Appendix D

ACCOUNTING FOR PARTNERSHIPS

True /False Questions

1. A partnership has a limited life.

2. A partnership is an incorporated association of two or more people to pursue a business for

profit as co-owners.

3. Mutual agency means each partner can commit or bind the partnership to any contract

within the scope of the partnership business.

4. Accounting procedures for both C corporations and S corporations are the same in all

aspects.

5. Partners in a partnership are taxed on the partnership income, not the amounts they

withdraw from the partnership.

6. Limited liability partnerships are designed to protect innocent partners from malpractice or

negligence claims resulting from the acts of another partner.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-2

7. A partnership may allocate salary allowances to the partners reflecting the relative value of

services provided.

8. In a limited partnership the general partner has unlimited liability.

9. Partner return on equity can be used by each partner to help decide whether additional

investment or withdrawal of resources is best for that partner.

10. Feldt is a partner in Feldt &Dodson Company. Feldt’s share of the partnership income is

$18,600 and her average partnership equity is $155,000. Her partner return on equity equals

8.33.

11. When partners invest in a partnership, their capital accounts are debited for the amount

invested.

12. Partners’ withdrawals are debited to their separate withdrawals accounts.

13. Partners can invest assets but not liabilities into a partnership.

14. The withdrawals account of each partner is closed to retained earnings at the end of the

accounting period.

15. In closing the accounts at the end of a period, the partners’ capital accounts are credited

for their share of the partnership net income or debited for their share of the partnership loss.

16. In the absence of a partnership agreement, the law says that income of a partnership will

be shared equally by the partners.

17. Salary allowances are reported as salaries expense on a partnership income statement.

18. The statement of changes in partners’ equity shows the beginning balance in retained

earnings, plus investments, less withdrawals, plus the income (or less the loss) and the ending

balance in retained earnings.

19. The equity section of the balance sheet of a partnership can report the separate capital

account balances of each partner.

20. Even if partners devote their time and services to their partnership, their salaries are not

expenses on the income statement.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-7

21. If the partners agree on a formula to share income and say nothing about losses, then the

losses are shared using the same formula.

22. Assume that the M & L partnership agreement gave March 60% and Ludwig 40% of

partnership income and losses. The partnership lost $27,000 in the current period. This

implies that March’s share of the loss equals $16,200, and Ludwig’s share equals $10,800.

23. When a partner leaves a partnership, the present partnership ends.

24. To buy into an existing partnership, the new partner must contribute cash to the

partnership.

25. When a partner leaves a partnership, the present partnership ends, but the business can

still continue to operate.

26. Assets invested by a partner into a partnership become the property of the business.

27. Admitting a partner by accepting assets is a personal transaction between one or more

current partners and the new partner.

28. Current partners usually require any new partner to pay a bonus for the privilege of

joining when the current value of a partnership is greater than the recorded amounts of equity.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-10

29. When a partner leaves a partnership, the withdrawing partner is entitled to a bonus if the

recorded equity is overstated.

30. When a partnership is liquidated, its business is ended.

31. A capital deficiency exists when at least one partner has a debit balance in his or her

capital account at the point of final cash distribution during liquidation.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-11

32. A capital deficiency can arise from liquidation losses, excessive withdrawals before

liquidation, or recurring losses in prior periods.

33. If a partner is unable to cover a deficiency and the other partners absorb the deficiency,

then the partner with the deficiency is thus relieved of all liability.

34. If at the time of partnership liquidation, a partner has a $5,000 capital deficiency and pays

the partnership $5,000 out of personal assets to cover the deficiency, then that partner is

entitled to share in the final distribution of cash.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-12

35. An unincorporated association of two or more persons to pursue a business for profit as

co-owners is a:

A. Partnership.

B. Proprietorship.

C. Contractual company.

D. Mutual agency.

E. Voluntary organization.

36. Advantages of a partnership include:

A. Limited life.

B. Mutual agency.

C. Unlimited liability.

D. Co-ownership of property.

E. Voluntary association.

37. A partnership agreement:

A. Is not binding unless it is in writing.

B. Is the same as a limited liability partnership.

C. Is binding even if it is not in writing.

D. Does not generally address the issue of the rights and duties of the partners.

E. Is also called the articles of incorporation.

38. Mutual agency means

A. Creditors can apply their claims to partners’ personal assets.

B. Partners are taxed on partnership withdrawals.

C. All partners must agree before the partnership can act.

D. The partnership has a limited life.

E. A partner can commit or bind the partnership in any contract within the scope of the

partnership business.

39. A partnership that has two classes of partners, general and limited, where the limited

partners have no personal liability beyond the amounts they invest in the partnership, and no

active role in the partnership, except as specified in the partnership agreement is a:

A. Mutual agency partnership.

B. Limited partnership.

C. Limited liability partnership.

D. General partnership.

E. Limited liability company.

40. A partnership designed to protect innocent partners from malpractice or negligence claims

resulting from acts of another partner is a(n):

A. Partnership.

B. Limited partnership.

C. Limited liability partnership.

D. General partnership.

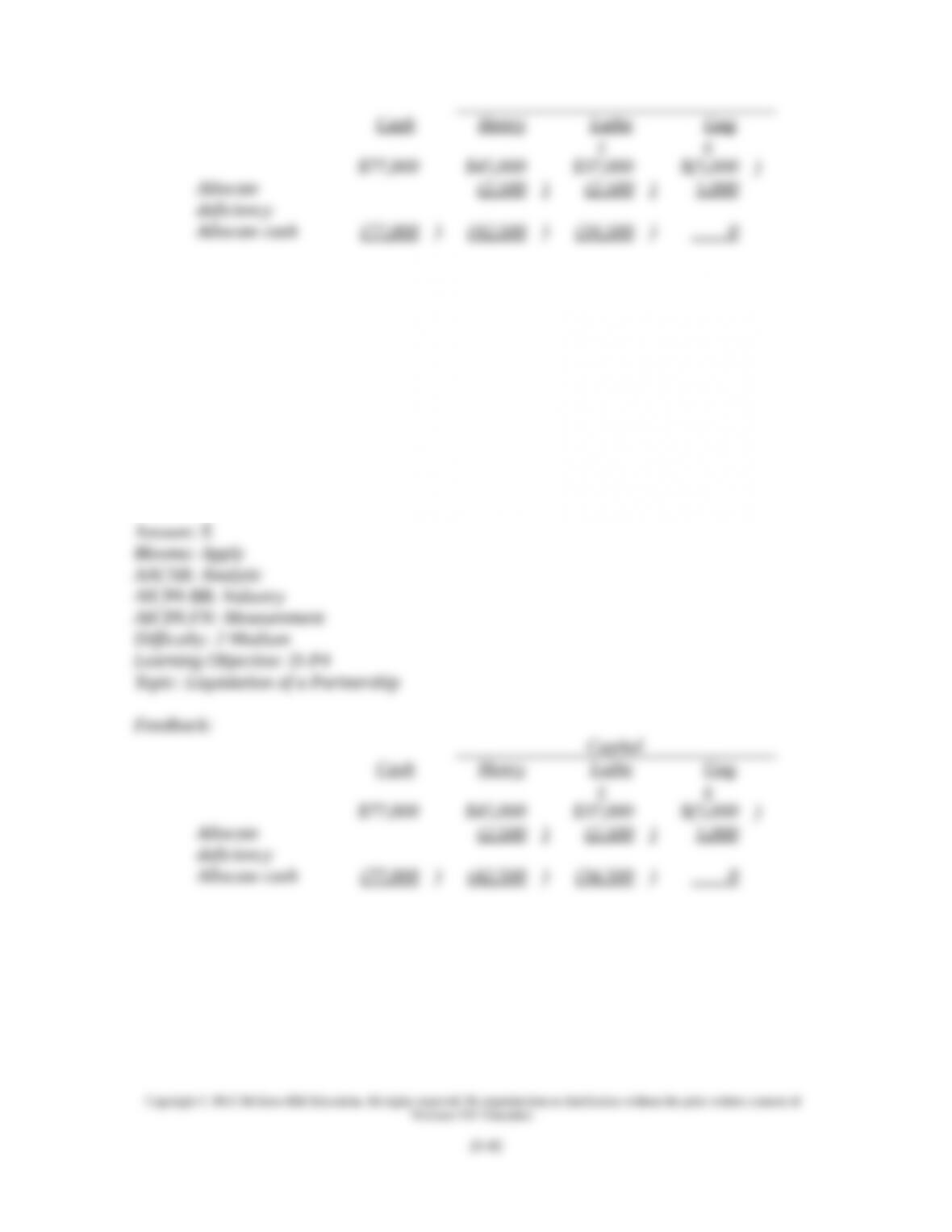

E. Unlimited liability company.

41. Mutual agency implies that each partner in a partnership is a fully authorized agent of the

partnership. Which of the following statements is correct regarding the authority of a partner

to bind the partnership in dealings with third parties?

