7–1

CHAPTER 7

FLEXIBLE BUDGETS, DIRECT–COST VARIANCES,

AND MANAGEMENT CONTROL

7–1 Management by exception is the practice of concentrating on areas not operating as

expected and giving less attention to areas operating as expected. Variance analysis helps

managers identify areas not operating as expected. The larger the variance, the more likely an

area is not operating as expected.

7–2 Two sources of information about budgeted amounts are (a) past amounts and (b)

detailed engineering studies.

7–3 A favorable variance––denoted F––is a variance that has the effect of increasing

operating income relative to the budgeted amount. An unfavorable variance––denoted U––is a

variance that has the effect of decreasing operating income relative to the budgeted amount.

7–4 The key difference is the output level used to set the budget. A static budget is based on

the level of output planned at the start of the budget period. A flexible budget is developed using

budgeted revenues or cost amounts based on the actual output level in the budget period. The

actual level of output is not known until the end of the budget period.

7–5 A flexible–budget analysis enables a manager to distinguish how much of the difference

between an actual result and a budgeted amount is due to (a) the difference between actual and

budgeted output levels, and (b) the difference between actual and budgeted selling prices,

variable costs, and fixed costs.

7–6 The steps in developing a flexible budget are:

Step 1: Identify the actual quantity of output.

Step 2: Calculate the flexible budget for revenues based on budgeted selling price and

actual quantity of output.

Step 3: Calculate the flexible budget for costs based on budgeted variable cost per output

unit, actual quantity of output, and budgeted fixed costs.

7–7 Four reasons for using standard costs are:

(i) cost management,

(ii) pricing decisions,

(iii) budgetary planning and control, and

(iv) financial statement preparation.

7–8 A manager should subdivide the flexible–budget variance for direct materials into a price

variance (that reflects the difference between actual and budgeted prices of direct materials) and

an efficiency variance (that reflects the difference between the actual and budgeted quantities of

direct materials used to produce actual output). The individual causes of these variances can then

be investigated, recognizing possible interdependencies across these individual causes.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–2

7–9 Possible causes of a favorable direct materials price variance are:

purchasing officer negotiated more skillfully than was planned in the budget,

purchasing manager bought in larger lot sizes than budgeted, thus obtaining quantity

discounts,

materials prices decreased unexpectedly due to, say, industry oversupply,

budgeted purchase prices were set without careful analysis of the market, and

purchasing manager received unfavorable terms on nonpurchase price factors (such as

lower quality materials).

7–10 Some possible reasons for an unfavorable direct manufacturing labor efficiency variance

are the hiring and use of underskilled workers; inefficient scheduling of work so that the

workforce was not optimally occupied; poor maintenance of machines resulting in a high

proportion of non–value–added labor; unrealistic time standards. Each of these factors would

result in actual direct manufacturing labor–hours being higher than indicated by the standard

work rate.

7–11 Variance analysis, by providing information about actual performance relative to

standards, can form the basis of continuous operational improvement. The underlying causes of

unfavorable variances are identified and corrective action taken where possible. Favorable

variances can also provide information if the organization can identify why a favorable variance

occurred. Steps can often be taken to replicate those conditions more often. As the easier changes

are made, and perhaps some standards tightened, the harder issues will be revealed for the

organization to act on—this is continuous improvement.

7–12 An individual business function, such as production, is interdependent with other

business functions. Factors outside of production can explain why variances arise in the

production area. For example:

poor design of products or processes can lead to a sizable number of defects,

marketing personnel making promises for delivery times that require a large number

of rush orders can create production–scheduling difficulties, and

purchase of poor–quality materials by the purchasing manager can result in defects

and waste.

7–13 The plant supervisor likely has good grounds for complaint if the plant accountant puts

excessive emphasis on using variances to pin blame. The key value of variances is to help

understand why actual results differ from budgeted amounts and then to use that knowledge to

promote learning and continuous improvement.

7–14 The sales–volume variance can be decomposed into two parts: a market–share variance

that reflects the difference in budgeted contribution margin due to the actual market share being

different from the budgeted share; and a market–size variance, which captures the impact of

actual size of the market as a while differing from the budgeted market size.

