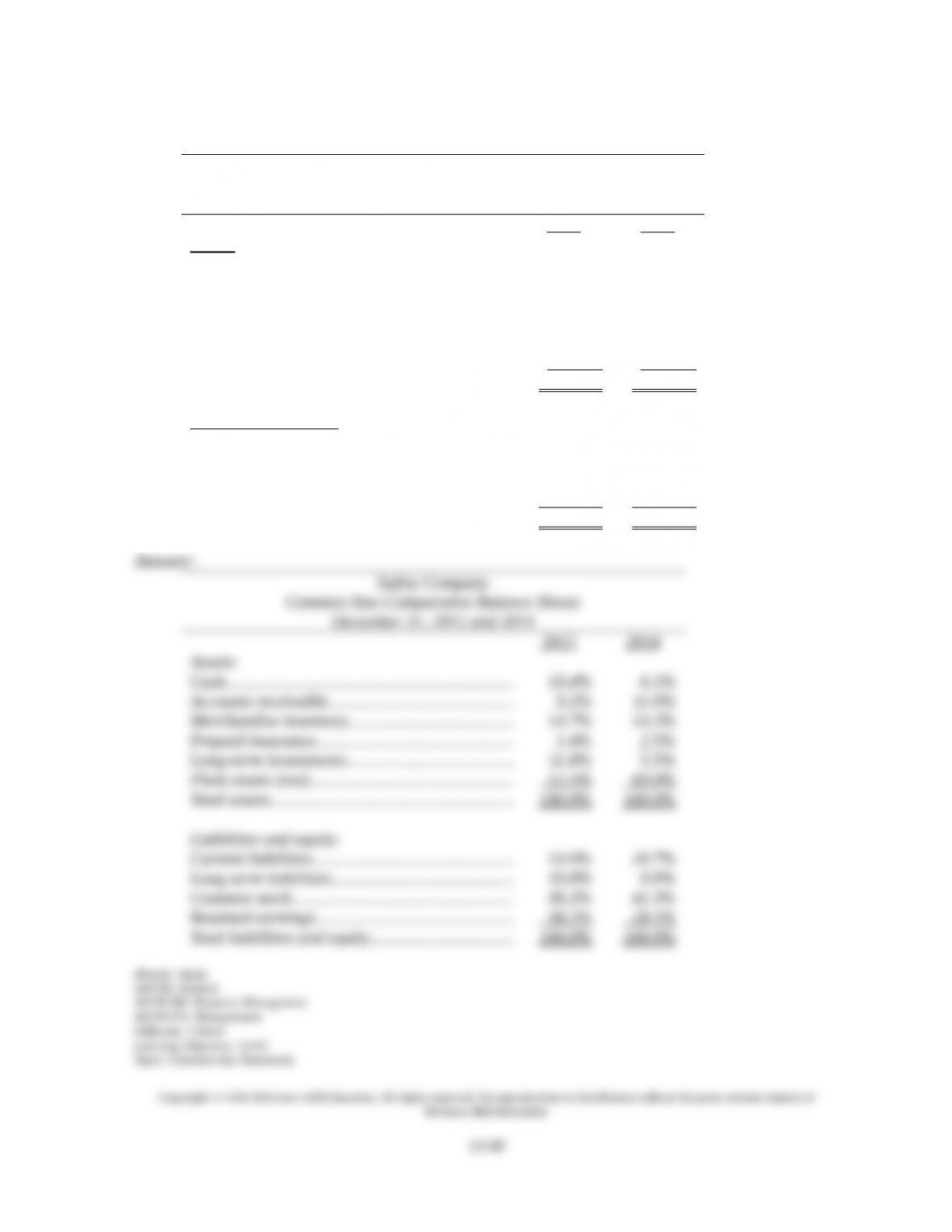

B. Liquidity and solvency.

C. Profitability.

D. Market prospects.

E. Creditworthiness.

74. Standards for comparisons in financial statement analysis do not include:

A. Intra-company standards.

B. Competitors’ standards.

C. Industry standards.

D. Management standards

E. . Guidelines (rules of thumb).

75. Intra-company standards for financial statement analysis:

A. Are based on a company’s prior performance and relations between its financial items.

B. Are often set by competitors.

C. Are set by the company’s industry through published statistics.

D. Are based on rules of thumb.

E. Are published in Dun and Bradstreet.

76. Industry standards for financial statement analysis:

A. Are based on a single competitor’s financial performance.

B. Are set by the government.

C. Are available for the financial performance and condition of the company’s industry.

D. Are based on rules of thumb.

E. Compare a company’s income with its prior year’s income.

77. Guidelines (rules-of-thumb) are general standards of comparison developed from:

A. Industry statistics from the government.

B. Past experience.

C. Analysis of competitors.

D. Relations between financial items.

E. Dun and Bradstreet.

78. Three of the most common tools of financial analysis are:

A. Financial reporting, ratio analysis, vertical analysis.

B. Ratio analysis, horizontal analysis, financial reporting.

C. Horizontal analysis, vertical analysis, ratio analysis.

D. Trend analysis, financial reporting, ratio analysis.

E. Vertical analysis, political analysis, horizontal analysis.

79. The comparison of a company’s financial condition and performance across time is known

as:

A. Horizontal analysis.

B. Vertical analysis.

C. Political analysis.

D. Financial reporting.

E. Investment analysis.

80. The measurement of key relations among financial statement items is known as:

A. Financial reporting.

B. Horizontal analysis.

C. Investment analysis.

D. Ratio analysis.

E. Risk analysis.

81. The comparison of a company’s financial condition and performance to a base amount is

known as:

A. Financial reporting.

B. Horizontal ratios.

C. Investment analysis.

D. Risk analysis.

E. Vertical analysis.

82. A financial statement analysis report does not include:

A. An auditor statement.

B. An analysis overview.

C. Evidential matter.

D. Qualitative and quantitative key factors.

E. .Inferences such as forecasts

83. The background on a company, its industry, and its economic setting is usually included in

which of the following sections of a financial statement analysis report:

A. Executive summary.

B. Analysis overview.

C. Evidential conclusions.

D. Factor analysis.

E. Inferences.

84. All of the following are true of financial statement analysis report, except:

A. Contains ambiguities and qualifications.

B. Forces preparers to organize their reasoning and to verify the logic of analysis.

C. Serves as a method of communication to users.

D. Helps users and preparers to refine conclusions based on evidence from key building

blocks.

E. Enables readers to see the process and rationale of analysis.

85. When a company’s activities include income-related events not part of normal, continuing

operations, the complete income statement could potentially have the following sections:

A. Items from continuing operations and earnings per share for a corporation.

B. Income or loss from operating a discontinued segment for the current period.

C. The loss from disposing of the discontinued segment’s net assets.

D. Extraordinary items.

E. Continuing operations, discontinued segments, extraordinary items, changes in accounting

principles, and earnings per share for a corporation.