A. The partner’s authority must be derived from the partnership agreement.

B. The partner’s authority may be effectively limited by a formal resolution of the other

partners, even if third parties are not aware of that limitation.

C. Only a partner with a majority interest in a partnership has the authority to represent the

partnership to third parties.

D. A partner has authority to deal with third parties on the behalf of the other partners only if

he has written permission to do so.

E. A partner may be able to legally bind the partnership to actions even if the other partners

are unaware of his actions.

42. Pat and Nicole formed Here & There as a limited liability company. Unless the member

owners elect to be treated otherwise, the Internal Revenue Service will tax the LLC as:

A. An S corporation.

B. A C corporation.

C. A non-taxable entity.

D. A joint venture.

E. A partnership.

43. A partnership in which all partners have mutual agency and unlimited liability is called:

A. Limited partnership.

B. Limited liability partnership.

C. General partnership.

D. S corporation.

E. Limited liability company.

44. Carter Pearson is a partner in Event Promoters. His beginning partnership capital balance

for the current year is $55,000, and his ending partnership capital balance for the current year

is $62,000. His share of this year’s partnership income was $6,250. What is his partner return

on equity?

A. 5.34%

B. 8.93%

C. 10.08%

D. 11.36%

E. 10.68%

45. Design Services is organized as a limited partnership, with Miko Toori as one of its

partners. Miko’s capital account began the year with a balance of $35,000. During the year,

Miko’s share of the partnership income was $7,500, and Miko received $4,000 in distributions

from the partnership. What is Miko’s partner return on equity?

A. 10.2%

B. 22.7%

C. 19.5%

D. 20.4%

E. 21.4%

46. The following information is available regarding Grace Smit’s capital account in

Enterprise Consulting Group, a general partnership, for a recent year:

Beginning of the year balance $22,000

Share of partnership income

$ 8,500

Withdrawals made during the year $ 6,000

What is Smit’s partner return on equity during the year in question?

A. 36.6%

B. 34.7%

C. 10.8%

D. 11.4%

E. 55.7%

47. Partnership accounting does not:

A. Use a capital account for each partner.

B. Use a withdrawals account for each partner.

C. Allocate net income to each partner according to the partnership agreement.

D. Allocate net loss to each partner according to the partnership agreement.

E. Tax the business entity.

48. Partnership accounting is the same as accounting for:

A. A sole proprietorship.

B. A corporation.

C. A sole proprietorship, except that separate capital and withdrawal accounts are kept for

each partner.

D. An S corporation.

E. A corporation, except that retained earnings is used to keep track of partners’ withdrawals.

49. Partners’ withdrawals of assets are:

A. Credited to their withdrawals accounts.

B. Debited to their withdrawals accounts.

C. Credited to their retained earnings.

D. Debited to their retained earnings.

E. Debited to their asset accounts.

50. The withdrawals account of each partner is:

A. Closed to that partner’s capital account with a credit.

B. Closed to that partner’s capital account with a debit.

C. A permanent account that is not closed.

D. Credited with that partner’s share of net income.

E. Debited with that partner’s share of net loss.

51. R. Stetson contributed $14,000 in cash plus office equipment valued at $7,000 to the SJ

Partnership. The journal entry to record the transaction for the partnership is:

A. Debit Cash $14,000; debit Office Equipment $7,000; credit R Stetson, Capital $21,000.

B. Debit Cash $14,000; debit Office Equipment $7,000; credit SJ Partnership, Capital

$21,000

C. Debit SJ Partnership $21,000; credit R. Stetson, Capital $21,000.

D. Debit R. Stetson, Capital $21,000; credit SJ Partnership, Capital $21,000.

E. Debit Cash $14,000; debit Office Equipment $7,000; credit Common Stock $21,000

52. T. Andrews contributed $14,000 in to the T & B Partnership. The journal entry to record

the transaction for the partnership is:

A. Debit Cash $14,000; credit T & B Partnership, Capital $14,000.

B. Debit Cash $14,000; credit T. Andrews, Capital $14,000

C. Debit T & B Partnership $14,000; credit T. Andrews, Capital $14,000.

D. Debit T. Andrews, Capital $14,000; credit T & B Partnership, Capital $14,000.

E. Debit Cash $14,000; credit Common Stock $14,000

53. Forman and Berry are forming a partnership. Forman will invest a building that currently

is being used by another business owned by Forman. The building has a market value of

$80,000. Also, the partnership will assume responsibility for a $20,000 note secured by a

mortgage on that building. Berry will invest $50,000 cash. For the partnership, the amounts to

be recorded for the building and for Forman’s Capital account are:

A. Building, $80,000 and Forman, Capital, $80,000.

B. Building, $60,000 and Forman, Capital, $60,000.

C. Building, $60,000 and Forman, Capital, $50,000.

D. Building, $80,000 and Forman, Capital, $60,000.

E. Building, $60,000 and Forman, Capital, $80,000.

54. Maxwell and Smart are forming a partnership. Maxwell is investing a building that has a

market value of $180,000. However, the building carries a $56,000 mortgage that will be

assumed by the partnership. Smart is investing $120,000 cash. The balance of Maxwell’s

Capital account will be:

A. $180,000.

B. $124,000.

C. $56,000.

D. $64,000.

E. $60,000.

55. Harvey and Quick have decided to form a partnership. Harvey is going to contribute a

depreciable asset to the partnership as his equity contribution to the partnership. The

following information regarding the asset to be contributed by Harvey is available:

Historical cost of the asset $76,000

Accumulated depreciation on the asset $40,000

Note payable secured by the asset* $18,000

Agreed-upon market value of the asset $45,000

*will be assumed by the partnership

Based on this information, Harvey’s beginning equity balance in the partnership will be:

A. $76,000

B. $36,000

C. $18,000

D. $27,000

E. $45,000

56. Dalworth and Minor have decided to form a partnership. Minor is going to contribute a

depreciable asset to the partnership as her equity contribution to the partnership. The

following information regarding the asset to be contributed by Minor is available:

Historical cost of the asset…………………………………………….… $276,000

Accumulated depreciation on the asset…………………………………. $140,000

Note payable secured by the asset and assumed by the partnership…….. $118,000

Agreed-upon market value of the asset………………………………….. $245,000

Based on this information, Minor’s beginning equity balance in the partnership will be:

A. $276,000

B. $158,000

C. $136,000

D. $127,000

E. $18,000

57. In the absence of a partnership agreement, the law says that income (and loss) should be

allocated based on:

A. A fractional basis.

B. The ratio of capital investments.

C. Salary allowances.

D. Equal shares.

E. Interest allowances.

58. In a partnership agreement, if the partners agreed to an interest allowance of 10% annually

on each partner’s investment, the interest allowance:

A. Is ignored when earnings are not sufficient to pay interest.

B. Can make up for unequal capital contributions.

C. Is an expense of the business.

D. Must be paid because the partnership contract has unlimited life.

E. Legally becomes a liability of the general partner.

59. Wheadon, Davis, and Singer formed a partnership with Wheadon contributing $60,000,

Davis contributing $50,000 and Singer contributing $40,000. Their partnership agreement

called for the income (loss) division to be based on the ratio of capital investments. If the

partnership had income of $75,000 for its first year of operation, what amount of income

(rounded to the nearest thousand) would be credited to Singer’s capital account?

A. $20,000.

B. $25,000.

C. $30,000.

D. $40,000.

E. $75,000.

60. Wheadon, Davis, and Singer formed a partnership with Wheadon contributing $60,000,

Davis contributing $50,000 and Singer contributing $40,000. Their partnership agreement

called for the income (loss) division to be based on the ratio of capital investments. If the

partnership had income of $75,000 for its first year of operation, what amount of income

(rounded to the nearest thousand) would be credited to Wheadon’s capital account?

