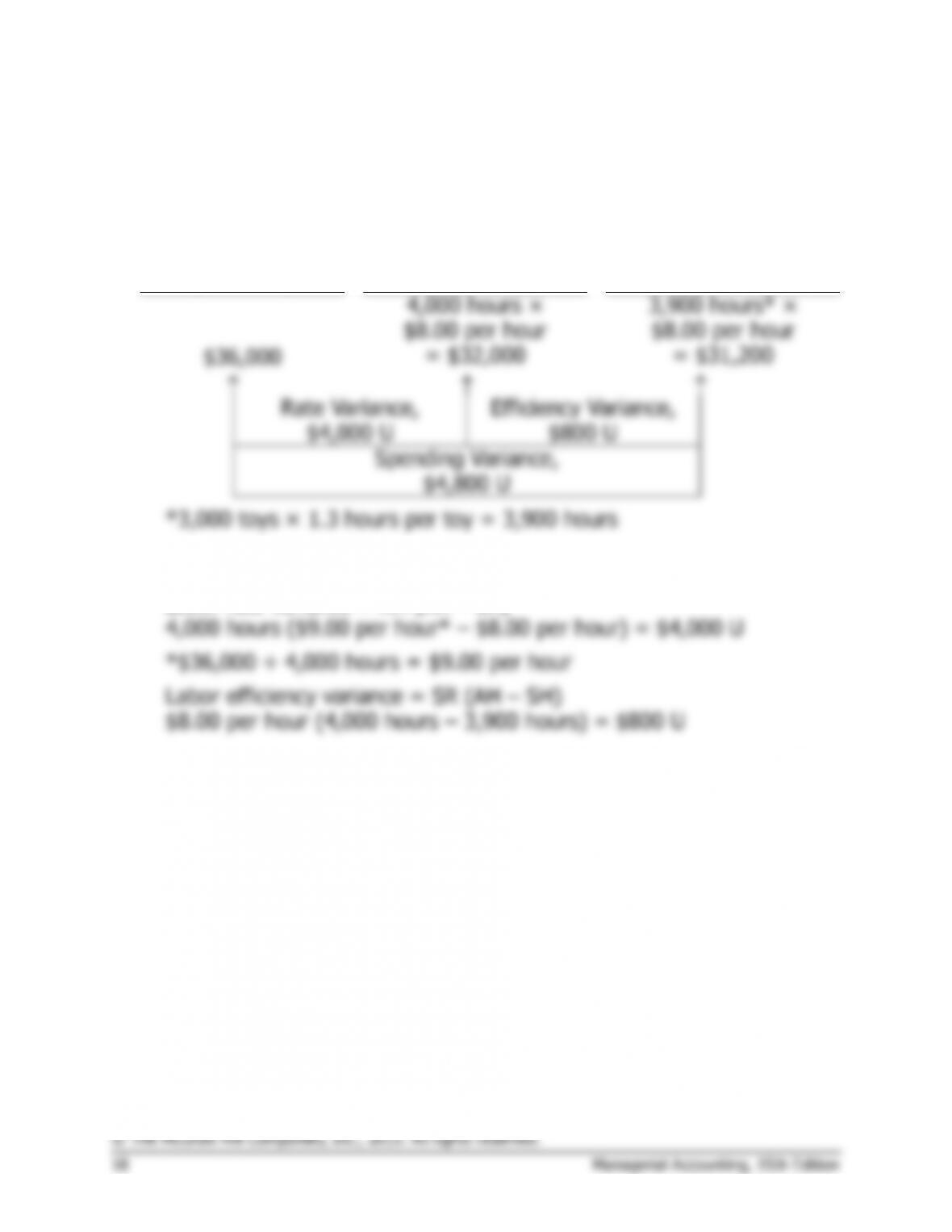

Exercise 10-4 (continued)

3.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,750 hours ×

$4.00 per hour

6,000 hours ×

$4.00 per hour

$21,850

= $23,000

= $24,000

Rate Variance,

$1,150 F

Efficiency Variance,

$1,000 F

Spending Variance,

$2,150 F

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

5,750 hours ($3.80 per hour* – $4.00 per hour) = $1,150 F

*$21,850 ÷ 5,750 hours = $3.80 per hour

Variable overhead efficiency variance = SR (AH – SH)

$4.00 per hour (5,750 hours – 6,000 hours) = $1,000 F