Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

The Pharmaceutical industry in the Global Economy

Introduction

This paper summarizes the results of our global pharmaceutical industry analysis and is

intended to increase awareness of the general public *€“ investors, policy makers,

managers, employees of the companies *€“ about its current developments. The paper has

the following major goals:

1) To analyze the current situation, major challenges and the prospects of the

pharmaceutical industry;

2) To identify major players of the global pharmaceutical industry and make a comparative

analysis of their business practices and financial results;

3) To determine the relative position of the U.S. pharmaceutical companies in the global

pharmaceutical industry, as well as to reveal opportunities for further strengthening of their

positions.

The paper consists of three major parts. In the first part we present an overview of the

pharmaceutical industry as a whole *€“ its major players, current trends and challenges.

The second part focuses on a more detailed analysis of major pharmaceutical companies.

These major companies are divided into two major groups: a) companies with

headquarters in the U.S., b) foreign pharmaceutical companies with headquarters outside

of the U.S. Pharmaceutical companies are compared with other companies in the same

group; and major trends within each group are analyzed. Part 3 sums up our findings.

Part 1. Pharmaceutical industry overview.

Major players of the world pharmaceutical industry

The pharmaceutical industry is characterized by a high level of concentration with fifteen

multinational companies dominating the industry. Table 1.1 contains information about

these major pharmaceutical companies that are sorted in the order of their 2004 revenues

from the sales of pharmaceutical products. Numbers provided in this table include sales of

all subsidiaries and affiliated companies that are consolidated in annual reports of the

corresponding companies. In order to facilitate a comparison of different companies

revenues of all of them are shown in US dollars; financial data of the companies with

headquarters outside of the U.S. was converted to US dollars using average 2004 rates

provided in Table 1.2.

