Studocu is not sponsored or endorsed by any college or university

PS3 S – Solutions to lecture 3 related questions

International Financial Strategy (Queen Mary University of London)

Studocu is not sponsored or endorsed by any college or university

PS3 S – Solutions to lecture 3 related questions

International Financial Strategy (Queen Mary University of London)

Downloaded by Namik Abramov (abramovnamik@gmail.com)

lOMoARcPSD|15008662

PROBLEM SET 3

1. Nataja Mumbai Ltd., the Indian subsidiary of a Belgian corporation, is a cardiothoracic

instruments manufacturer. Nataja manufactures the instruments primarily for the medical

industry globally—though with recent advances in cardiovascular surgery, its business has

begun to grow rapidly. Sales are primarily to hospitals based on Europe and Asia. Nataja

Mumbai’s balance sheet in thousands of Indian Rupees (INR) as of March 31 is as follows:

Balance Sheet (thousands)

Indian Rupee

Assets

Statement

Cash

INR 26,000

Accounts receivable

38,000

Inventory

46,000

Net plant & equipment

65,000

Total

INR 175,000

Liabilities & Net Worth

Accounts payable

INR 11,000

Bank loans

70,000

Common stock

20,000

Retained earnings

74,000

Total

INR 175,000

Exchange rates for translating Nataja Mumbai’s balance into euros (€) are:

INR79.19/€ April 1st exchange rate after 25% devaluation.

INR59.39/€ March 31st exchange rate, before 25% devaluation. All inventory was acquired at

this rate.

INR50.00 /€ Historical exchange rate at which plant and equipment were acquired and the

common stock was issued.

a. Using the data presented, assume that the Indian rupee dropped in value from INR59.39/€

to INR79.19/€ between March 31st and April 1st. Assuming no change in the balance sheet

between these two days, calculate the gain or loss from translation by both the current rate

method and the temporal method. Explain the translation gain or loss in terms of change in

the value of the exposed accounts.

b. Can you show how a company can minimise translation exposure under the current rate

method using a balance sheet hedge? Explain the strategy.

c. Using the original data provided for Nataja Mumbai, assume that the Indian rupee

appreciated in value from INR59.39/€ to INR54.50/€ between March 31 and April 1.

Assuming no change in balance sheet accounts between those two days, calculate the gain or

loss from translation by both the current rate method and the temporal method. Explain the

translation gain or loss in terms of changes in the value of the exposed accounts.

Model Answer:

Downloaded by Namik Abramov (abramovnamik@gmail.com)

lOMoARcPSD|15008662

a.