7–15 Evidence on the costs of other companies is one input managers can use in setting the

performance measure for next year. However, caution should be taken before choosing such an

amount as next year‘s performance measure. It is important to understand why cost differences

across companies exist and whether these differences can be eliminated. It is also important to

examine when planned changes (in, say, technology) next year make even the current low–cost

producer not a demanding enough hurdle.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–3

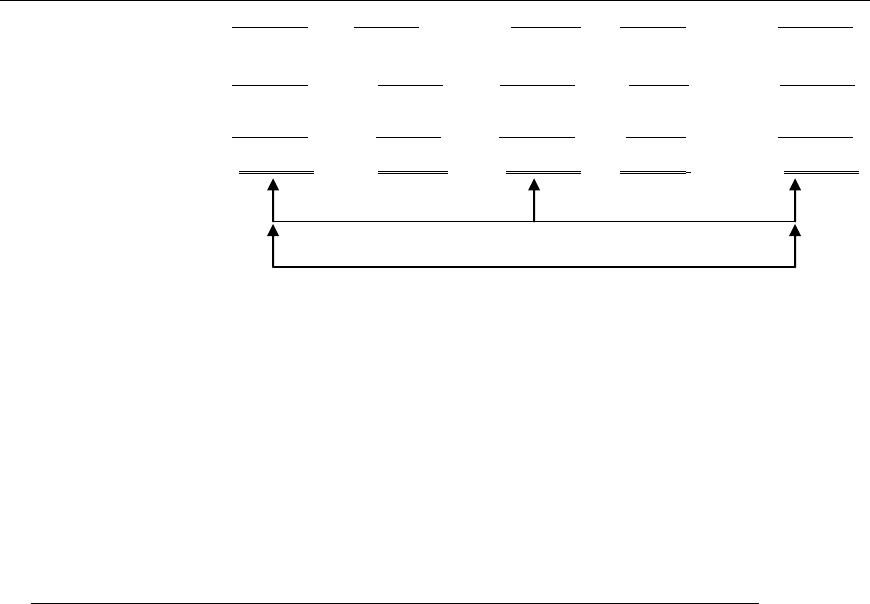

7–16 (20–30 min.) Flexible budget.

Variance Analysis for Brabham Enterprises for August 2012

Actual

Results

(1)

Flexible-

Budget

Variances

(2) = (1) – (3)

Flexible

Budget

(3)

Sales-Volume

Variances

(4) = (3) – (5)

Static

Budget

(5)

Units (tires) sold

2,800g

0

2,800

200 U

3,000g

Revenues

$313,600a

$ 5,600 F

$308,000b

$22,000 U

$330,000c

Variable costs

229,600d

22,400 U

207,200e

14,800 F

222,000f

Contribution margin

84,000

16,800 U

100,800

7,200 U

108,000

Fixed costs

50,000g

4,000 F

54,000g

0

54,000g

Operating income

$ 34,000

$12,800 U

$ 46,800

$ 7,200 U

$ 54,000

$12,800 U $ 7,200 U

Total flexible–budget variance Total sales–volume variance

$20,000 U

Total static–budget variance

a $112 × 2,800 = $313,600

b $110 × 2,800 = $308,000

c $110 × 3,000 = $330,000

d Given. Unit variable cost = $229,600 ÷ 2,800 = $82 per tire

e $74 × 2,800 = $207,200

f $74 × 3,000 = $222,000

g Given

2. The key information items are:

Actual

Budgeted

Units

Unit selling price

Unit variable cost

Fixed costs

2,800

$ 112

$ 82

$50,000

3,000

$ 110

$ 74

$54,000

The total static–budget variance in operating income is $20,000 U. There is both an unfavorable

total flexible–budget variance ($12,800) and an unfavorable sales–volume variance ($7,200).

