Why This Chapter Matters to You

In your

professional

life

ACCOUNTING You need to understand how to calculate and analyze

operating and financial leverage and to be familiar with the tax and

earnings effects of various capital structures.

INFORMATION SYSTEMS You need to understand the types of capital

and what capital structure is because you will provide much of the

information needed in management’s determination of the best capital

structure for the firm.

MANAGEMENT You need to understand leverage so that you can con-

trol risk and magnify returns for the firm’s owners and to understand

capital structure theory so that you can make decisions about the firm’s

optimal capital structure.

MARKETING You need to understand breakeven analysis, which you

will use in pricing and product feasibility decisions.

OPERATIONS You need to understand the impact of fixed and variable

operating costs on the firm’s breakeven point and its operating

leverage because these costs will have a major impact on the firm’s risk

and return.

Like corporations, you routinely

incur debt, using both credit cards

for short-term needs and negotiated long-term loans. When you borrow

over the long term, you experience the benefits and consequences of

leverage. Also, the level of your outstanding debt relative to net worth

is conceptually the same as a firm’s capital structure. It reflects your

financial risk and affects the availability and cost of borrowing.

In your

personal

life

Learning Goals

Discuss leverage, capital

structure, breakeven analysis, the

operating breakeven point, and

the effect of changing costs on the

breakeven point.

Understand operating, financial,

and total leverage and the

relationships among them.

Describe the types of capital,

external assessment of capital

structure, the capital structure of

non–U.S. firms, and capital

structure theory.

Explain the optimal capital

structure using a graphical view

of the firm’s cost-of-capital

functions and a zero-growth

valuation model.

Discuss the EBIT–EPS approach to

capital structure.

Review the return and risk of

alternative capital structures, their

linkage to market value, and

other important considerations

related to capital structure.

LG 6

LG 5

LG 4

LG 3

LG 2

LG 1

13 Leverage and Capital

Structure

506

507

Trading Equity for Debt

As the broader U.S. stock market roared back to

life in 2009, shares in the biotechnology firm,

Genzyme, dropped 28 percent. Contamination prob-

lems at Genzyme’s main manufacturing facility

prompted the firm to stop production during the

cleanup, and that in turn led to production shortages of

some of the firms best-selling drugs. That performance

irked one of Genzyme’s largest shareholders, Carl

Icahn, who promptly launched a proxy fight to gain four seats on the company’s board of direc-

tors. In June 2010, Genzyme reached an agreement with Icahn giving his representatives two

seats on their board.

Just eight days later, Genzyme’s stock rose 3.7 percent on the announcement that the com-

pany would issue $1 billion in debt. Genzyme planned to use the proceeds from the issue,

along with $1 billion in cash reserves, to repurchase approximately 40 million shares of

common stock. That move represented a significant shift in the firm’s capital structure (that is, its

mix of debt and equity financing), a move that would put more cash in the hands of share-

holders and apply more pressure on Genzyme management to generate positive cash flow from

the business. With more of its financing coming from debt, Genzyme was adding financial

leverage to its business, meaning that if the firm succeeds in selling its products, the returns to

shareholders will be magnified. However, if Genzyme instead experiences further declines in its

business, paying back the debt may prove to be difficult, and returns to shareholders will suffer

as a result.

Genzyme Corp.

508 PART 6 Long-Term Financial Decisions

13.1 Leverage

Leverage refers to the effects that fixed costs have on the returns that shareholders

earn. By “fixed costs” we mean costs that do not rise and fall with changes in a

firm’s sales. Firms have to pay these fixed costs whether business conditions are

good or bad. These fixed costs may be operating costs, such as the costs incurred

by purchasing and operating plant and equipment, or they may be financial costs,

such as the fixed costs of making debt payments. Generally, leverage magnifies

both returns and risks. A firm with more leverage may earn higher returns on

average than a firm with less leverage, but the returns on the more leveraged firm

will also be more volatile.