A. $20,000.

B. $25,000.

C. $30,000.

D. $40,000.

E. $75,000.

61. Christie and Jergens formed a partnership with capital contributions of $300,000 and

$400,000, respectively. Their partnership agreement calls for Christie to receive a $60,000 per

year salary. Also, each partner is to receive an interest allowance equal to 10% of a partner’s

beginning capital investments. The remaining income or loss is to be divided equally. If the

net income for the current year is $135,000, then Christie and Jergens’s respective shares are:

A. $67,500; $67,500.

B. $92,500; $42,500.

C. $57,857; $77,143.

D. $90,000; $40,000.

E. $35,000; $100,000.

62. Farmer and Taylor formed a partnership with capital contributions of $200,000 and

$250,000, respectively. Their partnership agreement calls for Farmer to receive a $70,000 per

year salary. The remaining income or loss is to be divided equally. If the net income for the

current year is $135,000, then Farmer and Taylor’s respective shares are:

A. $67,500; $67,500.

B. $130,000; $5,000.

C. $106,140; $28,860.

D. $90,000; $45,000.

E. $102,500; $32,500.

63. Which of the following statements is true?

A. Partners are employees of the partnership.

B. Salaries to partners are expenses on the partnership income statement.

C. Salary allowances usually reflect the relative value of services provided by partners.

D. Salary allowances are expenses.

E. Interest allowances are expenses.

64. Zheng invested $100,000 and Murray invested $200,000 in a partnership. They agreed to

share incomes and losses by allowing a $60,000 per year salary allowance to Zheng and a

$40,000 per year salary allowance to Murray, plus an interest allowance on the partners’

beginning-year capital investments at 10%, with the balance to be shared equally. Under this

agreement, the shares of the partners when the partnership earns $105,000 in income are:

A. $52,500 to Zheng; $52,500 to Murray.

B. $35,000 to Zheng; $70,000 to Murray.

C. $57,500 to Zheng; $47,500 to Murray.

D. $42,500 to Zheng; $62,500 to Murray.

E. $70,000 to Zheng; $60,000 to Murray.

65. Brown invested $200,000 and Freeman invested $150,000 in a partnership. They agreed to

an interest allowance on the partners’ beginning-year capital investments at 10%, with the

balance to be shared equally. Under this agreement, the shares of the partners when the

partnership earns $205,000 in income are:

A. $102,500 to Brown; $102,500 to Freeman.

B. $117,143 to Brown; $87,857 to Freeman.

C. $122,500 to Brown; $82,500 to Freeman.

D. $105,000 to Brown; $100,000 to Freeman.

E. $112,750 to Brown; $92,250 to Freeman.

66. The partnership agreement for Wilson, Pickett & Nelson, a general partnership, provided

that profits be shared between the partners in the ratio of their financial contributions to the

partnership. Wilson contributed $100,000, Pickett contributed $50,000 and Nelson contributed

$50,000. In the partnership’s first year of operation, it incurred a loss of $110,000. What

amount of the partnership’s loss, rounded to the nearest dollar, should be absorbed by

Nelson?

A. $50,000

B. $27,500

C. $36,667

D. $0

E. $40,000

67. Olivia Greer is a partner in Made for You. An analysis of Greer’s capital account indicates

that during the most recent year, she withdrew $30,000 from the partnership. Her share of the

partnership’s net loss was $16,000 and she made an additional equity contribution of $10,000.

Her capital account ended the year at $150,000. What was her capital balance at the

beginning of the year?

A. $154,000

B. $170,000

C. $180,000

D. $186,000

E. $196,000

68. The following information is available on TGR Enterprises, a partnership, for the most

recent fiscal year:

Total partnership capital at beginning of the year $180,000

Partnership net income for the year $150,000

Withdrawals by partners during the year $120,000

Additional investments by partners during the year $ 60,000

There are three partners in TGR Enterprises: Tracey, Gregory and Rodgers. At the end of the

year, the partners’ capital accounts were in the ratio of 2:1:2, respectively. Compute the

ending capital balances of the three partners.

A. Tracey = $108,000; Gregory = $54,000; Rodgers = $108,000.

B. Tracey = $90,000; Gregory = $90,000; Rodgers = $90,000.

C. Tracey = $204,000; Gregory = $102,000; Rodgers = $204,000.

D. Tracey = $84,000; Gregory = $102,000; Rodgers = $84,000.

E. Tracey = $60,000; Gregory = $30,000; Rodgers = $60,000.

69. The following information is available on PDC Enterprises, a partnership, for the most

recent fiscal year:

Total partnership capital at beginning of the year $1,080,000

Partnership net income for the year $1,250,000

Withdrawals by partners during the year $ 320,000

Additional investments by partners during the year $ 70,000

There are three partners in TGR Enterprises: Pearson, Darling and Cathay. At the end of the

year, the partners’ capital accounts were in the ratio of 2:2:1, respectively. Compute the

ending capital balances of Cathay.

A. $466,000.

B. $402,000.

C. $416,000.

D. $544,000.

E. $388,000.

70. A partner can withdraw from a partnership by any of the following means except:

A. Selling his/her interest to another person for cash.

B. Selling his/her interest to another person in exchange for assets.

C. Receiving cash from the partnership in the amount of his/her interest.

D. Receiving assets from the partnership in the amount of his/her interest.

E. Close the business and liquidate the assets under the mutual agency principle.

71. A bonus may be paid in all of the following situations except:

A. By a new partner when the current value of a partnership is greater than the recorded

amounts of equity.

B. By a withdrawing partner to remaining partners if the recorded value of the equity is

overstated.

C. To a new partner with exceptional talents.

D. By remaining partners to a withdrawing partner if the recorded equity is understated.

E. By an existing partner to him or herself when in need of personal cash flow.

72. When a partner is added to a partnership:

A. The previous partnership ends.

B. The underlying business operations end.

C. The underlying business operations must close and then re-open.

D. The partnership must continue.

E. The partnership equity always increases.

73. A partnership recorded the following journal entry:

Cash………………………………………………………………………………….… 60,000

B. Founder, Capital………………………………………………………….……. 10,000

R. Aqui, Capital………………………………………………….………….…….. 10,000

H. Joiner, Capital…………………………………………….. 80,000

This entry reflects:

A. Acceptance of a new partner who invests $60,000 and receives a $20,000 bonus.

B. Withdrawal of a partner who pays a $10,000 bonus to each of the other partners.

C. Addition of a partner who pays a bonus to each of the other partners.

D. Additional investment into the partnership by Founder and Aqui.

E. Withdrawal of $10,000 each by Founder and Aqui upon the admission of a new partner.

74. Wright, Bell, and Edison are partners and share income in a 2:5:3 ratio. The partnership’s

capital balances are as follows: Wright, $33,000, Bell $27,000 and Edison $40,000. Edison

decides to withdraw from the partnership, and the partners agree not to revalue the assets

upon Edison’s retirement. The journal entry to record Edison’s June 1 withdrawal from the

partnership if Edison sells his interest to Whitney for $45,000 after the other two partners

approve Whitney as partner is:

A. Debit Edison, Capital $45,000; credit Whitney, Capital $45,000.

B. Debit Edison, Capital $40,000; credit Cash $40,000.

C. Debit Edison, Capital $40,000; debit Wright, Capital $2,500; debit Bell, Capital $2,500;

credit Whitney, Capital $45,000.

D. Debit Edison, Capital $40,000; credit Whitney, Capital $40,000.

E. Debit Edison, Capital $40,000; debit Cash $5,000; credit Whitney, Capital $45,000.

75. Wright, Bell, and Edison are partners and share income in a 2:5:3 ratio. The partnership’s

capital balances are as follows: Wright, $33,000, Bell $27,000 and Edison $40,000. Edison

decides to withdraw from the partnership, and the partners agree not to revalue the assets

upon Edison’s retirement. The journal entry to record Edison’s June 1 withdrawal from the

partnership if Edison is paid $40,000 for his equity is:

A. Debit Edison, Capital $40,000; credit Cash $40,000.

B. Debit Wright, Capital $20,000; Debit Bell, Capital $20,000; credit Cash $40,000.

C. Debit Wright, Capital $20,000; Debit Bell, Capital $20,000; credit Edison, Capital

$40,000.

