5–1

CHAPTER 5

ACTIVITY-BASED COSTING AND ACTIVITY–BASED MANAGEMENT

5–1 Broad averaging (or ―peanut–butter costing‖) describes a costing approach that uses broad

averages for assigning (or spreading, as in spreading peanut butter) the cost of resources

uniformly to cost objects when the individual products or services, in fact, use those resources in

non–uniform ways.

Broad averaging, by ignoring the variation in the consumption of resources by different

cost objects, can lead to inaccurate and misleading cost data, which in turn can negatively impact

the marketing and operating decisions made based on that information.

5–2 Overcosting may result in overpricing and competitors entering a market and taking

market share for products that a company erroneously believes are low–margin or even

unprofitable.

Undercosting may result in companies selling products on which they are in fact losing

money, when they erroneously believe them to be profitable.

5–3 Costing system refinement means making changes to a simple costing system that

reduces the use of broad averages for assigning the cost of resources to cost objects and provides

better measurement of the costs of overhead resources used by different cost objects.

Three guidelines for refinement are

1. Classify as many of the total costs as direct costs as is economically feasible.

2. Expand the number of indirect cost pools until each of these pools is more

homogenous.

3. Use the cause–and–effect criterion, when possible, to identify the cost–allocation base

for each indirect–cost pool.

5–4 An activity–based approach refines a costing system by focusing on individual activities

(events, tasks, or units of work with a specified purpose) as the fundamental cost objects. It uses

the cost of these activities as the basis for assigning costs to other cost objects such as products

or services.

5–5 Four levels of a cost hierarchy are

(i) Output unit–level costs: costs of activities performed on each individual unit of a

product or service.

(ii) Batch–level costs: costs of activities related to a group of units of products or

services rather than to each individual unit of product or service.

(iii) Product-sustaining costs or service–sustaining costs: costs of activities undertaken to

support individual products or services regardless of the number of units or batches

in which the units are produced.

(iv) Facility-sustaining costs: costs of activities that cannot be traced to individual

products or services but support the organization as a whole.

5–6 It is important to classify costs into a cost hierarchy because costs in different cost pools

relate to different cost–allocation bases and not all cost–allocation bases are unit–level. For

example, an allocation base like setup hours is a batch–level allocation base, and design hours is

a product–sustaining base, both insensitive to the number of units in a batch or the number of

units of product produced. If costs were not classified into a cost hierarchy, the alternative would

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–2

be to consider all costs as unit–level costs, leading to misallocation of those costs that are not

unit–level costs.

5–7 An ABC approach focuses on activities as the fundamental cost objects. The costs of

these activities are built up to compute the costs of products, and services, and so on. Simple

costing systems have one or a few indirect cost pools, irrespective of the heterogeneity in the

facility while ABC systems have multiple indirect cost pools. An ABC approach attempts to use

cost drivers as the allocation base for indirect costs, whereas a simple costing system generally

does not. The ABC approach classifies as many indirect costs as direct costs as possible. A

simple costing system has more indirect costs.

5–8 Four decisions for which ABC information is useful are

1. pricing and product mix decisions,

2. cost reduction and process improvement decisions,

3. product design decisions, and

4. decisions for planning and managing activities.

5–9 No. Department indirect–cost rates are similar to activity–cost rates if (1) a single activity

accounts for a sizable fraction of the department’s costs, or (2) significant costs are incurred on

different activities within a department but each activity has the same cost–allocation base, or (3)

significant costs are incurred on different activities with different cost–allocation bases within a

department but different products use resources from the different activity areas in the same

proportions.

5–10 ―Tell–tale‖ signs that indicate when ABC systems are likely to provide the most benefits

are as follows:

1. Significant amounts of indirect costs are allocated using only one or two cost pools.

2. All or most indirect costs are identified as output–unit–level costs (i.e., few indirect

costs are described as batch–level, product–sustaining, or facility–sustaining costs).

3. Products make diverse demands on resources because of differences in volume,

process steps, batch size, or complexity.

