THE DEUTSCH-CASELLA JOINT VENTURE AND

[YELLOW TAIL]® WINES: TRADING UP OR TRADING DOWN?[1]

Armand Gilinsky, Jr. (Sonoma State University)

Raymond H. Lopez (Pace University)

America’s W. J. Deutsch & Sons (a wine importer) and Australia’s Casella (a wine

producer) operate a joint venture that has successfully launched the [Yellow

Tail]® wines. Now facing a financial crisis, top executives face a strategic decision in

terms of pricing.

We should be very proud of our portfolio of wine brands, but we admit that the [yellow tail]® story

has redefined and refocused our firm over the last decade. While the current economic environment

creates uncertainty for most businesses, we must be confident of our ability to navigate uncharted

waters and continue to compete in global markets. — Bill Deutsch

These were the words of Bill Deutsch, founder and chairman of W.J. Deutsch & Sons, a New York-based

importer, to his son, Peter. W.J. Deutsch & Sons was joint venture (JV) partner in the export and sale of

the [yellow tail]® brand of wines from the Casella family winery in New South Wales, Australia. It was

early February 2009. W.J. Deutsch & Sons’ wines were sold to trade intermediaries (wholesalers and

distributors) with marketing and promotional support and in turn, offered to retailers and consumers at

fair market prices.

Bill opened a strategy session with his management team. They met to review final 2008 revenue and

cost data and decide on a strategy for the next two years. Success of [yellow tail]® wines, thecore

brandin W.J. Deutsch & Sons’ portfolio of brands, was expected to play a crucial role in the company’s

future, now guided by CEO Peter Deutsch, Bill’s son.

John Casella, Managing Director of Casella Wines, then joined the meeting on the speakerphone from

his home in Australia: “What are your feelings about going down market on price? Do you believe we

could adopt a differential pricing strategy for the white wines in our U.S. and even our Caribbean

markets, while maintaining prices on our red wines?”

Peter Deutsch mused, “Could ‘trading down’ by customers actually benefit the firm and the brand?

Would recent promotion strategies be sufficient to maintain current [yellow tail]® sales volumes?” He

considered whether or not to leave pricing on all brands unchanged, adopt John Casella’s suggestion to

drop prices on some brands but not others, or possibly even raise prices on some or all brands despite a

turbulent economic outlook for 2009 and beyond. Then again, perhaps it was now time to consider new

brands from other producers besides the Casellas, to add more diversity to the Deutsch wine portfolio.

Peter felt that he had to be careful to decide on a course of action that would benefit all stakeholders in

the brand, not only in the short term, but also for years to come. After all, [yellow tail]® had been the

number one imported brand in the United States for only six years.

A CHANGING LANDSCAPE

During the global recession that had begun in 2008, for many wine producers and importers, survival

was at stake. Wholesalers and distributors had become reluctant to take on any new wine inventory

until existing levels were depleted. Restaurants and hotels that sold wine “on–premises” severely

curtailed new wine purchases. To reduce existing stocks, “off–premises” retailers, such as chain

supermarkets and specialty wine shops, began using quantity discounts and special limited-time

promotions. Numerous small-to-medium-sized domestic wine producers and importers, unable to sell

through traditional wholesale channels began going into default. After more than a quarter century of

wine consumers’ continuously “trading up” to higher priced, higher quality wine brands, a “trading

down” phenomenon had now taken hold.

Consumption Patterns

The “Baby Boom” generation (born 1946-1964) represented the core market for wine in the United

States in early 2009. This demographic segment was not only aging, but also increasing in spending

power, and thus willing to spend its disposable income on wine, at least up until the global financial

crisis began in 2008.

