W15317

STRIDES ARCOLAB LIMITED’S DIVIDEND PAY-OUT DECISION

Tulsi Jayakumar and Indu Niranjan wrote this case solely to provide material for class discussion. The authors do not intend to

illustrate either effective or ineffective handling of a managerial situation. The authors may have disguised certain names and

other identifying information to protect confidentiality.

This publication may not be transmitted, photocopied, digitized or otherwise reproduced in any form or by any means without the

permission of the copyright holder. Reproduction of this material is not covered under authorization by any reproduction rights

organization. To order copies or request permission to reproduce materials, contact Ivey Publishing, Ivey Business School,

Western University, London, Ontario, Canada, N6G 0N1; (t) 519.661.3208; (e) cases@ivey.ca; www.iveycases.com.

Copyright © 2015, Richard Ivey School of Business Foundation Version: 2015-07-22

On December 10, 2013, Arun Kumar, founder and group chief executive officer of Strides Arcolab

Limited (Strides) — a first generation, Indian pharmaceutical company headquartered in Bengaluru —

prepared for a crucial meeting of the Board of Directors to discuss the proposed dividend pay-out to the

company’s shareholders following the completion of a US$1.725 billion sale of its specialty division

— Agila Specialties to a U.S.-based pharmaceutical company, Mylan Inc.

1

Kumar proposed that Strides

distribute all the free cash available from the sale after settling their debts and making employee as well

as additional pay-outs, in the form of dividends to its shareholders.

Strides had already communicated its decision to settle debts and reduce its financial leverage.

2

In 2013,

the dividend rates among Strides’ top 10 peers in the Indian pharmaceutical sector were very high,

ranging from Cipla’s 100 per cent to Divis Labs’ 750 per cent.

3

Yet the proposed dividend pay-out,

based on a residual dividend pay-out policy, was a bold and unconventional move. It would be a drastic

change from Strides’ previous dividend pay-outs, which had not surpassed 21 per cent. In fact, if passed

by the Board, the dividend pay-out of $650–700 million — amounting to a 5,050 per cent dividend rate

and a dividend pay-out ratio (dividend/earnings) of close to 85 per cent — would be one of the largest

dividend pay-outs in the history of all Indian corporations.

What signal would the high dividends send and how would this affect Strides’ clientele? Would the market reward

a high dividend pay-out with high share prices? What would be the opportunity cost of low debts and a high

dividend pay-out? Would it jeopardize the financing of the company’s future growth plans? Would the board

support the dividend pay-out decision, or would it suggest other means of returning cash to the shareholders?

4

Kumar knew that convincing the Board to move forward with the dividend pay-out would be difficult.

Yet, he believed that this was a strong strategic move, and that the company would benefit significantly

through creating value for its shareholders.

BACKGROUND OF THE INDIAN PHARMACEUTICAL INDUSTRY

The Indian pharmaceutical industry

5

was the third largest global player in terms of volume and tenth largest

in terms of value in 2013.

6

The industry was estimated to be worth $34 billion (including exports) in 2013-

2014, with the domestic formulations market constituting about 1.1 per cent of the global pharmaceutical

market in terms of value. The exports of the Indian pharmaceutical industry grew at a compound annual

This document is authorized for use only in Prof. Samveg Patel’s Corporate Finance / PGDM at Management Development Institute – Gurgaon from Jan 2023 to Apr 2023.

Page 2 9B15N011

growth rate (CAGR) of 26.1 per cent during the period of 2005–2006 to 2013–2014 to reach $10.1 billion

in 2012–2013. From April 2013 to December 2013, the sector had accounted for $8 billion worth of exports.

In 2013, the Indian pharmaceutical market was highly fragmented, comprising about 24,000 players and

more than a million drugs across various therapeutic categories produced every year in India. Yet, with

about 330 players in the organized sector, and the top 10 formulation companies accounting for 42.2 per

cent of the formulation sales, the industry attracted several multinational pharmaceutical companies.