4. Products that a company is well suited to make and sell show small profits, whereas

products that a company is less suited to produce and sell show large profits.

5. Operations staff has significant disagreements with the accounting staff about the

costs of manufacturing and marketing products and services.

5–11 The main costs and limitations of ABC are the measurements necessary to implement the

systems. Even basic ABC systems require many calculations to determine costs of products and

services. Activity–cost rates often need to be updated regularly. Very detailed ABC systems are

costly to operate and difficult to understand. Sometimes the allocations necessary to calculate

activity costs often result in activity–cost pools and quantities of cost–allocation bases being

measured with error. When measurement errors are large, activity–cost information can be

misleading.

5–12 No, ABC systems apply equally well to service companies such as banks, railroads,

hospitals, and accounting firms, as well merchandising companies such as retailers and

distributors.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–3

5–13 No. An activity–based approach should be adopted only if its expected benefits exceed its

expected costs. It is not always a wise investment. If the jobs, products or services are alike in

the way they consume indirect costs of a company, then a simple costing system will suffice.

5–14 Increasing the number of indirect–cost pools does NOT guarantee increased accuracy of

product or service costs. If the existing cost pool is already homogeneous, increasing the number

of cost pools will not increase accuracy. If the existing cost pool is not homogeneous, accuracy

will increase only if the increased cost pools themselves increase in homogeneity vis–à–vis the

single cost pool.

5–15 The controller faces a difficult challenge. The benefits of a better accounting system

show up in improved decisions by managers. It is important that the controller have the support

of these managers when seeking increased investments in accounting systems. Statements by

these managers showing how their decisions will be improved by a better accounting system are

the controller’s best arguments when seeking increased funding. For example, the new system

will result in more accurate product costs which will influence pricing and product mix

decisions. The new system can also be used to reduce product costs which will lower selling

prices. As a result, the customer will benefit from the new system.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–4

5–16 (20 min.) Cost hierarchy.

1. a. Indirect manufacturing labor costs of $1,450,000 support direct manufacturing labor

and are output unit–level costs. Direct manufacturing labor generally increases with

output units, and so will the indirect costs to support it.

b. Batch–level costs are costs of activities that are related to a group of units of a product

rather than each individual unit of a product. Purchase order–related costs (including

costs of receiving materials and paying suppliers) of $850,000 relate to a group of

units of product and are batch–level costs.

c. Cost of indirect materials of $275,000 generally changes with labor hours or machine

hours which are unit–level costs. Therefore, indirect material costs are output unit–

level costs.

d. Setup costs of $630,000 are batch–level costs because they relate to a group of units

of product produced after the machines are set up.

e. Costs of designing processes, drawing process charts, and making engineering

changes for individual products, $775,000, are product–sustaining because they relate

to the costs of activities undertaken to support individual products regardless of the

number of units or batches in which the product is produced.

f. Machine–related overhead costs (depreciation and maintenance) of $1,500,000 are

output unit–level costs because they change with the number of units produced.

g. Plant management, plant rent, and insurance costs of $925,000 are facility–sustaining

costs because the costs of these activities cannot be traced to individual products or

services but support the organization as a whole.

2. The complex boom box made in many batches will use significantly more batch–level

overhead resources compared to the simple boom box that is made in a few batches. In addition,

the complex boom box will use more product–sustaining overhead resources because it is

complex. Because each boom box requires the same amount of machine–hours, both the simple

and the complex boom box will be allocated the same amount of overhead costs per boom box if

Hamilton uses only machine–hours to allocate overhead costs to boom boxes. As a result, the

complex boom box will be undercosted (it consumes a relatively high level of resources but is

reported to have a relatively low cost) and the simple boom box will be overcosted (it consumes

a relatively low level of resources but is reported to have a relatively high cost).

3. Using the cost hierarchy to calculate activity–based costs can help Hamilton to identify

both the costs of individual activities and the cost of activities demanded by individual products.