The unfavorable sales–volume variance arises solely because actual units manufactured

and sold were 200 less than the budgeted 3,000 units. The unfavorable flexible–budget variance

of $12,800 in operating income is due primarily to the $8 increase in unit variable costs. This

increase in unit variable costs is only partially offset by the $2 increase in unit selling price and

the $4,000 decrease in fixed costs.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–4

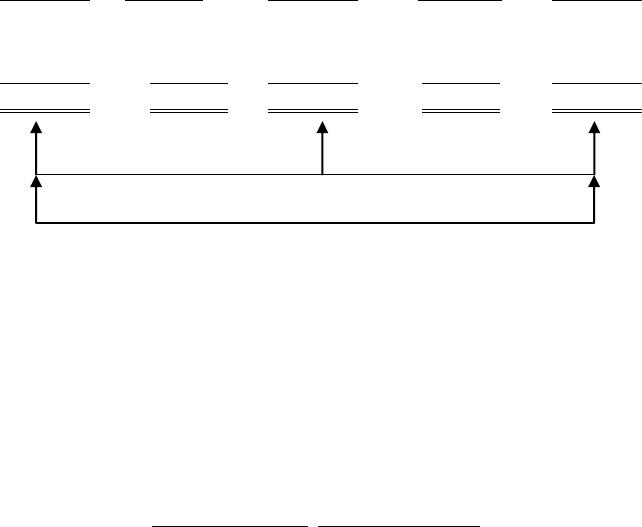

7–17 (15 min.) Flexible budget.

The existing performance report is a Level 1 analysis, based on a static budget. It makes no

adjustment for changes in output levels. The budgeted output level is 10,000 units––direct

materials of $400,000 in the static budget ÷ budgeted direct materials cost per attaché case of

$40.

The following is a Level 2 analysis that presents a flexible–budget variance and a sales–

volume variance of each direct cost category.

Variance Analysis for Connor Company

Actual

Results

(1)

Flexible-

Budget

Variances

(2) = (1) – (3)

Flexible

Budget

(3)

Sales-

Volume

Variances

(4) = (3) – (5)

Static

Budget

(5)

Output units

Direct materials

Direct manufacturing labor

Direct marketing labor

Total direct costs

8,800

$364,000

78,000

110,000

$552,000

0

$12,000 U

7,600 U

4,400 U

$24,000 U

8,800

$352,000

70,400

105,600

$528,000

1,200 U

$48,000 F

9,600 F

14,400 F

$72,000 F

10,000

$400,000

80,000

120,000

$600,000

$24,000 U $72,000 F

Flexible–budget variance Sales–volume variance

$48,000 F

Static–budget variance

The Level 1 analysis shows total direct costs have a $48,000 favorable variance.

However, the Level 2 analysis reveals that this favorable variance is due to the reduction in

output of 1,200 units from the budgeted 10,000 units. Once this reduction in output is taken into

account (via a flexible budget), the flexible–budget variance shows each direct cost category to

have an unfavorable variance indicating less efficient use of each direct cost item than was

budgeted, or the use of more costly direct cost items than was budgeted, or both.

Each direct cost category has an actual unit variable cost that exceeds its budgeted unit

cost:

Actual

Budgeted

Units

Direct materials

Direct manufacturing labor

Direct marketing labor

8,800

$ 41.36

$ 8.86

$ 12.50

10,000

$ 40.00

$ 8.00

$ 12.00

Analysis of price and efficiency variances for each cost category could assist in further the

identifying causes of these more aggregated (Level 2) variances.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–5

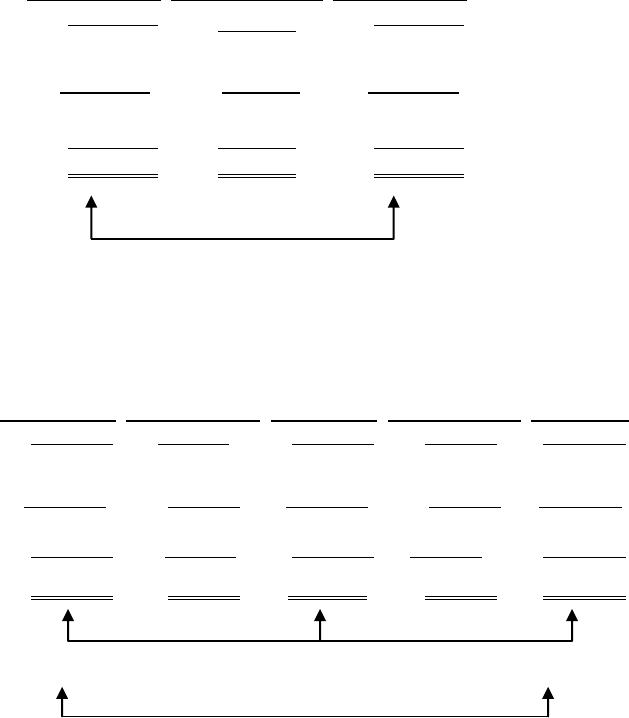

7–18 (25–30 min.) Flexible–budget preparation and analysis.

