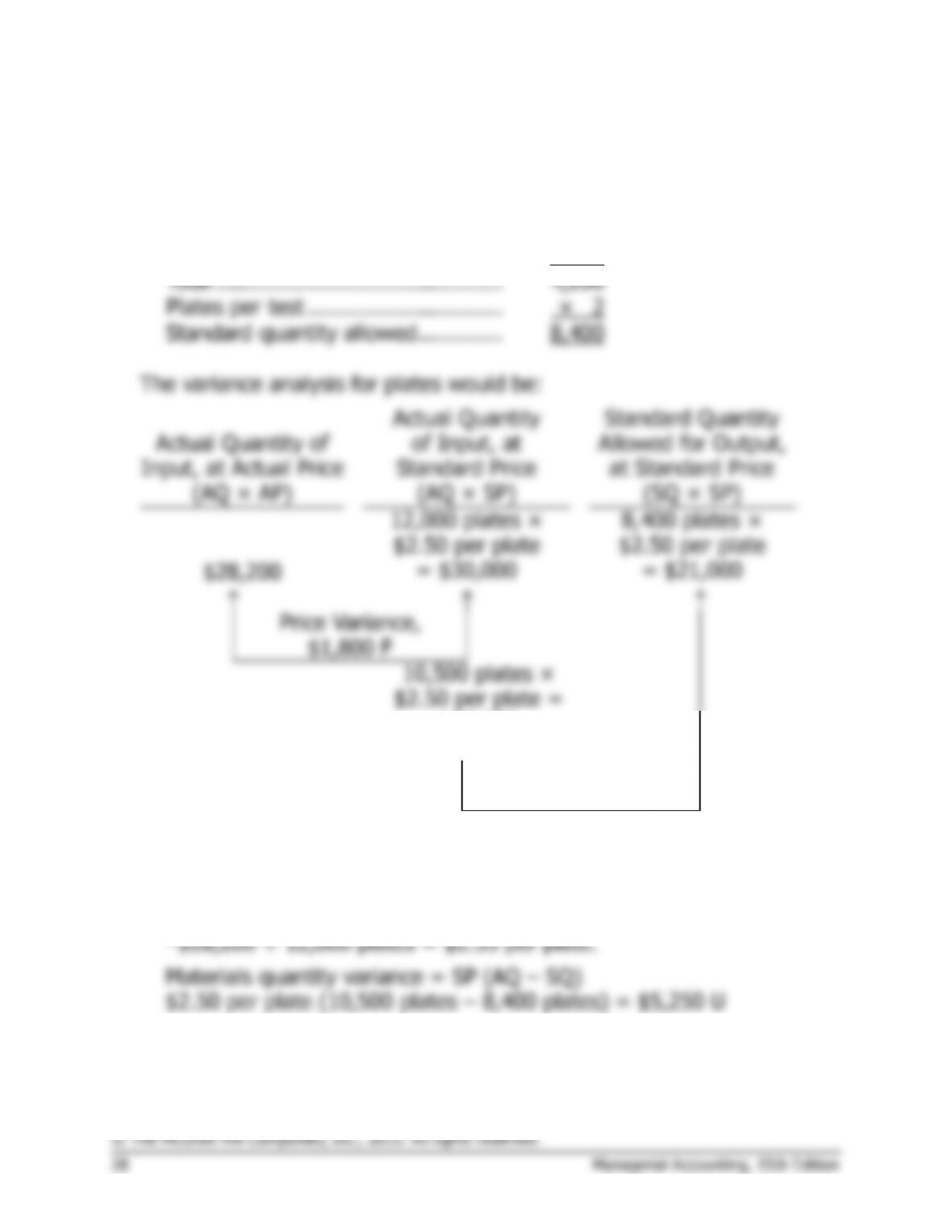

Problem 10-9 (continued)

2. Many students will miss parts 2 and 3 because they will try to use

product

costs as if they were

hourly

costs. Pay particular attention to

the computation of the standard direct labor time per unit and the

standard direct labor rate per hour.