D. Debit Edison, Capital $40,000; credit Wright, Capital $20,000; credit Bell, Capital

$20,000.

E. Debit Cash $40,000; credit Edison, Capital $40,000.

76. Hewlett and Martin are partners. Hewlett’s capital balance in the partnership is $64,000,

and Martin’s capital balance $67,000. Hewlett and Martin have agreed to share equally in

income or loss. The existing partners agree to accept Black with a 20% interest. Black will

invest $35,000 in the partnership. The bonus that is granted to Hewlett and Martin equals:

A. $900 each.

B. $1,500 each.

C. $600 each.

D. 600 to Hewlett; $900 to Martin.

E. $0, because Hewlett and Martin actually grant a bonus to Black.

77. Hewlett and Martin are partners. Hewlett’s capital balance in the partnership is $64,000,

and Martin’s capital balance $61,000. Hewlett and Martin have agreed to share equally in

income or loss. Hewlett and Martin agree to accept Black with a 25% interest. Black will

invest $35,000 in the partnership. The bonus that is granted to Black equals:

A. $5,000.

B. $2,500.

C. $6,667.

D. $3,333.

E. $0, because Black must actually grant a bonus to Hewlett and Martin.

78. Masters, Hardy, and Rowen are dissolving their partnership. Their partnership agreement

allocates income and losses equally among the partners. The current period’s ending capital

account balances are Masters, $15,000; Hardy, $15,000; Rowen, $(2,000). After all the assets

are sold and liabilities are paid, but before any contributions to cover any deficiencies, there is

$28,000 in cash to be distributed. Rowen pays $2,000 to cover the deficiency in his account.

The general journal entry to record the final distribution would be:

A. Debit Masters, Capital $15,000; debit Hardy, Capital $15,000; credit Cash $30,000.

B. Debit Masters, Capital $14,000; debit Hardy, Capital $14,000; credit Cash $28,000.

C. Debit Masters, Capital $15,000; debit Hardy, Capital $15,000; credit Rowen, Capital

$2,000; credit Cash $28,000.

D. Debit Cash $28,000; debit Rowen, Capital $2,000; credit Masters, Capital $15,000; credit

Hardy, Capital $15,000.

E. Debit Masters, Capital $9,334; debit Hardy, Capital $9,333; debit Rowen, Capital $9,333;

credit Cash $28,000.

79. Masters, Hardy, and Rowen are dissolving their partnership. Their partnership agreement

allocates income and losses equally among the partners. The current period’s ending capital

account balances are Masters, $15,000; Hardy, $15,000; Rowen, $30,000. After all the assets

are sold and liabilities are paid, but before any contributions to cover any deficiencies, there is

$54,000 in cash to be distributed. The general journal entry to record the final distribution

would be:

A. Debit Masters, Capital $18,000; debit Hardy, Capital $18,000; debit Rowen, Capital

$18,000; credit Cash $54,000.

B. Debit Masters, Capital $13,500; debit Hardy, Capital $13,500; debit Rowen, Capital

$27,000; credit Cash $54,000.

C. Debit Masters, Capital $15,000; debit Hardy, Capital $15,000; debit Rowen, Capital

$30,000; credit Gain from Liquidation $6,000; credit Cash $54,000.

D. Debit Cash $54,000; credit Rowen, Capital $13,500; credit Masters, Capital $13,500;

credit Hardy, Capital $27,000.

E. Debit Masters, Capital $15,000; debit Hardy, Capital $15,000; debit Rowen, Capital

$30,000; credit Retained Earnings $6000; credit Cash $54,000.

80. When a partnership is liquidated:

A. Noncash assets are distributed to partners.

B. Any gain or loss on liquidation is allocated to the partner with the highest capital account

balance.

C. Liabilities are paid or settled.

D. Any remaining cash is distributed to the partners equally.

E. The business may continue to operate.

81. A capital deficiency means that:

A. The partnership has a loss.

B. The partnership has more liabilities than assets.

C. At least one partner has a debit balance in his/her capital account.

D. At least one partner has a credit balance in his/her capital account.

E. The partnership has been sold at a loss.

82. When a partner is unable to pay a capital deficiency:

A. The partner must take out a loan to cover the deficient balance.

B. The deficiency is absorbed by the remaining partners before distribution of cash.

C. The partnership ends before distribution of cash.

D. The deficient partner is relieved of the liability.

E. The remaining partners must wait for the deficiency to be paid before cash is distributed.

83. Henry, Luther, and Gage are dissolving their partnership. Their partnership agreement

allocates each partner 1/3 of all income and losses. The current period’s ending capital

account balances are Henry, $45,000; Luther, $37,000; and Gage, $(5,000). After all assets

are sold and liabilities are paid, there is $77,000 in cash to be distributed. Gage is unable to

pay the deficiency. The journal entry to record the distribution should be:

A. Debit Henry, Capital $25,667; debit Luther, Capital $25,667; debit Gage, Capital $25,666;

credit Cash $77,000.

B. Debit Henry, Capital $42,500; debit Luther, Capital $34,500; credit Cash $77,000.

C. Debit Henry, Capital $45,000; debit Luther, Capital $37,000; credit Gage, Capital $5,000;

credit Cash $77,000.

D. Debit Cash $77,000, debit Gage, Capital $5,000, credit Henry, Capital $45,000, credit

Luther, Capital $37,000.

E. Debit Cash $77,000; credit Henry, Capital $25,667; credit Luther, Capital $25,667; credit

Gage, Capital $25,666.

84. Henry, Luther, and Gage are dissolving their partnership. Their partnership agreement

allocates each partner 1/3 of all income and losses. The current period’s ending capital

account balances are Henry, $45,000; Luther, $37,000; and Gage, $(5,000). After all assets

are sold and liabilities are paid, there is $77,000 in cash to be distributed. Gage is unable to

pay the deficiency. What amount of cash will Gage receive upon liquidation?

A. $25,667.

B. $20,667.

C. $30,667.

D. Gage will be invoiced for $5,000.

E. $0.

85. Fontaine and Monroe are forming a partnership. Fontaine invests a building that has a

market value of $250,000; the partnership assumes responsibility for a $75,000 note secured

by a mortgage on the property. Monroe invests $100,000 in cash and equipment that has a

market value of $55,000. For the partnership, the amounts recorded for the building and for

Fontaine’s Capital account are:

A. Building $250,000; Fontaine, Capital $250,000.

B. Building $175,000; Fontaine, Capital $175,000.

C. Building $250,000; Fontaine, Capital $75,000.

D. Building $250,000; Fontaine, Capital $175,000.

E. Building $175,000; Fontaine, Capital $75,000.

86. Fontaine and Monroe are forming a partnership. Fontaine invests a building that has a

market value of $250,000; the partnership assumes responsibility for a $75,000 note secured

by a mortgage on the property. Monroe invests $100,000 in cash and equipment that has a

market value of $55,000. For the partnership, the amounts recorded for Fontaine’s Capital

account and for Monroe’s Capital account are:

A. Fontaine, Capital $175; Monroe, Capital $45,000.

B. Fontaine, Capital $0; Monroe, Capital $100,000.

C. Fontaine, Capital $250,000; Monroe, Capital $100,000.

D. Fontaine, Capital $250,000; Monroe, Capital $155,000.

E. Fontaine, Capital $175,000; Monroe, Capital $155,000.

87. Fontaine and Monroe are forming a partnership. Fontaine invests a building that has a

market value of $250,000; the partnership assumes responsibility for a $75,000 note secured

by a mortgage on the property. Monroe invests $100,000 in cash and equipment that has a

market value of $55,000. For the partnership, the amounts recorded for total assets and for

total capital account are:

A. Total assets $405,000; total capital $330,000.

B. Total assets $350,000; total capital $350,000.

C. Total assets $350,000; total capital $275,000.

D. Total assets $305,000; total capital $230,000.

E. Total assets $405,000; total capital $305,000.

88. Cox, North, and Lee form a partnership. Cox contributes $180,000, North contributes

$150,000, and Lee contributes $270,000. Their partnership agreement calls for the income or

loss division to be based on the ratio of capital invested. If the partnership reports income of

$150,000 for its first year, what amount of income is credited to Cox’s capital account?

