Question 1

A fixed-income portfolio manager is managing a portfolio that is currently

valued at 10$ million. The manager is seeking to realize a rate of return of at

least 4% annually over a 5-year investment period. Three years later, spot

rates are at 6% for all maturities. How much can the value of the portfolio fall at

this time before the manager is forced to immunize, to be assured of achieving

the minimum required return? State any assumptions you make.

PV=10M R=4% R’=6%

FV (5) =10m*(1+4%)5=12.1665m

FV (3’) =12.1665m/ (1+6%)2=10.82814m

FV (3) =1212.1665m/ (1+4%)2=11.24861m

Possible fall of the value=FV (3)-FV (3’) = 11.24861m-10.82814m=0.4204m

Question 2

Consider three fixed rate mortgages, M1, M2 and M3, and assume that the

“fixed” rates may vary in parallel. Assume that a parallel shift in interest rates is

the same as an identical shift in each of the yields to maturity and ignore the

initial cashflow (i.e. ignore the fact that the mortgagee receives the initial

principal). The details of the mortgages are

All interest rates are compounded monthly. Mortgage repayments are

assumed to be monthly.

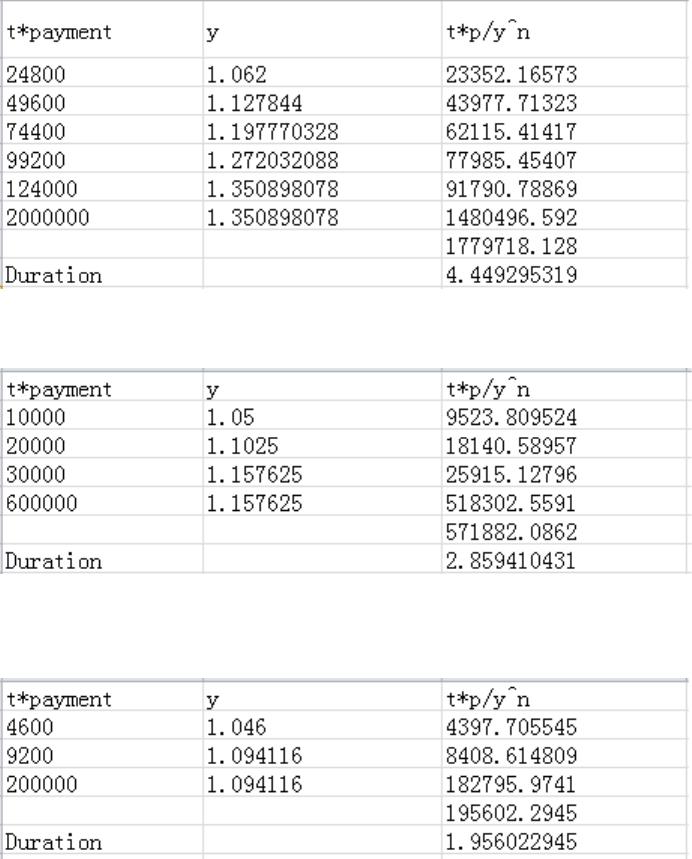

a. Find the yields to maturity of the mortgages from the bank’s point of view.

Effective Annual Yield = (1+r)^n–1

Y1 = 1.005^12 – 1 = 0.062

Y2 = 1.004^12 – 1 = 0.050

Y3 = 1.00375^12 – 1 = 0.046

b. Find the Macaulay, modified duration and convexity of the mortgages from

the bank’s point of view.

Macaulay Duration 1 = 4.45

Macaulay Duration 2 = 2.86

Macaulay Duration 3 = 1.96

Modified Duration = Macaulay Duration / (1+Y)

Modified Duration 1 = 4.19

Modified Duration 2 = 2.72

Modified Duration 3 = 1.87

Convexity = N(0~n)t*(t+1)*PV/P * 1/(1+y)^2

Convexity 1 = 22.72

Convexity 2 = 13.34

Convexity 3 = 7.83

c. If the bank wishes to hedge one 5 year mortgage against parallel shifts in

the interest rates using a 3 year mortgage. How many of these mortgages

does it require? How might the bank achieve this hedge?

In order to be able to hedge a long position in 5 year mortgage, we need to

take a short position in the same amount in 3 year mortgage. So we need

2 3–year mortgages as 400,000=200,000*2. In 5 years time, we close out

the position by taking a short position in 5 year mortgage and a long

position in 3 year mortgage. By doing this, we setup a hedge where the

losses of one position will approximately be equal to the gains of other

positions, hence creating a hedge position for our portfolio.