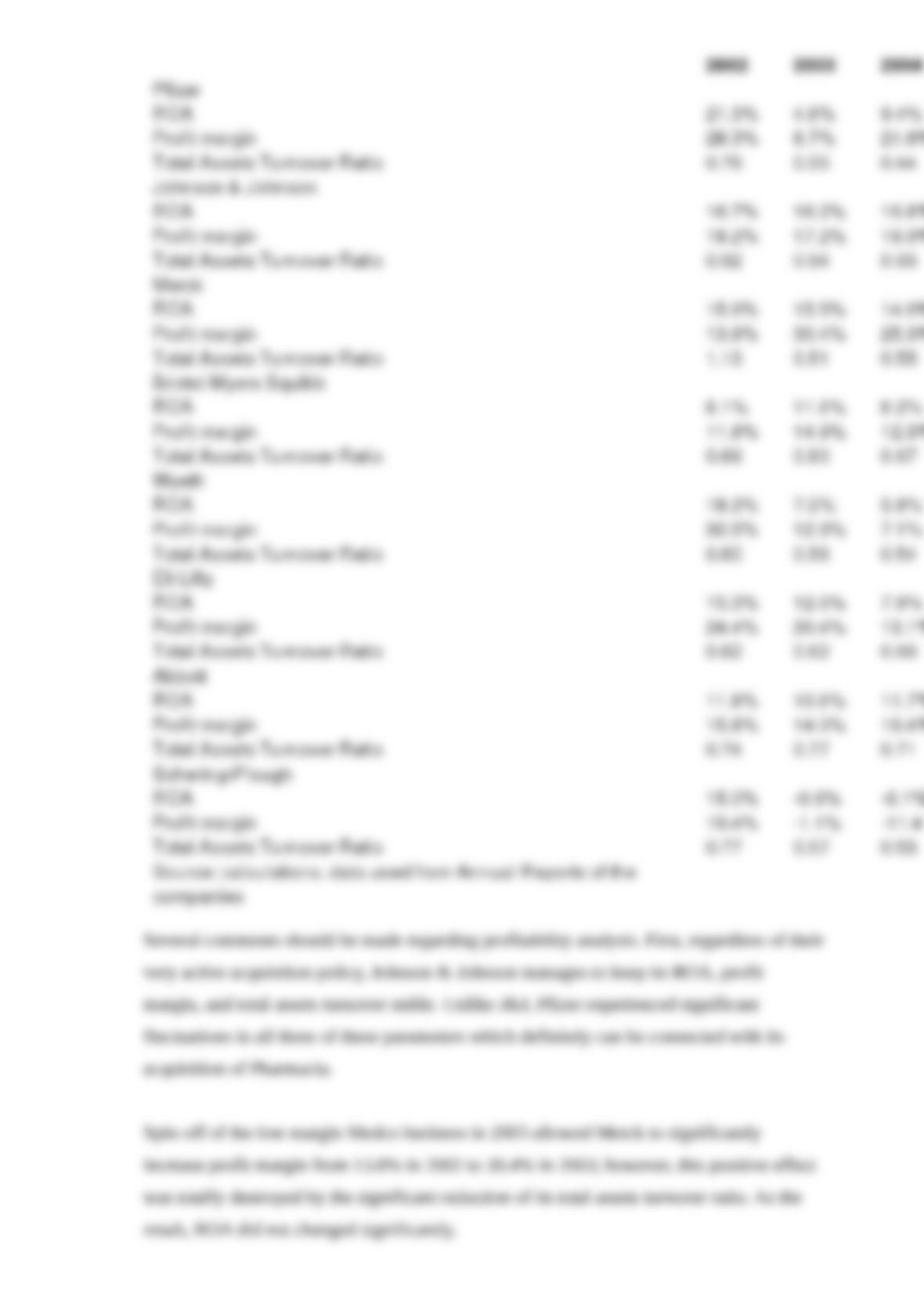

Table 1.1. Major pharmaceutical companies.

As Table 1.1 shows, the majority of the largest pharmaceutical companies are not

diversified. They are either concentrated exclusively on pharmaceutical products (Eli Lilly

and AstraZeneca are good examples with virtually 100% of their revenues coming from

sales of pharmaceutical products) or, although they develop and manufacture other health

care products, they still have pharmaceutical divisions as the core of their business that

provide more than 50% of their revenues. Other products manufactured by these

companies usually include medical devices, nutritional products, consumer healthcare

products and products for animal health.

Only two out of these 15 major pharmaceutical companies have revenues from sales of

pharmaceutical products that are lower than 50% of their total sales. These companies are

world giants Johnson & Johnson (which besides pharmaceutical products manufactures

consumer goods and medical devices) and Bayer which has only about 15% of its revenues

from the sales of pharmaceutical products.

Eli Lillys $13.1 billion sales figure made it the twelfth largest company *€“ with

Pharmaceutical sales considerably larger than Bayers $5.5 billion but a lot less than Pfizers

$46.1 billion.

Geographical headquarters of major pharmaceutical companies are approximately evenly

distributed between the U.S. and Western Europe with only one Asian company in the list.

Indiana is home to one of these companies, Eli Lilly. More detailed analysis of these

companies will be made in the second part of this paper.

Table 1.2. Average 2004 exchange rates.

Industry Trends

Here we examine structural changes causing significant transformations, major factors

leading to strong future sales growth, and point out the industrys strong reliance on

research and development.

Structural changes

The pharmaceutical industry is currently undergoing a period of very significant

transformation. The majority of Big Pharma companies generate high returns, thus

providing them with excess cash for further rapid growth *€“ whether organic, or through

mergers and acquisitions. Although size of the company on its own does not guarantee

success, it gives a significant advantage, especially in pharmaceutical industry. Besides

economies of scale in manufacturing, clinical trials and marketing, bigger companies can

allow investments in more research and development (R&D) projects that diversify their

future drugs portfolio and make them much more stable in the long term. As the result,

top-companies in the industry were active participants of mergers and acquisitions (M&A),

new joint ventures and spin-offs of non-core businesses.

