Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13 - Financial Statements and Closing Procedures

76. Brianna Graham is the owner of a dress shop. The firm had a net loss of $9,000 for the

year. What accounts are debited and credited to transfer the net loss to the owner's capital

account during the closing process?

77. Teresa Davis is the owner of a convenience shop. The firm had a net income of $4,500 for

the year. What accounts are debited and credited to transfer the net loss to the owner's capital

account during the closing process?

13-35

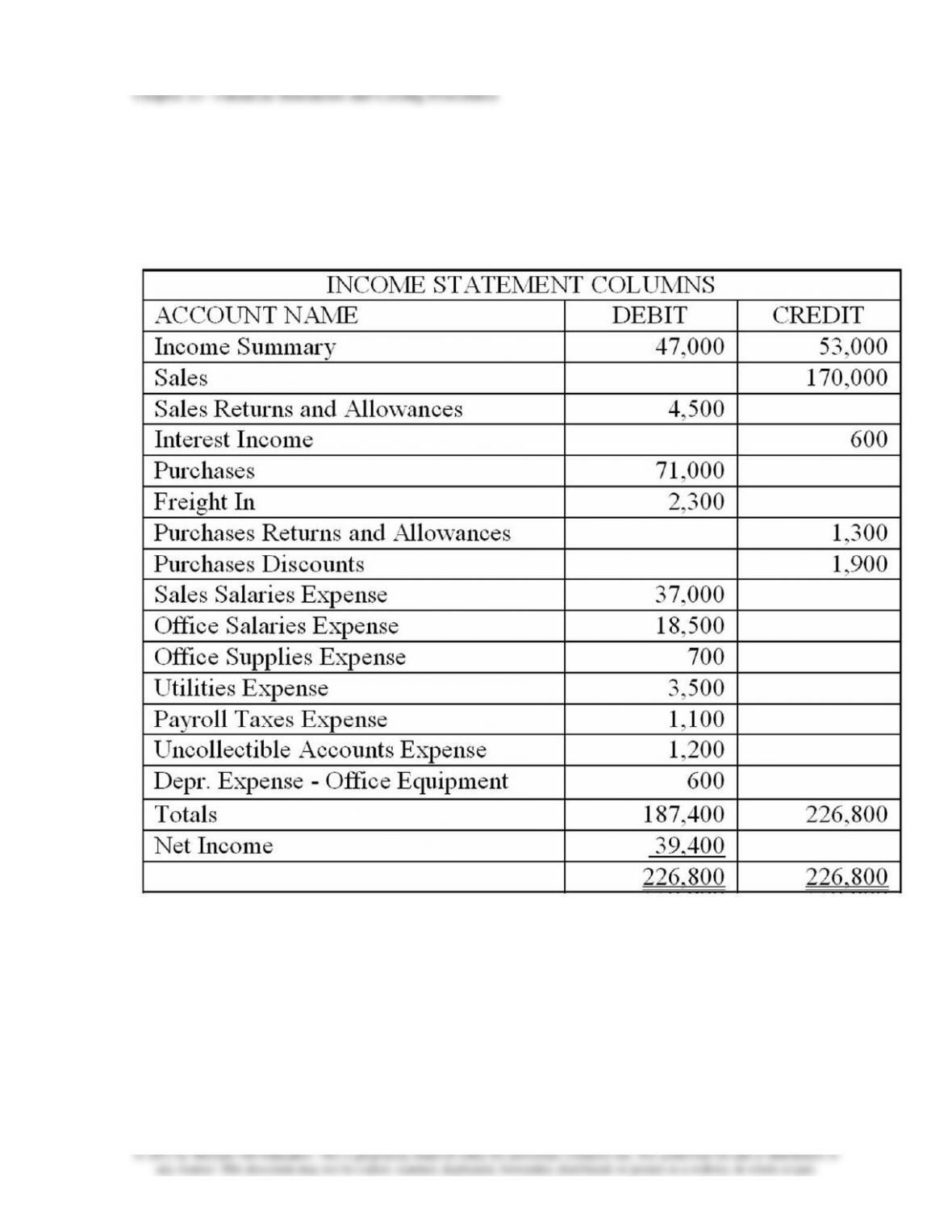

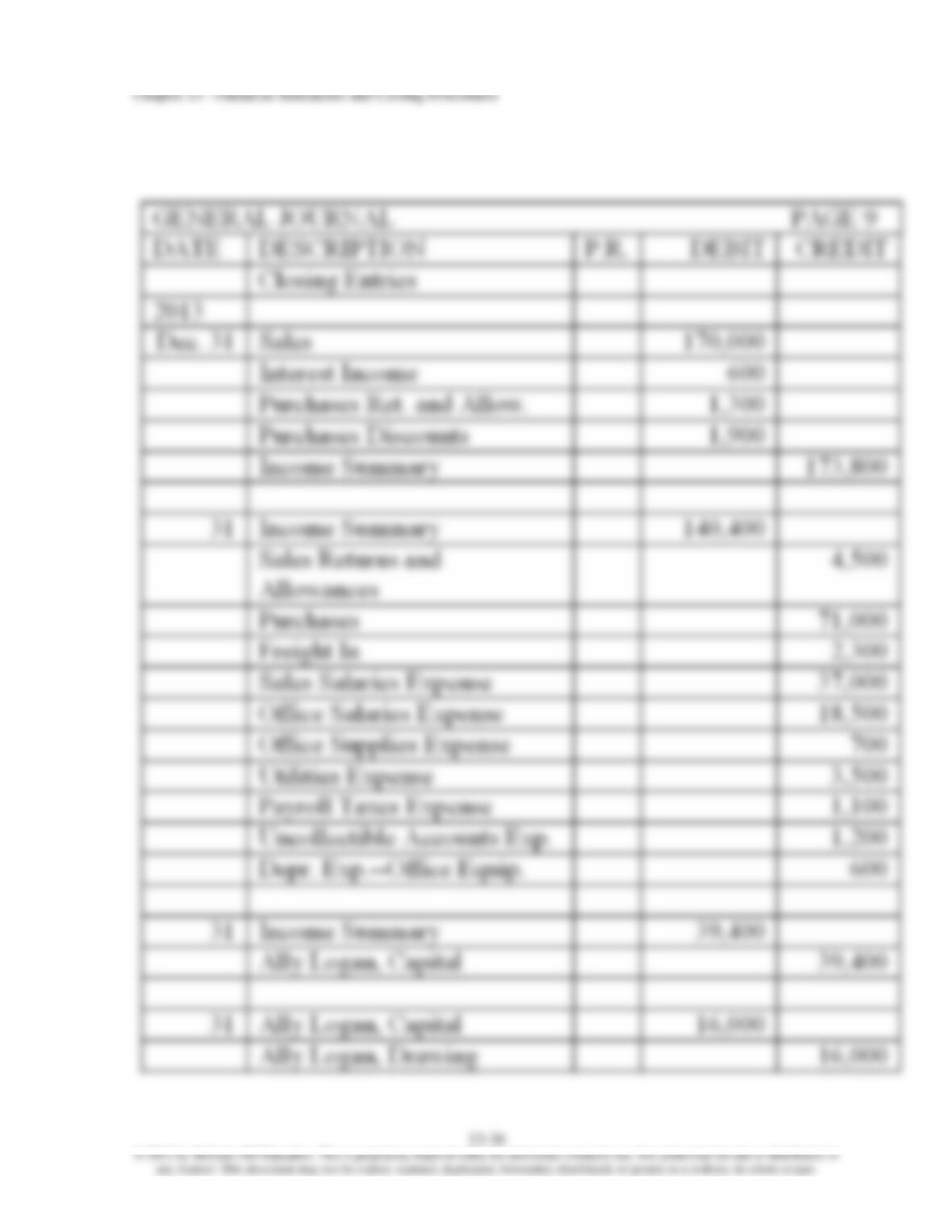

80. On December 31, 2013, the Income Statement section of the worksheet is shown below.

The balance of Ally Logan's drawing account is $16,000. Record the necessary closing entries

on page 9 of a general journal.