A. $50,000.

B. $64,286.

C. $45,000.

D. $36,000.

E. $60,000.

89. Cox, North, and Lee form a partnership. Cox contributes $180,000, North contributes

$150,000, and Lee contributes $270,000. Their partnership agreement calls for the income or

loss division to be based on the ratio of capital invested. If the partnership reports income of

$150,000 for its first year, what amount of income is credited to Lee’s capital account?

A. $50,000.

B. $67,500.

C. $45,000.

D. $54,000.

E. $60,000.

90. Cox, North, and Lee form a partnership. Cox contributes $180,000, North contributes

$150,000, and Lee contributes $270,000. Their partnership agreement calls for a 5% interest

allowance on the partner’s capital balances with the remaining income or loss to be allocated

equally. If the partnership reports income of $150,000 for its first year, what amount of

income is credited to North’s capital account?

A. $50,000.

B. $63,500.

C. $61,500.

D. $47,500.

E. $45,000.

91. Cox, North, and Lee form a partnership. Cox contributes $180,000, North contributes

$150,000, and Lee contributes $270,000. Their partnership agreement calls for a 5% interest

allowance on the partner’s capital balances with the remaining income or loss to be allocated

equally. If the partnership reports income of $174,000 for its first year, what amount of

income is credited to Lee’s capital account?

A. $58,000.

B. $57,000.

C. $61,500.

D. $55,500.

E. $48,000.

92. Mace and Bowen are partners and share equally in income or loss. Mace’s current capital

balance is $135,000 and Bowen’s is $120,000. Mace and Bowen agree to accept Kent with a

30% interest in the partnership. Kent invests $115,000 in the partnership. The amount

credited to Kent’s capital account is:

A. $111,000.

B. $115,000.

C. $92,500.

D. $120,000.

E. $119,000.

93. Mace and Bowen are partners and share equally in income or loss. Mace’s current capital

balance is $135,000 and Bowen’s is $120,000. Mace and Bowen agree to accept Kent with a

30% interest in the partnership. Kent invests $115,000 in the partnership. The balances in

Mace’s and Bowen’s capital accounts after admission of the new partner equal:

A. Mace $135,000; Bowen $120,000.

B. Mace $137,000; Bowen $122,000

C. Mace $133,000; Bowen $118,000.

D. Mace $139,000; Bowen $120,000.

E. Mace $135,000; Bowen $124,000.

94. Peters and Chong are partners and share equally in income or loss. Peters’ current capital

balance is $140,000 and Chong’s is $130,000. Peters and Chong agree to accept Aaron with a

30% interest in the partnership. Aaron invests $98,000 in the partnership. The balances in

Peters’s and Chong’s capital accounts after admission of the new partner equal:

A. Peters $140,000; Chong $130,000.

B. Peters $146,200; Chong $136,200.

C. Peters $145,000; Chong $135,000.

D. Peters $133,800; Chong $123,800.

E. Peters $166,027; Chong $156,027.

95. Peters and Chong are partners and share equally in income or loss. Peters’ current capital

balance is $140,000 and Chong’s is $130,000. Peters and Chong agree to accept Aaron with a

30% interest in the partnership. Aaron invests $98,000 in the partnership. The amount

credited to Aaron’s capital account is:

A. $81,000.

B. $102,600.

C. $110,400.

D. $98,000.

E. $114,533.

96. Peters, Chong, and Aaron are dissolving their partnership. Their partnership agreement

allocates each partner an equal share of all income and losses. The current period’s ending

capital account balances are Peters, $54,000; Chong, $42,000; and Aaron, $(2,000). After all

assets are sold and liabilities are paid, there is $94,000 in cash to be distributed. Aaron is

unable to pay the deficiency. The journal entry to record the distribution should be:

A. Debit Peters, Capital $54,000; debit Chong, Capital $40,000; credit Cash $94,000.

B. Debit Peters, Capital $54,000; debit Chong, Capital $42,000; credit Cash $96,000.

C. Debit Peters, Capital $53,000; debit Chong, Capital $41,000; credit Cash $94,000.

D. Debit Cash $94,000, debit Aaron, Capital $2,000, credit Peters, Capital $54,000, credit

Chong, Capital $42,000.

E. Debit Cash $94,000; credit Peters, Capital $47,000; credit Chong, Capital $47,000.

97. Barber and Atkins are partners in an accounting firm and share net income and loss

equally. Barber’s beginning partnership capital balance for the current year is $285,000, and

Atkins’ beginning partnership capital balance for the current year is $370,000. The

partnership had net income of $250,000 for the year. Barber withdrew $90,000 during the

year and Atkins withdrew $100,000. What is Barber’s ending equity?

A. $357,500

B. $362,500

C. $445,000

D. $320,000

E. $195,000

98. Barber and Atkins are partners in an accounting firm and share net income and loss

equally. Barber’s beginning partnership capital balance for the current year is $285,000, and

Atkins’ beginning partnership capital balance for the current year is $370,000. The

partnership had net income of $250,000 for the year. Barber withdrew $90,000 during the

year and Atkins withdrew $100,000. What is Barber’s return on equity?

A. 41.3%

B. 43.9%

C. 32.7%

D. 33.8%

E. 36.5%

99. Barber and Atkins are partners in an accounting firm and share net income and loss

equally. Barber’s beginning partnership capital balance for the current year is $285,000, and

Atkins’ beginning partnership capital balance for the current year is $370,000. The

partnership had net income of $250,000 for the year. Barber withdrew $90,000 during the

year and Atkins withdrew $100,000. What is Atkins’s return on equity?

A. 41.3%

B. 43.9%

C. 32.7%

D. 33.8%

E. 36.5%

100. Fellows and Marshall are partners in an accounting firm and share net income and loss

equally. Fellows’ beginning partnership capital balance for the current year is $185,000, and

Marshall’s beginning partnership capital balance for the current year is $260,000. The

partnership had net income of $350,000 for the year. Fellows withdrew $80,000 during the

year and Marshall withdrew $70,000. What is Marshall’s return on equity?

A. 67.3%

B. 60.3%

C. 78.7%

D. 54.3%

E. 56.0%

101. If a company wants to protect its three investors against personal liability risk, which of

the following business forms would not be a suitable option?

A. C Corporation

B. S Corporation

C. Limited liability partnership

D. Partnership

E. Limited liability company

102. Reno contributed $104,000 in cash plus equipment valued at $27,000 to the RD

Partnership. The journal entry to record the transaction for the partnership is:

A. Debit Cash $104,000; debit Equipment $27,000; credit RD Partnership, Capital $131,000.

B. Debit Cash $104,000; debit Equipment $27,000; credit Common Stock $131,000

C. Debit Cash $104,000; debit Equipment $27,000; credit Reno, Capital $131,000.

D. Debit Reno, Capital $131,000; credit RD Partnership, Capital $131,000.

E. Debit RD Partnership, Capital $131,000; credit Reno, Capital $131,000.

103. Bloom and Plant organize a partnership on January 1. Bloom’s initial investment consists

of $800 cash, $1,700 equipment and a $500 note payable reflecting a bank loan for the new

business. Plant’s initial investment is cash of $2,000. These amounts are the values agreed on

by both partners. The journal entry to record Bloom’s investment is:

A. Debit Cash $800; debit Equipment $1,700; credit Note Payable $500; credit Bloom,

Capital $2,000.

