Chapter 18 – Property, Plant, and Equipment

18–35

77. DJG Corporation purchased land in order to build new corporate headquarters for a

purchase price of $758,000. The lawyers charged $2,500 to handle the legal aspects of the

purchase. Closing costs paid by DJG amounted to $15,160. There was an old factory and

warehouse on the property that cost DJG $7,500 to have removed. In addition, CSB

Construction charged the corporation $1,800 to grade the property to ensure proper drainage

and an additional $15,800 build a drive, parking lot, and walkways. What amount should be

recorded as land? What other account(s) should be increased and for what amount(s)?

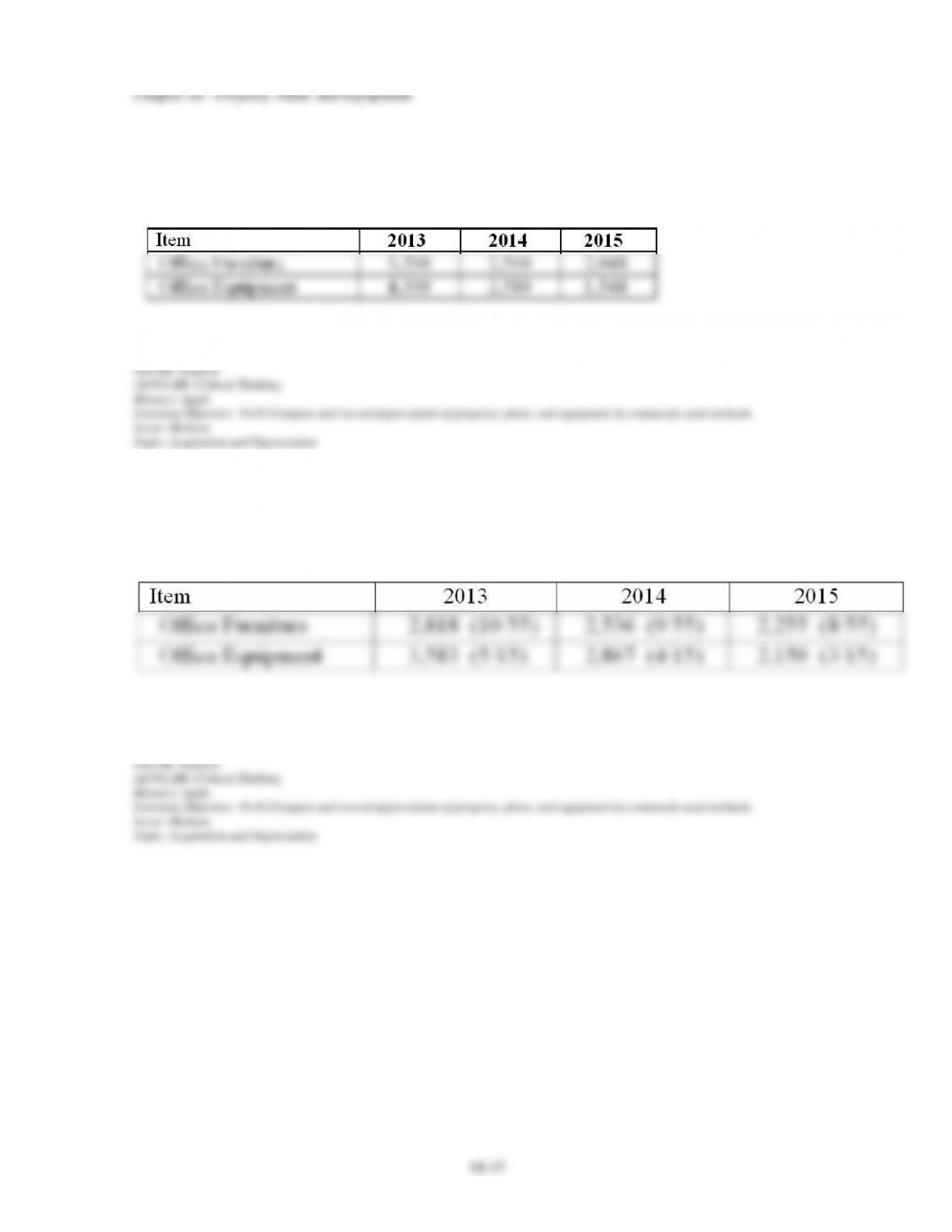

ARB Company purchased several pieces of equipment on January 2, 2013. Office Furniture

cost the company $16,000, has an estimated useful life of ten years, at which time they expect

to sell it for a total of $500. Office Equipment was also purchased for a total of $10,750 and

has an estimated useful life of five years. They don’t expect it to have any residual value at the

end of that time.

Chapter 18 – Property, Plant, and Equipment

18–44

Ryadom Industries has several assets with book values that exceed their fair market values.

At the end of the year (December 31, 2013), management at Ryadom reviewed the

circumstances around several of its assets during the current year and determined that they

were impaired. Each of the assets reviewed has a book value (carrying value) that exceeds its

fair market value. The accountant at Ryadom applied the recoverability test to each.

The first item is a Mixer that combines materials for a product that can now be made more

efficiently due to new technology. The new mixer can produce seven products for every two

that the Mixer Ryadom currently uses. This reduces Ryadom’s ability to compete with

companies who have invested in the newly developed mixers. In addition, the Mixer now has

a market value of zero. The Mixer cost $235,000, had an original residual of $35,000 and an

estimated life of ten years. Ryadom uses straight-line depreciation for its equipment. The

Accumulated Depreciation for the Mixer is $120,000. The projected cash flows generated by

the Mixer are $50,000 over the next four years.

The second impaired asset is one of its facilities at a location that now cannot transport its

product due to the closing of a rail line. Because the product cannot be transported given the

present dilemma, the estimated future revenues generated by this facility are $30,000—the

amount for which it is estimated that the facility can be sold. The facility buildings have a

new value of $24,000 and the land has an unchanged estimated value of $7,000. The

estimated remaining life of the facility is unchanged. The facility would require a large

investment in order to accommodate trucks to pick up and transport the product or to deliver

materials. This additional investment is not merited. Therefore, Ryadom plans to close and

hopefully sell this facility. The facility has total recorded costs of $2,500,000 and its related

accumulated depreciation account totals $1,800,000 (residual value was $100,000, estimated

life was 8 years and straight-line depreciation was used). If the facility is not sold within the

next two years, it will be demolished. It will be depreciated using the straight-line method

assuming a zero residual value at that time.