In 2013, a number of factors led to a decline in the Indian pharmaceutical industry growth rate to 9.8 per cent

from 16.6 per cent in 2012. However, the slowdown was more prominent in the case of the multinationals than

in Indian companies. Thus the top 10 multinational companies experienced a decline in the growth rate from

16 per cent to 8 per cent over 2012–2013 to 2013–2014. Indian companies, on the other hand, experienced a

deceleration in the growth rate, from 18 percent in 2012–2013 to 13 percent in 2013–2014.

Opportunities

Strong opportunities existed for cost-competitive Indian pharmaceutical companies, especially after 2011,

due to the presence of ‘patent cliffs’ in international pharmaceutical markets. Patent cliffs referred to the

situation faced by several top pharmaceutical companies, including Pfizer (for Lipitor), Novartis (for

Diovan), Merck (for Singulair), Bristol Myers Squibb and Sanofi-Aventis (for Plavix) arising from the

expiration of the patents they held for several of their important prescription drugs (so-called “blockbuster

drugs”). Such patent expirations led to the mass production of generic versions of these by small

pharmaceutical laboratories, which in turn led to revenue losses for major pharmaceutical companies.

For example, Ranbaxy — a generic drug manufacturer — was an Indian company that benefitted from

such a patent cliff and achieved an initial breakthrough in the United States market when Pfizer faced

a loss of exclusivity for its blockbuster drug Lipitor in 2011. Owing to patent expiration, Pfizer entered

into a licensing agreement with Ranbaxy that provided Ranbaxy with the exclusive rights to produce

atorvastatin (Lipitor) for 180 days.

The number of Indian companies that filed patent challenges in the United States against various global

generic pharmaceutical companies — called “Para IV filings”7 — had increased since 2011. Ranbaxy,

Sun Pharma, Dr. Reddy’s, Lupin, Alembic Pharma, Claris Lifescience and Torrent Pharmaceutical have

all submitted Para IV filings since 2011. Furthermore, Ranbaxy and Dr. Reddy’s earned 56 per cent and

20 per cent of their total revenues in 2011–2012 from Para IV filings.

In addition to the opportunities offered by expiring blockbuster drug patents and Para IV filings, Indian

generic drug producers were drawn into lucrative niche segments such as the injectable drug markets.

The overall size of the injectable drug market had increased from $200 billion during 2009 to $220

billion in 2011, with generic drug penetration being 15 per cent. The United States accounted for the

largest share of the overall injectable drug market.

Challenges

The National Pharmaceutical Pricing Policy (NPPP) adopted by the Indian Government in 2012 was

one of the main factors affecting the industry growth rate. All drug prices were brought under the

purview of this government policy. As such, price controls were imposed. This affected margins and

thus industry growth.The Indian government effectively enhanced the scope of the Drugs Price Control

Order through the NPPP to bring within the scope of the National List of Effective Medicines (and

hence price controls) almost all available drugs, including combination drugs. The implementation of

the NPPP had led to an erosion of retail and distributor margins from 20 and 10 per cent to 16 and 8 per

This document is authorized for use only in Prof. Samveg Patel’s Corporate Finance / PGDM at Management Development Institute – Gurgaon from Jan 2023 to Apr 2023.

Page 3 9B15N011

cent, respectively. Faced with decreases in margins and lower profits, many distributors were uncertain

about the feasibility of staying in business.

Industry growth was also constrained by several regulatory challenges that arose because of the unique

characteristics of the industry. Clinical trials are the gold standard in the pharmaceutical industry to ensure

the twin requirements of safety and effectiveness for new drugs before they are given regulatory approval.

However, unethical practices in past clinical trials had led the Indian government to impose strict

regulatory procedures for such trials. Consequently, delays in clinical trials had become the norm. While

foreign direct investment through the automatic route8 was possible in the Indian pharmaceutical sector,

in practice there were several uncertainties in the implementation of foreign direct investment policy as

there were also strict regulatory conditions for such investment. Additionally, the government — in an

attempt to make patented medicines available at reasonable prices — had imposed compulsory licensing9

which affected both Indian and foreign pharmaceutical companies.