1. Variance Analysis for Bank Management Printers for September 2012

Level 1 Analysis

Actual

Results

(1)

Static-Budget

Variances

(2) = (1) – (3)

Static

Budget

(3)

Units sold

Revenue

12,000

$252,000a

3,000 U

$48,000 U

15,000

$300,000c

Variable costs

84,000d

36,000 F

120,000f

Contribution margin

Fixed costs

Operating income

168,000

150,000

$ 18,000

12,000 U

5,000 U

$17,000 U

180,000

145,000

$ 35,000

$17,000 U

Total static–budget variance

2. Level 2 Analysis

Actual

Results

(1)

Flexible-

Budget

Variances

(2) = (1) – (3)

Flexible

Budget

(3)

Sales

Volume

Variances

(4) = (3) – (5)

Static

Budget

(5)

Units sold

12,000

0

12,000

3,000 U

15,000

Revenue

$252,000a

$12,000 F

$240,000b

$60,000 U

$300,000c

Variable costs

84,000d

12,000 F

96,000e

24,000 F

120,000f

Contribution margin

168,000

24,000 F

144,000

36,000 U

180,000

Fixed costs

150,000

5,000 U

145,000

0

145,000

Operating income

$ 18,000

$19,000 F

$ (1,000)

$36,000 U

$ 35,000

$19,000 F $36,000 U

Total flexible–budget Total sales–volume

variance variance

$17,000 U

Total static–budget variance

a 12,000 × $21 = $252,000 d 12,000 × $7 = $ 84,000

b 12,000 × $20 = $240,000 e 12,000 × $8 = $ 96,000

c 15,000 × $20 = $300,000 f 15,000 × $8 = $120,000

3. Level 2 analysis breaks down the static–budget variance into a flexible–budget variance

and a sales–volume variance. The primary reason for the static–budget variance being

unfavorable ($17,000 U) is the reduction in unit volume from the budgeted 15,000 to an actual

12,000. One explanation for this reduction is the increase in selling price from a budgeted $20 to

an actual $21. Operating management was able to reduce variable costs by $12,000 relative to

the flexible budget. This reduction could be a sign of efficient management. Alternatively, it

could be due to using lower quality materials (which in turn adversely affected unit volume).

