Problem 10A-12 (continued)

Alternative solution:

Budget variance:

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $1,600 U

Volume variance:

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

´

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $9.00 per DLH (30,000 DLHs – 36,000 DLHs)

= $54,000 F

Summary of variances:

Variable overhead rate variance …………….

$ 3,800

U

Variable overhead efficiency variance ……..

9,000

U

Fixed overhead budget variance …………….

1,600

U

Fixed overhead volume variance ……………

54,000

F

Overapplied overhead …………………………

$39,600

F

© The McGraw-Hill Companies, Inc., 2015. All rights reserved.

Solutions Manual, Appendix 10B 73

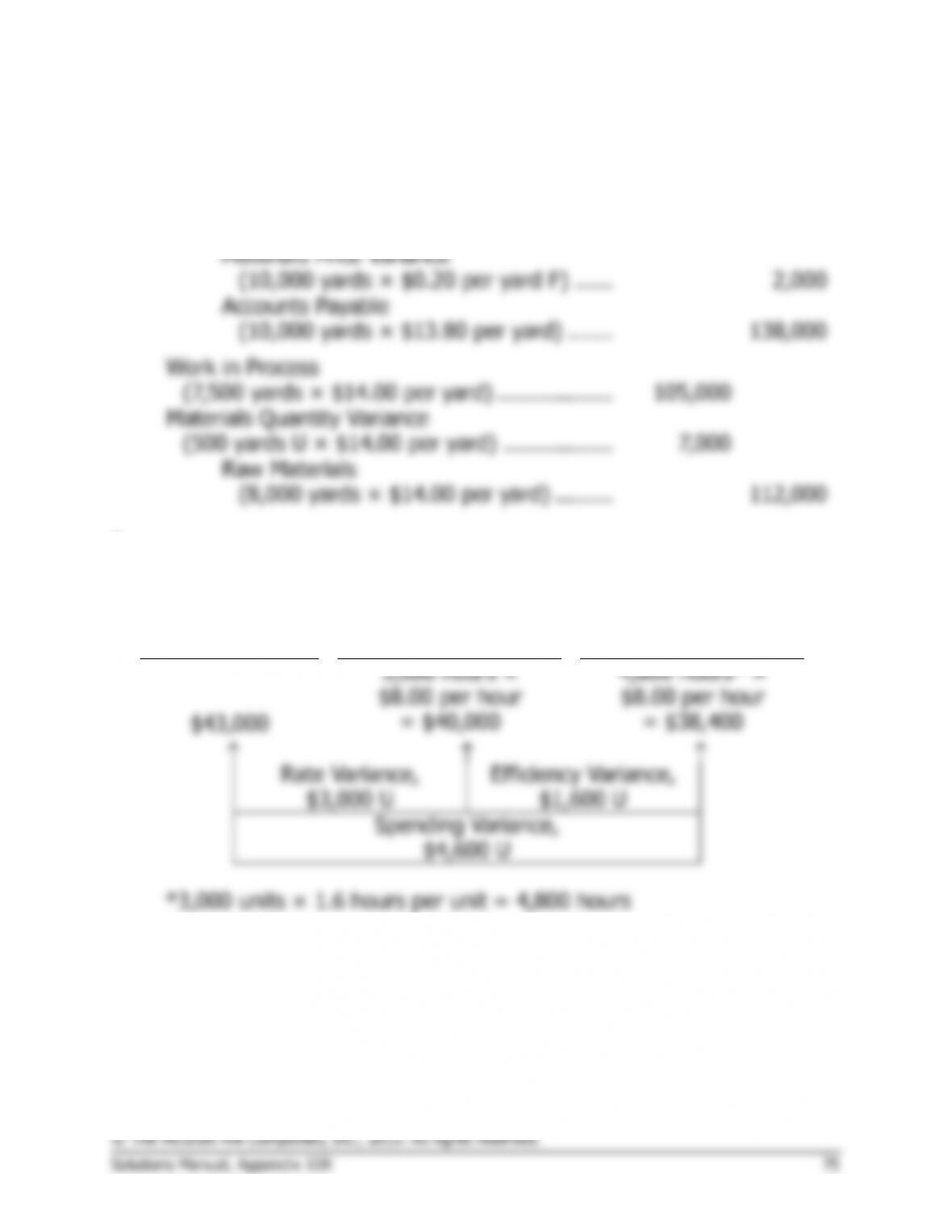

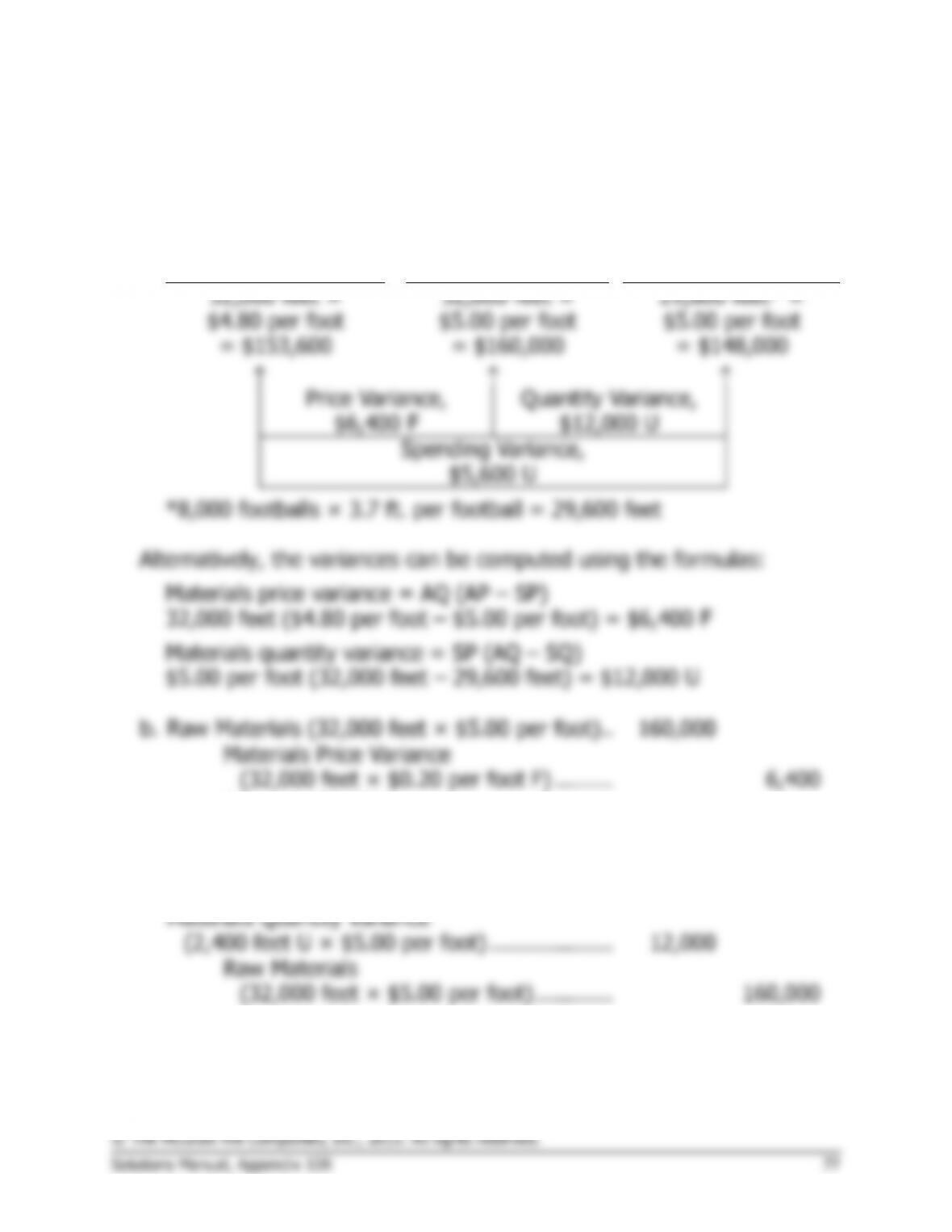

Exercise 10B-1 (20 minutes)

1. The general ledger entry to record the purchase of materials for the

month is:

Raw Materials

(12,000 meters at $3.25 per meter) ………………

39,000

Materials Price Variance

(12,000 meters at $0.10 per meter F) …….

1,200

Accounts Payable

(12,000 meters at $3.15 per meter) ……….

37,800

2. The general ledger entry to record the use of materials for the month is:

Work in Process

(10,000 meters at $3.25 per meter) ………………

32,500

Materials Quantity Variance

(500 meters at $3.25 per meter U) ………………..

1,625

Raw Materials

(10,500 meters at $3.25 per meter) ……….

34,125

3. The general ledger entry to record the incurrence of direct labor cost for

the month is:

Work in Process (2,000 hours at $12.00 per hour)

24,000

Labor Rate Variance

(1,975 hours at $0.20 per hour U) …………………

395

Labor Efficiency Variance

(25 hours at $12.00 per hour F)…………….

300

Wages Payable

(1,975 hours at $12.20 per hour) …………..

24,095