Chapter 10

Standard Costs and Variances

Solutions to Questions

10-1 A quantity standard indicates how much

of an input should be used to make a unit of

price variance and a quantity variance provides

10-3 The materials price variance is usually

the responsibility of the purchasing manager.

10-4 The materials price variance can be

computed either when materials are purchased

10-5 This combination of variances may

indicate that inferior quality materials were

blame for problems, they can breed resentment

contractual rate paid to workers can cause a

labor rate variance. For example, skilled workers

with high hourly rates of pay can be given duties

more skilled workers with higher rates of pay,

10-8 If poor quality materials create

production problems, a result could be excessive

10-9 If overhead is applied on the basis of

direct labor-hours, then the variable overhead

10-10 If labor is a fixed cost and standards are

tight, then the only way to generate favorable

before the bottleneck in the production process

© The McGraw-Hill Companies, Inc., 2015. All rights reserved.

2 Managerial Accounting, 15th Edition

inventory will build up in front of the

workstations with the least capacity.

The Foundational 15

1. The raw materials cost included in the planning budget is $1,000,000

(= 125,000 pounds × $8.00 per pound = $1,000,000).

2, 3, and 4.

The raw materials cost included in the flexible budget (SQ × SP =

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

= 160,000 pounds ($7.50 per pound – $8.00 per pound)

= $80,000 F

The Foundational 15 (continued)

5. and 6.

The materials price variance ($85,000 F) and the materials quantity

variance ($80,000 U) can be computed as follows:

Actual Quantity

of Input,

at Actual Price

(AQ × AP)

Actual Quantity

of Input,

at Standard Price

(AQ × SP)

Standard Quantity

Allowed for Actual

Output,

at Standard Price

(SQ × SP)

170,000 pounds ×

$7.50 per pound

= $1,275,000

170,000 pounds ×

$8.00 per pound

= $1,360,000

150,000 pounds* ×

$8.00 per pound

= $1,200,000

Materials price variance

= $85,000 F

160,000 pounds ×

$8.00 per pound

= $1,280,000

Materials quantity

variance = $80,000 U

*30,000 units × 5 pounds per unit = 150,000 units

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

= 170,000 pounds ($7.50 per pound – $8.00 per pound)

= $85,000 F

The Foundational 15 (continued)

7. The direct labor cost included in the planning budget is $700,000 (=

50,000 hours × $14.00 per hour = $700,000).

8, 9, 10, and 11.

The direct labor cost included in the flexible budget (SH × SR = $840,000),

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

= 55,000 hours ($15.00 per hour – $14.00 per hour)

= $55,000 U

The Foundational 15 (continued)

12. The variable manufacturing overhead cost included in the planning

budget is $250,000 (= 50,000 hours × $5.00 per hour = $250,000).

13, 14, and 15.

The variable overhead cost included in the flexible budget (SH × SR =

** $280,500 ÷ 55,000 hours = $5.10 per hour

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR* – SR)

= 55,000 hours ($5.10 per hour – $5.00 per hour)

Exercise 10-2 (20 minutes)

1.

Number of meals prepared ……………….

4,000

Standard direct labor-hours per meal ….

× 0.25

Total direct labor-hours allowed …………

1,000

Standard direct labor cost per hour …….

× $9.75

Total standard direct labor cost ………….

$9,750

Actual cost incurred …………………………

$9,600

Total standard direct labor cost (above)

9,750

Total direct labor variance ………………..

$ 150

Favorable

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

960 hours ×

$10.00 per hour

960 hours ×

$9.75 per hour

1,000 hours ×

$9.75 per hour

= $9,600

= $9,360

= $9,750

Rate Variance,

$240 U

Efficiency Variance,

$390 F

Spending Variance,

$150 F

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH(AR – SR)

= 960 hours ($10.00 per hour – $9.75 per hour)

= $240 U

Labor efficiency variance = SR(AH – SH)

= $9.75 per hour (960 hours – 1,000 hours)

= $390 F

Exercise 10-4 (30 minutes)

1.

Number of units manufactured ………………………..