Hamilton can use this information to manage its business in several ways:

a. Pricing and product mix decisions. Knowing the resources needed to manufacture and

sell different types of boom boxes can help Hamilton to price the different boom

boxes and also identify which boom boxes are more profitable. It can then emphasize

its more profitable products.

b. Hamilton can use information about the costs of different activities to improve

processes and reduce costs of the different activities. Hamilton could have a target of

reducing costs of activities (setups, order processing, etc.) by, say, 3% and constantly

seek to eliminate activities and costs (such as engineering changes) that its customers

perceive as not adding value.

c. Hamilton management can identify and evaluate new designs to improve performance

by analyzing how product and process designs affect activities and costs.

d. Hamilton can use its ABC systems and cost hierarchy information to plan and

manage activities. What activities should be performed in the period and at what cost?

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–5

5–17 (25 min.) ABC, cost hierarchy, service.

1. Output unit–level costs

a. Direct–labor costs, $146,000

b. Equipment–related costs (rent, maintenance, energy, and so on), $350,000

These costs are output unit–level costs because they are incurred on each unit of materials

tested, that is, for every hour of testing.

Batch–level costs

c. Setup costs, $430,000

These costs are batch–level costs because they are incurred each time a batch of materials

is set up for either HT or ST, regardless of the number of hours for which the tests are

subsequently run.

Service-sustaining costs

d. Costs of designing tests, $264,000.

These costs are service–sustaining costs because they are incurred to design the HT and

ST tests, regardless of the number of batches tested or the number of hours of test time.

2.

Heat Testing (HT)

Stress Testing (ST)

Total

(1)

Per Hour

(2) = (1) 40,000

Total

(3)

Per Hour

(4) = (3) 30,000

Direct labor costs (given)

$100,000

$ 2.50

$ 46,000

$ 1.53

Equipment-related costs

$5 per hour* 40,000 hours

200,000

5.00

$5 per hour* 30,000 hours

150,000

5.00

Setup costs

$25 per setup-hour† 13,600 setup-hours

340,000

8.50

$25 per setup-hour† 3,600 setup-hours

90,000

3.00

Costs of designing tests

$60 per hour** 3,000 hours

180,000

4.50

$60 per hour** 1,400 hours

84,000

2.80

Total costs

$820,000

$20.50

$370,000

$12.33

*$350,000 (40,000 + 30,000) hours = $5 per test–hour

†$430,000 (13,600 + 3,600) setup hours = $25 per setup–hour

**$264,000 (3,000 + 1,400) hours = $60 per hour

At a cost per test–hour of $17, the simple costing system undercosts heat testing ($20.50) and

overcosts stress testing ($12.33). The reason is that heat testing uses direct labor, setup, and

design resources per hour more intensively than stress testing. Heat tests are more complex, take

longer to set up, and are more difficult to design. The simple costing system assumes that testing

costs per hour are the same for heat testing and stress testing.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–6

3. The ABC system better captures the resources needed for heat testing and stress testing

because it identifies all the various activities undertaken when performing the tests and

recognizes the levels of the cost hierarchy at which costs vary. Hence, the ABC system generates

more accurate product costs.

Vineyard’s management can use the information from the ABC system to make better

pricing and product mix decisions. For example, it might decide to increase the prices charged

for the more costly heat testing and consider reducing prices on the less costly stress testing.

Vineyard should watch if competitors are underbidding Vineyard in stress testing, and causing it

to lose business. Vineyard can also use ABC information to reduce costs by eliminating

processes and activities that do not add value, identifying and evaluating new methods to do

testing that reduce the activities needed to do the tests, reducing the costs of doing various

activities, and planning and managing activities.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–7

5–18 (15 min.) Alternative allocation bases for a professional services firm.

1.

