Problem 10A-9 (continued)

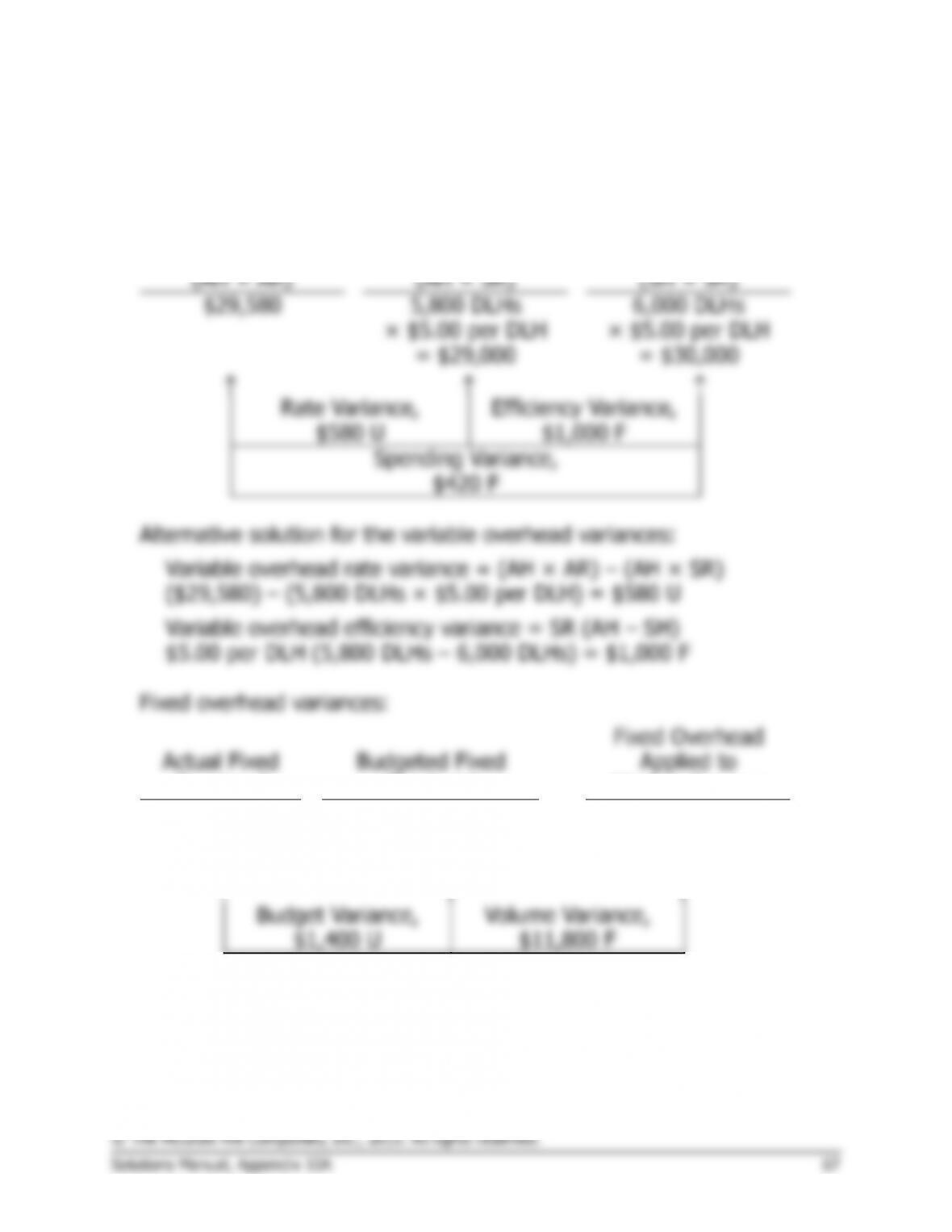

Fixed overhead variances:

Actual Fixed

Overhead

Budgeted Fixed

Overhead

Fixed Overhead Applied to

Work in Process

$209,400

$210,000

32,000 hours ×

$6 per hour = $192,000

Budget Variance,

$600 F

Volume Variance,

$18,000 U

Alternative solution:

Budget variance:

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $209,400 – $210,000

= $600 F

Volume variance:

Fixed portion of Standard

Volume Denominator

= the predetermined – hours

Variance hours

overhead rate allowed

= $6.00 per hour (35,000 hours – 32,000 hours)

= $18,000 U

æö

÷

ç÷

ç÷

ç÷

ç÷

÷

ç

èø

Verification:

Variable overhead rate variance ……..

$ 3,000

U

Variable overhead efficiency variance

5,000

F

Fixed overhead budget variance ……..

600

F

Fixed overhead volume variance …….

18,000

U

Underapplied overhead ………………..

$15,400

U