Many business risks are out of the control of managers, but not the risks

associated with leverage. Managers can limit the impact of leverage by adopting

strategies that rely more heavily on variable costs than on fixed costs. For

example, a basic choice that many firms confront is whether to make their own

products or to outsource manufacturing to another firm. A company that does its

own manufacturing may invest billions in factories around the world. These fac-

tories generate costs whether they are running or not. In contrast, a company that

outsources production can completely eliminate its manufacturing costs simply

by not placing orders. Costs for a firm like this are more variable and will gener-

ally rise and fall as demand warrants.

In the same way, managers can influence leverage in their decisions about

how the company raises money to operate. The amount of leverage in the firm’s

capital structure—the mix of long-term debt and equity maintained by the firm—

can significantly affect its value by affecting return and risk. The more debt a firm

issues, the higher are its debt repayment costs, and those costs must be paid

regardless of how the firm’s products are selling. Because leverage can have such

a large impact on a firm, the financial manager must understand how to measure

and evaluate leverage, particularly when making capital structure decisions.

Table 13.1 uses an income statement to highlight where different sources of

leverage come from.

LG 1

leverage

Refers to the effects that fixed

costs have on the returns that

shareholders earn; higher

leverage generally results in

higher but more volatile

returns.

capital structure

The mix of long-term debt and

equity maintained by the firm.

General Income Statement Format and Types of Leverage

Sales revenue

Less: Cost of goods sold

Operating leverage Gross profits

Less: Operating expenses

Earnings before interest and taxes (EBIT)

Less: Interest Total leverage

Net profits before taxes

Less: Taxes

Financial leverage Net profits after taxes

Less: Preferred stock dividends

Earnings available for common stockholders

Earnings per share (EPS)

TABLE 13.1

LG 2

•Operating leverage is concerned with the relationship between the firm’s sales

revenue and its earnings before interest and taxes (EBIT) or operating profits.

When costs of operations (such as cost of goods sold and operating expenses) are

largely fixed, small changes in revenue will lead to much larger changes in EBIT.

•Financial leverage is concerned with the relationship between the firm’s EBIT

and its common stock earnings per share (EPS). On the income statement, you

can see that the deductions taken from EBIT to get to EPS include interest,

taxes, and preferred dividends. Taxes are clearly variable, rising and falling

with the firm’s profits, but interest expense and preferred dividends are usu-

ally fixed. When these fixed items are large (that is, when the firm has a lot of

financial leverage), small changes in EBIT produce larger changes in EPS.

•Total leverage is the combined effect of operating and financial leverage. It is

concerned with the relationship between the firm’s sales revenue and EPS.

We will examine the three types of leverage concepts in detail. First, though,

we will look at breakeven analysis, which lays the foundation for leverage con-

cepts by demonstrating the effects of fixed costs on the firm’s operations.

BREAKEVEN ANALYSIS

Firms use breakeven analysis, also called cost-volume-profit analysis, (1) to deter-

mine the level of operations necessary to cover all costs and (2) to evaluate the

profitability associated with various levels of sales. The firm’s operating

breakeven point is the level of sales necessary to cover all operating costs. At that

point, earnings before interest and taxes (EBIT) equals $0.1

The first step in finding the operating breakeven point is to divide the cost of

goods sold and operating expenses into fixed and variable operating costs. Fixed

costs are costs that the firm must pay in a given period regardless of the sales

volume achieved during that period. These costs are typically contractual; rent,

for example, is a fixed cost. Because fixed costs do not vary with sales, we typi-

cally measure them relative to time. For example, we would typically measure

rent as the amount due per month. Variable costs vary directly with sales volume.

Shipping costs, for example, are a variable cost.2We typically measure variable

costs in dollars per unit sold.

Algebraic Approach

Using the following variables, we can recast the operating portion of the firm’s

income statement given in Table 13.1 into the algebraic representation shown in

Table 13.2.

VC =variable operating cost per unit

FC =fixed operating cost per period

Q=sales quantity in units

P=sale price per unit

CHAPTER 13 Leverage and Capital Structure 509

1. Quite often, the breakeven point is calculated so that it represents the point at which all costs—both operating

and financial—are covered. For now, we focus on the operating breakeven point as a way to introduce the concept

of operating leverage. We will discuss financial leverage later.