B. Debit Cash $2,000; credit Bloom, Capital $2,000

C. Debit Cash $800; debit Equipment $1,700; credit Bloom, Capital $2,500.

D. Debit Cash $800; debit Equipment $1,200; credit Bloom, Capital $2,000.

E. Debit Bloom, Capital $3,000; credit Common Stock $3,000

104. Bloom and Plant organize a partnership on January 1. Bloom’s initial investment consists

of $800 cash, $1,700 equipment and a $500 note payable reflecting a bank loan for the new

business. Plant’s initial investment is cash of $2,000. These amounts are the values agreed on

by both partners. The journal entry to record Plant’s investment is:

A. Debit Cash $1,500; debit Note Payable $500; credit Plant, Capital $2,000.

B. Debit Cash $2,000; credit Note Payable $500, credit Plant, Capital $1,500

C. Debit Bloom, Capital $2,000; credit Cash $2,000.

D. Debit Cash $2,500; credit Note Payable $500; credit Plant, Capital $2,500.

E. Debit Cash $2,000; credit Plant, Capital $2,000

105. Wallace and Simpson formed a partnership with Wallace contributing $60,000 and

Simpson contributing $40,000. Their partnership agreement calls for the income (loss)

division to be based on the ratio of capital investments. The partnership had income of

$150,000 for its first year of operation. When the Income Summary is closed, the journal

entry to allocate partner income is:

A. Debit Income Summary $150,000; credit Wallace, Capital $75,000; credit Simpson,

Capital $75,000.

B. Debit Wallace, Capital $75,000; debit Simpson, Capital $75,000; credit Income Summary

$150,000

C. Debit Income Summary $150,000; credit Wallace, Capital $90,000; credit Simpson,

Capital $60,000.

D. Debit Cash $150,000; credit Wallace, Capital $90,000; credit Simpson, Capital $60,000.

E. Debit Wallace, Capital $90,000; debit Simpson, Capital $60,000; credit Cash $150,000

106. Wallace and Simpson formed a partnership with Wallace contributing $60,000 and

Simpson contributing $40,000. Their partnership agreement calls for the income (loss)

division to be based on the ratio of capital investments. Wallace sold one-half of his

partnership interest to Prince for $55,000 when his capital balance was $78,000. The

partnership would record the admission of Prince into the partnership as:

A. Debit Wallace, Capital $55,000; credit Prince, Capital $55,000.

B. Debit Wallace, Capital $39,000; credit Prince, Capital $39,000.

C. Debit Prince, Capital $55,000; credit Wallace, Capital $55,000.

D. Debit Wallace, Capital $30,000; credit Prince, Capital $30,000.

E. Debit Wallace, Capital $39,000; debit Cash $16,000; credit Prince, Capital $55,000.

107. Wallace, Simpson, and Prince are partners and share income and losses in a 3:4:3 ratio.

The partnership’s capital balances are Wallace, $68,000; Simpson, $90,000; and Prince,

$42,000. Royal is admitted to the partnership on July 1 with a 20% equity and invests

$50,000. The partnership would record the admission of Royal into the partnership as:

A. Debit Wallace, Capital $15,000; debit Simpson, Capital, $20,000; debit Prince, Capital

$15,000; credit Royal, Capital $50,000.

B. Debit Cash $20,000; credit Prince, Capital $20,000.

C. Debit Cash $40,000; debit Wallace, Capital $3,000; debit Simpson, Capital, $4,000; debit

Prince, Capital $3,000; credit Royal, Capital $50,000.

D. Debit Cash $50,000; credit Royal, Capital $50,000.

E. Debit Cash $50,000; credit Simpson, Capital $10,000, credit Royal, Capital $40,000.

108. Match each of the following terms with the appropriate definitions.

A. S corporation

B. Mutual agency

C. Partnership

D. Unlimited liability of partners

E. Partnership contract

F. C corporation

G. General partner

H. Limited liability partnership

I. Statement of partners’ equity

J. Limited partnership

___ 1. A financial statement that shows total capital balances at the beginning of the

period, any additional investment by partners, the income or loss of the

period, the partners’ withdrawals, and the ending capital balances.

___ 2. A partnership that has two classes of partners, limited partners and general

partners. Limited partners have no personal liability beyond the amount they

invest in the partnership, and have no active role except as specified in the

partnership agreement.

___ 3. A partnership that protects innocent partners from malpractice or negligence

claims resulting from the acts of another partner.

___ 4. The legal relationship among general partners that makes each of them

personally responsible for paying the debts of the partnership if the

partnership cannot pay.

___ 5. The agreement between partners that sets terms under which the affairs of the

partnership are conducted.

___ 6. An unincorporated association of two or more persons to pursue a business

for profit as co-owners.

___ 7. A partner who assumes unlimited liability for the debts of the partnership.

___ 8. The legal relationship among partners whereby each partner can commit or

bind the partnership to any contract within the scope of the partnership’s

business.

___ 9. A corporation that does not qualify for nor elect to be treated as a partnership

for income tax purposes and therefore is subject to income taxes.

___ 10. A corporation with 100 or fewer stockholders that can elect to be treated as a

partnership for income tax purposes but retain the same limited liability as

other corporations.

1. I; 2. J; 3. H; 4. D; 5. E; 6. C; 7. G; 8. B; 9. F; 10. A

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-64

Blooms: Remember

AACSB: Communication

AICPA BB: Industry

AICPA BB: Legal

AICPA FN: Decision Making

Difficulty: 1 Easy

Learning Objective: D-C1

Topic: Partnership Form of Organization

Short Answer Questions

109. Identify and discuss the key characteristics of partnerships. Also, identify other

organizations that possess partnership characteristics.

110. Define the partner return on equity ratio and explain how a specific partner would use

this ratio.

111. How are partners’ investments in a partnership recorded?

112. Discuss the options for the allocation of income and loss among partners, including with

and without a partnership agreement.

113. What are the ways that a new partner can be admitted to an existing partnership? Explain

how to account for the admission of the new partner under each of these circumstances.

114. What are the ways a partner can withdraw from a partnership? Explain how to account

for the withdrawal of a current partner from a partnership.

115. Explain the steps involved in the liquidation of a partnership.

116. What factors should be considered before establishing a partnership?

117. Cinema Products LP is organized as a limited partnership that sells movie props.

Information related to capital balances is given below. Compute the partner return on equity

for each limited partner. How would each partner evaluate the success of the partnership?

What would you recommend the partners do with respect to additional investments or

withdrawals?

Turner

Kelly

Total

Capital balance, beginning of year

890,000

570,000

1,460,000

Net income for current year 85,000 65,000 150,000

Withdrawals for current year 40,000 25,000 65,000

118. Cinema Products LP is organized as a limited partnership that sells movie props.

Information related to the capital balances is given below. Compute the partnership return on

equity.

Turner

Kelly

Total

Capital balance, beginning of year

890,000

570,000

1,460,000

Net income for current year 85,000 65,000 150,000

Withdrawals for current year 40,000 25,000 65,000

119. Caroline Meeks and Charlie Fox decide to form a partnership on August 1. Meeks

invests the following assets and liabilities in the new partnership:

Market Value

Land………………………………………….………... $80,000

Building……………………………………………..… 250,000

Note payable………………………….…….………. 114,000

The note payable is associated with the building and the partnership will assume

responsibility for the loan. Fox invested $100,000 in cash and $95,000 in equipment in the

new partnership. Prepare the journal entries to record the two partners’ original investments in

the new partnership.

120. Montez and Flair formed a partnership. Montez contributed $15,000 cash and accounts

receivable worth $11,000. Flair contributed cash of $5,000; inventory valued at $16,000; and

supplies valued at $2,000. Prepare the journal entries to record each partner’s investment in

the new partnership.

121. MacArthur, Strong, and Viet form a partnership. MacArthur contributes $190,000 cash

and Strong contributes $200,000 in cash. Viet contributes equipment worth $215,000. Prepare

the single journal entry to record the formation of this partnership.

122. Ranger and Sol formed a partnership with capital contributions of $150,000 and

$180,000, respectively. Their partnership agreement called for Ranger to receive a $60,000

annual salary allowance. They also agreed to allow each partner a share of income equal to

10% of their initial capital investments. The remaining income or loss is to be divided

equally. If the net income for the current year is $110,000, what are Ranger’s and Sol’s

respective shares?

Answer:

Ranger

Sol

Total

Net income…………………….….………….…..

$110,000

Salary Allowance….……………………………

$60,000

(60,000)

Interest allowance

$150,000 x 0.10 15,000 (15,000)

$180,000 x 0.10

18,000

(18,000

)

17,000

Remainder

Allocation of remainder 8,500 8,500 (17,000)

Total $83,500 $26,500 -0-

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: D-P2

Topic: Dividing Income or Loss

123. Bannister invested $110,000 and Wilder invested $99,500 in a new partnership. They

agreed to an annual interest allowance of 10% on the partners’ beginning-year capital balance,

with the balance of income or loss to be divided equally. Under this agreement, what are the

income or loss shares of the partners if the annual partnership income is $202,000?