13-36

© 2012 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

13-37

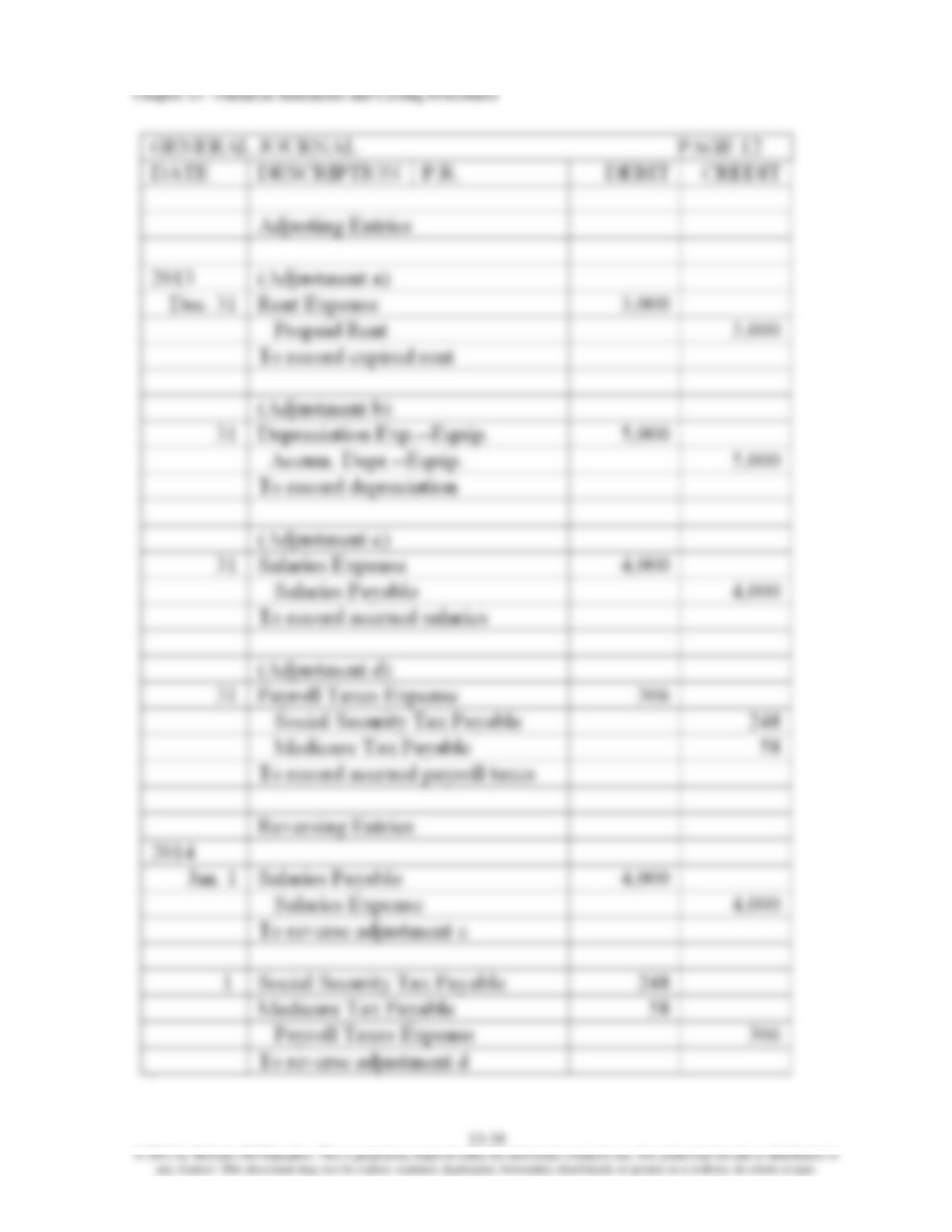

81. The data below concerns adjustments to be made at the Conner Company. Record the

adjusting entries on page 12 of a general journal as of December 31, 2013. On the same page

of the general journal, record the reversing entries as of January 1, 2014. Include descriptions.

Adjustment data:

(a) On October 1, 2013, the firm paid rent of $6,000 in advance for a 6-month period.

(b) A total of $5,000 should be recorded as depreciation of equipment for 2013.

(c) On December 31, 2013, the firm owed salaries of $4,000 that will not be paid until

January 2014.

(d) On December 31, 2013, the firm owed the employer's social security (6.2%) and Medicare

(1.45%) taxes on all of the accrued salaries.

13-38

© 2012 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

13-39

82. The data below concerns adjustments to be made at the Tyson Company. Record the

adjusting entries on page 12 of a general journal as of December 31, 2013. On the same page

of the general journal, record the reversing entries as of January 1, 2014. Include descriptions.

Adjustment data:

(a) On October 1, 2013, the firm paid rent of $18,000 in advance for a 6-month period.

(b) A total of $15,000 should be recorded as depreciation of equipment for 2013.

(c) On December 31, 2013, the firm owed salaries of $12,000 that will not be paid until

January 2014.

(d) On December 31, 2013, the firm owed the employer's social security (6.2%) and Medicare

(1.45%) taxes on all of the accrued salaries.

13-40

© 2012 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

13-41

83. A. Check all of the following accounts that would be classified as a current asset.

B. Check all of the following accounts that would be classified as a current liability.

Chapter 13 - Financial Statements and Closing Procedures

Matching Questions

84. Match the accounting terms with the description by entering the proper number.

1. The amount of gross profit from each dollar of sales

Single-step

income statement

8

2. A format by which revenues and expenses on the

income statement, and assets and liabilities on the

balance sheet, are divided into groups of similar accounts

and a subtotal is given for each group

Gross profit

6

3. The ease with which an item can be converted into

cash

Classified

financial statement

2

4. A type of income statement on which several subtotals

are computed before the net income is calculated

Multiple-step

income statement

4

5. Property that will be used in the business for longer

than one year

Gross profit

percentage

1

6. The difference between net sales and the cost of goods

sold

Inventory

turnover

13

7. Debts that must be paid within one year

Liquidity

3

8. A type of income statement where only one

computation is needed to determine the net income (total

revenue - total expenses = net income)

Plant and

equipment

5

9. A relationship between current assets and current

liabilities that provides a measure of a firm's ability to

pay its current debts

Reversing entries

11

10. Debts of a business that are due more than one year

in the future

Current ratio

9

11. Journal entries made to reverse the effect of certain

adjusting entries involving accrued income or accrued

expenses to avoid problems in recording future payments

or receipts of cash in a new accounting period

Current assets

12

12. Assets consisting of cash, items that normally will be

converted into cash within one year, or items that will be

used up within one year

Long-term

liabilities

10

13. The number of times inventory is purchased and sold

during the accounting period

Current

liabilities

7