The largest acquisitions in the industry during last years were the acquisition of Pharmacia

by Pfizer (purchase price $58 billion), and acquisition of Guidant by Johnson & Johnson

(purchase price $25 billion). Both acquisitions allowed these twoth acquisitions allowed

these 2an Pfize eleventh largest company -- considerably g towast have a good time. snt do

much good t U.S.-based companies to solidify their places among the elite of the

pharmaceutical industry. European companies were even more aggressive in M&A activity

than their American competitors *€“ 3 out of 6 major European companies underwent

mergers during the last several years: GlaxoSmithKline (merger of Glaxo Wellcome and

SmithKline Beecham), AstraZeneca (merger of Astra and Zeneca) and Sanofi-Aventis

(merger of Sanofi-Synthelabo and Aventis).

Another form of structural change in the industry was establishing of new strategic

alliances and joint ventures. So far as the research and development process for each drug

take many years and requires significant investments, and the outcome of these

investments of time and financial resources remains unclear until the final approval of the

drug, Big Pharma companies are constantly looking for synergies that they can get from

cooperation with their competitors. Last years gave multiple examples of such initiatives.

For example, cooperation of Sanofi-Aventis and Bristol-Myers Squibb resulted in

production of Plavix, which is currently one of the top-selling products for each of these

companies.

Finally, Big Pharma companies in order to maintain strong sales growth and meet

profitability expectations of their shareholders were actively selling low-profitability or

non-core businesses. For example, in 2003 Merck sold its low-profitability Medco Health

Solutions that helped to increase its profitability margin. Massive sales of

non-pharmaceutical businesses by Takeda also were compatible with its strategy to

concentrate its financial resources on its core pharmaceutical business.

Major factors of future growth

The pharmaceutical industry showed high sales growth rates in the recent past, and a

number of factors suggest that this trend will continue in the future.

First, due to numerous advancements in science and technology, including those in the

health care industry, life expectancy in the developed countries has been steadily growing.

As the result, growing proportion of elderly people promises further growth of demand for

healthcare products.

Moreover, according to various studies, a significant portion of elderly population in the

United States and other countries does not receive proper treatment. For example, only

about one third of the U.S. population who requires medical therapy for high cholesterol is

actually receiving adequate treatment. As it is expected, the Medicare Prescription Drug

Improvement and Modernization Act starting from the beginning of 2006 will increase

access of senior citizens to the prescription drug coverage, thus increasing pharmaceutical

sales.

Although developing countries at the moment have a small portion of world

pharmaceutical sales, these countries also have a significant potential for the

pharmaceutical industry in the future. Fast growing economies in Asia, South America and

Central & Eastern Europe suggest an increasing solvency of population and make these

markets more and more attractive for Big Pharma companies. Further reforms of

legislation systems in the countries of these regions, especially regarding patent protection

issues, will inevitably result in growing pharmaceutical sales.

Strong emphasis on R&D

One of the distinctive characteristics of the Big Pharma companies is a very high level of

investments in research and development. On average, it takes about 10-15 years, and

millions of dollars to develop a new medicine. According to industry statistics, only about

one in ten thousand chemical compounds discovered by pharmaceutical industry

researchers proves to be both medically effective and safe enough to become an approved

medicine, and about half of all new medicines fail in the late stages of clinical trials. Not

surprisingly, according to Research and Development in Industry: 2001 report of the

National Science Foundation, in 2001 the pharmaceutical industry had one of the highest

R&D expenditures as percentage of net sales. More detailed information on this issue is

provided in the second part of this paper.

Key Challenges

The main challenges for drug companies come from four areas. First, they must deal with

competition from within and without. Second, they must manage within a world of price

controls that dictate a wide range of prices from place to place. Third, companies must be

constantly on guard for patent violations and seek legal protection in new and growing

global markets. Finally, they must manage their product pipelines so that patent expirations

do not leave them without protection for their investment.

Competition

The pharmaceutical industry currently represents a highly competitive environment. One

can distinguish three layers of competition for Big Pharma companies:

First, obviously, Big Pharma companies compete among themselves. Although not all

leading pharmaceutical companies cover all segments of pharmaceutical market, almost all

of them are active in R&D and production of drugs in the segments with the highest

potential *€“ such as treatment of infectious, cardiovascular, psychiatric or oncology

diseases.

Secondly, Big Pharma companies experience significant profit losses due to competition