124. Bannister invested $110,000 and Wilder invested $99,000 in a new partnership. Their

partnership agreement called for Wilder to receive a $70,000 annual salary allowance. They

also agreed to an annual interest allowance of 5% on the partners’ beginning-year capital

balance, with the balance of income or loss to be divided equally. Under this agreement, what

are the income or loss shares of the partners if the annual partnership income is $82,000?

125. Bannister invested $110,000 and Wilder invested $99,000 in a new partnership. Their

partnership agreement called for Wilder to receive a $70,000 annual salary allowance. Under

this agreement, what are the income or loss shares of the partners if the annual partnership

income is $90,000?

126. Fallon and Springer formed a partnership on January 1. Fallon contributed $90,000 cash

and equipment with a market value of $60,000. Springer’s investment consisted of: cash,

$30,000; inventory, $20,000; all at market values. Partnership net income for Year 1 and Year

2 was $75,000 and $120,000, respectively.

1. Determine each partner’s share of the net income for each year, assuming each of the

following independent situations:

(a) Income is divided based on the partners’ failure to sign an agreement.

(b) Income is divided based on a 2:1 ratio (Fallon: Springer).

(c) Income is divided based on the ratio of the partners’ original capital investments.

(d) Income is divided based on interest allowance of 12% on the original capital investments;

salary allowance to Fallon of $30,000 and Springer of $25,000; and the remainder to be

divided equally.

2. Prepare the journal entry to record the allocation of the Year 1 income under alternative (d)

above.

127. Lin and Coral invested $99,000 and $126,000, respectively, in a partnership they began

one year ago. Assuming the partnership earned $120,000 during the current year; compute

the share of the net income each partner should receive under each of these independent

assumptions.

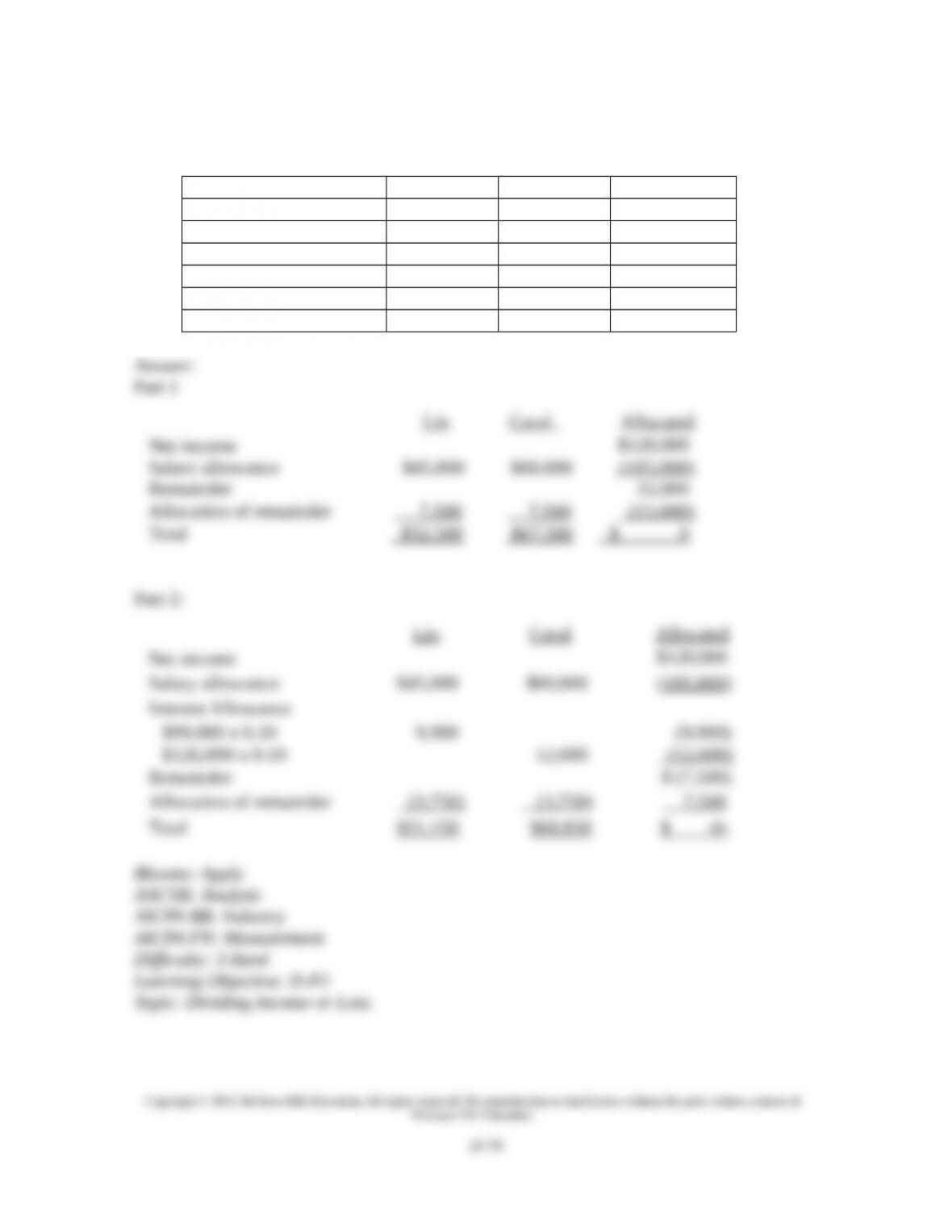

1. The partnership contract specifies salary allowances of $45,000 to Lin and $60,000 to

Coral, and any balance shared equally.

Lin Coral Allocated

Net Income

Salary allowance

Remainder

Allocation of remainder

Total

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-78

2. The partnership contract specifies salary allowances of $45,000 to Lin and $60,000 to

Coral, interest allowance of 10% on the partners’ beginning capital balance for the year.

Lin Coral Allocated

Net Income

Salary allowance

Interest allowance

Remainder

Allocation of remainder

Total

128. Glade, Marker, and Walters are partners with beginning-year capital balances of

$100,000, $50,000, and $50,000, respectively. Partnership net income for the year is $84,000.

Make the necessary journal entry to close Income Summary to the capital accounts if:

a. Partners agree to divide income based on their beginning-year capital balances.

b. Partners agree to divide income based on the ratio of 5:3:2 (Glade:Marker:Walters),

respectively.

c. Partnership agreement is silent as to division of income and less.

129. Glade, Marker, and Walters are partners with beginning-year capital balances of

$250,000, $150,000, and $100,000, respectively. Partnership net income for the year is

$192,000. Make the necessary journal entry to close Income Summary to the capital accounts

if partners agree to divide income based on their beginning-year capital balances.

130. Jakobs, Penn, and Lundt are partners with beginning-of-year capital balances of

$400,000, $320,000, and $160,000, respectively. The partners agreed to share income and

loss as follows: Salary of $30,000 to Jakobs, $50,000 to Penn, and $36,000 to Lundt. An

interest allowance of 8% on beginning-of-year capital balances. Any remaining balance is to

be divided equally. If partnership net income for the year is $190,000, determine each

partner’s share and make the appropriate journal entry to close the Income Summary to the

capital accounts.

131. Darien and Hayden agree to accept Kevin into their partnership. Kevin will contribute

$22,000 in cash. Prepare the journal entry to record this transaction.

132. Palmer withdraws from the FAP Partnership. The remaining partners agree to buy out

her share for her capital balance of $65,000. Prepare the journal entry to record the

withdrawal from the partnership.

133. Lemon and Parks are partners. On October 1, Lemon’s capital balance is $75,000, and

Parks’ capital balance is $125,000. With the partnership’s approval, Parks sells ½ of his

partnership interest to Tambling for $70,000. Prepare the journal entry to record this

transaction in the partnership records.

134. Leto and Duncan allow Gunner to purchase a 25% interest in their partnership for

$30,000 cash. Gunner has exceptional talents that will enhance the partnership. Leto’s and

Duncan’s capital account balances are $55,000 each. The partners have agreed to share

income or loss equally. Prepare the general journal entry to record the admission of Lepley to

the partnership.