86. Which of the following items is not likely an extraordinary item?

A. Write down of inventories.

B. Condemnation of property by the city government.

C. Loss of use of property due to a new and unexpected environmental regulation.

D. Loss due to an unusual and infrequent calamity.

E. Expropriation of property by a foreign government.

87. Financial statements with data for two or more successive accounting periods placed in

columns side by side, sometimes with changes shown in both dollar amounts and percentages,

are referred to as:

A. Period-to-period statements.

B. Controlling statements.

C. Successive statements.

D. Comparative statements.

E. Serial statements.

88. Horizontal analysis:

A. Is a method used to evaluate changes in financial data across time.

B. Is also called vertical analysis.

C. Is the presentation of financial ratios.

D. Is a tool used to evaluate financial statement items relative to industry statistics.

E. Evaluates financial data across industries.

89. The dollar change for a comparative financial statement item is calculated by:

A. Subtracting the analysis period amount from the base period amount.

B. Subtracting the base period amount from the analysis period amount.

C. Subtracting the analysis period amount from the base period amount, dividing the result by

the base period amount, then multiplying that amount by 100.

D. Subtracting the base period amount from the analysis period amount, dividing the result by

the base period amount, then multiplying that amount by 100.

E. Subtracting the base period amount from the analysis amount, then dividing the result by

the base amount.

90. A company’s sales in Year 1 were $250,000 and in Year 2 were $287,500. Using Year 1 as

the base year, the percentage change for Year 2 compared to the base year is:

A. 87%.

B. 100%.

C. 115%.

D. 15%.

E. 13%.

91. Yeats Corporation’s sales in Year 1 were $396,000 and in Year 2 were $380,000. Using

Year 1 as the base year, the percentage change for Year 2 compared to the base year is:

A. 104%.

B. 100%.

C. 4%.

D. 96%.

E. 4.2%.

92. Ash Company reported sales of $400,000 for Year 1, $450,000 for Year 2, and $500,000

for Year 3. Using Year 1 as the base year, what were the percentage increases for Year 2 and

Year 3 compared to the base year?

A. 80% for Year 2 and 90% for Year 3.

B. 88% for Year 2 and 80% for Year 3.

C. 88% for Year 2 and 90% for Year 3.

D. 112.5% for Year 2 and 125% for Year 3.

E. 125% for Year 2 and 112.5% for Year 3.

93. In horizontal analysis the percent change is computed by:

A. Subtracting the analysis period amount from the base period amount.

B. Subtracting the base period amount from the analysis period amount.

C. Subtracting the analysis period amount from the base period amount, dividing the result by

the base period amount, then multiplying that amount by 100.

D. Subtracting the base period amount from the analysis period amount, dividing the result by

the base period amount, then multiplying that amount by 100.

E. Subtracting the base period amount from the analysis amount, then dividing the result by

the analysis period amount.

94. To compute trend percentages the analyst should:

A. Select a base period, assign each item in the base period statement a weight of 100%, and

then express financial numbers from other periods as a percent of their base period number.

B. Subtract the analysis period number from the base period number.

C. Subtract the base period amount from the analysis period amount, divide the result by the

analysis period amount, then multiply that amount by 100.

D. Compare amounts across industries using Dun and Bradstreet.

E. Compare amounts to a competitor.

95. Comparative financial statements in which each individual financial statement amount is

expressed as a percentage of a base amount are called:

A. Asset comparative statements.

B. Percentage comparative statements.

C. Common-size comparative statements.

D. Sales comparative statements.

E. General-purpose financial statements.

96. Common-size statements:

A. Reveal changes in the relative importance of each financial statement item to a base

amount.

B. Do not emphasize the relative importance of each item.

C. Compare financial statements over time.

D. Show the dollar amount of change for financial statement items.

E. Reveal patterns in data across successive periods.

97. The common-size percent is computed by:

A. Dividing the analysis amount by the base amount.

B. Dividing the base amount by the analysis amount.

C. Dividing the analysis amount by the base amount and multiplying the result by 100.

D. Dividing the base amount by the analysis amount and multiplying the result by 1,000.

E. Subtracting the base amount from the analysis amount and multiplying the result by 100.

98. A corporation reported cash of $14,000 and total assets of $178,300 on its balance sheet.

Its common-size percent for cash equals:

A. .0785%.

B. 7.85%.

C. 12.73%.

D. 1273%.

E. 7850%.

99. A corporation reported cash of $27,000 and total assets of $461,000 on its balance sheet.

Its common-size percent for cash equals:

A. 17.1%.

B. 58.6%.

C. 100%.

D. 5.86%.

E. 1707%.

100. Current assets minus current liabilities is:

A. Profit margin.

B. Financial leverage.

C. Current ratio.

D. Working capital.

E. Quick assets.

101. Jones Corp. reported current assets of $193,000 and current liabilities of $137,000 on its

most recent balance sheet. The working capital is:

A. 141%.

B. 71%.

C. ($56,000).

D. $56,000.

E. 41%.

102. Jones Corp. reported current assets of $193,000 and current liabilities of $137,000 on its

most recent balance sheet. The current ratio is:

A. 1.4:1

B. 0.7:1.

C. 0.3:1.

D. 1:1.

E. 0.4:1.

103. Jones Corp. reported current assets of $193,000 and current liabilities of $137,000 on its

most recent balance sheet. The current assets consisted of $62,000 Cash; $43,000 Accounts

Receivable; and $88,000 of Inventory. The acid-test (quick) ratio is:

A. 1.4:1

B. 0.77:1.

C. 0.54:1.

D. 1:1.

E. 0.64:1.

104. Current assets divided by current liabilities is the:

A. Current ratio.

B. Quick ratio.

C. Debt ratio.

D. Liquidity ratio.

E. Solvency ratio.

105. Quick assets divided by current liabilities is the:

A. Acid-test ratio.

B. Current ratio.

C. Working capital ratio.

D. Current liability turnover ratio.

E. Quick asset turnover ratio.

106. Net sales divided by Average accounts receivable, net is the:

A. Days’ sales uncollected.

B. Average accounts receivable ratio.

C. Current ratio.

D. Profit margin.

E. Accounts receivable turnover ratio.

107. Powers Company reported Net sales of $1,200,000 and average Accounts Receivable,

net of $78,500. The accounts receivable turnover ratio is:

A. 0.65 times

B. 14.3 times.

C. 28.6 times

D. 15.3 times

E. 16.3 times.

108. Powers Company reported Net sales of $1,200,000 and Accounts Receivable, net of

$78,500. The Day’s sales uncollected (rounded to whole days) is:

A. 24 days

B. 15 days.

C. 4 days.

D. 56 days.

E. 48 days.

109. Dividing Accounts receivable, net by Net sales and multiplying the result by 365 is the:

A. Profit margin.

B. Days’ sales uncollected.

C. Accounts receivable turnover ratio.

D. Average accounts receivable ratio.

E. Current ratio.

110. Dividing ending inventory by cost of goods sold and multiplying the result by 365 is the:

A. Inventory turnover ratio.

B. Profit margin.

C. Days’ sales in inventory.

D. Current ratio.

E. Total asset turnover.

111. Zhang Company reported Cost of goods sold of $835,000, beginning Inventory of

$37,200 and ending Inventory of $46,300. The average Inventory amount is:

A. $37,200

B. $46,300.

C. $83,500.

D. $41,750.

E. $9,100.

112. Zhang Company reported Cost of goods sold of $835,000 and average Inventory of

$41,750. The Inventory turnover ratio is:

A. 0.5 times

B. 418 times.

C. 20 times.

D. 56 times.

E. 19 times.

113. Zhang Company reported Cost of goods sold of $835,000 and ending Inventory of

$41,750. The Days’ sales in inventory (rounded to whole days) is:

A. 18 days

B. 418 days.

C. 10 days.

D. 56 days.

E. 20 days.

114. Net sales divided by average total assets is the:

A. Profit margin.

B. Total asset turnover.

C. Current ratio.

D. Sales return ratio.

E. Return on total assets.

115. Carducci Corporation reported Net sales of $3.6 million and average Total assets of $1.1

million. The Total asset turnover is:

A. 0.31 times

B. 3.27 times.

C. 4.30 times.

D. 2.27 times.

E. 0.77 times.

116. Carducci Corporation reported Net sales of $3.6 million and beginning Total assets of

$0.9 million and ending Total assets of 1.3 million. The average Total asset amount is:

A. $2.3 million

B. $2.7 million.

C. $0.25 million.

D. $0.36 million.

E. $1.1 million.

117. Net income divided by net sales is the:

A. Return on total assets.

B. Profit margin.

C. Current ratio.

D. Total asset turnover.

E. Days’ sales in inventory.

118. Martinez Corporation reported Net sales of $765,000 and Net income of $142,000. The

Profit margin is:

A. 539.0%.

B. 5.39%.

C. 81.4%.

D. 1.86%.

E. 18.56%.

119. Net income divided by average total assets is:

A. Profit margin.

B. Total asset turnover.

C. Return on total assets.

D. Days’ income in assets.

E. Current ratio.

120. Clairmont Industries reported Net income of $283,000 and average Total assets of

$637,000. The Return on total assets is:

A. 55.6%.

B. 88.8%.

C. 61.5%.

D. 44.4%.

E. 125.1%.

121. Annual cash dividends per share divided by market price per share is the:

A. Price-earnings ratio

B. Price-dividends ratio.

C. Profit margin.

D. Dividend yield ratio.

E. Earnings per share.

122. The market price of Horokhiv Corporation’s common stock at the start of 2014 was

$47.50 and it declared and paid cash dividends of $3.28 per share. The Dividend yield ratio

is:

A. 14.5%.

B. 7.4%.

C. 6.5%.

D. 144.8%.

E. 6.9%.

123. How long a company holds inventory before selling it can be measured by dividing cost

of goods sold by the average inventory balance to determine the:

A. Accounts receivable turnover.

B. Inventory turnover.

C. Days’ sales uncollected.

D. Current ratio.

E. Price earnings ratio.

124. A component of operating efficiency and profitability, calculated by expressing net

income as a percent of net sales, is the:

A. Acid-test ratio.

B. Merchandise turnover.

C. Price earnings ratio.

D. Accounts receivable turnover.

E. Profit margin ratio.

125. One of several ratios that reflects solvency includes the:

A. Acid-test ratio.

B. Current ratio.

C. Times interest earned ratio.

D. Total asset turnover.

E. Days’ sales in inventory.

126. A company had a market price of $27.50 per share, earnings per share of $1.25, and

dividends per share of $0.40. Its price-earnings ratio equals:

A. 3.1.

B. 22.0.

C. 93.8.

D. 32.0.

E. 3.3.

127. A company reports basic earnings per share of $3.50, cash dividends per share of $1.25,

and a market price per share of $64.75. The company’s dividend yield equals:

A. 1.93%.

B. 2.14%.

C. 4.67%.

D. 5.41%.

E. 18.50%.

128. Rajan Company’s most recent balance sheet reported total assets of $1.9 million, total

liabilities of $0.8 million, and total equity of $1.1 million. Its Debt to equity ratio is:

A. 0.42

B. 0.58

C. 1.38

D. 0.73

E. 1.00

129. Desjardin Landscaping’s income statement reports net income of $75,300, which

includes deductions for interest expense of $11,500 and income taxes of $34,900. Its times

interest earned is:

A. 10.6 times

B. 7.5 times

C. 4.0 times

D. 6.5 times

E. 0.15 times

130. Selected current year company information follows:

Net income ………………………………………………. $ 15,953

Net sales………………………………………………..…. 712,855

Total liabilities, beginning-year…….……........... 83,932

Total liabilities, end-of-year..………..…………….. 103,201

Total stockholders‘ equity, beginning-year….. 198,935

Total stockholders‘ equity, end-of-year............. 121,851

The total asset turnover is:

A. 2.24 times

B. 2.81 times

C. 3.64 times

D. 4.67 times

E. 6.28 times

131. Selected current year company information follows:

Net income ………………………………………………. $ 15,953

Net sales………………………………………………..…. 712,855

Total liabilities, beginning-year…….……........... 83,932

Total liabilities, end-of-year..………..…………….. 103,201

Total stockholders‘ equity, beginning-year…… 198,935

Total stockholders‘ equity, end-of-year............. 121,851

The return on total assets is:

A. 2.24%

B. 2.81%

C. 3.64%

D. 4.67%

E. 6.28%

132. All of the following statements regarding a business segment are true except:

A. A business segment is a part of a company’s operations that serves a particular product

line.

B. A segment has assets, liabilities, and financial results of operations that can be

distinguished from those of other parts of the company.

C. A company’s gain or loss from selling or closing down a segment is reported separately.

D. The income tax effects of a discontinued segment are combined with income tax from

continuing operations.

E. A segment’s income for the period prior to the disposal and the gain or loss resulting from

disposing of the segment’s assets are reported separately.

133. Use the following selected information from Wheeler, LLC to determine the 2015 and

2014 common size percentages for cost of goods sold using Net sales as the base.

2015 2014

Net sales $276,200 $231,400

Cost of goods sold 151,900 129,590

Operating expenses 55,240 53,240

Net earnings 27,820 19,820

A. 36.4% for 2015 and 41.1% for 2014.

B. 55.0% for 2015 and 56.0% for 2014.

C. 119.4% for 2015 and 100.0% for 2014.

D. 117.2% for 2015 and 100.0% for 2014.

E. 65.1% for 2015 and 56.0% for 2014.

134. Use the following selected information from Wheeler, LLC to determine the 2015 and

2014 common size percentages for operating expenses using Net sales as the base.

2015 2014

Net sales $276,200 $231,400

Cost of goods sold 151,900 129,590

Operating expenses 55,240 53,240

Net earnings 27,820 19,820

A. 36.4% for 2015 and 41.1% for 2014.

B. 55.0% for 2015 and 56.0% for 2014.

C. 23.9% for 2015 and 23.0% for 2014.

D. 103.8% for 2015 and 100.0% for 2014.

E. 20.0% for 2015 and 23.0% for 2014.

135. Use the following selected information from Wheeler, LLC to determine the 2015 and

2014 trend percentages for net sales using 2014 as the base.

2015 2014

Net sales $276,200 $231,400

Cost of goods sold 151,900 129,590

Operating expenses 55,240 53,240

Net earnings 27,820 19,820

A. 36.4% for 2015 and 41.1% for 2014.

B. 55.0% for 2015 and 56.0% for 2014.

C. 119.4% for 2015 and 100.0% for 2014.

D. 117.2% for 2015 and 100.0% for 2014.

E. 65.1% for 2015 and 64.6% for 2014.

136. Use the following selected information from Wheeler, LLC to determine the 2015 and

2014 trend percentages for cost of goods sold using 2014 as the base.

2015 2014

Net sales $276,200 $231,400

Cost of goods sold 151,900 129,590

Operating expenses 55,240 53,240

Net earnings 27,820 19,820

A. 36.4% for 2015 and 41.1% for 2014.

B. 55.0% for 2015 and 56.0% for 2014.

C. 119.4% for 2015 and 100.0% for 2014.

D. 117.2% for 2015 and 100.0% for 2014.

E. 65.1% for 2015 and 64.6% for 2014.

137. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s working capital for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. $232,700.