2. Some costs, commonly called semifixed or semivariable, are partly fixed and partly variable. An example is sales

commissions that are fixed for a certain volume of sales and then increase to higher levels for higher volumes. For

convenience and clarity, we assume that all costs can be classified as either fixed or variable.

breakeven analysis

Used to indicate the level of

operations necessary to cover

all costs and to evaluate the

profitability associated with

various levels of sales; also

called

cost-volume-profit

analysis

.

operating breakeven point

The level of sales necessary to

cover all

operating costs;

the

point at which EBIT $0.=

Rewriting the algebraic calculations in Table 13.2 as a formula for earnings

before interest and taxes yields Equation 13.1:

(13.1)

Simplifying Equation 13.1 yields:

(13.2)

As noted above, the operating breakeven point is the level of sales at which all

fixed and variable operating costs are covered—the level at which EBIT equals

$0. Setting EBIT equal to $0 and solving Equation 13.2 for Qyields:

(13.3)

Qis the firm’s operating breakeven point.3

Assume that Cheryl’s Posters, a small poster retailer, has fixed operating costs of

$2,500. Its sale price is $10 per poster, and its variable operating cost is $5 per

poster. Applying Equation 13.3 to these data yields:

At sales of 500 units, the firm’s EBIT should just equal $0. The firm will have

positive EBIT for sales greater than 500 units and negative EBIT, or a loss, for

sales less than 500 units. We can confirm this by substituting values above and

below 500 units, along with the other values given, into Equation 13.1.

Q=$2,500

$10 –$5 =$2,500

$5 =500 units

Example 13.1 3

Q=FC

P–VC

EBIT =Q*(P–VC)–FC

EBIT =(P*Q)–FC –(VC *Q)

510 PART 6 Long-Term Financial Decisions

Operating Leverage, Costs, and Breakeven Analysis

Algebraic

Item representation

Sales revenue (PQ)

Operating leverage Less: Fixed operating costs FC

Less: Variable operating costs

Earnings before interest and taxes EBIT

–(VC *Q)

–

*

TABLE 13.2

3. Because the firm is assumed to be a single-product firm, its operating breakeven point is found in terms of unit

sales, Q. For multiproduct firms, the operating breakeven point is generally found in terms of dollar sales, S. This is

done by substituting the contribution margin, which is 100 percent minus total variable operating costs as a per-

centage of total sales, denoted VC%, into the denominator of Equation 13.3. The result is Equation 13.3a:

(13.3a)

This multiproduct-firm breakeven point assumes that the firm’s product mix remains the same at all levels of sales.

