RISING CONSUMERS ON THE HORIZON IN CHINA AND SOUTH AFRICA

Rising Consumers on the Horizon in China and South Africa

Keisha Hill

Across China and South Africa, rising incomes are creating a new class of consumers. As

these consumers gain purchasing power their needs and preferences will have great impact on the

global economy. Although separated by almost 7,000 miles in geographical distance, China and

South Africa have many similarities as it relates to the growth in their consumer markets. Some

of the largest business opportunities in South Africa and China will be in their rising consumer

markets. From 2000 to 2010, the size of the Chinese economy more than doubled increasing

consumption from around $650 billion to almost $1.4 trillion. (Townson 2012) While both countries

can expect growth in consumer markets there are differences in the way these changes will

manifest.

There are many different theories used to define the middle class, and how much one

needs to earn to fall into that category. The dictionary defines the middle class as the

socioeconomic class between the working class and the upper class. However, in South Africa

the middle class is loosely defined as a household of four people with a total income between

5,600 and 40,000 Rand per month after income tax, which is approximately $400- $2900 USD

(Business Tech 2016). Similarly, defining the Chinese middle class can vary and be confusing,

depending on the source or which numbers you use. According to “The official data from

China’s National Bureau of Statistics, the Chinese middle class is categorized as households with

an annual income ranging from $7,250 to $62,500 (60,000 to 500,000 Yuan)” (Wang, 2010).

RISING CONSUMERS ON THE HORIZON IN CHINA AND SOUTH AFRICA

By the beginning of the next decade both China and South Africa will see a significant increase

in their middle class population. According to a report by McKinsey “Over the past decade more

than three and a half million South Africans have been lifted out of extreme poverty. As of 2015, the

country’s consuming class grew to encompass about nine million households, accounting for $191

billion in private consumption.” (Woetzel 2015). The rise in the middle class in South Africa has also

vastly increased the size of their black middle class. The countries black middle class was estimated

to be 4.2 million in 2012, which is just over 50% and is double the rate in 2004 (Business Tech,

2014). “Of the 8.3 million adults classified as middle class in 2012, 51% are black, 34% white.

South Africa’s middle class pends a whopping $40 billion annually on average” (Dürr 2013).

Increased spending power by the black middle class has caused an influx of fast-food outlets, as

well as increased spending on travel, groceries, and apparel. China has also seen exponential

growth in the expansion of its middle class, with 300 million people moving into its middle class

over the last 30 years. The Chinese middle class will be one of the biggest economic growth engines

in the years to come, as a projected 200 million people will join the middle class by 2026. If these

projections are accurate China will account for more than 66 percent of the world’s middle class

population by 2026. (Woetzel 2013).

One would expect that vast increases in the middle class would significantly increase the

demand for luxury products and upsurge spending. In China purchases have followed this

predictable trajectory, while consumers in South Africa continue to make cautious financial

decisions. According to McKinsey, “South Africans are still under tremendous financial pressure due

to higher prices (inflation has averaged 5.4 percent over the past five years, edging up to 6.4 percent in

2016) and low real growth in wages (averaging 1.3 percent in the past five years) (Magnus 2012)”.

Despite increased purchasing power, inflation and wage increases keep spending stagnant.

RISING CONSUMERS ON THE HORIZON IN CHINA AND SOUTH AFRICA

Studies show that even if their financial situation were to improve, South African consumers

will not necessarily increase spending. In a study conducted by McKinsey, survey respondents said that

“if their income were to rise by 10 percent, they would spend only about 22 cents of every additional

rand; the rest would go into savings and toward paying off debt” (Magnus 2012). Among consumers

who said they would spend a portion of their extra income, most said it would be to buy everyday

necessities. On the other hand, South Africans belonging to the middle class have increased

discretionary income, which has increased consumption of buying new cars, modern electronics,

mobile phones, houses and designer clothes. In particular the middle class, has relatively high

spending levels. This is particularly true for the new black middle class that has emerged. These

consumers seek sophisticated goods and tend to spend less on vital commodities or housing.

On the contrary, Chinese consumers have continued increased spending on products that offer high

value for low cost and luxury items. Consumer focused companies that have mastered providing value

while remaining affordable, have flourished. They have focused on providing basic necessities such as

furniture, washing machines, and small residential apartments.