B. $220,600.

C. $147,200.

D. $111,700.

E. $142,700.

138. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s current ratio for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 2.26.

B. 1.98.

C. 2.95.

D. 3.05.

E. 1.88.

139. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s acid-test ratio for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 2.26.

B. 1.98.

C. 2.95.

D. 3.05.

E. 1.88.

140. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s accounts receivable turnover for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 8.62.

B. 8.28.

C. 8.94.

D. 5.78.

E. 7.90.

141. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s inventory turnover for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 4.72.

B. 4.33.

C. 3.28.

D. 5.78.

E. 3.86.

142. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s days’ sales uncollected for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 43.9.

B. 42.3.

C. 46.2.

D. 80.0.

E. 113.3.

143. Refer to the following selected financial information from McCormik, LLC. Compute

the company’s days’ sales in inventory for Year 2.

Year 2 Year 1

Cash $37,500 36,850

Short-term investments 90,000 90,000

Accounts receivable, net 85,500 86,250

Merchandise inventory 121,000 117,000

Prepaid expenses 12,100 13,500

Plant assets 388,000 392,000

Accounts payable 113,400 111.750

Net sales 711,000 706,000

Cost of goods sold 390,000 385,500

A. 43.9.

B. 42.3.

C. 46.2.

D. 80.0.

E. 113.3.

144. Refer to the following selected financial information from Frankle Corp. Compute the

company’s working capital.

Current Assets 306,450

Plant assets 338,000

Current Liabilities 107,800

Net sales 676,000

Net Income 75,000

A. $536,650.

B. $230,200.

C. $568,200.

D. $198,650.

E. $231,450.

145. Refer to the following selected financial information from Frankle Corp. Compute the

company’s current ratio.

Current assets 306,450

Plant assets 388,000

Current Liabilities 107,800

Net sales 676,000

Net Income 75,000

A. 6.44.

B. 2.84.

C. 6.27.

D. 3.60.

E. 1.44.

146. Refer to the following selected financial information from Dodge Company. Compute

the company’s acid-test ratio.

Cash $42,250

Short-term investments 60,000

Accounts receivable, net 79,500

Merchandise inventory 115,000

Prepaid expenses 9,700

Accounts payable 111,400

A. 2.75.

B. 2.66.

C. 0.92.

D. 1.12.

E. 1.63.

147. Refer to the following selected financial information from Marston Company. Compute

the company’s accounts receivable turnover for Year 2.

Year 2 Year 1

Accounts receivable, net 86,500 82,750

Net sales 723,000 693,000

A. 8.36.

B. 8.37.

C. 4.78.

D. 8.59.

E. 8.54.

148. Refer to the following selected financial information from Marston Company. Compute

the company’s days’ sales uncollected for Year 2.

Year 2 Year 1

Accounts receivable, net 86,500 82,750

Net sales 723,000 693,000

A. 43.9.

B. 43.7.

C. 46.2.

D. 85.4.

E. 42.7.

149. Refer to the following selected financial information from Graceworks Corp. Compute

the company’s inventory turnover for Year 2.

Year 2 Year 1

Merchandise inventory 271,000 253,500

Cost of goods sold 486,400 433,100

A. 1.79.

B. 1.71.

C. 1.85.

D. 0.93.

E. 1.75.

150. Refer to the following selected financial information from Graceworks, Corp. Compute

the company’s days’ sales in inventory for Year 2.

Year 2 Year 1

Merchandise inventory 271,000 253,500

Cost of goods sold 486,400 433,100

A. 203.4.

B. 228.4.

C. 179.5.

D. 215.1.

E. 113.3.

151. Refer to the following selected financial information from Shakley’s Incorporated.

Compute the company’s profit margin for Year 2.

Year 2 Year 1

Net sales $478,500 $426,250

Cost of goods sold 276,300 250,120

Interest expense 9,700 10,700

Net income before tax 67,250 52,680

Net income after tax 46,050 39,900

Total assets 317,100 288,000

Total liabilities 181,400 167,300

Total equity 135,700 120,700

A. 14.1%.

B. 11.7%.

C. 9.6%.

D. 16.7%.

E. 33.9%.

152. Refer to the following selected financial information from Shakley’s Incorporated.

Compute the company’s return on total assets for Year 2.

Year 2 Year 1

Net sales $478,500 $426,250

Cost of goods sold 276,300 250,120

Interest expense 9,700 10,700

Net income before tax 67,250 52,680

Net income after tax 46,050 39,900

Total assets 317,100 288,000

Total liabilities 181,400 167,300

Total equity 135,700 120,700

A. 9.6%.

B. 15.2%.

C. 2.6%.

D. 22.2%.

E. 14.5%.

153. Refer to the following selected financial information from Shakley’s Incorporated.

Compute the company’s debt-to-equity ratio for Year 2.

Year 2 Year 1

Net sales $478,500 $426,250

Cost of goods sold 276,300 250,120

Interest expense 9,700 10,700

Net income before tax 67,250 52,680

Net income after tax 46,050 39,900

Total assets 317,100 288,000

Total liabilities 181,400 167,300

Total equity 135,700 120,700

A. 1.75.

B. 2.34.

C. 0.75.

D. 1.34.

E. 2.63.

154. Refer to the following selected financial information from Shakley’s Incorporated.

Compute the company’s times interest earned for Year 2.

Year 2 Year 1

Net sales $478,500 $426,250

Cost of goods sold 276,300 250,120

Interest expense 9,700 10,700

Net income before tax 67,250 52,680

Net income after tax 46,050 39,900

Total assets 317,100 288,000

Total liabilities 181,400 167,300

Total equity 135,700 120,700

A. 6.9.

B. 4.8.

C. 5.8.

D. 14.0.

E. 7.9.

155. Refer to the following selected financial information from Graphics, Inc. Compute the

company’s times interest earned.

Interest expense 9,100

Income tax expense 22,700

Net income after tax 56,500

A. 6.2.

B. 2.5.

C. 8.7.

D. 9.7.

E. 3.7.

156. Refer to the following selected financial information from Keller Company. Compute the

company’s debt to equity for Year 2.

Year 2 Year 1

Total assets 327,800 301,000

Total liabilities 171,400 169,300

Total equity 156,400 131,700

A. 0.9.

B. 1.1.

C. 0.5.

D. 1.9.

E. 2.1.

157. Match each of the following terms with the appropriate definitions.

A. Comparative financial statement

B. Horizontal analysis

C. Liquidity and efficiency

D. Vertical analysis

E. Financial statement analysis

F. Market prospects

G. Solvency

H. Debt to equity ratio

I. Profitability

J. Common-size financial statement

______ (1) A company’s ability to generate positive market expectations.

______ (2) The application of analytical tools to general-purpose financial statements and

related data for making business decisions.

______ (3) A measure of solvency presented as the ratio of total liabilities to total equity.

______ (4) A statement with data for two or more successive accounting periods placed in

side-by-side columns, often with changes shown in dollar amounts and percentages.

______ (5) A company’s ability to provide financial rewards sufficient to attract and retain

capital.

______ (6)A statement where each amount is expressed as a percent of a base amount to

reveal the relative importance of each financial statement item.