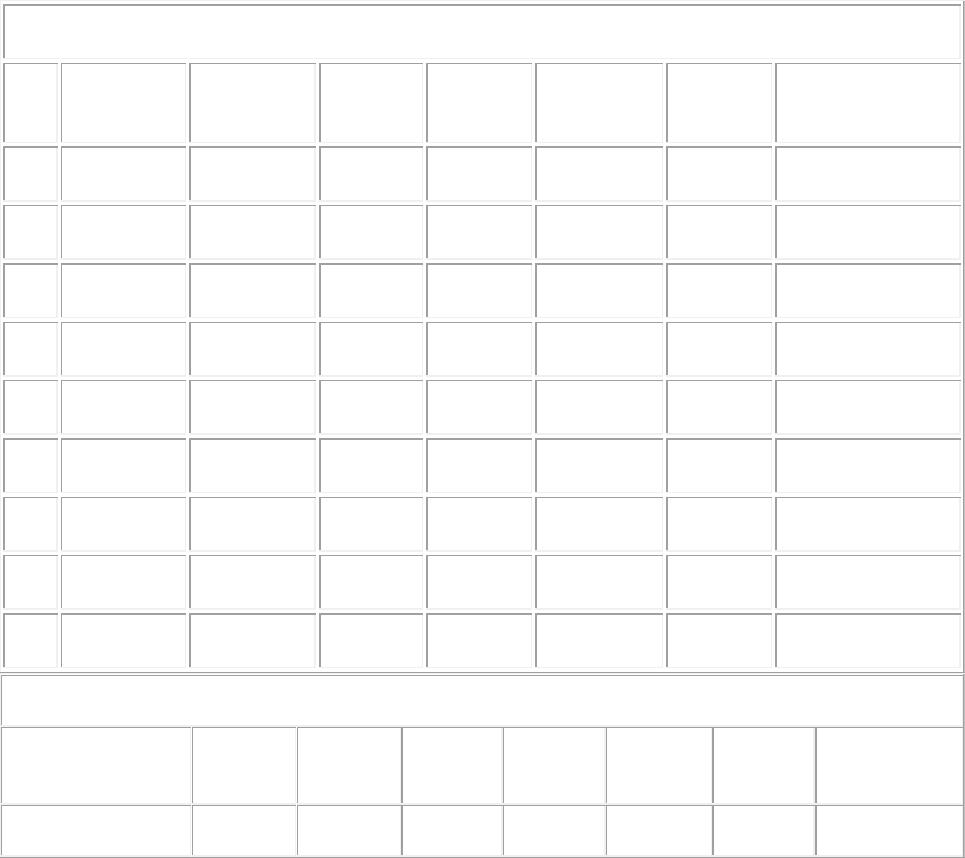

Wine consumption in the United States increased every year from 2000–2008, according to the US

Department of Commerce and Adams Wine Handbook, the latter an industry trade publication (shown

in Exhibit 1). Domestically produced wine, predominantly from California, made some inroads into the

US market. From 2000–2008, the consumption of domestically produced table wine grew 22%, while

over the same period inroads made by wine imports led to expansion in that category approximately

74%. By comparison, however, imported table wine, which accounted for 10.3% of total US wine

consumption in 1991, accounted for 23.5% by 2008. Also, share of imports by volume, which was 14.5%

in 1991, grew to 25.6% in 2008, according to the U.S. Department of Commerce and Adams Wine

Handbook.

Exhibit 1

Domestic v. Imported Wine Consumption: % Share and Growth Rates in the United

States, by Category, 2003-2008

% share by volume (000 nine-liter cases)

Year

Table

Domestic

Other

Domestic

Total

Domestic

Table

Imported

Other

Imported

Total

Imported

Total Wine

Consumption

2008

68.11

6.13

74.24

23.50

2.60

25.76

100.00

2007

67.27

6.26

73.53

24.14

2.33

26.47

100.00

2006

67.53

6.47

74.00

23.64

2.36

26.00

100.00

2005

67.82

6.75

74.57

23.09

2.34

25.43

100.00

2004

68.32

7.10

75.42

22.27

2.32

24.58

100.00

2003

68.69

7.42

76.11

21.56

2.34

23.89

100.00

2002

69.27

8.15

77.42

20.18

2.40

22.58

100.00

2001

70.32

8.99

79.31

18.26

2.43

20.69

100.00

2000

71.23

8.97

80.20

17.19

2.61

19.80

100.00

Growth rate %ages by volume (000 nine-liter cases)

Year

Table

Domestic

Other

Domestic

Total

Domestic

Table

Imported

Other

Imported

Total

Imported

Total Wine

Consumption

2008

2.16

-1.15

1.88

-1.77

12.63

-1.80

0.91

2007

2.83

-0.19

2.56

5.38

1.87

5.06

3.21

2006

2.96

-0.87

2.62

5.85

4.29

5.71

3.40

2005

1.34

-2.87

0.95

5.88

3.19

5.63

2.10

2004

3.25

-0.68

2.86

7.22

2.98

6.81

3.81

2003

3.98

-4.60

3.08

12.02

1.96

10.95

4.86

2002

3.48

-4.76

2.55

16.09

3.70

14.63

5.05

2001

0.07

1.59

0.24

7.68

-5.47

5.94

1.37

CAGR, 2000-2008

2.50

-1.71

2.09

7.18

3.04

6.52

3.08

Note: The “Other” category includes fortified wines such as vermouth, sherry, and port.