Direct Professional Time

Support Services

Amount

Client

Rate per

Hour

Number

of Hours

Total

Rate

Total

Billed to

Client

(1)

(2)

(3)

(4) = (2) (3)

(5)

(6) = (4) (5)

(7) = (4) + (6)

SAN ANTONIO

DOMINION

Walliston

Boutin

Abbington

$640

220

100

26

5

39

$16,640

1,100

3,900

30%

30

30

$4,992

330

1,170

$21,632

1,430

5,070

$28,132

AMSTERDAM

ENTERPRISES

Walliston

Boutin

Abbington

$640

220

100

4

14

52

$2,560

3,080

5,200

30%

30

30

$768

924

1,560

$ 3,328

4,004

6,760

$14,092

2.

Direct Professional Time

Support Services

Client

Rate

per

Hour

Number

of Hours

Total

Rate per

Hour

Total

Amount

Billed to

Client

(1)

(2)

(3)

(4) = (2) (3)

(5)

(6) = (3) (5)

(7) = (4) + (6)

SAN ANTONIO

DOMINION

Walliston

Boutin

Abbington

$640

220

100

26

5

39

$16,640

1,100

3,900

$75

75

75

$1,950

375

2,925

$18,590

1,475

6,825

$26,890

AMSTERDAM

ENTERPRISES

Walliston

Boutin

Abbington

$640

220

100

4

14

52

$2,560

3,080

5,200

$75

75

75

$ 300

1,050

3,900

$ 2,860

4,130

9,100

$16,090

Requirement 1 Requirement 2

San Antonio Dominion $28,132 $26,890

Amsterdam Enterprises 14,092 16,090

$42,224 $42,980

Both clients use 70 hours of professional labor time. However, San Antonio Dominion uses a

higher proportion of Walliston’s time (26 hours), which is more costly. This attracts the highest

support–services charge when allocated on the basis of direct professional labor costs.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–8

3. Assume that the Walliston Group uses a cause–and–effect criterion when choosing the

allocation base for support services. You could use several pieces of evidence to determine

whether professional labor costs or hours is the driver of support–service costs:

a. Interviews with personnel. For example, staff in the major cost categories in support

services could be interviewed to determine whether Walliston requires more support

per hour than, say, Abbington. The professional labor costs allocation base implies

that an hour of Walliston’s time requires 6.40 ($640 ÷ $100) times more support–

service dollars than does an hour of Abbington’s time.

b. Analysis of tasks undertaken for selected clients. For example, if computer–related

costs are a sizable part of support costs, you could determine if there was a systematic

relationship between the percentage involvement of professionals with high billing

rates on cases and the computer resources consumed for those cases.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–9

5–19 (20 min.) Plantwide, department and ABC indirect cost rates.

1.

Actual plant-wide variable

MOH rate based on machine

hours, $308,600

4,000

$77.15 per machine hour

United

Motors

Holden

Motors

Leland

Vehicle

Total

Variable manufacturing overhead, allocated

based on machine hours

($77.15

120; $77.15

2,800; $77.15

1,080)

$9,258

$216,020

$83,322

$308,600

2.

Department

Variable MOH

in 2011

Total

Driver Units

Rate

Design

$39,000

390

$100

per CAD-design hour

Production

29,600

370

$ 80

per engineering hour

Engineering

240,000

4,000

$ 60

per machine hour

United

Motors

Holden

Motors

Leland

Vehicle

Total

Design-related overhead, allocated on CAD–design hours

(110

$100; 200

$100; 80

$100)

$11,000

$ 20,000

$ 8,000

$ 39,000

Production-related overhead, allocated on engineering hours

(70

$80; 60

$80; 240

$80)

5,600

4,800

19,200

29,600

Engineering-related overhead, allocated on machine hours

(120

$60; 2,800

$60; 1,080

$60)

7,200

168,000

64,800

240,000

Total

$23,800

$192,800

$92,000

$308,600

3.

United

Motors

Holden

Motors

Leland

Vehicle

a. Department rates

(Requirement 2)

b. Plantwide rate

(Requirement 1)

$23,800

$ 9,258

$192,800

$216,020

$92,000

$83,322

Ratio of (a) ÷ (b)

2.57

0.89

1.10

The variable manufacturing overhead allocated to United Motors increases by 157% under the

department rates, the overhead allocated to Holden decreases by about 11% and the overhead

allocated to Leland increases by about 10%.