______ (7) The comparison of a company’s financial condition and performance to a base

amount.

______ (8) Examination of financial data across time.

______ (9) A company’s ability to generate future revenues and meet long-term obligations.

______ (10) The availability of resources to meet short-term obligations and to efficiently

generate revenues.

1. F; 2. E; 3. H; 4. A; 5. I; 6. J; 7. D; 8. B; 9. G; 10. C

Blooms: Remember

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 1 Easy

Learning Objective: 13-C1

Learning Objective: 13-C2

Learning Objective: 13-P1

Learning Objective: 13-P2

Learning Objective: 13-P3

Topic: Purpose of Analysis

Topic: Standards for Comparisons

Topic: Comparative Statements

Topic: Common-Size Statements

Topic: Ratio Analysis

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-77

158. Match each of the following terms with the appropriate formulas.

A. Days’ sales in inventory

B. Dividend yield

C. Total asset turnover

D. Inventory turnover

E. Return on common stockholders’ equity

F. Gross margin ratio

G. Days’ sales uncollected

H. Profit margin ratio

I. Times interest earned

J. Debt ratio

__________ (1) Net income – Preferred dividends

Average common stockholders’ equity

__________(2) Accounts receivable * 365

Net sales

__________(3) Total liabilities

Total assets

__________ (4) Income before interest expense and income taxes

Interest expense

__________ (5) Annual cash dividends per share

Market price per share

__________ (6) Net sales – Cost of goods sold

Net sales

__________ (7) Cost of goods sold

Average inventory

__________ (8) Net sales

Average total assets

__________(9) Net income

Net sales

__________(10) Ending inventory * 365

Cost of goods sold

1. E; 2. G; 3. J; 4. I; 5. B; 6. F; 7. D; 8. C; 9. H; 10. A

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-78

Blooms: Understand

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 13-P3

Topic: Ratio Analysis

159. Identify the financial analysis building block most appropriately associated with each

ratio listed below by placing the letter of the building block a through d beside each ratio 1

through 10. Each building block may be used more than once.

A. Liquidity and Efficiency

B. Solvency

C. Profitability

D. Market Prospects

__________ (1) Price Earnings Ratio

__________ (2) Dividend Yield

__________ (3) Accounts Receivable Turnover

__________ (4) Days’ Sales in Inventory

__________ (5) Return on Total Assets

__________ (6) Equity Ratio

__________ (7) Debt Ratio

__________ (8) Inventory Turnover

__________ (9) Basic Earnings per Share

__________ (10) Times Interest Earned

1. D; 2. D; 3. A; 4. A; 5. C; 6. B; 7. B; 8. A; 9. C; 10. B

Blooms: Understand

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 13-P3

Topic: Ratio Analysis

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-79

Short Answer Questions

160. Explain the purpose of financial statement analysis for both external and internal users.

161. Identify and explain the four building blocks of financial statement analysis.

162. What are the four standards for comparisons in financial analysis? Give an example of

each.

163. Identify and describe three common tools of financial statement analysis.

Analysis: Three common tools of financial statement analysis are: (1) horizontal analysis,

which compares a company’s financial condition and performance across time; (2) vertical

analysis, which compares a company’s financial condition and performance to a base amount;

and (3) ratio analysis, which uses key relations between financial statement items.

Blooms: Understand

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 2 Medium

Learning Objective: 13-C2

Topic: Standards for Comparisons

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-81

164. What is the purpose of a good financial statement analysis report? What are the key

components?

165. Describe the purpose of horizontal financial statement analysis and how it is applied.

166. Describe the purpose of vertical financial statement analysis and how it is applied.

167. Describe ratio analysis including its purpose, application, and interpretation.

168. A company’s sales in Year 1 were $280,000, and its sales in Year 2 were $341,600. Using

Year 1 as the base year, what is the sales trend percent for Year 2?

169. Calculate the percent increase or decrease for each of the following financial statement

items:

Year 2 Year 1

Cash…………………………………………..…..……..… $ 37,500 $ 30,000

Accounts receivable……………..………................ 63,000 52,500

Inventory………………………………………………..... 67,500 90,000

Accounts payable…….………..…………................ 35,100 27,000

Sales……………………………………………………..…. 187,500 150,000

Equipment……………………………………………...… 165,000 125,000

170. Comparative statements for Warmer Corporation are shown below:

Warmer Corporation

Comparative Income Statements

For the years ended December 31

2016 2015 2014

Sales……………..…………………............................ $14,800 $13,229 $13,994

Cost of goods sold……..………..…....................... 8,225 8,661 8,375

Gross profit…………………………………………...….. 6,575 4,568 5,619

Operating expenses………..……………..…….......... 3,664 3,576 3,487

Operating income…..…..………........................... $ 2,911 $ 992 $ 2,132

Calculate trend percentages for all income statement amounts shown and comment on the

results. Use 2014 as the base year. Comment on the results.

171. Calculate the percent increases for each of the following selected balance sheet items.

2016 2015

Cash……………………………………………………………... $ 569 $ 448

Accounts receivable………………………………………… 2,234 2,337

Merchandise inventory…..………..……..................... 1,062 1,071

Plant assets………………………………………..…..……... 2,432 2,138

Bonds payable…….…..…………………....................... 1,164 1,666

Equity……………………………………………….…..…..…. 2,777 2,894

172. For the following financial statement items, calculate trend percentages using 2014 as the

base year:

2018 2017 2016 2015 2014

Sales…………………… $1,195,400 $1,118,000 $1,049,000 $963,200 $860,000

Cost of sales………….. 752,400 704,000 671,000 616,700 559,000

Gross profit……………. $443,000 $414,000 $378,000 $346,500 $301,000

173. Express the following income statement information in common-size percentages and in

trend percentages using 2014 as the base year.

Common-Size Trend

Percentages Percentages

2015 2014 2015 2014 2015 2014

Sales……..................... $540,000 $460,000 ____ ____ ____ ____

Cost of goods sold...... 290,000 240,000 ____ ____ ____ ____

Gross profit…….…….... $250,000 $220,000 ____ ____ ____ ____

174. The comparative balance sheet for Silverlight Co. is shown below. Express the balance

sheet in common-size percentages.

Silverlight Company

Comparative Balance Sheets (in $000)

December 31, 2014–2016

2016 2015 2014

Cash……………………………………………………………... $ 49.6 $ 34.2 $ 35.7

Accounts receivable………………………………………… 74.4 85.5 76.5

Merchandise inventory…..………..……..................... 148.8 125.4 91.8

Plant assets (net)…………………………………………..… 347.2 324.9 306.0

Total assets….…..…………………..….......................... $620.0 $570.0 $510.0

Accounts payable……………………………………………. $117.8 $ 51.3 $ 76.5

Bonds payable…….…..…………………....................... 130.2 159.6 107.1

Common stock……………………………………………….. 266.6 279.3 265.2

Retained earnings….…………………..…..................... 105.4 79.8 61.2

Total liabilities and equity.…..…............................. $620.0 $570.0 $510.0

175. Express the following balance sheets for Safety Company in common-size percentages.

Safety Company

Balance Sheets

December 31, 2015 and 2014

2015 2014

Assets

Cash…………………………………………..…..……..… $ 43,000 $ 22,000

Accounts receivable……………..………................ 38,000 42,000

Merchandise inventory…..………..……………....... 61,000 52,000

Prepaid insurance…….………..…………................ 6,000 9,000

Long-term investments……………………………….. 49,000 20,000

Plant assets (net)…..……………........................... 218,000 218,000

Total assets…………………………………………..…... $415,000 $363,000

Liabilities and Equity

Current liabilities………..……….......................... $ 62,000 $ 75,000

Long-term liabilities…………………………………… 45,000 36,000

Common stock…..…………………..…................... 150,000 150,000

Retained earnings………………………………….…... 158,000 102,000

Total liabilities and equity.…..…………............... $415,000 $363,000

176. Express the following income statement information in common-size percentages (round

to nearest whole percent). Comment on the results.