Source: Case authors’ analysis of data from Adams Wine Handbook, 1999-

2008, www.beveragehandbooks.com.

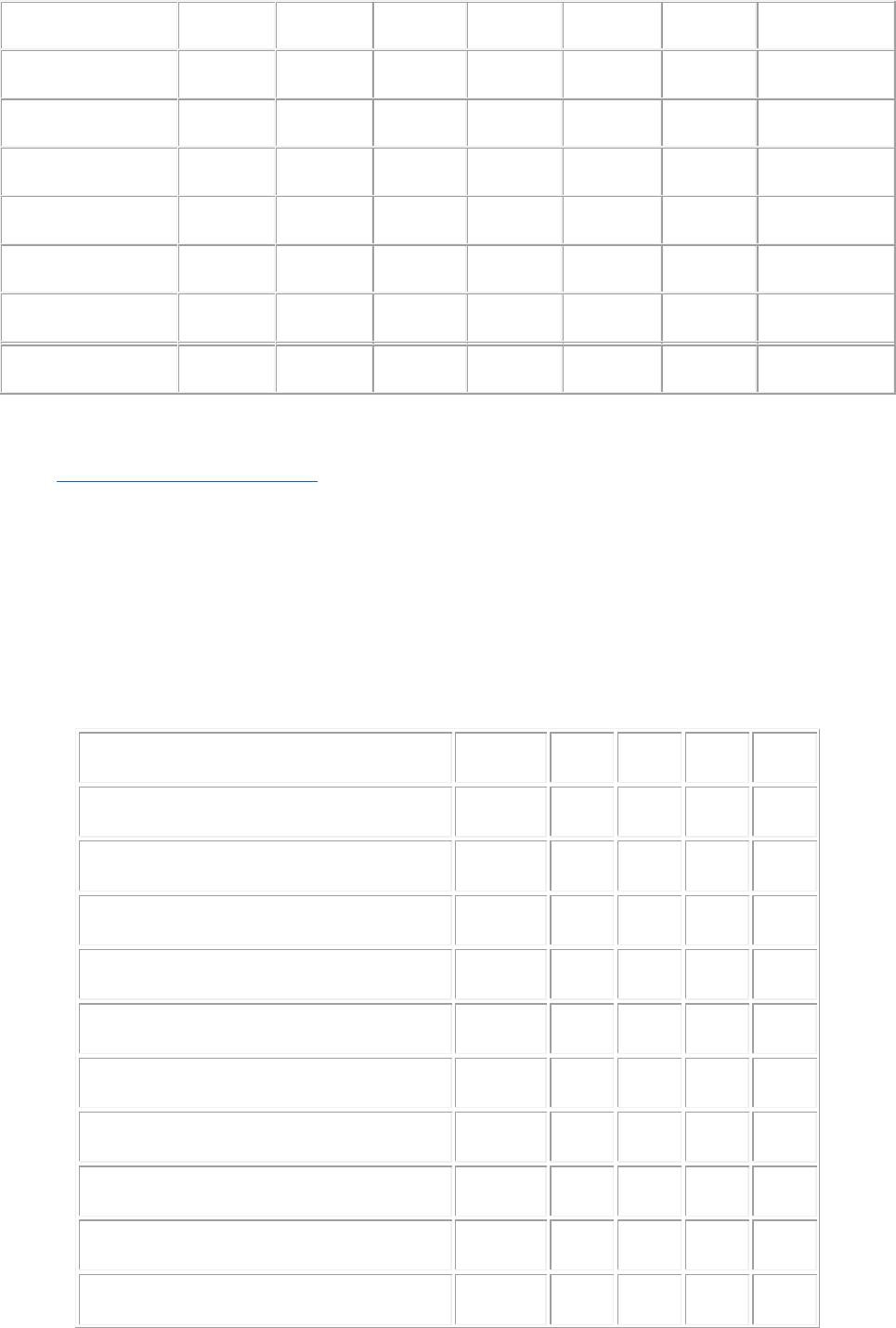

Exhibit 2 presents an analysis of wine imports from 2003–2008 by country of origin, showing that Italy