The three contracts differ sizably in the way they use the resources of the three

departments.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–10

The percentage of total driver units in each department used by the companies is:

Department

Cost

Driver

United

Motors

Holden

Motors

Leland

Vehicle

Design

Engineering

Production

CAD-design hours

Engineering hours

Machine hours

28%

19

3

51%

16

70

21%

65

27

The United Motors contract uses only 3% of total machines hours in 2011, yet uses 28%

of CAD design–hours and 19% of engineering hours. The result is that the plantwide rate, based

on machine hours, will greatly underestimate the cost of resources used on the United Motors

contract. This explains the 157% increase in indirect costs assigned to the United Motors

contract when department rates are used. The Leland Vehicle contract also uses far fewer

machine–hours than engineering–hours and is also undercosted.

In contrast, the Holden Motors contract uses less of design (51%) and engineering (16%)

than of machine–hours (70%). Hence, the use of department rates will report lower indirect costs

for Holden Motors than does a plantwide rate.

Holden Motors was probably complaining under the use of the simple system because its

contract was being overcosted relative to its consumption of MOH resources. United and Leland,

on the other hand, were having their contracts undercosted and underpriced by the simple

system. Assuming that AP is an efficient and competitive supplier, if the new department–based

rates are used to price contracts, United and Leland will be unhappy. AP should explain to

United and Leland how the calculation was done, and point out United’s high use of design and

engineering resources and Leland’s high use of engineering resources relative to production

machine hours. Discuss ways of reducing the consumption of those resources, if possible, and

show willingness to partner with them to do so. If the price rise is going to be steep, perhaps

offer to phase in the new prices.

4. Other than for pricing, AP can also use the information from the department–based

system to examine and streamline its own operations so that there is maximum value–added from

all indirect resources. It might set targets over time to reduce both the consumption of each

indirect resource and the unit costs of the resources. The department–based system gives AP

more opportunities for targeted cost management.

5. It would not be worthwhile to further refine the cost system into an ABC system if (1) a

single activity accounts for a sizable proportion of the department’s costs or (2) significant costs

are incurred on different activities within a department, but each activity has the same cost driver

or (3) there wasn’t much variation among contracts in the consumption of activities within a

department. If, for example, most activities within the design department were, in fact, driven by

CAD–design hours, then the more refined system would be more costly and no more accurate

than the department–based cost system. Even if there was sufficient variation, considering the

relative sizes of the 3 department cost pools, it may only be cost–effective to further analyze the

engineering cost pool, which consumes 78% ($240,000

$308,600) of the manufacturing

overhead.