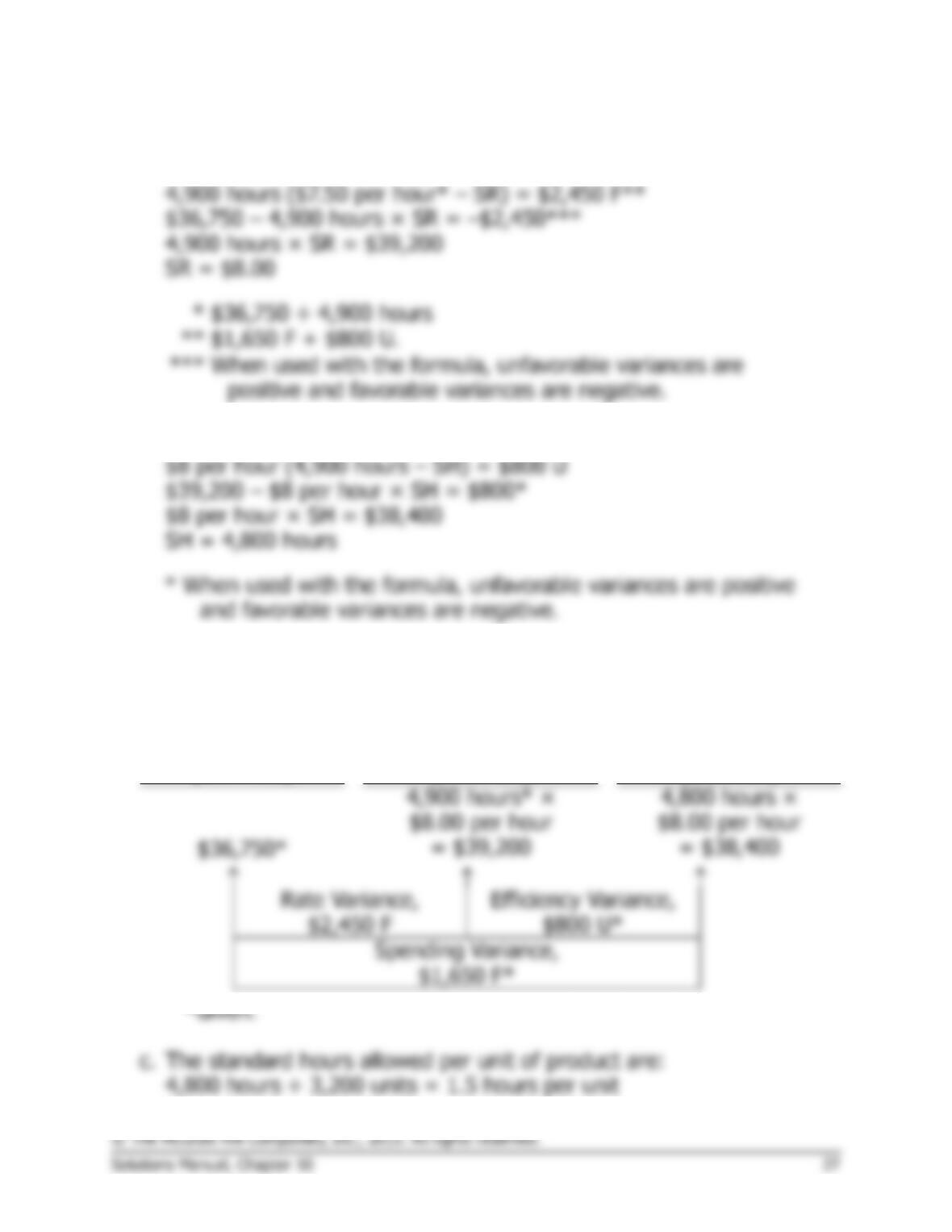

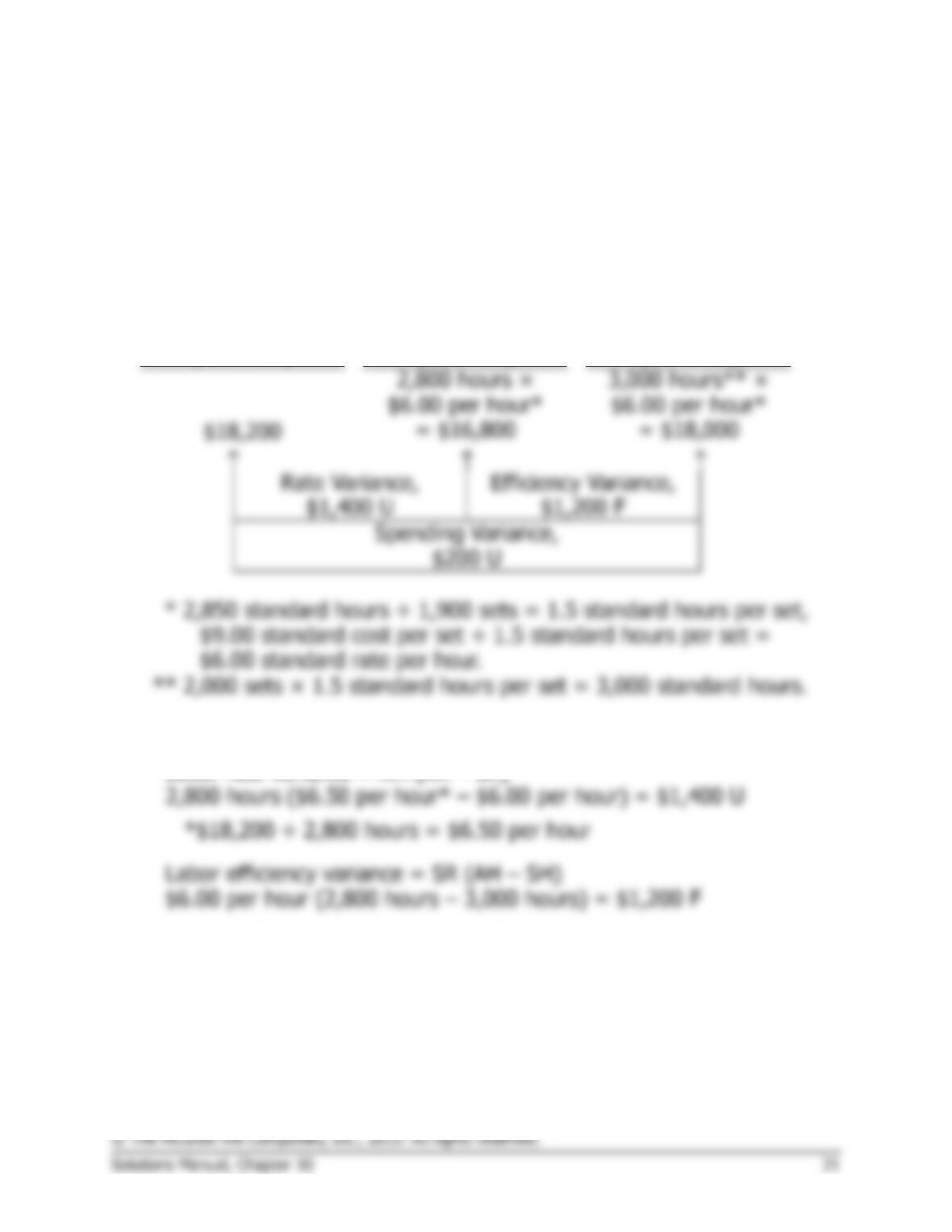

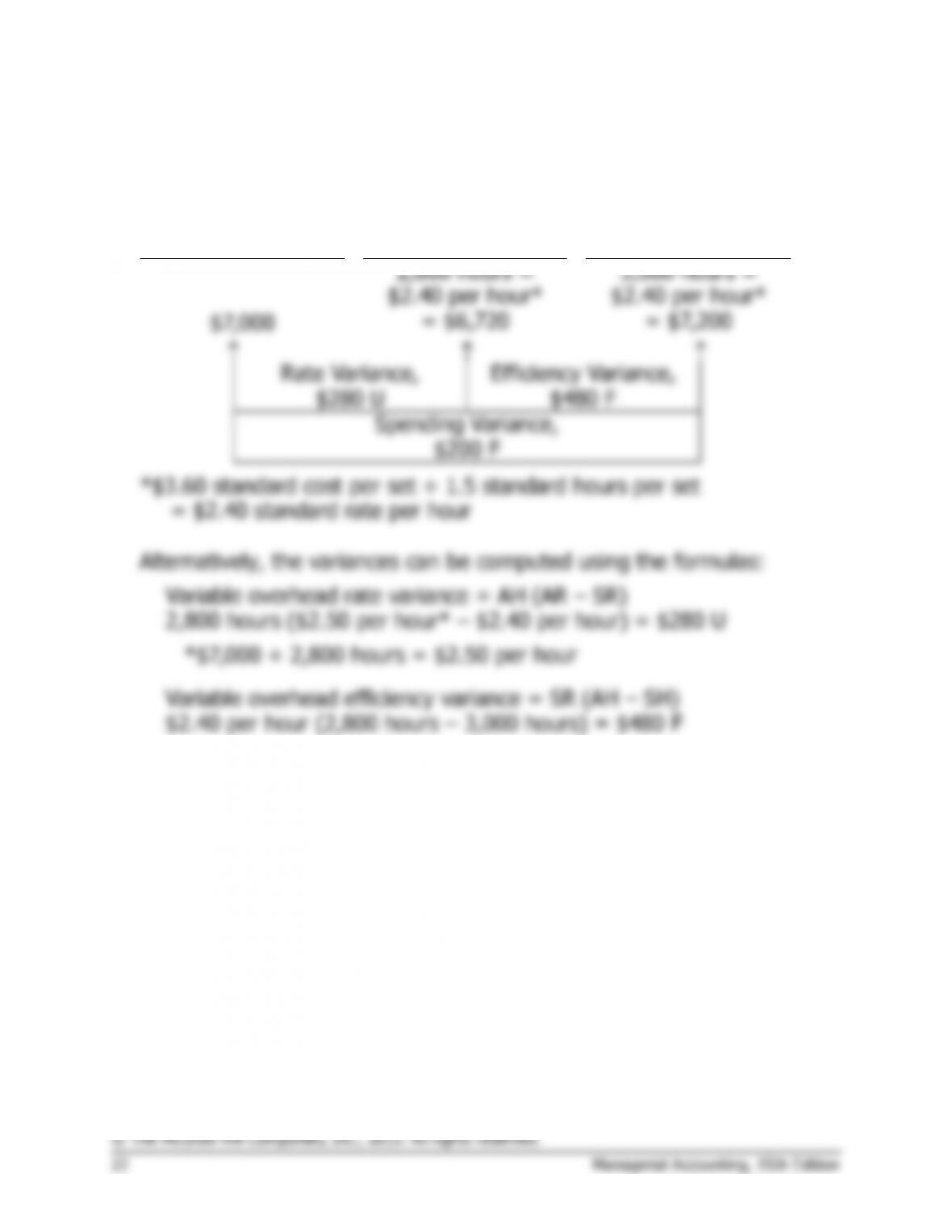

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

2,800 hours ×

$6.00 per hour*

3,000 hours** ×

$6.00 per hour*

$18,200

= $16,800

= $18,000

Rate Variance,

$1,400 U

Efficiency Variance,

$1,200 F

Spending Variance,

$200 U

*

2,850 standard hours ÷ 1,900 sets = 1.5 standard hours per set,

$9.00 standard cost per set ÷ 1.5 standard hours per set =

$6.00 standard rate per hour.

**

2,000 sets × 1.5 standard hours per set = 3,000 standard hours.

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

Problem 10-10 (45 minutes)

1.

Standard

Quantity or

Hours

Standard Price

or Rate

Standard

Cost

Alpha6:

Direct materials—X442 ……

1.8 kilos

$3.50 per kilo

$ 6.30

Direct materials—Y661 ……

2.0 liters

$1.40 per liter

2.80

Direct labor—Sintering …….

0.20 hours

$19.80 per hour

3.96

Direct labor—Finishing …….

0.80 hours

$19.20 per hour

15.36

Total …………………………..

$28.42

Zeta7:

Direct materials—X442 ……

3.0 kilos

$3.50 per kilo

$10.50

Direct materials—Y661 ……

4.5 liters

$1.40 per liter

6.30

Direct labor—Sintering …….

0.35 hours

$19.80 per hour

6.93

Direct labor—Finishing …….

0.90 hours

$19.20 per hour

17.28

Total …………………………..

$41.01