Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Appendix A

Pricing Products and Services

Solutions to Questions

A-1 In cost-plus pricing, prices are set by

unit sales of a product with elastic demand

are

sensitive to the price charged for the product.

A-3 The profit-maximizing price should de-

Fixed costs are relevant in a decision of whether

to offer a product or service at all, but are not

A-4 The markup over variable cost depends

on the price elasticity of demand. A product

the product. Full cost is an alternative approach

A-6 The absorption costing approach as-

sumes that consumers do not react to prices at

all—consumers will purchase the forecasted unit

sales regardless of the price that is charged.

A-7 The protection offered by full cost pric-

ing is an illusion. All costs will be covered only if

A-8 Target costing is used to price new

products. The target cost is the expected selling

price of the new product less the desired profit

Exercise A-1 (30 minutes)

1. Maria makes more money selling the ice cream cones at the lower price,

as shown below:

$1.89 Price

$1.49 Price

Unit sales ......................

1,500

2,340

Sales .............................

$2,835.00

$3,486.60

Cost of sales @ $0.43 .....

645.00

1,006.20

Contribution margin .......

2,190.00

2,480.40

Fixed expenses ..............

675.00

675.00

Net operating income .....

$1,515.00

$1,805.40

2. The price elasticity of demand, as defined in the text, is computed as

follows:

d =

ln(1+% change in quantity sold)

ln(1+% change in price)

2,340-1,500

ln(1+ )

1,500

æö

÷

ç÷

ç÷

÷

ç

èø

Exercise A-1 (continued)

3. The profit-maximizing price can be estimated using the following formu-

la from the text:

d

d

ε

Profit-maximizing price = Variable cost per unit

1+ε

-1.87

= $0.43

1+(-1.87)

= 2.1494 × $0.43 = $0.92

æö

÷

ç÷

ç÷

ç÷

ç

èø

æö

÷

ç÷

ç÷

÷

ç

ç

èø

This price is much lower than the prices Maria has been charging in the

past. Rather than immediately dropping the price to $0.92, it would be

prudent to drop the price a bit and see what happens to unit sales and

to profits. The formula assumes that the price elasticity is constant,

which may not be the case.

Exercise A-2 (15 minutes)

1.

( )

( )

Required ROI Selling and administraive

+

× Investment expenses

Markup percentage =

on absorption cost Unit sales × Unit product cost

12% × $750,000 + $50,000

= 14,000 units × $25 per unit

$140,000

= = 4

$350,000 0%

2.

Unit product cost ...............

$25

Markup (40% × $25).........

10

Selling price per unit ..........

$35

Exercise A-3 (10 minutes)

Sales (300,000 units × $15 per unit) ........

$4,500,000

Less desired profit (12% × $5,000,000) ...

600,000

Target cost for 300,000 units ...................

$3,900,000

Problem A-4 (45 minutes)

1. The postal service makes more money selling the souvenir sheets at the

lower price, as shown below:

$7 Price

$8 Price

Unit sales ...............................

100,000

85,000

Sales ......................................

$700,000

$680,000

Cost of sales @ $0.80 per unit .

80,000

68,000

Contribution margin ................

$620,000

$612,000

2. The price elasticity of demand, as defined in the text, is computed as

follows:

d =

ln(1 + % change in quantity sold)

ln(1 + % change in price)

85,000 - 100,000

ln(1 + )

100,000

æö

÷

ç÷

ç÷

÷

ç

èø

Problem A-4 (continued)

3. The profit-maximizing price can be estimated using the following formu-

d

1+ε

ç÷

ç

èø

=

-1.2163 $0.80

1+(-1.2163)

æö

÷

ç÷

ç÷

÷

ç

ç

èø

Problem A-4 (continued)

The critical assumption in these calculations is that the percentage in-

crease (decrease) in quantity sold is always the same for a given per-

centage decrease (increase) in price. If this is true, we can estimate the

Problem A-4 (continued)

The profit at each price in the above demand schedule can be computed

as follows:

Price

(a)

Quantity

Sold (b)

Sales

(a) × (b)

Cost of Sales

$0.80 × (b)