S=FC

1–VC%

Graphical Approach

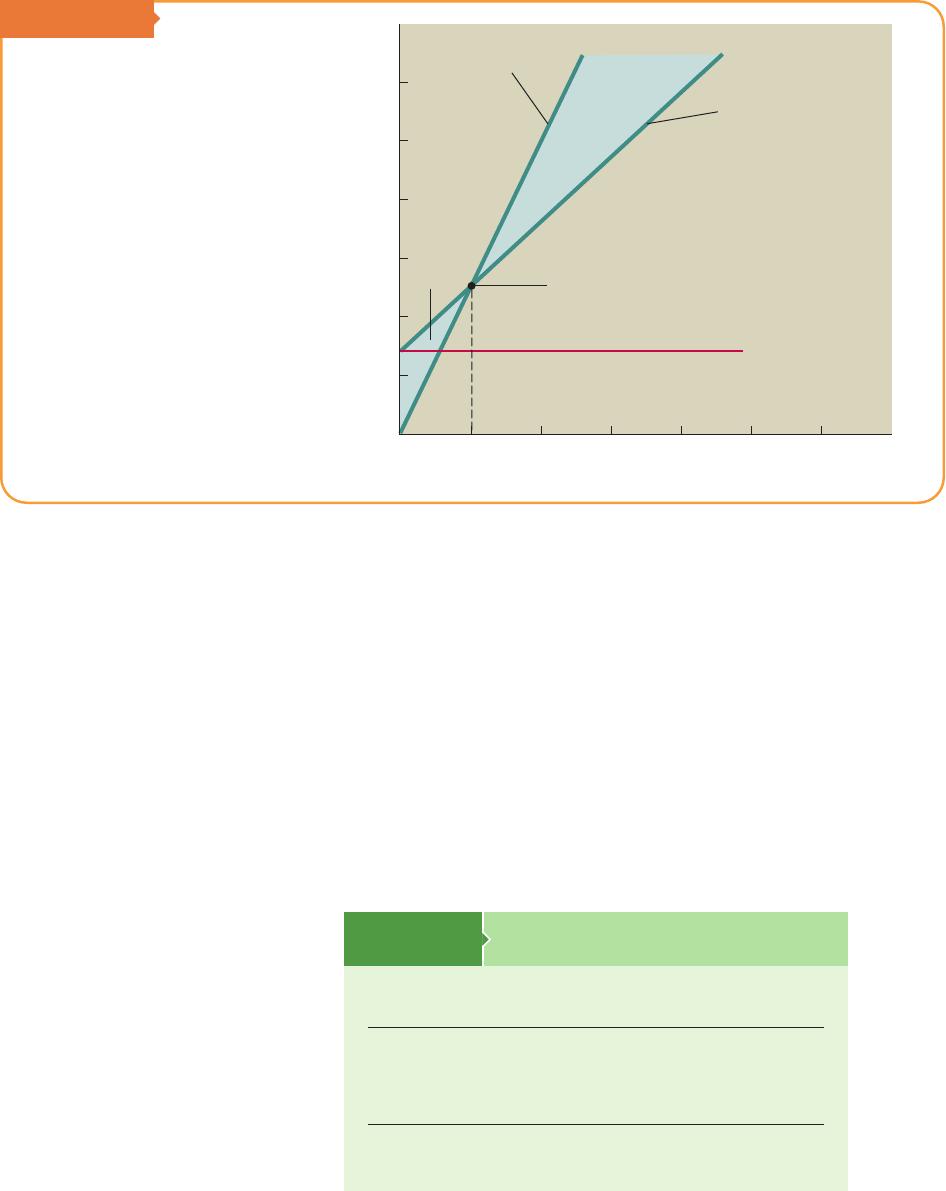

Figure 13.1 presents in graphical form the breakeven analysis of the data in the

preceding example. The firm’s operating breakeven point is the point at which its

total operating cost—the sum of its fixed and variable operating costs—equals

sales revenue. At this point, EBIT equals $0. The figure shows that for sales

below 500 units, total operating cost exceeds sales revenue, and EBIT is less than

$0 (a loss). For sales above the breakeven point of 500 units, sales revenue

exceeds total operating cost, and EBIT is greater than $0.

Changing Costs and the Operating Breakeven Point

A firm’s operating breakeven point is sensitive to a number of variables: fixed

operating cost (FC), the sale price per unit (P), and the variable operating cost per

unit (VC). Refer to Equation 13.3 to see how increases or decreases in these vari-

ables affect the breakeven point. The sensitivity of the breakeven sales volume

(Q) to an increase in each of these variables is summarized in Table 13.3. As

CHAPTER 13 Leverage and Capital Structure 511

Sales

Revenue

Total

Operating

Cost

Operating

Breakeven

Point

EBIT

Fixed

Operating

Cost

5000 1,000 1,500 2,000 2,500 3,000

Loss

12,000

10,000

8,000

6,000

4,000

2,000

Costs/Revenues ($)

Sales (units)

FIGURE 13.1

Breakeven Analysis

Graphical operating

breakeven analysis

Sensitivity of Operating Breakeven Point

to Increases in Key Breakeven Variables

Effect on operating

Increase in variable breakeven point

Fixed operating cost (FC) Increase

Sale price per unit (P) Decrease

Variable operating cost per unit (VC) Increase

Note: Decreases in each of the variables shown would have the opposite

effect on the operating breakeven point.

TABLE 13.3

might be expected, an increase in cost (FC or VC) tends to increase the operating

breakeven point, whereas an increase in the sale price per unit (P) decreases the

operating breakeven point.

