Problem 10-15 (continued)

2. Summary of variances:

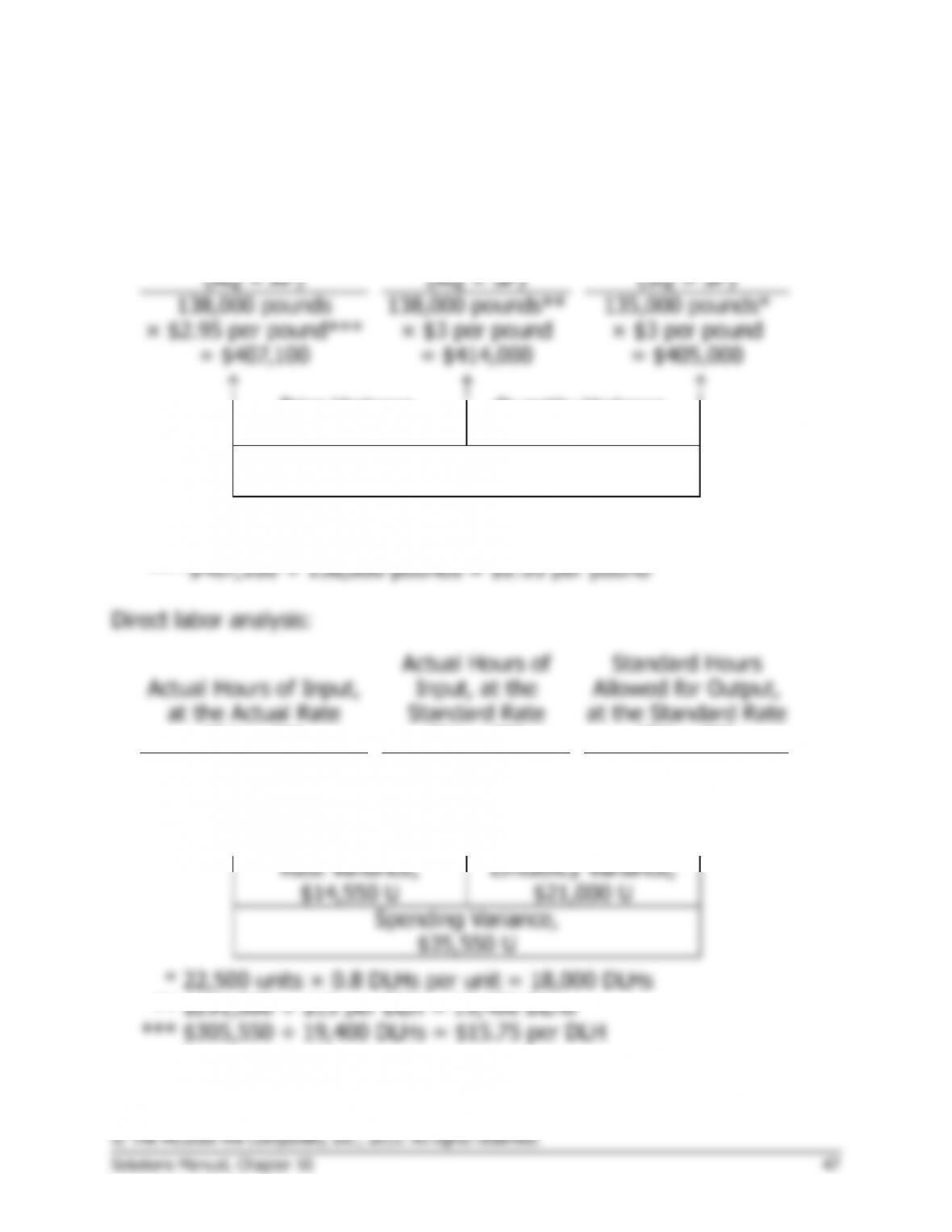

Material price variance ……………………..

$ 3,000

F

Material quantity variance …………………

8,400

U

Labor rate variance ………………………….

11,800

U

Labor efficiency variance …………………..

1,200

F

Variable overhead rate variance ………….

590

U

Variable overhead efficiency variance …..

300

F

Net variance …………………………………..

$16,290

U

Budgeted cost of goods sold at $12 per pool ………

$180,000

Add the net unfavorable variance, as above ……….

16,290

Actual cost of goods sold ……………………………….

$196,290

This $16,290 net unfavorable variance also accounts for the difference

between the budgeted net operating income and the actual net

operating income for the month.

Budgeted net operating income ……………………….

$36,000

Deduct the net unfavorable variance added to cost

of goods sold for the month …………………………

16,290

Net operating income ……………………………………

$19,710

3. The two most significant variances are the materials quantity variance

and the labor rate variance. Possible causes of the variances include:

Materials quantity variance:

Outdated standards, unskilled workers,

poorly adjusted machines,

carelessness, poorly trained workers,

inferior quality materials.

Labor rate variance:

Outdated standards, change in pay

scale, overtime pay.

Appendix 10A

Predetermined Overhead Rates and Overhead

Analysis in a Standard Costing System

Exercise 10A-1 (15 minutes)

1.

Fixed overhead

Fixed portion of the =

predetermined overhead rate Denominator level of activity

$250,000

= 25,000 DLHs

= $10.00 per DLH

2.

Budget Actual fixed Budgeted fixed

= –

variance overhead overhead

= $254,000 – $250,000

= $4,000 U

( )

Fixed portion of

Volume Denominator Standard hours

= the predetermined × –

variance hours allowed

overhead rate

= $10.00 per DLH × (25,000 DLHs – 26,000 DLHs)

= $10,000 F