FINA Case 2

Rosetta Stone: Pricing the 2009 IPO

Michael Morrison, Thomas Huang, Rachel Sims, Matthew Lustig,

EXECUTIVE SUMMARY

We recommend that you invest in Rosetta Stone, given the near-certainty that its stock price will continue

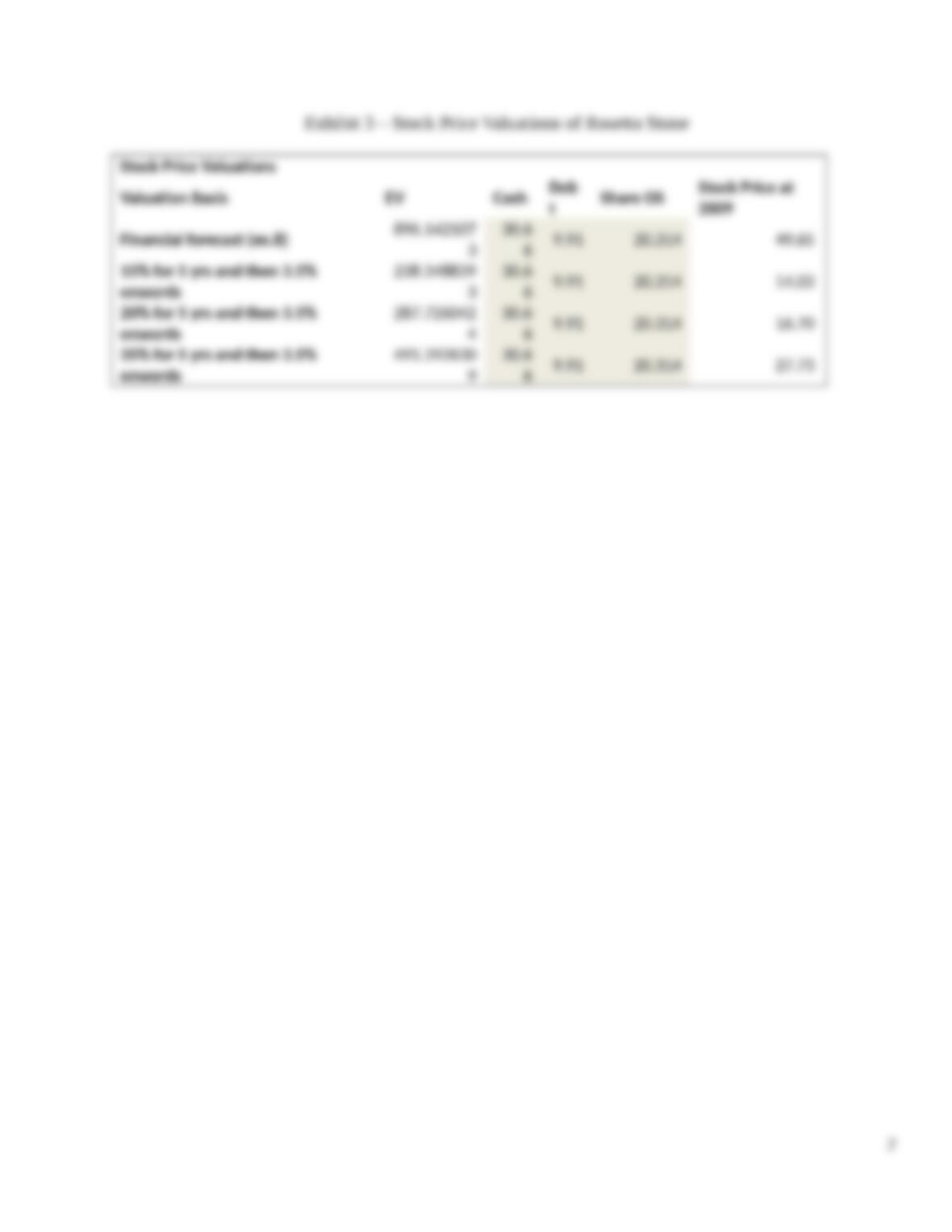

rising after the IPO. Using the conservative valuation, the stock will open around $14, which is lower than the

executives’ estimate. However, since investor response was highly enthusiastic, we doubt that will be the final

IPO price. We suspect the IPO price will rise above the $15-$17 range, and we recommend that you buy if the

price is anywhere below $20. We also estimate that the stock price of Rosetta Stone will grow to $32, even

potentially reaching $49.79 in the first year.

ADVANTAGES AND DISADVANTAGES OF THE IPO

First, the increase in capital from the IPO will fuel growth for Rosetta Stone. Rosetta Stone remained

profitable through 2008, the lowest year of the recession, demonstrating its potential for growth. In addition, 95%

of Rosetta Stone’s sales comes from the U.S., which reveals clear potential to expand internationally. The

language-learning market is $5 billion in the U.S., $2 billion of which is self-study learning, like Rosetta Stone’s

signature product. Moreover, Rosetta Stone will use its proven ability to adapt (e.g. Rosetta Studio and Rosetta

World offerings), to continue to gain market share. Rosetta Stone has already obtained seven times the awareness

of any other language-learning company, and the IPO will further increase public awareness of the brand1.