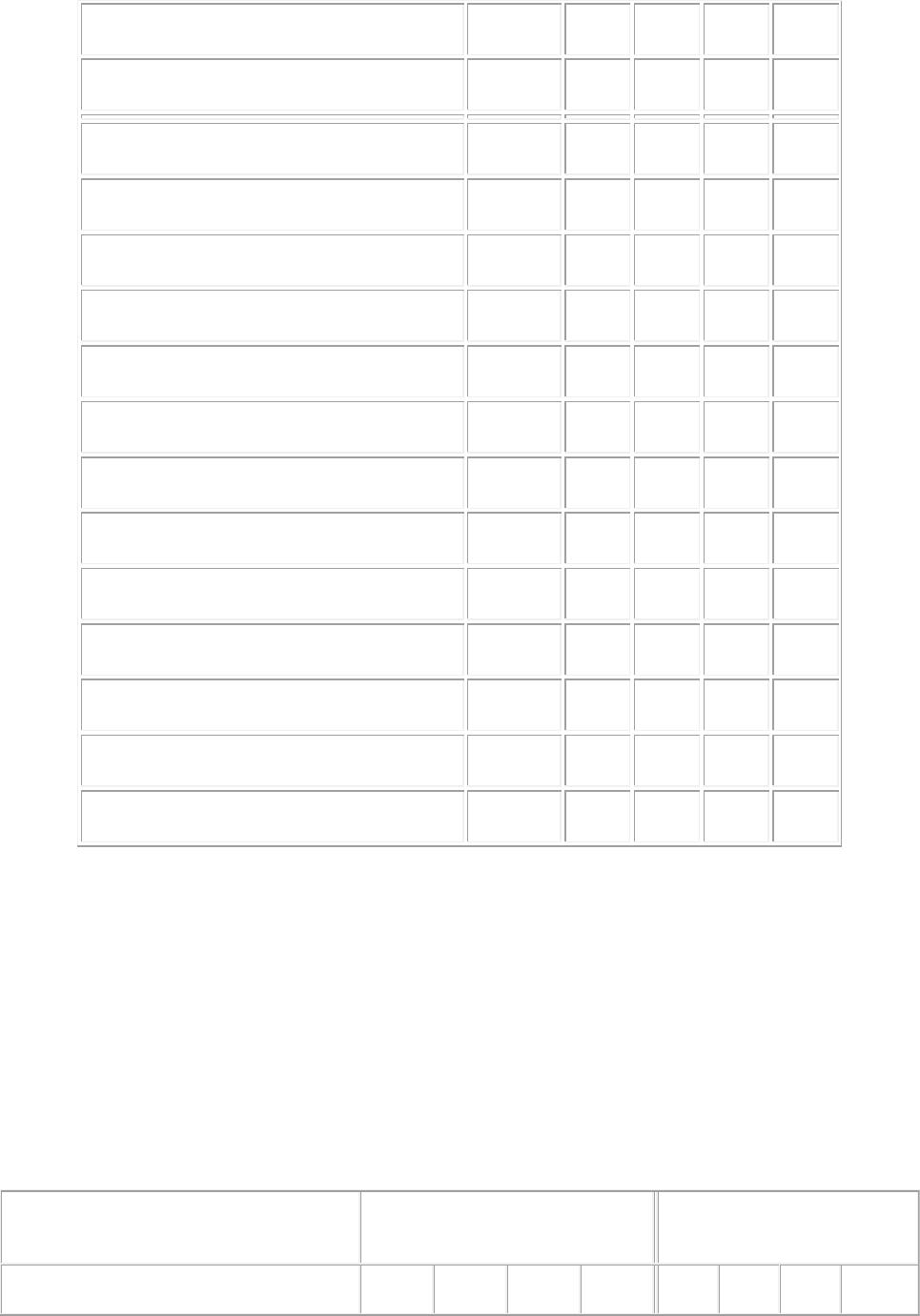

and Australia led in total exports to the United States. Exhibit 3 shows the analysis of sales and market

shares of the 25 largest wine brands imported to the United States from the years 2005–2008.