The industry faced regulations not only in the domestic but also in the foreign markets, especially in the

United States. The Indian pharmaceutical industry’s key strengths lay in its cost-competitiveness and

advanced process chemistry skills which made it possible for Indian companies to produce generics without

licensing from the original patent-holders. As such, exports, especially to the United States and Europe (who

have high health expenditures) contributed to a large part of the industry’s revenues.10 However, for sustained

growth, the industry would need to comply with strict manufacturing and quality practices that fell in line

with United States Food and Drug Administration (FDA) norms which governed the most lucrative market.

There were other factors in the domestic macroeconomic environment that posed challenges to domestic

pharmaceutical industry players. The domestic inflation rate as measured by the consumer price index

(CPI) combined had remained high at 10.2 per cent in 2012–2013, followed by 9.5 per cent in 2013–

2014.11 The central bank — the Reserve Bank of India — had followed a tight monetary policy to contain

such inflation and had raised the operational policy rate — the repo rate — by 525 basis points during

March 2010 to October 2011.12 In May 2013, when fears of “tapering”13 by the United States caused high

capital outflows and a severe pressure on the exchange rates with the rupee depreciating, the Reserve

Bank of India resorted to exceptional measures to further tighten monetary policy and curtail liquidity

available in the system. Consequently, the lending rates remained high and industrial credit off-take

moderated. The Index of Industrial Production — an index measuring industrial growth across its

manufacturing, mining and electricity sectors — consequently declined from 8.2 percent growth rate in

2010–2011 to 1.1 percent in 2012–2013 (see Exhibit 1).

Further environmental challenges existed in the form of the increasing difficulty of acquiring lands for

projects, as well as obtaining environmental clearances. A recent report on the ease of doing business

in India stated that India was 132nd among 185 economies.14

The Indian pharmaceutical sector had seen their debts mount and revenues fall. The aggregate debt of

the domestic drug and pharmaceutical sector in India increased from $4.02 billion in 2010–2011 to $4.4

billion in 2013–2014, and a three-year CAGR of 13.4 per cent.15 Non-conducive equity markets made

funding more difficult. Moreover, with international credit rating agencies, Standard & Poor and Fitch,

downgrading India sovereign ratings to a negative in 2012, the External Commercial Borrowings route

was also difficult for many companies. In December 2012, for instance, Ranbaxy’s debt-equity ratio

was 2.48, which would increase more than twice by 2015.16

This document is authorized for use only in Prof. Samveg Patel’s Corporate Finance / PGDM at Management Development Institute – Gurgaon from Jan 2023 to Apr 2023.

Page 4 9B15N011

STRIDES ARCOLAB LIMITED

History

Arun Kumar17 founded Strides — a first generation pharmaceutical company — in 1990 in Vashi, New

Bombay.18 Kumar recalled his early days in the mid-1980s at the Bombay Drug House, one of the first

Indian companies to export finished products, as well as his stint as a “buying agent” for European

companies. He had believed in following certain guiding principles in his business — namely, focusing

on exports, forging partnerships and concentrating on building scale-to-sell.

Within two years of its establishment, Strides had started exporting pharmaceutical products to Nigeria.

In 1994, the company received venture capital funding from Schroder Capital Partners, which became

a large stakeholder in Strides with a nearly 37 per cent stake. Arcolab — a Swiss customer of Strides

— provided Strides with a capital funding of $2 million in 1992, which proved to be an important

milestone in the evolution of Strides. In exchange, Strides changed its name to Strides Arcolab Limited

in 1996.

