Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Problem 10B-3 (continued)

5. The variances have many possible causes. Some of the more likely

causes include the following:

Materials variances:

Favorable price variance: Good price, inferior quality materials, unusual

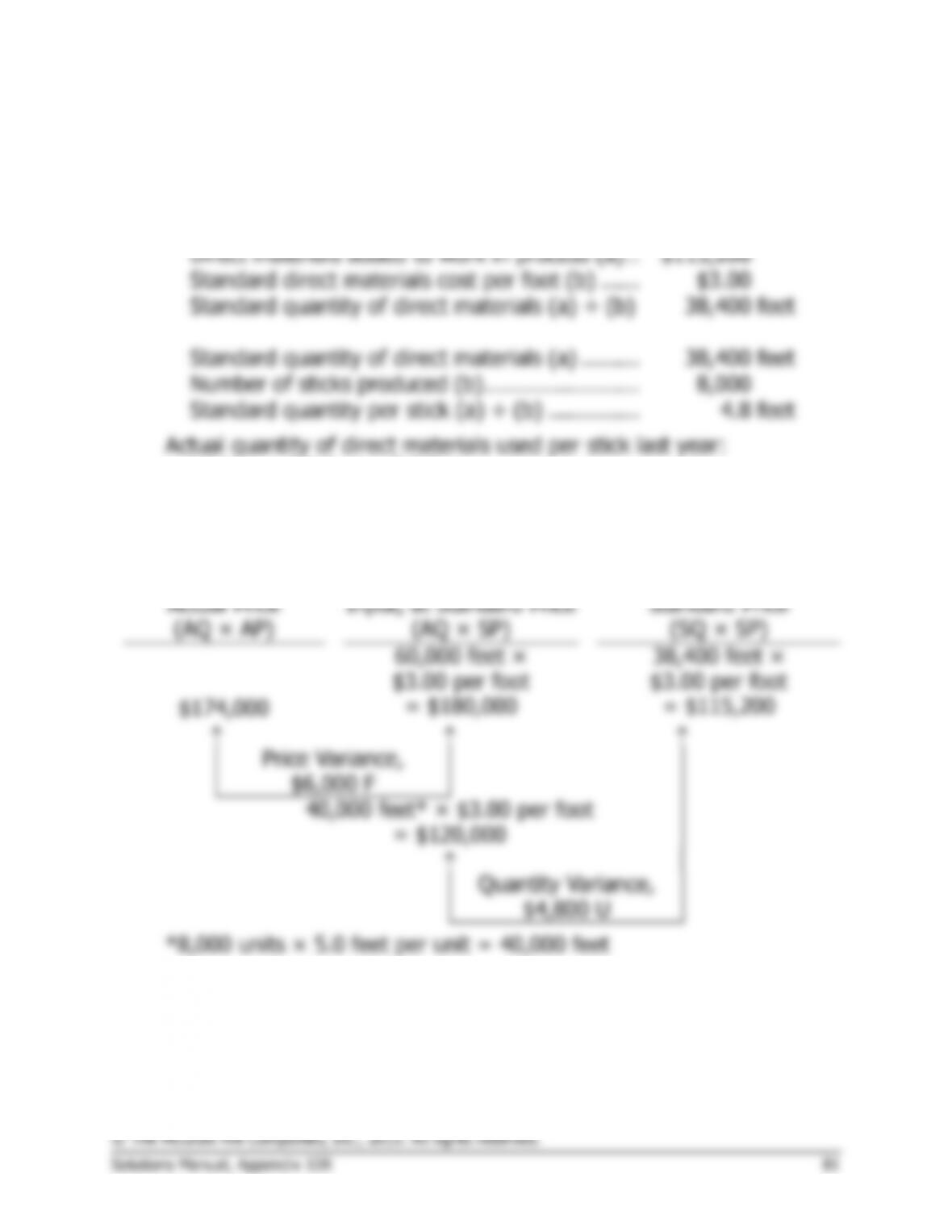

Problem 10B-4 (continued)