Haans Corp.

Comparative Income Statements

For Years Ended December 31, 2016 and 2015

2016 2015

Sales……………………………………………………..…. $1,200,000 $1,000,000

Cost of goods sold…………………………………..…. 804,000 650,000

Gross profit…….………..………………................... $ 396,000 $ 350,000

Selling expenses…………………………………….….. 132,000 120,000

Administrative expenses…..……........................ 180,000 150,000

Net income…………………………………………..…... $ 84,000 $ 80,000

177. Use the balance sheets of Glover shown below to calculate the following ratios for 2016

(round to the hundredths):

(a) Current ratio.

(b) Acid-test ratio.

(c) Debt ratio.

(d) Equity ratio.

Glover Company

Balance Sheets

December 31, 2016 and 2015

2016 2015

Assets:

Cash…………………………………………..…..……..… $ 43,000 $ 22,000

Accounts receivable……………..………................ 38,000 42,000

Merchandise inventory…..………..……………....... 61,000 52,000

Prepaid insurance…….………..…………................ 6,000 9,000

Long-term investments……………………………….. 49,000 20,000

Plant assets (net)…..……………........................... 218,000 218,000

Total assets…………………………………………..…... $415,000 $363,000

Liabilities and Equity:

Current liabilities………..……….......................... $ 62,000 $ 75,000

Long-term liabilities…………………………………… 45,000 36,000

Common stock…..…………………..…................... 150,000 150,000

Retained earnings………………………………….…... 158,000 102,000

Total liabilities and equity.…..…………............... $415,000 $363,000

178. The following information is available for the Starr Corporation:

Sales……………………………………………………. $750,000

Cost of goods sold……….……………………….. 450,000

Gross profit……………………………….…………. 300,000

Operating income……….………………………… 85,000

Net income………………………………………..…. 42,000

Inventory, beginning-year………………………. 71,200

Inventory, end-of-year…………………………… 48,800

Calculate the company’s inventory turnover and its days’ sales in inventory.

179. The following current year information is available from a manufacturing company:

Sales…………………………………………..……….. $740,000

Gross profit on sales……………………………… 276,000

Operating income……………………….………… 64,000

Income before taxes….…….……………………. 44,000

Net income………………………………………….. 33,600

Accounts Receivable, beginning-year……… 58,000

Accounts Receivable, end-of-year…..……… 72,000

Calculate the company’s accounts receivable turnover and its days’ sales uncollected.

180. Information from a manufacturing company’s current year income statement follows.

Calculate the company’s (a) profit margin ratio, (b) gross margin ratio, and (c) times interest

earned.

Blooms: Apply

AACSB: Analytic

AICPA BB: Resource

Management

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: 13-P3

Topic: Ratio Analysis

181. A company

reported net income

of $78,000 and had

15,000 common

shares outstanding

throughout the

current year. At year-

end, the price per share of the company’s stock was $49.40. What is the company’s year-end

price-earnings ratio?

Answer: Earnings per share = $78,000/15,000 shares = $5.20 per share

Price-earnings ratio = $49.40/$5.20 = 9.5

Blooms: Apply

AACSB: Analytic

AICPA BB: Resource Management

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: 13-P3

Topic: Ratio Analysis

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-95

Sales……………………………….………………….. $850,000

Cost of goods sold……….……………………….

455,000

Gross profit…………………………….…………… $395,000

Operating expenses………………………….……

260,000

Operating income……….……………………….. $ 135,000

Interest expense…………………………………….

32,000

Income before taxes……………………………... $103,000

Income taxes expense……………………………

12,400

Net income………………………………………….. $ 90,600

Answer:

(a) $90,600/$850,000 = 10.7%

(b) $395,000/$850,000 = 46.5%

(c) $135,000/$32,000 = 4.2

182. A company paid cash dividends on its preferred stock of $40,000 in the current year

when its net income was $120,000 and its average common stockholders’ equity was

$640,000. What is the company’s return on common stockholders’ equity?

183. Use the financial data shown below to calculate the following ratios for the current year:

(a) Current ratio.

(b) Acid-test ratio.

(c) Accounts receivable turnover.

(d) Days’ sales uncollected.

(e) Inventory turnover.

(f) Days’ sales in inventory.

Income statement data

Sales (all on credit)………………………………… $650,000

Cost of goods sold…………………………………. 425,000

Income before taxes……………………………….. 78,000

Net income………………………………………… 54,600

Ending

Balances

Beginning

Balances

Cash…………………………………………………….. $ 19,500 $ 15,000

Accounts receivable (net) ……………………… 65,000 60,000

Inventory………………………………….………….. 71,500 64,500

Plant and equipment (net)…………………….…

195,000

183,900

Total assets……………………….………………….. $351,000 $323,400

Current liabilities ….….………………………….. $ 62,400 $ 52,700

Long-term notes payable…..….……………….. 97,500 100,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-96

184. A company’s calendar-year financial data are shown below. The company had total assets

of $339,000 and total equity of $144,400 for the prior year. No additional shares of common

stock were issued during the year. The December 31 market price per share is $49.50. Cash

dividends of $19,500 were paid during the year. Calculate the following ratios for the

company:

(a) profit margin ratio

(b) gross margin ratio

(c) return on total assets

(d) return on common stockholders’ equity

(e) book value per common share

(f) basic earnings per share

(g) price earnings ratio

(h) dividend yield.

Net sales………………………………………………...… $650,000

Cost of goods sold…………………………………..…. 422,500

Gross profit………………………………....…..…..….. $227,500

Operating expenses………..………….................... 140,500

Operating income………………………………….…... $ 87,000

Interest expense…………………………………………. 9,100

Income before taxes…………………..................... $ 77,900

Income taxes………..…………………..................... 23,400

Net income…………………………………………..…... $ 54,500

Ending

Balances

Cash…………………………………………..…..……..… $ 19,500

Accounts receivable (net)………………………..….. 65,000

Inventory………………………………………………..... 71,500

Plant assets (net)…..……………........................... 195,000

Total assets…………………………………………..…... $351,000

Current liabilities………..……….......................... $ 74,100

Long-term notes payable…..…………………......... 97,500

Common stock, $5 par value …..………..…......... 65,000

Retained earnings………………………………….…... 114,400

Total liabilities and equity.…..…………............... $351,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-98

185. A company’s calendar-year financial data are shown below. The company had total assets

of $339,000 and total equity of $144,400 for the prior year. No additional shares of common

stock were issued during the year. The December 31 market price per share is $49.50. Cash

dividends of $19,500 were paid during the year. Calculate the following ratios for the

company:

(a) debt ratio

(b) equity ratio

(c) debt-to-equity ratio

(d) times interest earned

(e) total asset turnover

Net sales………………………………………………...… $650,000

Cost of goods sold…………………………………..…. 422,500

Gross profit………………………………....…..…..….. $227,500

Operating expenses………..………….................... 140,500

Operating income………………………………….…... $ 87,000

Interest expense…………………………………………. 9,100

Income before taxes…………………..................... $ 77,900

Income taxes………..…………………..................... 23,400

Net income…………………………………………..…... $ 54,500

Ending

Balances

Cash…………………………………………..…..……..… $ 19,500

Accounts receivable (net)………………………..….. 65,000

Inventory………………………………………………..... 71,500

Plant assets (net)…..……………........................... 195,000

Total assets…………………………………………..…... $351,000

Current liabilities………..……….......................... $ 74,100

Long-term notes payable…..…………………......... 97,500

Common stock, $5 par value …..………..…......... 65,000

Retained earnings………………………………….…... 114,400

Total liabilities and equity.…..…………............... $351,000

186. Comparative calendar-year financial data for a company are shown below. Calculate the

following ratios for the company for 2016:

(a) accounts receivable turnover

(b) day’s sales uncollected

(c) inventory turnover

(d) days’ sales in inventory

2016 2015

Sales……………………………………………………..…. $ 720,000 $607,500

Cost of goods sold…………………………………..…. 450,000 382,700

Operating expenses………..………….................... 168,500 134,900

Net income…………………………………………..…... 51,200 51,700

December 31, December 31,

2016 2015

Accounts receivable (net)….…..……………..…..... $ 157,500 $162,500

Inventory………………………………………………..... 139,500 110,500

Total assets…………………………………………..…... 1,012,500 944,800

187. Comparative calendar year financial data for a company are shown below. Calculate the

following ratios for 2016:

(a) return on total assets

(b) return on common stockholders’ equity.

2016 2015

Sales……………………………………………………..…. $ 720,000 $ 607,500

Gross profit…….………..………………................... 270,000 224,800

Income before taxes…………………..................... 79,200 78,700

Net income…………………………………………..…... 51,200 51,700

December 31, December 31,

2016 2015

Liabilities……………………………………..…..……... $ 493,500 $ 452,500

Common stock ($12 par)…….………..…………..... 180,000 180,000

Contributed capital in excess of par.................. 135,000 135,000

Retained earnings………………………………….…... 204,000 177,300

Total liabilities and equity.…..…………............... $1,012,500 $ 944,800

188. The current year-end balance sheet data for a company are shown below. Calculate the

company’s:

(a) working capital

(b) current ratio

(c) acid-test ratio.

Assets:

Cash………………………………………………………….. $ 38,000

Marketable securities……………………................. 45,000

Accounts receivable (net)….………..................... 127,500

Merchandise inventory………….......................... 149,500

Long-term investments…………..…..................... 135,000

Plant assets (net)….…………………....................... 517,500

Total assets………………………………………...…..…. $ 1,012,500

Liabilities and equity:

Accounts payable………………………………..……... $ 148,700

Accrued liabilities……………………………...…..….. 90,000

Notes payable (secured by plant assets) 254,800

Common stock ($12 par)……..…........................ 180,000

Contributed capital in excess of par.................. 135,000

Retained earnings……………………………………..... 204,000

Total liabilities and equity.….............................. $

1,012,500

189. The comparative income statements for Silverlight Company are shown below. Calculate

the following ratios for 2016:

(a) profit margin

(b) gross margin

(c) times interest earned.

Silverlight Company

Income Statements

For Years Ended December 31,

2016 2015

Net sales………………………………………………...… $720,000 $607,500

Cost of goods sold…………………………………..…. 450,000 382,700

Gross profit…….………..………………................... $270,000 $224,800

Operating expense……………………………………... 168,500 134,900

Income from operations…………........................ $101,500 $ 89,900

Interest expense…………………………………………. 22,300 11,200

Income before taxes…………………..................... $ 79,200 $ 78,700

Income taxes………..…………………..................... 28,000 27,000

Net income…………………………………………..…... $ 51,200 $ 51,700

190. A corporation reports the following year-end balance sheet data. Calculate the following

ratios:

(a) working capital

(b) acid-test ratio

(c) current ratio

(d) debt ratio

(e) equity ratio

(f) debt-to-equity ratio

Cash……………………….. $ 50,000 Current liabilities……………..………….. $ 64,000

Accounts receivable………. 35,000 Long-term liabilities………..…………….72,000

Inventory………………….. 60,000 Common stock……………...…………..100,000

Equipment………………… 140,000

Retained earnings………………………….49 ,000

Total assets……………….. $285,000

Total liabilities and equity…..…….$285 ,000

191. Selected balances from a company’s financial statements are shown below. Calculate the

following ratios for 2016:

(a) accounts receivable turnover

(b) inventory turnover

(c) days’ sales uncollected

(d) days’ sales in inventory

(d) profit margin.

(e) return on total assets.

Dec. 31, Dec. 31, For the

2016 2015 Year 2016

Accounts receivable……………..………................ $ 27,000 $ 24,000

Merchandise inventory…..………..……………....... 25,000 20,000

Total assets…………………………………………..…... 296,000 244,000

Accounts payable…….………..…………................ 26,000 32,000

Salaries payable……………..…............................ 3,000 4,400

Sales (all on credit)…..…..……........................... $312,000

Cost of goods sold…………………………………..…. 165,600

Salaries expense………………………………....…..… 48,000

Other expenses……………………………….…..…..… 75,000

Net income…………………………………………..…... 24,000

192. The following selected financial information for a company was reported for the current

year end. Calculate the following company ratios:

(a) Accounts receivable turnover.

(b) Inventory turnover.

(c) Days’ sales uncollected

Accounts receivable, beginning-year……………. $170,000

Accounts receivable, year-end…………………… 190,000

Merchandise inventory, beginning-year…………. 80,000

Merchandise inventory, year-end………………… 60,000

Cost of goods sold………………………………… 580,000

Credit sales………………………………………… 1,000,000

193. Selected current year end financial information for a company is presented below.

Calculate the following company ratios:

(a) Profit margin.

(b) Total asset turnover.

(c) Return on total assets.

(d) Return on common stockholders’ equity (assume the company has no preferred stock).

Net income……………………………….. $ 325,000

Net sales………………………………….. 4,700,000

Total liabilities, beginning-year………….. 550,000

Total liabilities, end-of-year……………… 530,000

Total stockholders’ equity, beginning-year. 760,000

Total stockholders’ equity, end-of-year….. 745,000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-107

194. Use the following information from the current year financial statements of a company to

calculate the ratios below:

(a) Current ratio.

(b) Accounts receivable turnover. (Assume the prior year’s accounts receivable balance was

$100,000.)

(c) Days’ sales uncollected.

(d) Inventory turnover. (Assume the prior year’s inventory was $50,200.)

(e) Times interest earned ratio.

(f) Return on common stockholders’ equity. (Assume the prior year’s common stock balance

was $480,000 and the retained earnings balance was $128,000.)

(g) Earnings per share (assuming the corporation has a simple capital structure, with only

common stock outstanding).

(h) Price earnings ratio. (Assume the company’s stock is selling for $26 per share.)

(i) Divided yield ratio. (Assume that the company paid $1.25 per share in cash dividends.)

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-108

Income statement data:

Sales (all on credit) ..…..………………................. $1,075,000

Cost of goods sold.……………............................ 575,000

Gross profit on sales………………….................... $ 500,000

Operating expenses………………………………..…..