The early history of Strides, like that of most first-generation companies, was one of attention to critical

size and scale. “There was very little emphasis on strategy in the early phases of growth. Size was

critical, since we needed bankers to lend and customers to buy.”19 Strides entered foreign markets

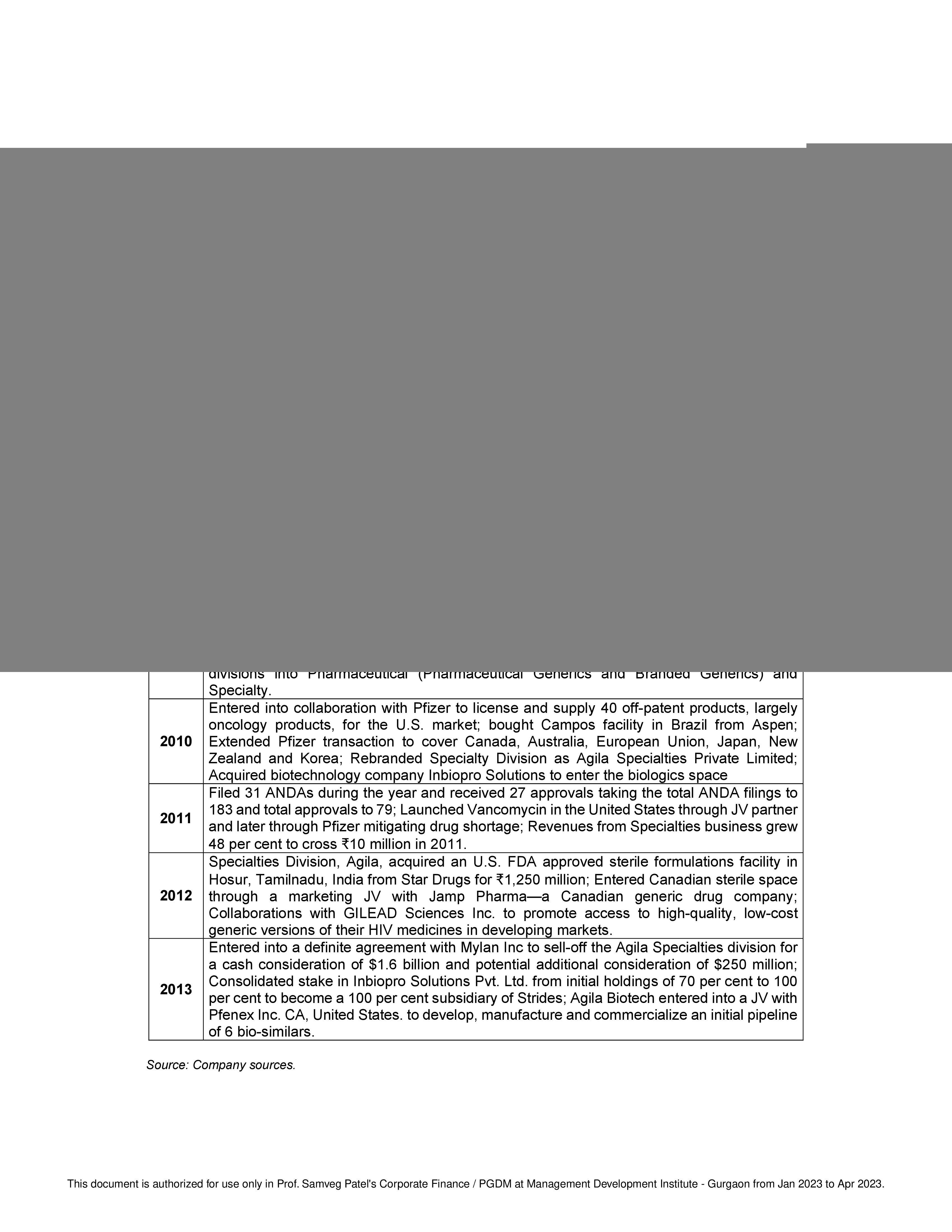

aggressively and also acquired both domestic and foreign companies during the period between 1990

and 2007 (see Exhibit 2). The company also became a listed company in this initial period, it was listed

with the National Stock Exchange in 2000 and with the Bombay Stock Exchange in 2002.