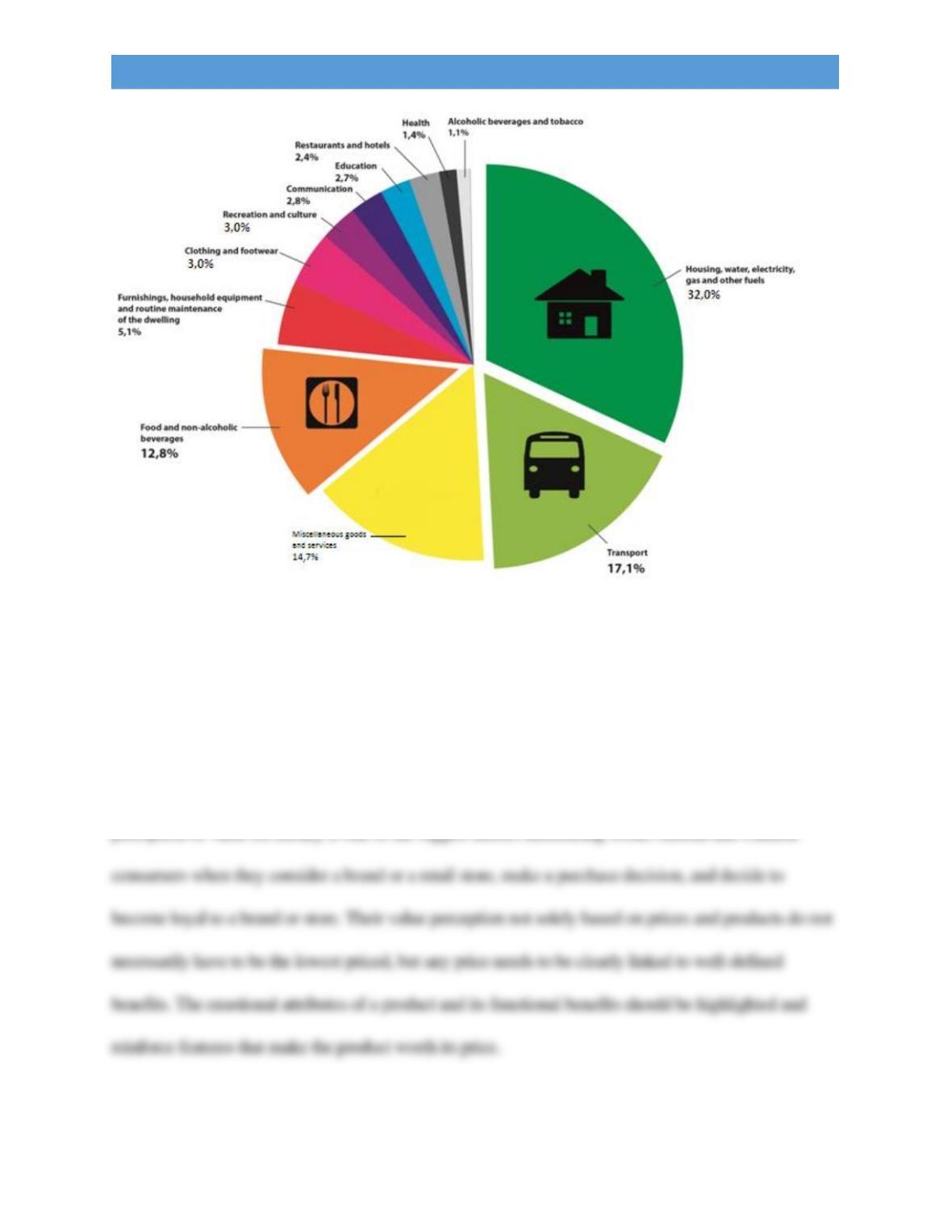

In South Africa approximately 32 percent of overall household consumption expenditure

went to housing, water, gas and electricity. They also tend to spend large quantities on

transportation, and food and beverage, which make up 17.1 and 12.8 percent respectively (Stats

SA 2013). The breakdown of South African consumer spending by category is illustrated

graphically below.

RISING CONSUMERS ON THE HORIZON IN CHINA AND SOUTH AFRICA

Source: (Stats SA, 2013)

There are several key habits that both Chinese and South Africans share. Both proactively

search for savings, are brand loyal contingent on price, and search for value. It is imperative that

companies give consumers solid reasons to choose their product or store over alternatives. The