Problem B-5 (continued)

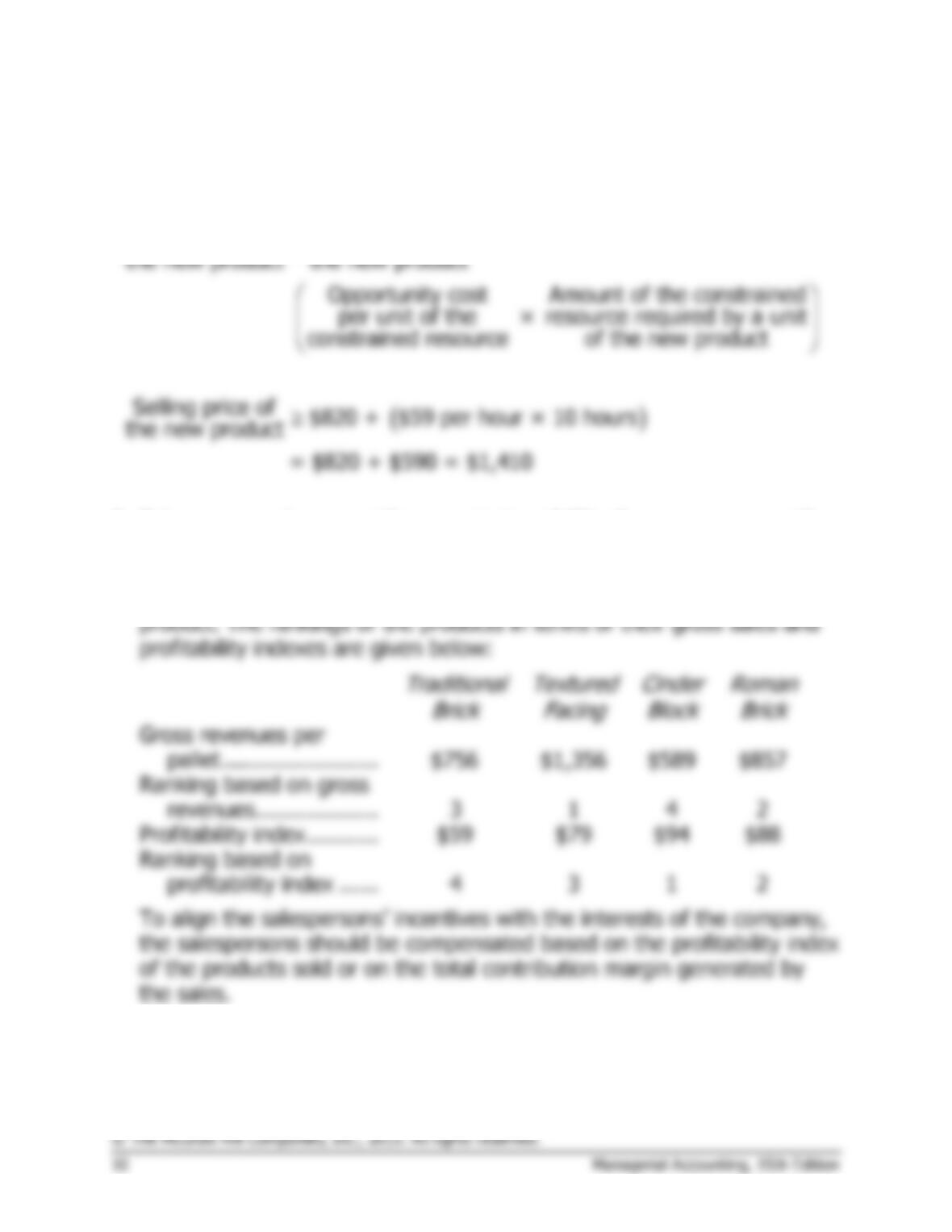

5. The selling price for the new product should at least cover its variable

cost and opportunity cost:

Selling price of Variable cost of

+

the new product the new product

Opportunity cost Amount of the constrained

per unit of the × resource required by a unit

constrained resource of the new product

Se

( )

lling price of $820 + $59 per hour × 10 hours

the new product

= $820 + $590 = $1,410

6. Salespersons who are paid a commission of 5% of gross revenues will

naturally prefer to sell a customer a pallet of anything other than cinder

blocks because they have the lowest gross revenues. However, given

the company’s constraint, they are in fact the company’s most profitable

Problem B-6 (45 minutes)

1. The relative profitability of segments should be measured by the

profitability index as follows:

Incremental profit from the segment

Profitability index= Amount of the constrained resource

used by the segment

2. It is appropriate to use the segment revenue in the denominator of the

profitability measure

only if total revenue is the organization’s

constraint

. In that case, the revenue of the segment would be the

Problem B-6 (continued)

Other situations might arise in which total revenue is the

Problem B-7 (60 minutes)

1. This problem can be solved by first computing the profitability index of

each customer and then ranking the customers based on that

profitability index:

Customer

Incremental

Profit

(A)

Regina’s

Time

Required

(B)

Profitability

Index

(A) ÷ (B)

Afonso ……

$195

5

$39

Carloni ……

$259

7

$37

Cullins ……

$105

3

$35

Frese ……..

$170

5

$34

Gerst ……..

$117

3

$39

Jelovich ….

$124

4

$31

Klarr ………

$192

6

$32

Melby …….

$144

4

$36

Rideau ……

$150

5

$30

Towner …..

$256

8

$32

Customer

Profitability

Index

Regina’s

Time

Required

Cumulative

Amount of

Regina’s Time

Required

Afonso ……

$39

5

5

Gerst ……..

$39

3

8

Carloni ……

$37

7

15

Melby …….

$36

4

19

Cullins ……

$35

3

22

Frese ……..

$34

5

27

Klarr ………

$32

6

33

Towner …..

$32

8

41

Jelovich ….

$31

4

45

Rideau ……

$30

5

50

Problem B-7 (continued)

2. The total profit on wedding cakes for the weekend after canceling the

four reservations would be:

Afonso ……

$195

Gerst ……..

117

Carloni ……

259

Melby……..

144

Cullins …….

105

Frese ……..

170

Total ………

$990

3. To avoid disappointing customers, reservations should probably not be

accepted for any particular week after 27 hours of Regina’s time have

been committed for that week’s cakes. To ensure that only the most

profitable cake reservations are accepted, a reservation for any cake

Problem B-7 (continued)

4. Ms. Therau should consider changing the way prices are set so that they

include a charge for Regina’s time. On average, the prices may be the

same, but they should be based not only on the size of the cakes, but

5. Making Regina happy involves not asking her to work more than 27

hours per week decorating cakes. Making customers happy involves not

canceling their reservations, not raising prices, and providing top quality

wedding cakes. Ms. Therau can accomplish both of these objectives

and

Case B-8 (45 minutes)

Vectra’s management is not contemplating adding or dropping products; it

simply wants to redirect salespersons’ efforts toward the more profitable

products. Therefore, this is a volume trade-off decision and the appropriate

way to measure profitability is with the profitability index:

Unit contribution margin

Profitability index for =

a volume trade-off decision Amount of the constrained

resource used by one unit

The unit contribution margin is the selling price of a product less sales

commissions and the cost of sales, which is a variable cost in this company.

The operating expenses are all fixed.

Selling price

– Sales commission

– Cost of sales

Profitability index for =

a volume trade-off decision Amount of the constrained

resource used by one unit

The case states that management wants “to redirect the effort of

salespersons towards the more profitable products.” Therefore, the

constraint must be the effort of salespersons. Unfortunately, there is no

direct measure of the amount of salespersons’ effort required to sell a unit

of each product. However, all other things equal, if one product has twice

the sales commission per unit as another, then we can expect salespersons

to exert twice as much effort selling the first product. Effort is likely to be

Case B-8 (continued)

Note that this profitability index takes into account the salespersons’