Assume that Cheryl’s Posters wishes to evaluate the impact of several options:

(1) increasing fixed operating costs to $3,000, (2) increasing the sale price per

unit to $12.50, (3) increasing the variable operating cost per unit to $7.50, and

(4) simultaneously implementing all three of these changes. Substituting the

appropriate data into Equation 13.3 yields the following results:

Comparing the resulting operating breakeven points to the initial value of 500

units, we can see that the cost increases (actions 1 and 3) raise the breakeven

point, whereas the revenue increase (action 2) lowers the breakeven point. The

combined effect of increasing all three variables (action 4) also results in an

increased operating breakeven point.

Rick Polo is considering having a new fuel-saving device

installed in his car. The installed cost of the device is $240 paid

up front, plus a monthly fee of $15. He can terminate use of the device any time

without penalty. Rick estimates that the device will reduce his average monthly

gas consumption by 20%, which, assuming no change in his monthly mileage,

translates into a savings of about $28 per month. He is planning to keep the car

for 2 more years and wishes to determine whether he should have the device

installed in his car.

To assess the financial feasibility of purchasing the device, Rick calculates

the number of months it will take for him to break even. Letting the installed

cost of $240 represent the fixed cost (FC), the monthly savings of $28 repre-

sent the benefit (P), and the monthly fee of $15 represent the variable cost

(VC), and substituting these values into the breakeven point equation,

Equation 13.3, we get:

Because the fuel-saving device pays itself back in 18.5 months, which is less than

the 24 months that Rick is planning to continue owning the car, he should have

the fuel-saving device installed in his car.

=18.5 months

Breakeven point (in months) =$240 ,($28 –$15) =$240 ,$13

Personal Finance Example 13.3 3

(4) Operating breakeven point =$3,000

$12.50 –$7.50 =600 units

(3) Operating breakeven point =$2,500

$10 –$7.50 =1,000 units

(2) Operating breakeven point =$2,500

$12.50 –$5 =3331

>3 units

(1) Operating breakeven point =$3,000

$10 –$5 =600 units

Example 13.2 3

512 PART 6 Long-Term Financial Decisions

OPERATING LEVERAGE

Operating leverage results from the existence of fixed costs that the firm must pay

to operate. Using the structure presented in Table 13.2, we can define operating

leverage as the use of fixed operating costs to magnify the effects of changes in

sales on the firm’s earnings before interest and taxes.