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

5–11

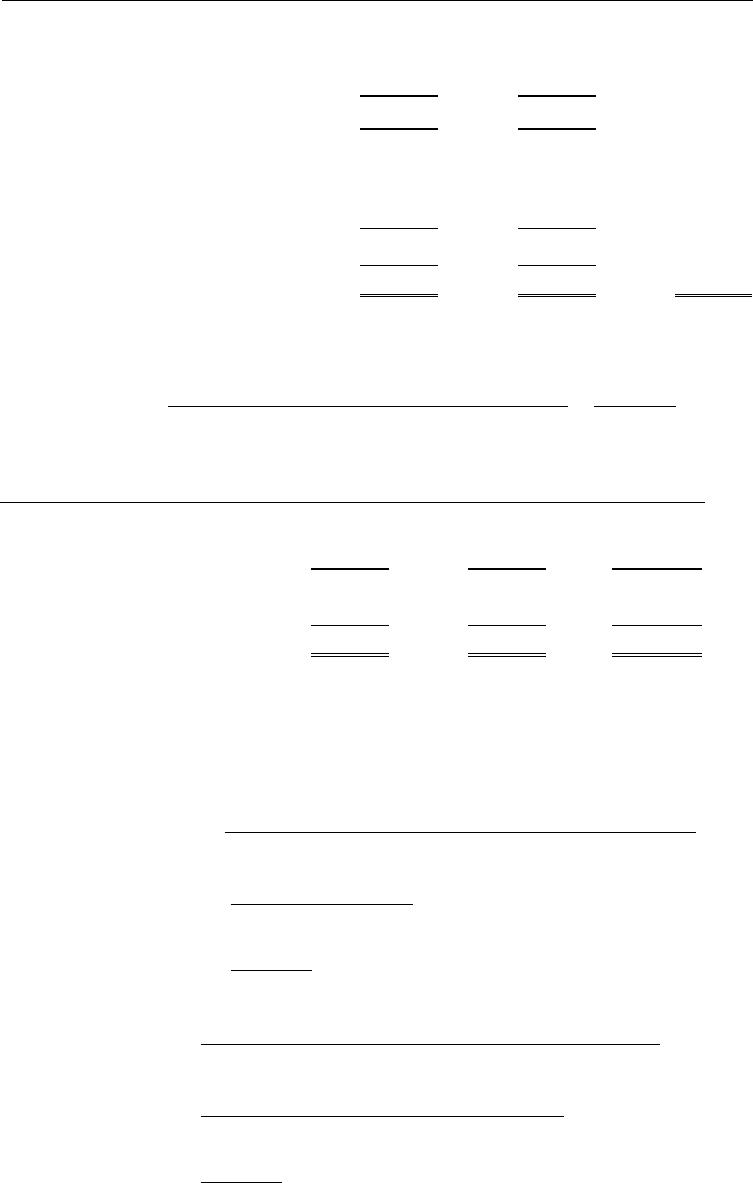

5–20 (50 min.) Plantwide, department, and activity–cost rates.

1.

Trophies

Plaques

Total

Direct materials

Forming

$13,000

$11,250

Assembly

2,600

9,375

Total

15,600

20,625

Direct Labor

Forming

15,600

9,000

Assembly

7,800

10,500

Total

23,400

19,500

Total direct costs

$39,000

$40,125

$79,125

Budgeted

overhead rate

=

($12, 000 $10,386 $23, 000 $10,960) $56,346

$79,125 $79,125

=

$0.712114

per dollar of direct cost

Trophies

Plaques

Total

Direct materials

$15,600

$20,625

$ 36,225

Direct labor

23,400

19,500

42,900

Total direct cost

39,000

40,125

79,125

Allocated overhead*

27,772

28,574

56,346

Total costs

$66,772

$68,699

$135,471

*Allocated overhead = Total direct cost Budgeted overhead rate (0.712114).

2.

Budgeted

overhead rate

Forming Dept.

—

=

Budgeted Forming Department overhead cos ts

Budgeted Forming Department direct–labor costs

=

$12, 000 $10,386

$15, 600 $9, 000

=

$22,386

$24, 600

$0.91 per Forming Department direct–labor dollar

Budgeted

overhead rate

Assembly Dept.

—

=

Budgeted Assembly Department overhead costs

Budgeted Assembly Department direct costs

=

$23, 000 $10,960

($2, 600 $9,375 $7,800 $10,500)

=

$33,960

$30, 275

$1.121718 per Assembly Department direct cost dollar

© 2012 Pearson Education, Inc. Publishing as Prentice Hall. SM Cost Accounting 14/e by Horngren

Trophies

Plaques

Total

Direct materials

$15,600

$20,625

$ 36,225

Direct labor

23,400

19,500

42,900

Total direct cost

39,000

40,125

79,125

Allocated overhead

Forming Dept.a

14,196

8,190

22,386

Assembly Dept.b

11,666

22,294

33,960

Total costs

$64,862

$70,609

$135,471

3.

Trophies

Plaques

Total

a Forming Dept.

Direct labor costs

$15,600

$ 9,000

$24,600

Allocated overhead

(0.91 × $15,600; $9,000)

$14,196

$ 8,190

$22,386

b Assembly Dept.

Total direct costs

($2,600 + $7,800; $9,375 + $10,500)

$10,400

$19,875

$30,275

Allocated overhead

$11,666

$22,294

$33,960