20,000

Standard labor time per unit

(18 minutes ÷ 60 minutes per hour) ………………

× 0.3

Total standard hours of labor time allowed …………

6,000

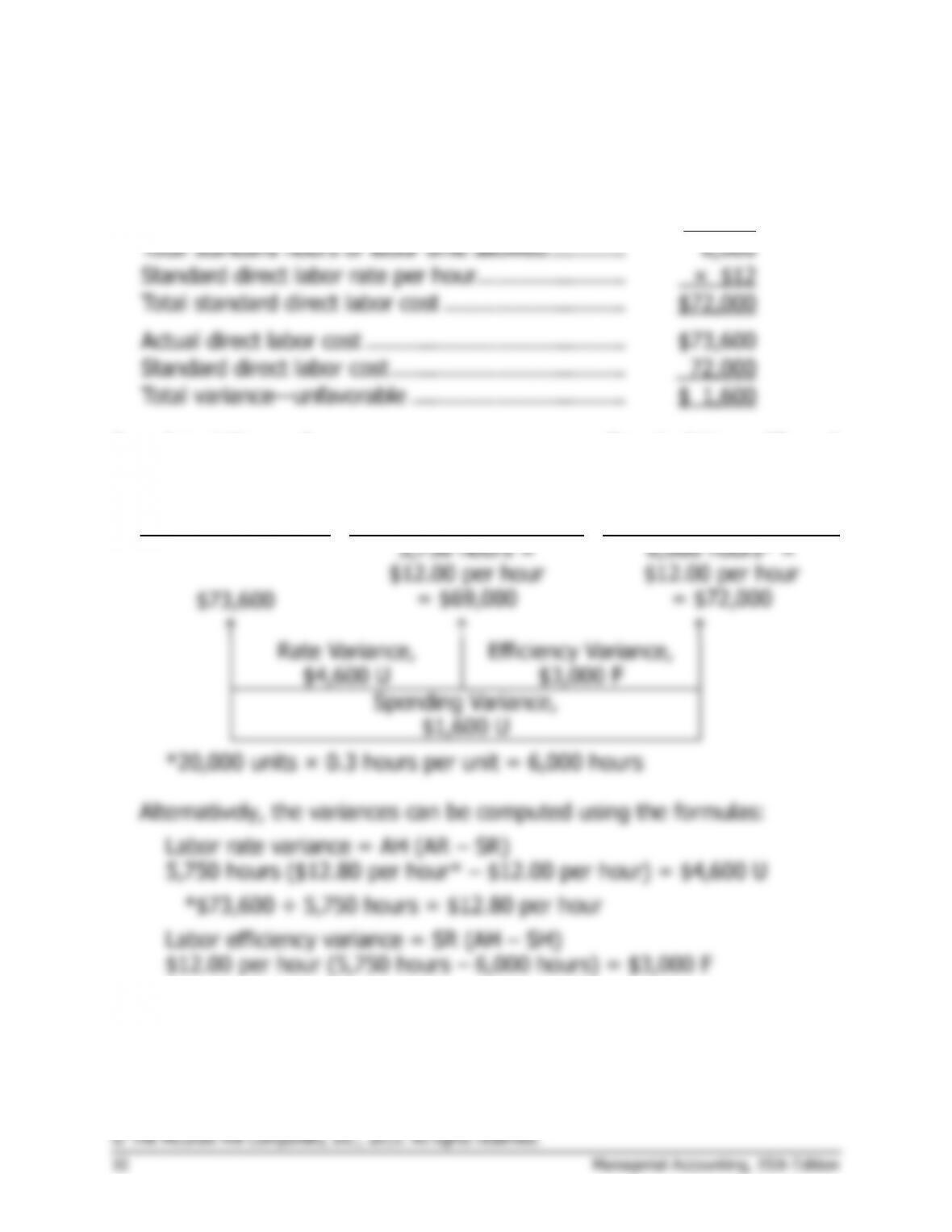

Standard direct labor rate per hour …………………..

× $12

Total standard direct labor cost ……………………….

$72,000

Actual direct labor cost …………………………..……..

$73,600

Standard direct labor cost ………………………………

72,000

Total variance—unfavorable …………………………...

$ 1,600

2.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours Allowed

for Output, at the

Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,750 hours ×

$12.00 per hour

6,000 hours* ×

$12.00 per hour

$73,600

= $69,000

= $72,000

Rate Variance,

$4,600 U

Efficiency Variance,

$3,000 F

Spending Variance,

$1,600 U

*20,000 units × 0.3 hours per unit = 6,000 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

5,750 hours ($12.80 per hour* – $12.00 per hour) = $4,600 U

*$73,600 ÷ 5,750 hours = $12.80 per hour

Labor efficiency variance = SR (AH – SH)

$12.00 per hour (5,750 hours – 6,000 hours) = $3,000 F