Using the data for Cheryl’s Posters (sale price, P$10 per unit; variable oper-

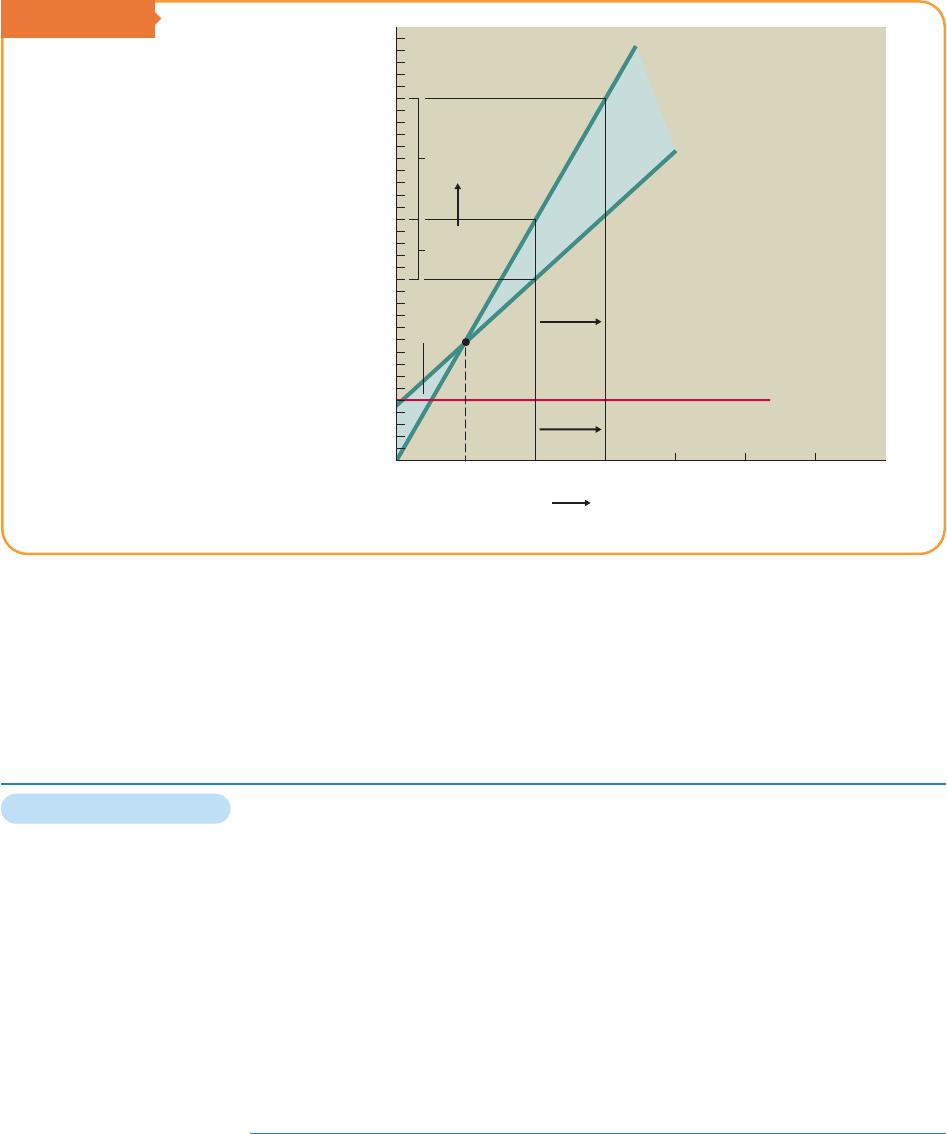

ating cost, VC $5 per unit; fixed operating cost, FC $2,500), Figure 13.2

presents the operating breakeven graph originally shown in Figure 13.1. The

additional notations on the graph indicate that as the firm’s sales increase from

1,000 to 1,500 units (Q1to Q2), its EBIT increases from $2,500 to $5,000 (EBIT1

to EBIT2). In other words, a 50% increase in sales (1,000 to 1,500 units) results

in a 100% increase in EBIT ($2,500 to $5,000). Table 13.4 includes the data for

Figure 13.2 as well as relevant data for a 500-unit sales level. We can illustrate

two cases using the 1,000-unit sales level as a reference point.

Case 1 A 50% increase in sales (from 1,000 to 1,500 units) results in a 100%

increase in earnings before interest and taxes (from $2,500 to $5,000).

Case 2 A 50% decrease in sales (from 1,000 to 500 units) results in a 100%

decrease in earnings before interest and taxes (from $2,500 to $0).

From the preceding example, we see that operating leverage works in both

directions. When a firm has fixed operating costs, operating leverage is present.

== =

Example 13.4 3

CHAPTER 13 Leverage and Capital Structure 513

operating leverage

The use of

fixed operating

costs

to magnify the effects of

changes in sales on the firm’s

earnings before interest and

taxes.

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

5000 1,000 1,500 2,000 2,500 3,000

Q1Q2

Sales (units)

Costs/Revenues ($)

EBIT1

$2,500

EBIT2

$5,000

Loss

EBIT

Fixed

Operating

Cost

Total

Operating

Cost

Sales

Revenue

FIGURE 13.2

Operating Leverage

Breakeven analysis and

operating leverage

An increase in sales results in a more-than-proportional increase in EBIT; a

decrease in sales results in a more-than-proportional decrease in EBIT.

Measuring the Degree of Operating Leverage (DOL)

The degree of operating leverage (DOL) is a numerical measure of the firm’s

operating leverage. It can be derived using the following equation:4

(13.4)

Whenever the percentage change in EBIT resulting from a given percentage

change in sales is greater than the percentage change in sales, operating leverage

exists. This means that as long as DOL is greater than 1, there is operating

leverage.

Applying Equation 13.4 to cases 1 and 2 in Table 13.4 yields the following results:

Case 1:

Case 2:

Because the result is greater than 1, operating leverage exists. For a given base

level of sales, the higher the value resulting from applying Equation 13.4, the

greater the degree of operating leverage.