Exhibit 2

Top Ten Wine Exporters to the United States by Country

Ranked by % Share in the U.S., 2004-2008

% share by volume of shipments

2008

2007

2006

2005

2004

Italy

29.37

30.49

30.34

30.98

31.45

Australia

24.34

25.18

29.11

30.14

30.39

France

12.24

13.78

13.90

12.09

13.10

Argentina

10.15

8.47

5.45

4.20

3.73

Chile

8.39

7.37

7.32

8.58

9.07

Spain

4.38

4.20

4.18

4.13

3.88

Germany

3.86

3.99

3.86

3.69

3.20

New Zealand

2.67

2.58

2.06

2.22

1.44

South Africa

2.00

1.26

1.29

1.27

1.09

Total, Top 10 Exporting Countries

97.41

97.33

97.53

97.31

97.33

Other Exporting Countries

2.59

2.67

2.47

2.69

2.67

Total

100.00

100.00

100.00

100.00

100.00

Growth rates by volume of shipments

5Y CAGR

2008

2007

2006

2005

Italy

3.56

-5.77

8.46

6.53

9.43

Australia

0.44

-5.44

-6.61

5.03

10.18

France

3.57

-13.15

7.02

25.04

2.57

Argentina

28.27

17.26

67.67

41.11

25.18

Chile

3.38

11.43

8.67

-7.26

5.16

Spain

7.60

1.97

8.56

10.16

18.26

Germany

9.03

-5.29

11.52

13.76

28.21

New Zealand

18.73

0.88

35.47

0.93

71.08

South Africa

18.51

55.73

4.92

10.45

29.52

Total, Top 10 Exporting Countries

5.01

-2.10

7.73

8.99

11.06

Other Exporting Countries

4.40

-5.09

16.66

-0.15

12.16

Total

4.99

-2.18

7.95

8.75

11.09

Notes:

(a) Includes wine coolers and other imported wines not listed

Numbers may not add due to rounding.

ACGR=Annual compound growth rate

Source: Case authors’ analysis of data from U.S. Dept. of Commerce and Adams Wine Handbook, 2009.

Exhibit 3

Shrinking Share of Top 25 Table Wine Importers to the United States, Depletions and

Share, 2005-2008

— Thousands of 9-liter cases

—

Imported Table Wine

Share

2008

2007

2006

2005

2008

2007

2006

2005

Yellow Tail (Deutsch)

8,300

8,050

8,050

7,500

11.4

10.7

11.2

10.8

Total Top 25

35,145

37,135

36,500

34,995

48.3

49.5

50.7

50.6

Other Brands

37,625

37,905

35,445

34,155

51.7

50.5

49.3

49.4

Total Imported Table Wine

Depletions

72,770

75,040

71,945

69,150

100

100

100

100

Note: Depletions are defined as sales of wines from inventories.

Source: Case authors’ analysis of data from Impact Databank, Table 6-43 (2008 edition) and Table 6-

44 (2009 edition).

Markets and Segmentation

Table wine was considered a luxury niche product in the universe of all alcoholic beverages, ranging

from beer to distilled spirits. Table wine had 7%–14 % alcohol content by volume and was traditionally

consumed at meals.2 A case of wine normally included twelve (12) 750ml bottles, or nine liters of wine.

Price segments. Regardless of where they were produced, table wines that retailed for less than $3.00

per 750ml bottle were deemed to be in the generic, economy, or “jug” wine category, while those wines

selling for more than $3.00 per bottle were considered to be in the premium wine category. Most

bottled wines in the premium category showed a vintage date on their labels—the product was made

with at least 95 % of grapes harvested, crushed, and fermented in the calendar year shown on the label

and also used grapes from an appellation of origin (i.e., Napa Valley, Central Coast, Willamette Valley).

Consumer segments. In 2008, the age group comprising 25-54 year-olds constituted the largest

component of US “core” wine drinkers. In the last two decades of the previous century, the US wine

industry had almost entirely relied on the Baby-Boomer generation (in 2009 comprising a 45-63 year-

old age group) to stimulate demand growth in the short term, and began turning its attention to the