In the mid-2000s, Kumar started investing in research and development (R&D), in order to transform

Strides Arcolab Ltd. into a specialized pharmaceutical company. By 2008, he was convinced that in the

$900 billion pharmaceutical industry — into which Strides was a late entrant — the key to success lay

not in achieving critical size, but focusing on value. The $5 billion generic injectable drug segment was

a small but profitable niche within the global pharmaceutical industry. The high capital expenditure and

long gestation lags meant that this segment had very few players. The segment “represented a scarcity

domain,” said Kumar, one which he felt the need to tap into.

In 2010, with large, established U.S. players facing regulatory issues and a shortage of global players,

prices in the injectable drug market increased drastically, by as much as 150 times in certain cases.20

Kumar saw an opportunity in this, since Strides did not face compliance issues at this stage. He

established manufacturing facilities in nine locations across India, Brazil and Poland and invested in

R&D to create a portfolio of products.

Strides and the Injectable Drug Market

In 2009, the injectable drug market was worth $200 billion, and grew by 10 per cent to $220 billion in

2011. The market for generic injectable drugs was more lucrative than the branded injectable drug

market, and within this sector, the segments of biologics and oncological agents were relatively more

lucrative. At 38 per cent, the United States accounted for the largest chunk of the overall global

injectable drug market in 2011. It was estimated that the U.S. generic injectable sales would grow at a

CAGR of 10 per cent between 2012 and 2015.21

However, strict compliance norms meant that the number of global injectable manufacturing facilities

were limited. In 2010–2011 the United States witnessed a considerable shortage of injectable drugs.

The number of injectable drugs on the shortage list increased from 39 to 139 in 2011.22 Such shortages

were exacerbated by the long lead-time required to manufacture those injectable drugs, as well as a very

low rate of approval for generic alternatives that could have made up for the shortage.

This document is authorized for use only in Prof. Samveg Patel’s Corporate Finance / PGDM at Management Development Institute – Gurgaon from Jan 2023 to Apr 2023.

Page 5 9B15N011

A large part of the injectable drug market faced limited competition, with more than 86 per cent of the

products having less than five players. The injectable drug market was a niche market that was subject

to higher compliance standards. This contributed to the presence of fewer players and high value

products — both factors contributed to higher margins. Realizing this, Kumar decided to restructure the

company into a pharmaceutical division as well as a specialty division for Injectable drugs — Agila —

as a subsidiary of Strides Arcolab Ltd. With this move he had found both niche and scarcity value in

the injectable drug market. The injectable drug market had “scarcity” partly because making injectable

drugs was more difficult than making tablets. Furthermore, since the product was targeted more at

hospitals than individuals, there were fewer customers. Thus, upon the expiration of patents, prices for

generic versions of the products did not fall drastically.

In 2010, the specialty subsidiary was rebranded “Agila Specialties Limited.” Kumar raised $200 million

in the first four years after establishing Agila in the specialty space.23 He remembered that there was

foreign institutional investor (FII) interest in Strides due to its move into the injectable drug market,

and that such an FII investment had accounted for 53 per cent of the investment in 2010. In December

2012, FIIs, the Indian public, trusts and foreign nationals accounted for more than 50 per cent of the

total shareholding (see Exhibit 3). In 2012, Strides had three business divisions: pharmaceuticals,

specialties — Agila — and biotechnology, which when combined had a global turnover of $435 million,

14 manufacturing facilities across six countries and a country presence across over 75 emerging and

developed markets. External markets accounted for about 95 per cent of its revenues (see Exhibit 4).

STRIDES AND THE AGILA SALE

The Strides growth story, especially after 2008, was one of not only identifying the right niche area, but

also of creating value and — more importantly — exiting this niche at the right time and at the right