–100%

–50% =2.0

+100%

+50% =2.0

Example 13.5 3

DOL =Percentage change in EBIT

Percentage change in sales

514 PART 6 Long-Term Financial Decisions

TABLE 13.4

4. The degree of operating leverage also depends on the base level of sales used as a point of reference. The closer the

base sales level used is to the operating breakeven point, the greater the operating leverage. Comparison of the

degree of operating leverage of two firms is valid only when the same base level of sales is used for both firms.

degree of operating

leverage (DOL)

The numerical measure of the

firm’s operating leverage.

The EBIT for Various Sales Levels

Case 2 Case 1

⫺50% ⫹50%

Sales (in units) 500 1,000 1,500

Sales revenuea$5,000 $10,000 $15,000

Less: Variable operating costsb2,500 5,000 7,500

Less: Fixed operating costs

Earnings before interest and taxes (EBIT) $ 0 $ 2,500 $ 5,000

⫺100% ⫹100%

aSales revenue $10/unit sales in units.

bVariable operating costs $5/unit sales in units.*=

*=

2,5002,5002,500

A more direct formula for calculating the degree of operating leverage at a

base sales level, Q, is shown in Equation 13.5.5

(13.5)

Substituting , and into Equation

13.5 yields the following result:

The use of the formula results in the same value for DOL (2.0) as that found by

using Table 13.4 and Equation 13.4.6

See the Focus on Practice box for a discussion of operating leverage at software

maker Adobe.

DOL at 1,000 units =1,000 *($10 –$5)

1,000 *($10 –$5) –$2,500 =$5,000

$2,500 =2.0

FC =$2,500Q=1,000, P=$10, VC =$5

Example 13.6 3

DOL at base sales level Q =Q*(P–VC)

Q*(P–VC)–FC

CHAPTER 13 Leverage and Capital Structure 515

5. Technically, the formula for DOL given in Equation 13.5 should include absolute value signs because it is possible

to get a negative DOL when the EBIT for the base sales level is negative. Because we assume that the EBIT for the

base level of sales is positive, we do not use the absolute value signs.

6. When total revenue in dollars from sales—instead of unit sales—is available, the following equation, in which

TR total revenue in dollars at a base level of sales and TVC total variable operating costs in dollars, can be used:

This formula is especially useful for finding the DOL for multiproduct firms. It should be clear that because in the

case of a single-product firm, , substitution of these values into Equation 13.5

results in the equation given here.

TR =Q*P and TVC =Q*VC

DOL at base dollar sales TR =TR –TVC

TR –TVC –FC

==

focus on PRACTICE

Adobe’s Leverage

2009. A 22.6 percent increase in

2007 sales resulted in EBIT growth of

39.7 percent. In 2008, EBIT increased

just a little faster than sales did, but in

2009 as the economy endured a severe

recession, Adobe revenues plunged

17.7 percent. The effect of operating

leverage was that EBIT declined even

faster, posting a 35.3 percent drop.

3

Summarize the pros and cons of

operating leverage.

development and initial marketing stages.

The up-front development costs are fixed,

and subsequent production costs are

practically zero. The economies of scale

are huge: Once a company sells enough

copies to cover its fixed costs, incremen-

tal dollars go primarily to profit.

As demonstrated in the following

table, operating leverage magnified

Adobe’s

increase

in EBIT in 2007 while

magnifying the

decrease

in EBIT in

Adobe Systems, the

second largest PC soft-

ware company in the United States,

dominates the graphic design, imag-

ing, dynamic media, and authoring-tool

software markets. Website designers

favor its Photoshop and Illustrator soft-

ware applications, and Adobe’s

Acrobat software has become a stan-

dard for sharing documents online.

Adobe’s ability to manage discre-

tionary expenses helps keep its bottom

line strong. Adobe has an additional

advantage:

operating leverage,

the use

of fixed operating costs to magnify the

effect of changes in sales on earnings

before interest and taxes (EBIT). Adobe

and its peers in the software industry

incur the bulk of their costs early in a

product’s life cycle, in the research and

in practice

Item FY2007 FY2008 FY2009

Sales revenue (millions) $3,158 $3,580 $2,946

EBIT (millions) $947 $1,089 $705

(1) Percent change in sales 22.6% 13.4% ⫺17.7%

(2) Percent change in EBIT 39.7% 15.0% ⫺35.3%

DOL [(2)⫼(1)] 1.8 1.1 2.0

Source:

Adobe Systems Inc., “2009 Annual Report,” http.//www.adobe.com/aboutadobe/invrelations/pdfs/fy09_10k.pdf.

