Questions for Wal-Mart case study.

1. Assess the financial health of Wal-Mart based on the analysis of the companys financial

statements.

2. Based on any additional available information (including annual reports and 10-K

filings) assess the economic conditions (as of the time of the case), the industry key

success factors and key competitive situation, and Wal-Marts strengths and weaknesses.

3. Develop a pro-forma income statement for Wal-Mart for the fiscal year ending January

31, 2006. Assume the following (in addition to the information in the case): selling,

general and administrative expenses at 17.3% of anticipated net sales; interest on debt at an

average of 4%; similar number of shares outstanding as of January 31, 2005. State any

other key assumptions. How profitable do you think Wal-Mart will be? Will Wal-Mart

need to increase its reliance on external borrowing?

4. Determine the intrinsic value of Wal-Mart tion a per share basis) using the dividend

discount model (DDM). Assess the value based on three forms of the DDM: the constant

growth version, an assessment based on three years of projected dividends and a projected

future stock price, and the three-stage DDM. Clearly state any assumptions including an

estimation of Wal-Mart investor required returns.

5. Determine the intrinsic value of Wal-Mart tion a per share basis) using Price – Earnings

(P/E) approach. As part of your analysis, you will need to determine an appropriate

forward-looking P/E multiple. Clearly state any assumption.

6. Based on your analysis, as Richard Martin, what recommendation would you make?

Justify your recommendation and reconcile any differences in your valuation assessments

(based on different methods).

Introduction

Wal-Mart is more than just another large company. Every week, over 130 million

customers visit Wal-Mart stores worldwide, making it the worlds largest retailers. It is the

largest corporation in the world, with total revenues of $285 billion for fiscal year ending

January 31, 2005. A leader in the discount industry, it has continued to specialize in selling

discounted household goods. The company has approximately 1.3 million employees

working at 3,100 locations in the United States and 1,000 locations in Mexico, Puerto

Rico, Canada, Argentina, Brazil, China, Korea, Germany, and the United Kingdom.

Currently the company is broken down into four divisions: Wal-Mart Supercenters,

Discount Stores, Neighborhood Markets, and SAMS Club Warehouses. Wal-Marts motto,

Everyday Low Prices, is present is each of the divisions. The magnitude and global

presence of Wal-Mart allows it to be a dominant player in the retailing market place.

During the past decade, as Wal-Mart sharply expanded its number of stores in the United

States, it increasingly encountered resistance from local communities. Opponents of

Wal-Mart have tried to block its entry on many grounds, including the prevention of urban

sprawl, preservation of historical culture, and protection of the environment. Mega

retailers, such as Wal-Mart, are expanding their product variety by focusing on groceries

and pharmaceutical drugs. To combat the market intrusion, Walgreen, CVS, and other drug

stores are adding groceries to their shelves. The mass merchandising industry is only

getting larger as the major players are offering more selection to gain a competitive edge.

Many companies like Wal-Mart are expanding by acquisitions. Competition within the

industry itself does not present a formidable threat to Wal-Mart Inc. because of its size and

profitability. Some of its direct competitors are Target, Kroger, and Costco. In summary,

Wal-Mart is ahead of the competition and the leader in the industry with a secure market

position. It is essential that fundamental relationships within the industry and the

companys environment be analyzed by Rachel Martin early in 2006 in order to efficiently

evaluate Wal-Mart, its stock and, the correct valuation of the companys stock.