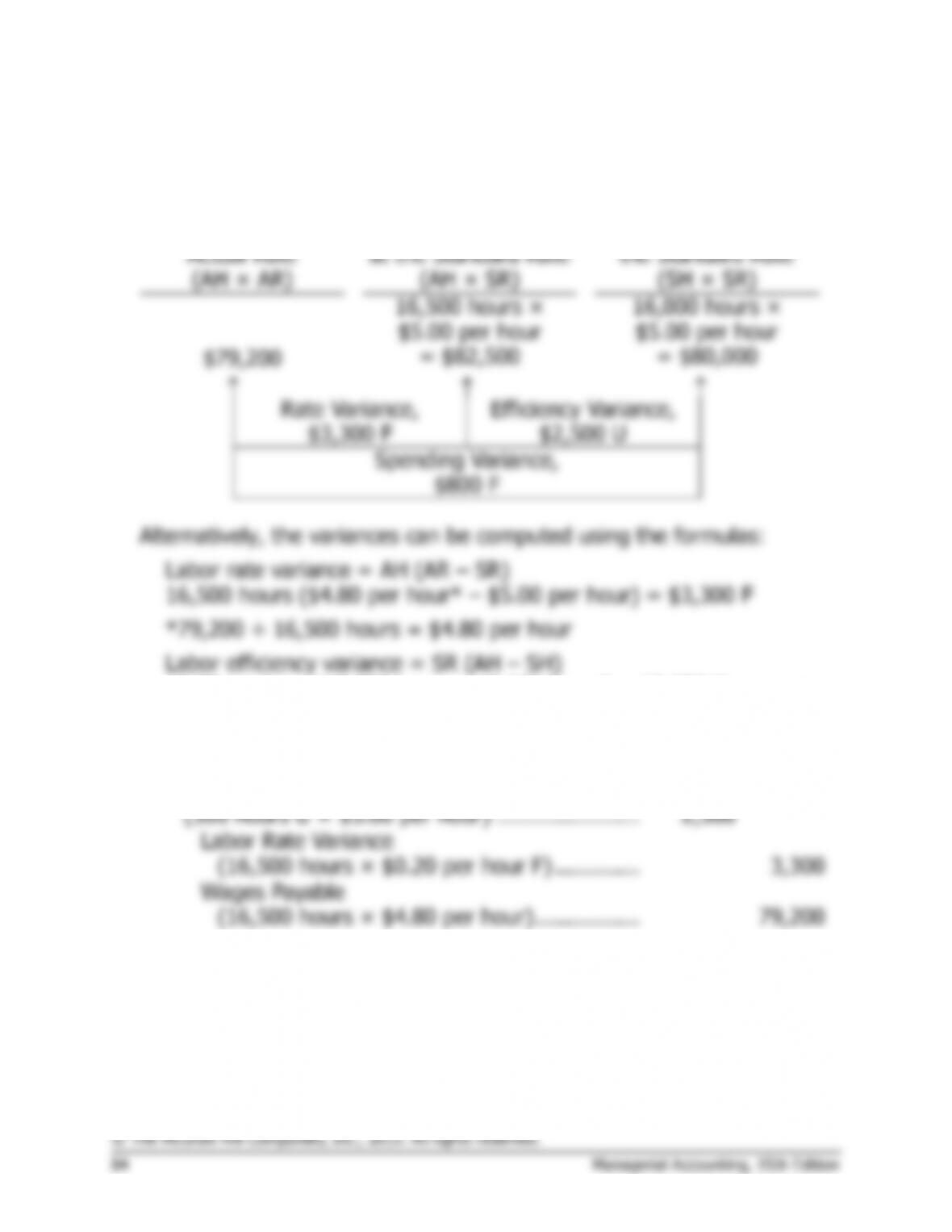

Given these figures, the variances are:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

16,500 hours ×

$5.00 per hour

16,000 hours ×

$5.00 per hour

$79,200

= $82,500

= $80,000

Rate Variance,

$3,300 F

Efficiency Variance,

$2,500 U

Spending Variance,

$800 F

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

16,500 hours ($4.80 per hour* – $5.00 per hour) = $3,300 F

*79,200 ÷ 16,500 hours = $4.80 per hour

Labor efficiency variance = SR (AH – SH)

$5.00 per hour (16,500 hours – 16,000 hours) = $2,500 U

b.

Work in Process

(16,000 hours × $5.00 per hour) .....................

80,000

Labor Efficiency Variance

(500 hours U × $5.00 per hour) ......................

2,500

Labor Rate Variance

(16,500 hours × $0.20 per hour F) .............

3,300

Wages Payable

(16,500 hours × $4.80 per hour) ................

79,200