Rosetta Stone’s marketing will determine the extent of these advantages, since it has the choice to market

either as a tech or educational company. While investors may seek to invest in tech firms, which would thus drive

the stock price up, the company’s long-term financial health depends on the product being marketed as an

educational tool. Ultimately consumers seek Rosetta stone as an educational tool, not a technology device.

1 https://blog.wealthfront.com/ipo-101-series-why-do-companies-go-public/

1

Marketing as a technology company would create confusion and create a negative impact on revenues in the long

term.

Another disadvantage of the IPO stems from the increase in free educational opportunities, such as

MOOCs on sites like Coursera and open courseware like Kahn Academy. These sources do not yet offer a high-

caliber foreign language learning experience like Rosetta Stone’s, but Rosetta Stone’s IPO will publicize its

optimism about the foreign language learning market and spur competitors to gain market share over Rosetta

Stone.

ALTERNATIVES TO THE IPO

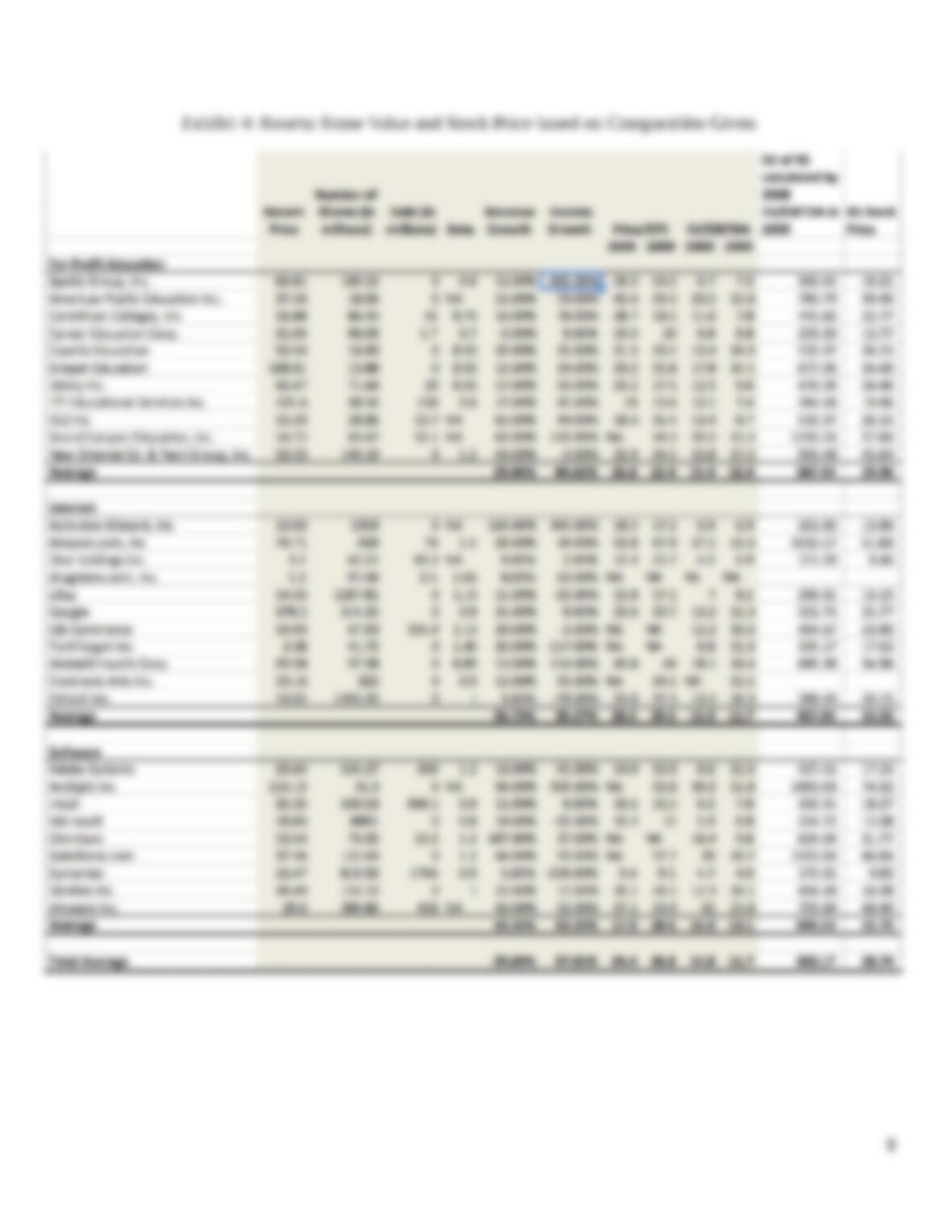

The first alternative to consider is selling to a tech firm. The average price per share of Internet and

software companies is $28.14. Using Rosetta’s full 20.3 million shares, this would put the stock valuation at

$571,242,000 (Ex.3). Secondly, Rosetta Stone could consider selling to a for-profit education company where the

average value per share equals $29.96. Again, using the 20.3 million shares, the stock valuation would be