Question 3

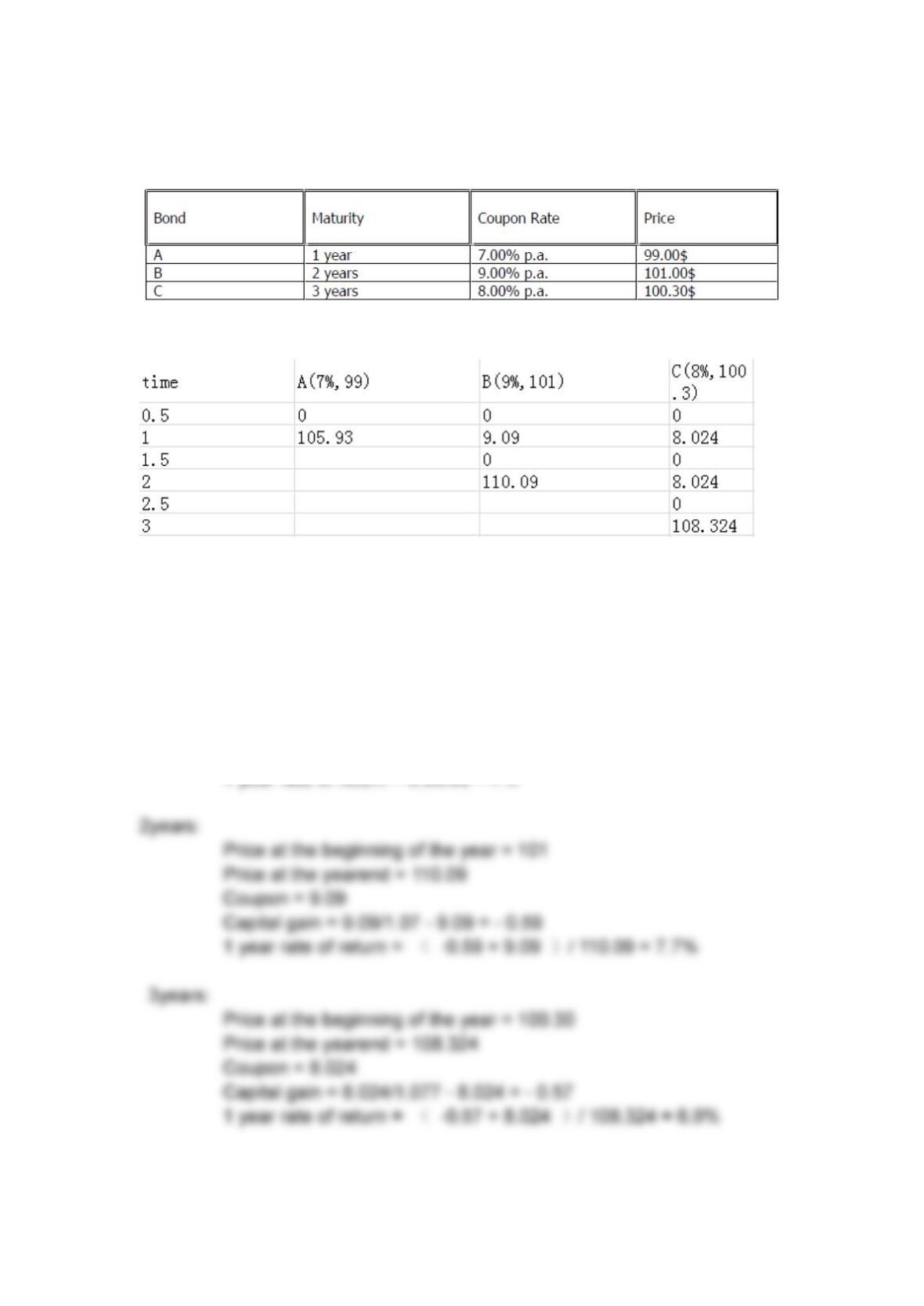

Consider the following annual-coupon paying Treasury bonds given in the

table below

a. Using the securities given in the table, construct portfolios that replicate the

cashflows of zeros with maturities of 1, 2 and 3 years.

b. Use the portfolios constructed to compute the prices of the zeros with

maturities of 1, 2 and

3 years.

1year:

Price at the beginning of the year = 99

Price at the yearend = 105.93

Coupon = 6.93