135. Conklin plans to leave the CAP Partnership. The recorded value of his capital account is

$48,000. The remaining partners Arthurs and Preston agree to pay Conklin $40,000 cash and

Conklin accepts. The partners share income and loss equally. Prepare the general journal

entry to record the withdrawal from the partnership.

136. Conklin plans to leave the CAP Partnership. The recorded balance in her capital account

is $48,000. The remaining partners, Arthurs and Preston, agree to pay Conklin $58,000 cash

and Conklin accepts. The partners share income and loss equally. Prepare the journal entry to

record the transaction.

137. Kramer and Jones allow Sanders to purchase a 25% interest in their partnership for

$50,000 cash. Kramer and Jones both have capital balances of $55,000 each, and have agreed

to share income and loss equally. Prepare the journal entry to record the admission of Sanders

to the partnership.

138. The Redtail Partnership agrees to dissolve. The remaining cash balance after liquidating

partnership assets and liabilities is $70,000. The final capital account balances are: Paulson,

$35,000; Gray, $25,000; and Chang, $10,000. Prepare the journal entry to distribute the

remaining cash to the partners.

139. The Redtail Partnership agrees to dissolve. The cash balance after selling all assets and

paying all liabilities is $56,000. The final capital account balances are: Paulson, $33,000;

Gray, $27,000; and Chang, ($4,000). Chang agrees to pay $4,000 cash from personal funds to

settle his deficiency. Prepare the journal entries to record the transactions required to dissolve

this partnership.

140. The Redtail Partnership agrees to dissolve. The cash balance after selling all assets and

paying all liabilities is $60,000. The final capital account balances are: Paulson, $35,000;

Gray, $29,000; and Chang, ($4,000). Chang is unable to pay the capital deficiency. Prepare

the journal entries to record the transactions required to dissolve this partnership.

141. Sharon and Nancy formed a partnership by making capital contributions of $130,000 and

$195,000 respectively. They predict annual partnership income of $230,000 and are

considering the following alternative plans of sharing income and loss: (a) in the ratio of their

initial capital investments; or (b) salary allowances of $40,000 to Sharon and $35,000 to

Nancy; interest allowances of 12% on their initial capital investments; and the balance shared

equally. Assuming that both partners put about the same amount of time into the business,

which method of allocating income would be best?

142. Sharon and Nancy formed a partnership by making capital contributions of $130,000 and

$195,000 respectively. The annual partnership income of $230,000 is to be allocated

assuming a salary allowance of $40,000 to Sharon and $35,000 to Nancy; interest allowances

of 12% on their initial capital investments; and the balance shared equally. Prepare the entries

to record the initial capital investments, the allocation of net income, and close the partner’s

withdrawal accounts assuming that Sharon withdrew $50,000 and Nancy withdrew $45,000.

143. Kramer and Feldman Company is organized as a partnership. At the prior year-end,

Kramer’s equity balance was $352,000 and Feldman’s was $256,000. For the current year,

partnership net income is $137,000 ($77,000 allocated to Kramer and $60,000 allocated to

Feldman); withdrawals are $87,000 ($45,000 for Kramer and $42,000 for Feldman).

Compute the total partnership return on equity and the individual partner return on equity

ratios.

144. Masco, Short, and Henderson who are partners in the MSH Company share income and

loss in a 2:2:1 ratio. They plan to liquidate their partnership. At liquidation, their balance

sheet appears as follows. Prepare journal entries for (a) the sale of land and equipment sold as

a package for $500,000, (b) the allocation of the gain or loss, (c) the payment of the liabilities,

and (d) the distribution of cash to the individual partners.

MSH Company

Balance Sheet

January 31

Assets Liabilities and Equity

Cash $200,000 Accounts Payable $221,500

Equipment 200,000 Masco, Capital 210,000

Land

350,000

Short, Capital

178,000

Henderson, Capital 140,500

Total assets $750,000 Total liabilities and equity $750,000

Blooms: Apply

AACSB: Analytic

AICPA BB: Industry

AICPA FN: Measurement

Difficulty: 3 Hard

Learning Objective: D-P4

Topic: Liquidation of a Partnership

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

D-93

145. Tower, Knight, and Spears are partners who share income and loss in a 3:2:2 ratio. The

partnership’s capital balances are as follows: Tower, $332,000; Knight, $124,000; and Spears,

$214,000. Spears decides to withdraw from the partnership, and the partners agree not to

have the assets revalued upon Spears’ retirement. Prepare journal entries to record Spears’

withdrawal from the partnership under each of the following separate assumptions: Spears (a)

sells his interest to Conner for $200,000 after Tower and Knight approve the entry of Conner

as a partner; (b) is paid $214,000 in partnership cash for his equity; (c) is paid $205,000 in

partnership cash for his equity; (d) is paid $220,000 in partnership cash for his equity.

146. Tower, Knight, and Spears are partners who share income and loss in a 4:2:2 ratio. The

partnership’s capital balances are as follows: Tower, $292,000; Knight, $114,000; and Spears,

$194,000. Damsel is admitted to the partnership on March 1 with a 25% equity. Prepare the

journal entries to record Damsel’s entry into the partnership under each of the following

separate assumptions: Damsel invests (a) $200,000; (b) $180,000; and (c) $240,000.

147. On May 1, Gosworth and Jordan formed a partnership. Gosworth contributed cash of

$100,000 and equipment valued at $142,000. Jordan contributed land valued at $130,000 and

a building valued at $250,000. The partnership also assumed responsibility for Jordan’s

$120,000 long-term note payable associated with the land and building. The partners agreed

to share income as follows: Gosworth is to receive a salary allowance of $38,000, both are to

receive an annual interest allowance of 8% of their beginning-year capital investments, and

any remaining income or loss is to be shared equally. During the year, Gosworth withdrew

$40,000 and Jordan withdrew $42,000 cash. After the adjusting and closing entries are made

to the revenue and expense accounts at the end of the year, the Income Summary account had

a credit balance of $140,000. Prepare the journal entries to record (a) the partners’ initial

capital investments, (b) their cash withdrawals, and (c) closing of both the Withdrawals and

Income Summary accounts.

148. Mesner’s and Sanchez’s company is organized as a partnership. At the prior year-end,

Mesner’s equity balance was $258,000 and Sanchez’s was $212,000. For the current year,

partnership net income is $125,000 ($75,000 allocated to Mesner and $50,000 allocated to

Sanchez); withdrawals are $77,000 ($40,000 for Mesner and $37,000 for Sanchez). Compute

the total partnership return on equity and the individual partner return on equity ratios.

149. The life of a partnership is ____________________ in duration.

150. A ________________ is an unincorporated association of two or more people to pursue a

business for profit as co-owners.

151. __________________ means that partners can commit or bind the partnership to any

contract within the scope of the partnership business.

152. __________________ implies that each partner in a partnership can be called on to

personally pay a partnership’s debts.

153. A partnership that has at least two classes of partners, general and limited, allows the

limited partners to have no personal liability beyond the amounts they invest in the

partnership, and the limited partners have no active role except as specified in the partnership

agreement is a ___________________ partnership.

154. A partnership designed to protect innocent partners from malpractice or negligence

claims resulting from the acts of other partners is a ________________________ partnership.

155. A relatively new form of business organization that protects partners with limited

liability, allows limited partners to assume an active management role, and is taxed as a

partnership is a ______________________________

156. Partners in a partnership are not taxed on their withdrawals , but rather on

_____________________________.

157. Partner net income divided by average partner equity equals ______________________.

158. When a partner invests in a partnership, his/her capital account is __________ for the

invested amount.

159. During the closing process, partner’s capital accounts are _______________ for their

share of net income and _________________ for their share of net loss.

160. During the closing process, each partner’s withdrawals account is closed to

_________________________.

161. If partners agree on how to share income, but say nothing about losses, then losses are

shared ___________________.

162. A partner can be admitted into a partnership by _________________________ or by

__________________________________.

163. If a partner withdraws from a partnership and the recorded value of his or her equity is

overstated, then a bonus goes to _________________________; if the recorded value of the

withdrawing partner’s equity is understated, then a bonus goes to ____________________.

164. At least one partner having a debit balance in his/her capital account at the point of the

final distribution of cash is known as a _________________________.