516 PART 6 Long-Term Financial Decisions

TABLE 13.5

Fixed Costs and Operating Leverage

Changes in fixed operating costs affect operating leverage significantly. Firms

sometimes can alter the mix of fixed and variable costs in their operations. For

example, a firm could make fixed-dollar lease payments rather than payments

equal to a specified percentage of sales. Or it could compensate sales representa-

tives with a fixed salary and bonus rather than on a pure percent-of-sales com-

mission basis. The effects of changes in fixed operating costs on operating

leverage can best be illustrated by continuing our example.

Assume that Cheryl’s Posters exchanges a portion of its variable operating costs

for fixed operating costs by eliminating sales commissions and increasing sales

salaries. This exchange results in a reduction in the variable operating cost per

unit from $5 to $4.50 and an increase in the fixed operating costs from $2,500 to

$3,000. Table 13.5 presents an analysis like that in Table 13.4, but using the new

costs. Although the EBIT of $2,500 at the 1,000-unit sales level is the same as

before the shift in operating cost structure, Table 13.5 shows that the firm has

increased its operating leverage by shifting to greater fixed operating costs.

With the substitution of the appropriate values into Equation 13.5, the

degree of operating leverage at the 1,000-unit base level of sales becomes

Comparing this value to the DOL of 2.0 before the shift to more fixed costs

makes it clear that the higher the firm’s fixed operating costs relative to variable

operating costs, the greater the degree of operating leverage.

FINANCIAL LEVERAGE

Financial leverage results from the presence of fixed financial costs that the firm

must pay. Using the framework in Table 13.1, we can define financial leverage as

DOL at 1,000 units =1,000 *($10 –$4.50)

1,000 *($10 –$4.50) –$3,000 =$5,500

$2,500 =2.2

Example 13.7 3

financial leverage

The use of

fixed financial costs

to magnify the effects of

changes in earnings before

interest and taxes on the firm’s

earnings per share.

Operating Leverage and Increased Fixed Costs

Case 2 Case 1

⫺50% ⫹50%

Sales (in units) 500 1,000 1,500

Sales revenuea$5,000 $10,000 $15,000

Less: Variable operating costsb2,250 4,500 6,750

Less: Fixed operating costs

Earnings before interest and taxes (EBIT) ⫺$ 250 $ 2,500 $ 5,250

⫺110% ⫹110%

aSales revenue was calculated as indicated in Table 13.4.

bVariable operating costs $4.50/unit sales in units.*=

3,0003,0003,000

the use of fixed financial costs to magnify the effects of changes in earnings before

interest and taxes on the firm’s earnings per share. The two most common fixed

financial costs are (1) interest on debt and (2) preferred stock dividends. These

charges must be paid regardless of the amount of EBIT available to pay them.7

Chen Foods, a small Asian food company, expects EBIT of $10,000 in the current

year. It has a $20,000 bond with a 10% (annual) coupon rate of interest and an

issue of 600 shares of $4 (annual dividend per share) preferred stock outstanding.

It also has 1,000 shares of common stock outstanding. The annual interest on the

bond issue is $2,000 (0.10 $20,000). The annual dividends on the preferred

stock are $2,400 ($4.00/share 600 shares). Table 13.6 presents the earnings

per share (EPS) corresponding to levels of EBIT of $6,000, $10,000, and

$14,000, assuming that the firm is in the 40% tax bracket. The table illustrates

two situations:

Case 1 A 40% increase in EBIT (from $10,000 to $14,000) results in a 100%

increase in earnings per share (from $2.40 to $4.80).

Case 2 A 40% decrease in EBIT (from $10,000 to $6,000) results in a 100%

decrease in earnings per share (from $2.40 to $0).

*

*

Example 13.8 3

CHAPTER 13 Leverage and Capital Structure 517

TABLE 13.6 The EPS for Various EBIT Levels

a