Tutorial 9 Year End Adjustments

5

Tutorial 9: Suggested solutions

Section A:

1. Accrued income is income/revenue earned/realised during the year, but

not yet received. Eg:- Commision for the year ended 31 Dec 2013 but

only received in Feb 2014. This should be included as year 2013

income and appear as a current asset in the SFP as at 31 Dec 2013.

Income in advance is income/revenue for following year that was not

yet earned/ realised during the year, but received in the current year.

Eg:- Rental income for Jan 2014 received in Dec 2013. This should be

excluded from year 2013 income and disclosed as a current liability in

th SFP as at 31 Dec 2013.

Accrued expenses are expenses incurred during the year but not yet

paid. Eg:- electicity bill for Dec 2013 that was only received and paid

in Jan 2014. This sgould be included as Dec 2013 expenses and

disclosed as a current liability in the SFP as at 31 Dec 2013.

Prepaid expenses are expenses for the following year paid in advance in

the current year. Eg :- Rental expense for Jan 2014 paid in Dec 2013.

This should be excluded from the 2013 expenses and disclosed as a

current asset in the SFP as at 31 Dec 2013.

2 (a) According to the Matching/Accruals Concept, the cost/expenses

incurred in an accounting period are matched with the revenue earned

in the same accounting period, regardless of the payment made or

revenue received. It should be stressed that only revenue and

cost/expenses that relate to that particular period should be matched. If

not, they should be excluded.

(b) Accrued income is income realised in this period but not yet

collected. It is an asset that is collectible within 12 months. Therefore,

it should be categorised under current asset in the SFP.

Income in advance is income for the following period but received in

this period. It is not yet realised. Therefore, it should be categorised as

current liability in the SFP.

3. RM1,800 covered Oct 2014 until Mar 2016 = 18 months

ie. RM100 per month

SPL = 12 months x RM100 = RM1,200

SFP = 3 months x RM100 = RM300 prepaid

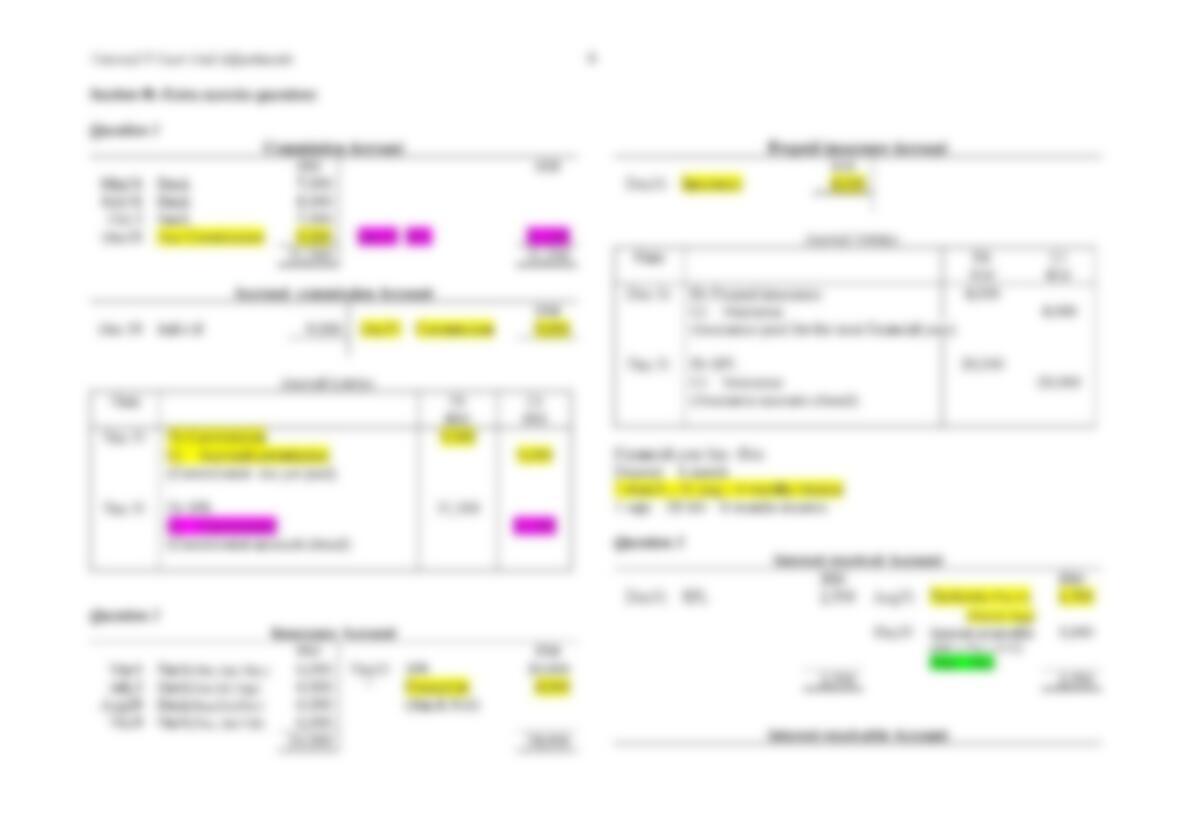

4. (The two-stage method is used for this illustration).

Prepaid advertising Account

2

01

7

RM

20

1

7

RM

Jun

1

Bal b/d

1,280

Jun

1

Advertising

1,280

Advertising Account

20

1

7

RM

201

8

RM

Jun

1

Prepaid Advertising

1,280

201

8

May

30

Cash

/Bank

600

May

30

Accrued

Advertising

200

May

30

S

PL

2,080

(4xRM50)

2,080

2,080

Accrued advertising Account

201

8

RM

201

8

RM

May

30

Bal c/d

200

May

30

Advertising

200

Jun

1

Bal b/d

200

Tutorial 9 Year End Adjustments

6

Accrued rental received Account

20

1

7

20

1

7

Jun

1

Bal b/d

2,000

Jun

1

Rental received

2,000

201

8

201

8

May

30

Rental received

4,000

May

30

Bal

c/d

4,000

Jun

1

Bal b/d

4,000

Rent received Account

20

1

7

RM

201

8

RM

Jun

1

Acc rental received

2,000

May

30

Cash

10,000

201

8

May

30

Acc rental received

4,000

May

30

S

PL

12,000

(RM1,000 x 4)

14,000

14,000

Question 5

(a) i)

Rent Account

RM

RM

Mar

31

Bank

4,400

Mar

31

SPL

4,800

Balance c/d

400

4,800

4,800

ii)

Insurance Account

RM

RM

Mar

31

Bank

1,600

Mar

31

SPL

1,300

Bal c/d

300

1,600

1,600

20

1

7

RM

20

1

7

RM

Jun

1

Electricity

120

Jun

1

Bal b/d

120

201

8

20

1

7

May

30

201

8

May

30

S

PL

730

May

30

Prepaid electricity

150

1,000

1,000

201

8

201

8

May

30

May

30

Jun

1

Bal b/d

150

Bal c/d

350

1,600

4,000

RM

RM

S

4,800

(15 mth)

6,000