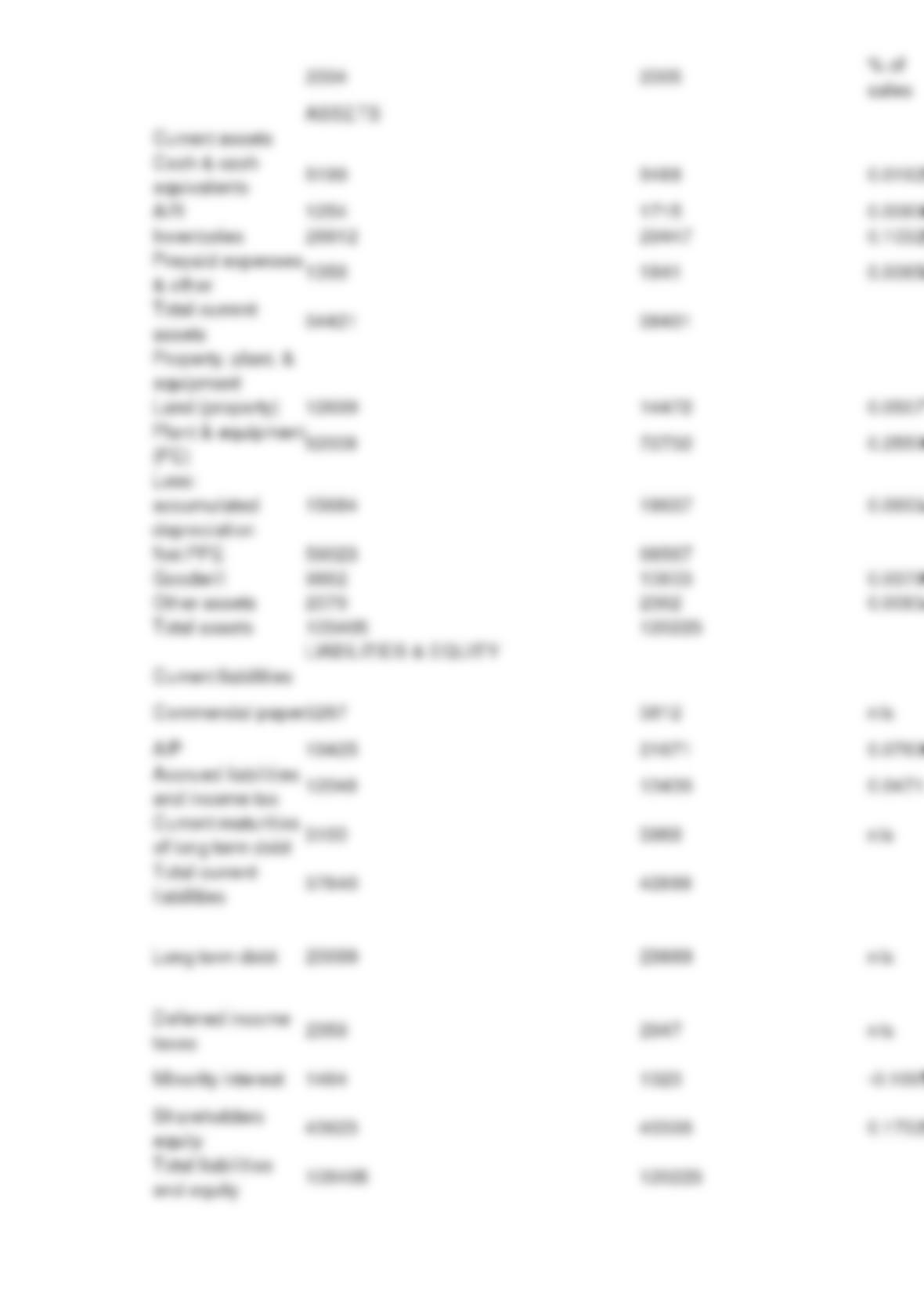

1. Analysis of the Financial Health of Wal-Mart for Calendar Years 2003 (FYE1/31/2004)

and 2004 (FYE 1/31/2005)

Ratios are very helpful in determining the financial health of a company. They can provide

indicators if a company is in financial trouble or moving in a positive direction and

experiencing growth.

The two years average current ratio for Wal-Mart is 0.91. Wal-Marts current ratio is less

than one, which means that by selling out its current assets in an emergency, it still would

not be able to cover its liabilities. Wal-Marts current ratio is low because of its heavy

reliance on short-term debts and commercial papers to finance its operations. This ratio

would have a heavy bearing on the investor motivation to invest in Wal-Mart. The fear of

not being able to cover its liabilities in the event of an unforeseen circumstance may deter

investors from purchasing the stock.

The higher the ratio is, the better the company financing. The two years average quick

ratio for Wal-Mart is 0.26 .Wal-Marts lower quick ratio is caused by Wal-Marts high

investment in inventory. Its quick ratio is low because of its dependence on current

liabilities. However, Wal-Marts high inventory is needed because if they do not have the

item in stock the customer will go to the competition. It is well known that keeping a

customer is cheaper than getting new ones, thus Wal-Mart does not want to lose any of its

customers.

The higher the Debt to Equity ratio is, the riskier the firm. Wal-Mart borrowed more

money proportionally to equity during the last two years. Any debt, which companies issue

or take, becomes a liability to the company and these risks are directly transferred to the

shareholders. Therefore, it is inherent that the more debt financing, the more risk is

present.

It is critical, however, to understand the type of firm being analyzed, the industry, and the