Tutorial 3 Purchases & Sales Cycles

3

Tutorial 3: Suggested solutions

Section A:

1. (a) Purchases Journal is also known as Purchases Day Book. It is a

listing of all the credit purchases during the period, based on dates of

purchases. The details listed are the suppliers names, suppliers’ invoice

numbers and amounts of the invoices. The total amount of purchases

will be posted to the purchases account at the end of the month.

(b) Sales Journal is also known as Sales Day Book. It is a listing of all

the credit sales during the period, based on dates of sales. The details

listed are the customers’ names, seller’s invoice numbers and amounts.

The total amount of sales will be posted to the sales account at the end

of the month.

2. (a)Sales returns are also known as returns inwards. These are returns of

goods by credit customers mainly due to defects, spoilage, legal rights

or etc. They are recorded in the returns inwards journal and the cource

document is the credit notes of the seller.

Purchases returns are also known as returns outwards. These are returns

to the trade suppliers due to defects, spoilage, wrong goods etc. They

are recorded in the returns outwards journal based on the credit notes of

the suppliers.

(b) Credit notes are issued by seller to buyer (receivables) to reduce the

amount owed by the buyer. This happens when the buyers return goods

to seller either due to defects, spoilage, wrong goods etc. Credit notes

are also used to reduce the debt when the seller has overcharged the

buyer in the first place.

Debit notes are issued by seller to buyer to increase the amount owed

by the buyer. This normally happens when the seller has undercharged

the buyer in the first place or where there is additional charges that has

been missed out. Normally a debit note is issued rather than a new

invoice.

3. Sales ledger basically is the “book” that consists of all the trade

receivables accounts. Trade receivables exist because of credit sales. It

should be noted that sales ledger does not include sales account, which is

included in the general ledger. This sales ledger is separately kept mainly

to monitor collections from the various trade receivables and usually is

the job of the credit control department. The total of all these trade

receivables are represented by a Trade Receivables Contol amount in the

general ledger for the purpose of accounts closing at the end of the

month.

Purchases ledger consists of all the trade payables accounts which arise

due to credit purchases. Similarly, it does not include the purchases

account , which is included in the general ledger. Purchases ledger are

kept separately mainly for payment purposes. The total of the trade

payables are represented by a Trade Payables Control amount in the

general ledger for accounts closing purpose.

Since they are not part of the general ledger, they are called the

secondary ledger. They are not part of the double entry system because

they are not used in the month end closing of accounts.

Tutorial 3 Purchases & Sales Cycles

4

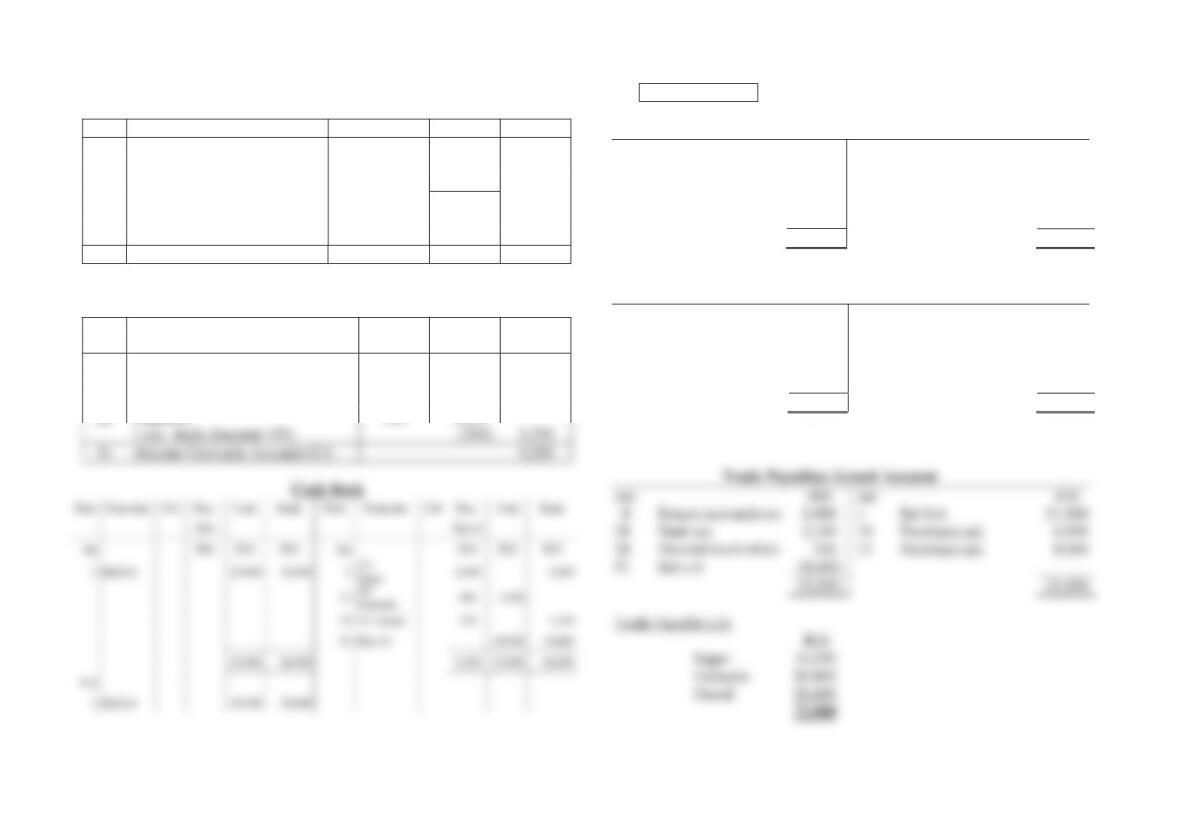

Question 4

(a) Purchases Journal

Date

Particular

s

Invoice No.

RM

RM

Jan

3

Fantastic

23

5,000

Less: trade discount

1

0%

(500

)

4,500

10

Super

542

7,000

Grand

421

6,000

15

Grand

455

8,000

31

Purchases Account (D

r)

25,500

Returns Outwards Journal

Date

Particular

s

Credit

RM

RM

Note

Jan

5

Super

876

500

8

Grand

098

1,000

(b) Purchases Ledger

Trade Payables: Super Account

Jan

RM

Jan

RM

5

Return outwards

500

1

Bal b/d

18,000

5

Bank

9,000

10

Purchases

7,000

5

Discount received

1,000

31

Bal c/d

14,500

25,000

25,000

Trade Payables: Fantastic Account

Jan

RM

Jan

RM

22

Return outwards

2,700

1

Bal b/d

30,000

12

Cash

4,500

3

Purchases

4,500

12

Discount received

500

31

Bal c/d

26,800

34,500

34,500

Jan

RM

Jan

RM

8

Return outwards a/c

1,000

1

Bal b/d

21,000

28

Bank a/c

2,160

10

Purchases a/c

6,000

28

240

15

Purchases a/c

8,000

31

Bal c/d

31,600