305,000

Operating income…..………..….......................... $ 195,000

Interest expense….………..………........................ 20,400

Income before taxes………………………………..…. $ 174,600

Income taxes…………………………………..…..….... 74,000

Net income..………..……………........................... $ 100,600

Balance sheet data:

Cash $ 38,400

Accounts receivable 120,000

Inventory 56,700

Prepaid Expenses 24,000

Total current assets $239,100

Total plant assets 708,900

Total assets $948,000

Accounts payable $ 91,200

Interest payable 4,800

Long-term liabilities 204,000

Total liabilities $300,000

Common stock, $10 par 480,000

Retained earnings 168,000

Total liabilities and equity $948,000

195. Financial information for Sigma Company is presented below. Calculate the following

ratios for 2016:

(a) Inventory turnover.

(b) Accounts receivable turnover.

(c) Return on total assets.

(d) Times interest earned.

(e) Total asset turnover.

2016 2015

Assets:

Cash…………………………………………..…..……..… $ 18,000 $ 22,000

Marketable securities…..……….......................... 25,000 0

Accounts receivable……………..………................ 38,000 42,000

Inventory………………………………………………..... 61,000 52,000

Prepaid insurance…….………..…………................ 6,000 9,000

Long-term investments……………………………….. 49,000 20,000

Plant assets, net……………..……………................. 218,000 225,000

Total assets…………………………………………..…... $415,000 $370,000

Net income…………………………………………..…... $ 62,250

Sales (all on credit)…..…..……........................... 305,000

Cost of goods sold…………………………………..…. 123,000

Interest expense…………………………………………. 15,600

Income tax expense………………………………….... 27,000

196. The following summaries from the income statements and balance sheets of Kouris

Company and Brittania, Inc. are presented below.

(1) For both companies for 2016, compute the:

(a) Current ratio

(b) Acid-test ratio

(c) Accounts receivable turnover

(d) Inventory turnover

(e) Days’ sales in inventory

(f) Days’ sales uncollected

Which company do you consider to be the better short-term credit risk? Explain.

(2) For both companies for 2016, compute the:

(a) Profit margin ratio

(b) Return on total assets

(c) Return on common stockholders’ equity

Which company do you consider to have better profitability ratios?

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-112

Kouris Company Consolidated Balance Sheets

(in millions)

May 31

2016 2015

Assets

Current assets:

Cash and cash equivalents…..…………………..……….................. $ 634.0 $575.5

Accounts receivable, net of allowance….…..……………..…........ 2,101.1 1,804.1

Inventories………………………………………………………………....… 1,514.9 1,373.8

Other current assets………..…………………..………...................... 429.9 401.3

Total current assets……………………..…………......................... 4,679.9 4,154.7

Property, plant, and equipment, net..…..……………....................... 1,620.8 1,614.5

Other long term assets…………………………………………...…..……... 413.2 670.8

Total assets……………………………………………..…..…..…..……... $6,713.9 $6,440.0

Liabilities and Stockholders’ Equity

Current liabilities:

Current portion of long-term debt…………………………………..... $ 205.7 $ 55.3

Notes payable……………………………………………………..…..….... 75.4 425.2

Accounts payable………………………………………………………...… 572.7 504.4

Accrued liabilities……………………………………………………..…... 1,054.2 765.3

Income taxes payable…………………..…………........................... 107.2 83.0

Total current liabilities……………………………………………..….. 2,015.2 1,833.2

Long term liabilities……………………………………….…..…..…..….... 708.0 767.8

Total liabilities………………………………………………………..….. 2,723.2 2,601.0

Stockholders’ equity:

Common stock………………………………………………………………. 2.8 2.8

Contributed capital in excess of par value………...................... 589.0 538.7

Unearned stock compensation….……………..……….................. (0.6) (5.1)

Accumulated other comprehensive loss..……………..…….......... (239.7) (192.4)

Retained earnings………………………………………….…..……..…... 3,639.2 3,495.0

Total stockholders’ equity……………………………………..…..….. 3,990.7 3,839.0

Total liabilities and stockholders’ equity.……………..……….... $6,713.9 $6,440.0

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-113

Kouris Company

Consolidated Statement of Income

May 31, 2016

(in millions)

Revenues……………………………………………………………………. $10,697.0

Cost of sales……………………………………………………….…..….. 6,313.6

Gross profit……………………………………………………..…..…..… 4,383.4

Operating expenses………………………………………….…..…..…. 3,137.6

Operating income……………………………………………………..…. 1,245.8

Interest expense…………………………………………………………… 42.9

Other revenues and expenses……………..………...................... 79.9

Income before tax…..………..…………………............................ 1,123.0

Income taxes………………………………………………….…..…….... 382.9

Income before effect of accounting change.………………........ 740.1

Cumulative effect of accounting change, net of tax.............. 266.1

Net income…………………………………………………………………. $ 474.0

Brittania, Inc.

Consolidated Balance Sheets

Jan. 3, Jan. 4,

2016 2015

Assets

Current assets:

Cash and cash equivalents…..…………………..……….................. $34.5 $22.2

Accounts receivable, net of allowance….…..……………..…........ 15.5 14.7

Inventories………………………………………………………………....… 27.2 28.4

Other current assets……………………………………..……..…..…..… 3.5 4.2

Total current assets……………………..…………......................... 80.7 69.5

Property, plant, and equipment, net..…..……………....................... 5.7 7.0

Other long term assets…………………………………………...…..……... 1.1 1.5

Total assets……………………………………………..…..…..…..……... $87.5 $78.0

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-114

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable………………………………………………………...… $ 8.5 $ 6.6

Accrued liabilities……………………………………………………..…... 7.8 5.6

Total current liabilities……………………………………………..….. 16.3 12.2

Long term liabilities……………………………………….…..…..…..….... 2.5 2.6

Total liabilities………………………………………………………..….. 18.8 14.8

Stockholders’ equity:

Common stock………………………………………………………………. 2.3 2.3

Contributed capital in excess of par value………...................... 17.8 17.4

Unearned stock compensation….……………..……….................. (0.1) (0.5)

Accumulated other comprehensive loss..……………..…….......... (0.9) (1.3)

Treasury stock…………………………………………..……..…..…..….. (6.3) (5.4)

Retained earnings………………………………………….…..……..…... 55.9 50.7

Total stockholders’ equity……………………………………..…..….. 68.7 63.2

Total liabilities and stockholders’ equity.……………..……….... $87.5 $78.0

Brittania, Inc.

Consolidated Statement of Income

January 3, 2016

(in millions)

Revenues…………………………………………………………………….

$133.5

Cost of sales……………………………………………………….…..…..

87.3

Gross profit……………………………………………………..…..…..…

46.2

Operating expenses………………………………………….…..…..….

37.3

Operating income……………………………………………………..….

8.9

Interest expense……………………………………………………………

(0.1)

Other revenues and expenses……………..………......................

0.3

Income before tax…..………..…………………............................

9.1

Income taxes………………………………………………….…..……....

3.9

Net income………………………………………………………………….

$ 5.2

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13-115

197. _________________ applies analytical tools to general-purpose financial statements and

related data for making business decisions.

198. A common focus of financial statement users in evaluating a company’s performance and

financial condition includes evaluating its (1) __________________, (2) ______________,

and (3) ___________________.