Contribution

Margin

$8.00

85,000

$680,000

$68,000

$612,000

$7.00

100,000

$700,000

$80,000

$620,000

$6.13

117,647

$721,176

$94,118

$627,058

$5.36

138,408

$741,867

$110,726

$631,141

$4.69

162,833

$763,687

$130,266

$633,421

$4.10

191,569

$785,433

$153,255

$632,178

$3.59

225,375

$809,096

$180,300

$628,796

$3.14

265,147

$832,562

$212,118

$620,444

$2.75

311,937

$857,827

$249,550

$608,277

$2.41

366,985

$884,434

$293,588

$590,846

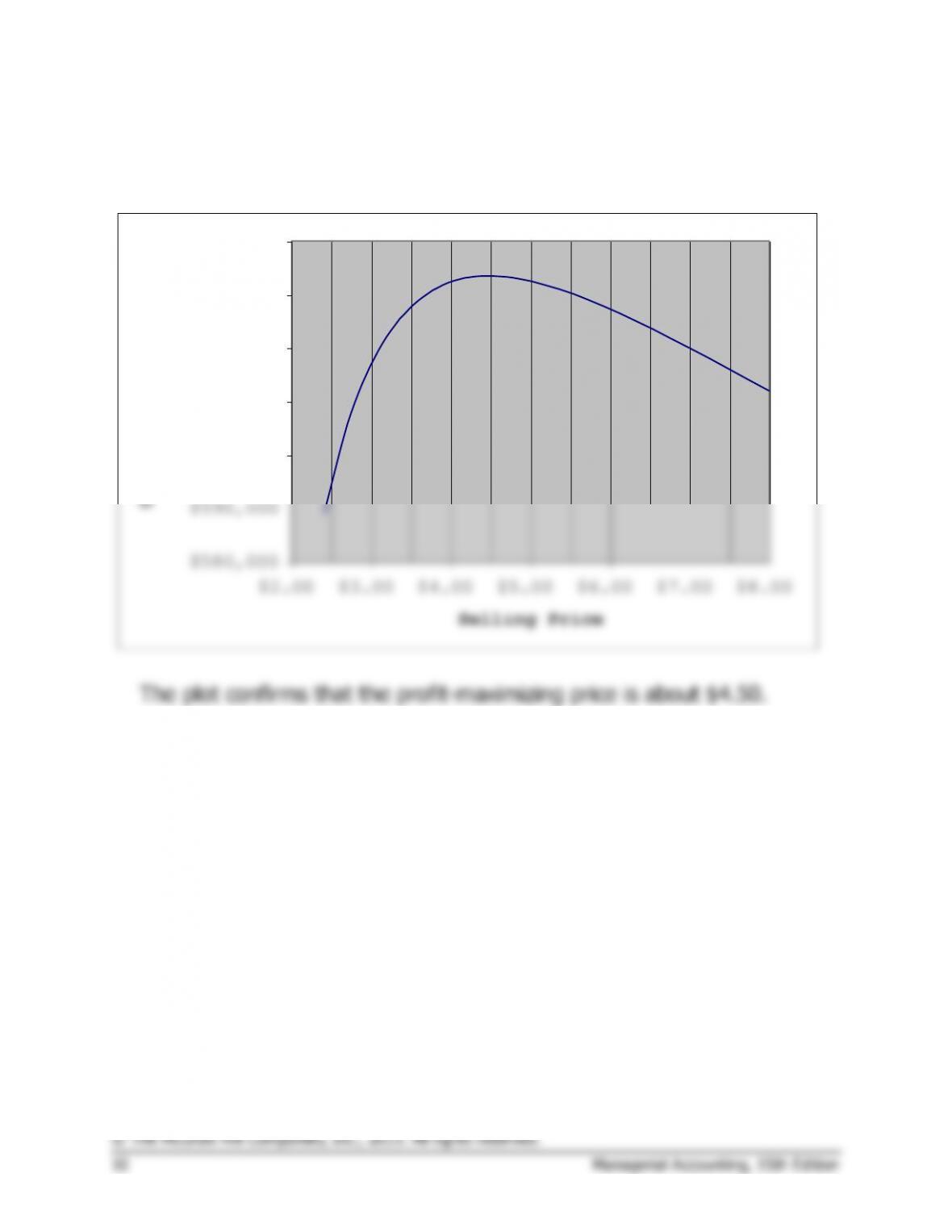

Problem A-4 (continued)

The contribution margin is plotted below as a function of the selling price:

$580,000

$590,000

$600,000

$610,000

$620,000

$630,000

$640,000

$2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00

Selling Price

Contribution Margin