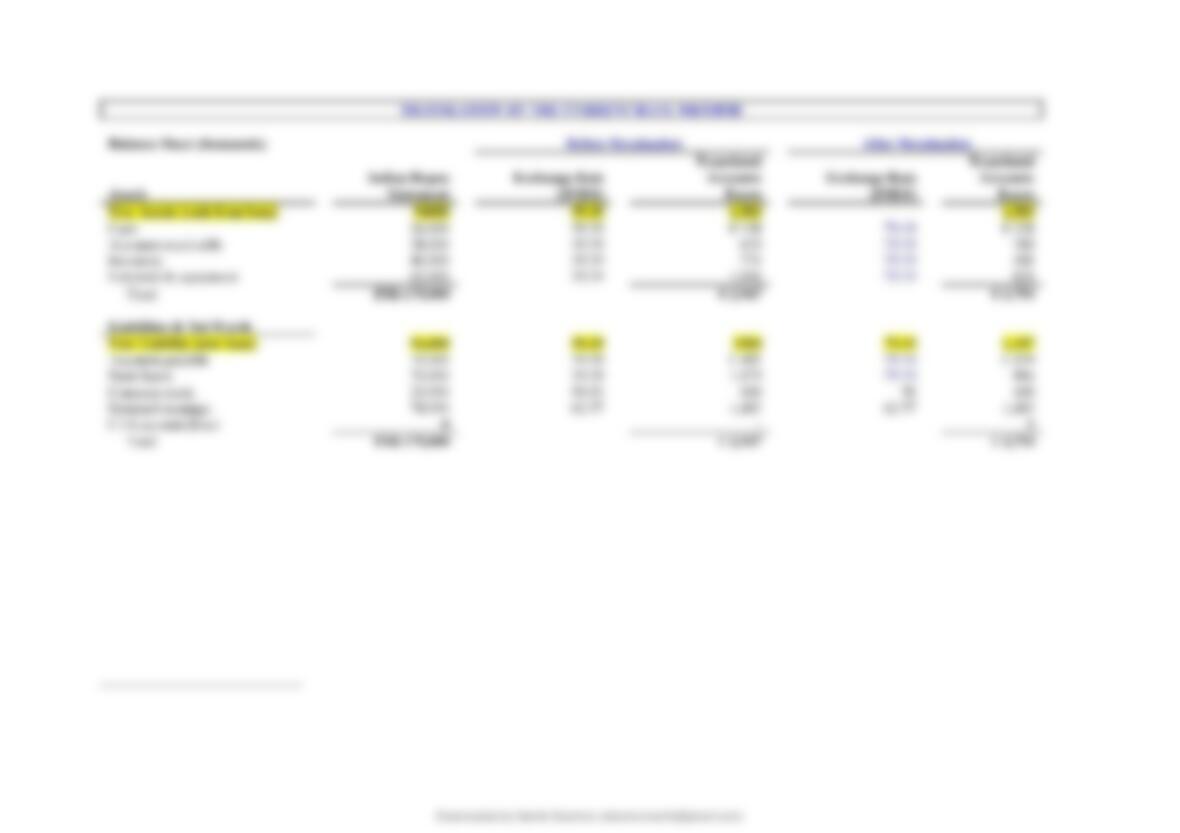

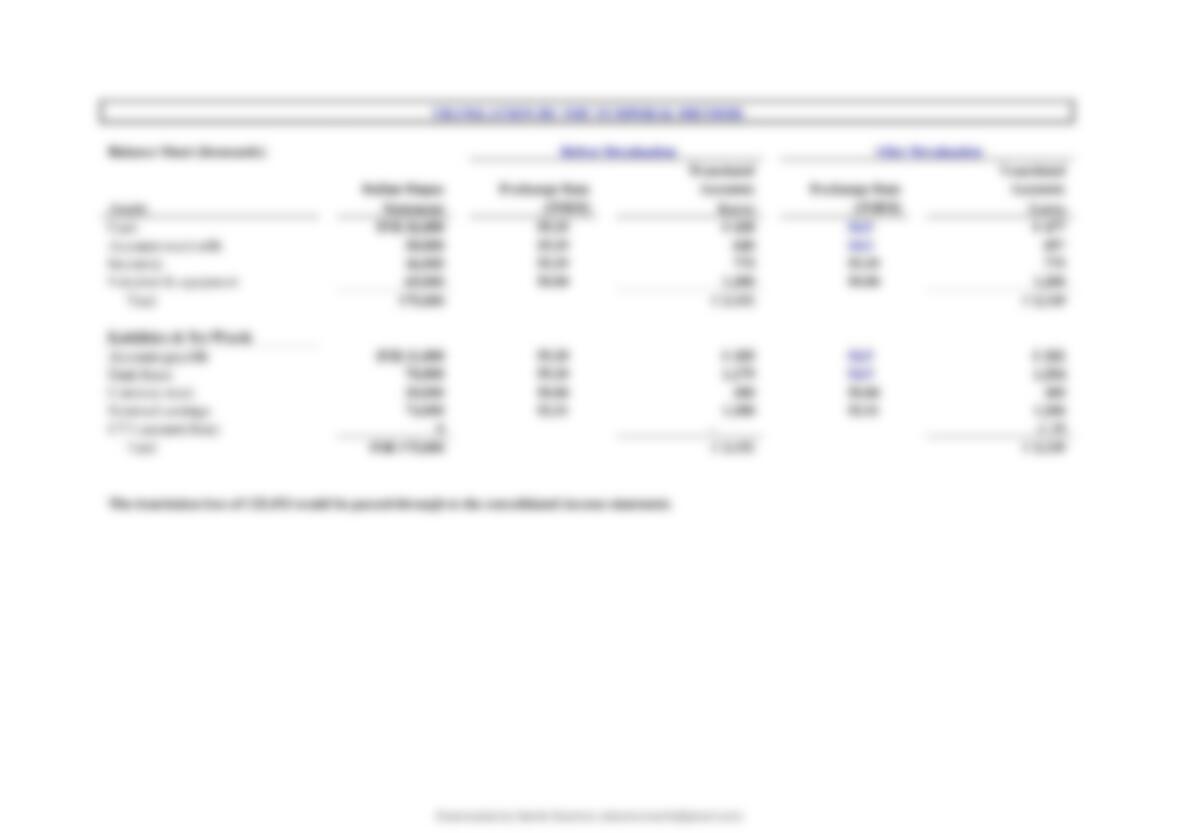

TRANSLATION BY THE CURRENT RATE METHOD

Balance Sheet (thousands)

Before Devaluation

After Devaluation

Translated

Translated

Indian Rupee

Exchange Rate

Accounts

Exchange Rate

Accounts

Assets

Statement

(INR/€)

Euros

(INR/€)

Euros

Cash

INR 26,000

59.39

€ 438

79.19

€ 328

Accounts receivable

38,000

59.39

640

79.19

480

Inventory

46,000

59.39

775

79.19

581

Net plant & equipment

65,000

59.39

1,094

79.19

821

Total

INR 175,000

€ 2,947

€ 2,210

Liabilities & Net Worth

Accounts payable

INR 11,000

59.39

€ 185

79.19

€ 139

lOMoARcPSD|15008662

Bank loans

70,000

59.39

1,179

79.19

884

Common stock

20,000

400

50.00

400

Retained earnings

74,000

1,183

1,183

CTA account (loss)

–

Total

INR 175,000

€ 2,947

€ 2,210