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–6

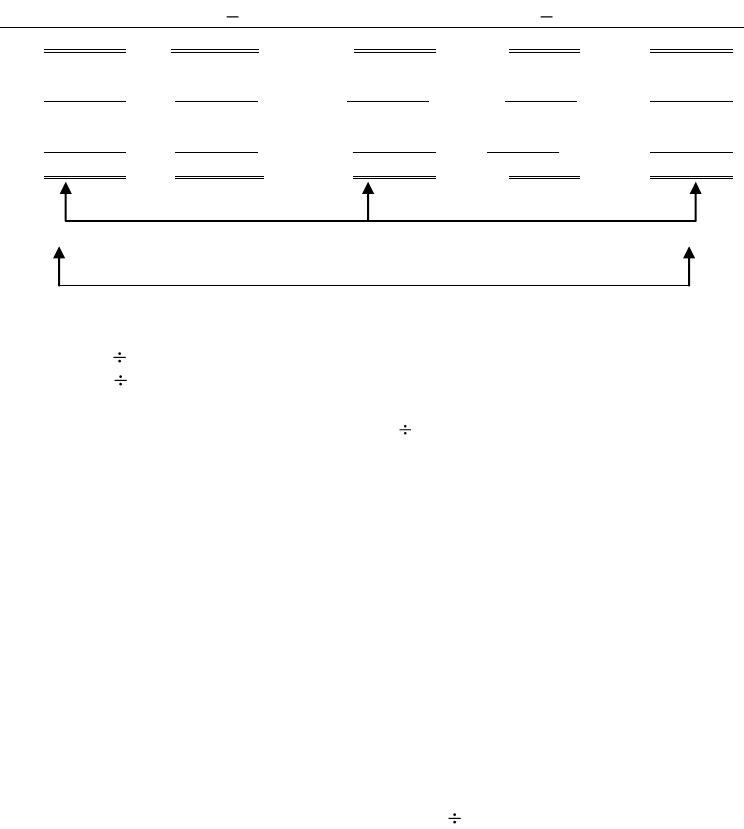

7–19 (30 min.) Flexible budget, working backward.

1. Variance Analysis for The Clarkson Company for the year ended December 31, 2012

Actual

Results

(1)

Flexible-

Budget

Variances

(2)=(1)(3)

Flexible

Budget

(3)

Sales-Volume

Variances

(4)=(3)(5)

Static

Budget

(5)

Units sold

130,000

0

130,000

10,000 F

120,000

Revenues

$715,000

$260,000 F

$455,000a

$35,000 F

$420,000

Variable costs

515,000

255,000 U

260,000b

20,000 U

240,000

Contribution margin

200,000

5,000 F

195,000

15,000 F

180,000

Fixed costs

140,000

20,000 U

120,000

0

120,000

Operating income

$ 60,000

$ 15,000 U

$ 75,000

$15,000 F

$ 60,000

a 130,000 × $3.50 = $455,000; $420,000 120,000 = $3.50

b 130,000 × $2.00 = $260,000; $240,000 120,000 = $2.00

2. Actual selling price: $715,000 130,000 = $5.50

Budgeted selling price: 420,000 ÷ 120,000 = $3.50

Actual variable cost per unit: 515,000 ÷ 130,000 = $3.96

Budgeted variable cost per unit: 240,000 ÷ 120,000 = $2.00

3. A zero total static–budget variance may be due to offsetting total flexible–budget and total

sales–volume variances. In this case, these two variances exactly offset each other:

Total flexible–budget variance $15,000 Unfavorable

Total sales–volume variance $15,000 Favorable

A closer look at the variance components reveals some major deviations from plan.

Actual variable costs increased from $2.00 to $3.96, causing an unfavorable flexible–budget

variable cost variance of $255,000. Such an increase could be a result of, for example, a jump in

direct material prices. Clarkson was able to pass most of the increase in costs onto their

customers—actual selling price increased by 57% [($5.50 – $3.50) $3.50], bringing about an

offsetting favorable flexible-budget revenue variance in the amount of $260,000. An increase in

the actual number of units sold also contributed to more favorable results. The company should

examine why the units sold increased despite an increase in direct material prices. For example,

Clarkson’s customers may have stocked up, anticipating future increases in direct material

prices. Alternatively, Clarkson’s selling price increases may have been lower than competitors’

price increases. Understanding the reasons why actual results differ from budgeted amounts can

help Clarkson better manage its costs and pricing decisions in the future. The important lesson

learned here is that a superficial examination of summary level data (Levels 0 and 1) may be

insufficient. It is imperative to scrutinize data at a more detailed level (Level 2). Had Clarkson

not been able to pass costs on to customers, losses would have been considerable.

$15,000 U

Total flexible-budget variance

$15,000 F

Total sales volume variance

$0

Total static-budget variance

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

7–20 (30-40 min.) Flexible budget and sales volume variances, market–share and market–size variances.

1. and 2.

Performance Report for Marron, Inc., June 2012

Actual

Flexible Budget

Variances

Flexible Budget

Sales Volume

Variances

Static

Budget

Static

Budget

Variance

Static Budget

Variance as

% of Static

Budget

(1)

(2) = (1) – (3)

(3)

(4) = (3) – (5)

(5)

(6) = (1) – (5)

(7) = (6) (5)

Units (pounds)

355,000

—

355,000

10,000

F

345,000

10,000

F

2.90%

Revenues

$1,917,000

$17,750

U

$1,934,750a

$54,500

F

$1,880,250

$36,750

F

1.95%

Variable mfg. costs

1,260,250

17,750

U

1,242,500b

35,000

U

1,207,500

52,750

U

4.37%