IMB 433

SEEMA GUPTA, KANCHAN MISHRA AND ASHISH MAHESHWARI

PROCTER & GAMBLE INDIA: GAP IN THE PRODUCT PORTFOLIO?

Procter & Gamble (P&G) the world’s largest consumer products company wanted to be as big as rival Unilever was

in India by 2015. Its India revenues were roughly a fourth of the Anglo-Dutch major’s local subsidiary. The

Cincinnati headquartered P&G wanted to shift the focus away from saturated western markets to emerging markets.

Developing economies accounted for just 30% of global sales. On the other hand, Unilever garnered more than half

of its revenues from India, Brazil, Indonesia, South Africa, China, and Vietnam. P&G started Project 2-3-4, to crack

open the Indian market – by 2015, P&G wanted to double the number of Indians who used its products, treble per

capita spending by Indians and quadruple net sales of its India operations. Shantanu Khosla, Head, P&G India said:

Of the 11 categories we play in, we are leaders in six – healthcare, blades & razors, feminine care,

baby care, anti-ageing skin care, and hair care. We have consistently achieved more than 20%

growth year on year and our business has grown 10 times over the last 8 years.i

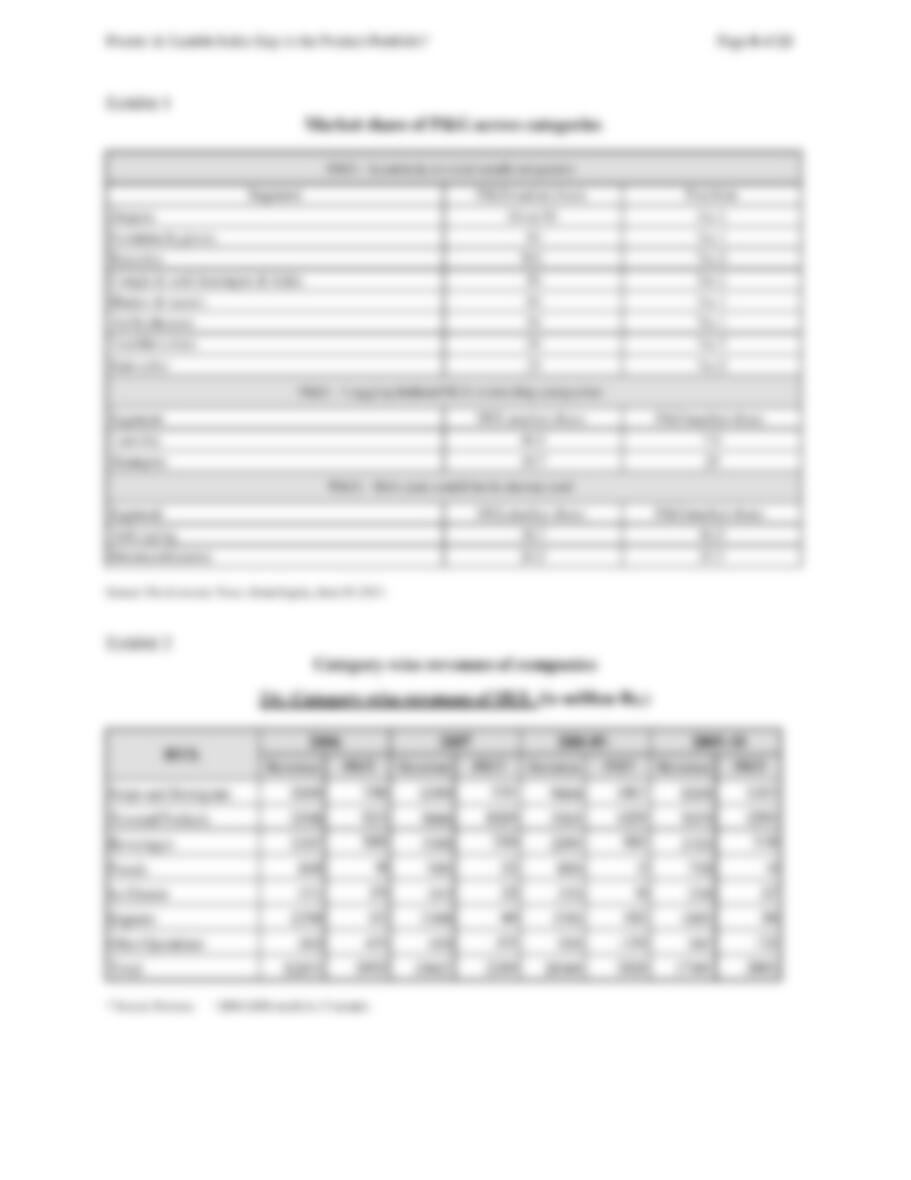

Although this was impressive, most of the categories that P&G dominated were still small. In the segments that

mattered such as detergents and hair care – which accounted for Rs. 180,000 million or a little over half of the home

& personal care (HPC) segment, HUL was the leader. Skin care with anti-aging and fairness creams could be its

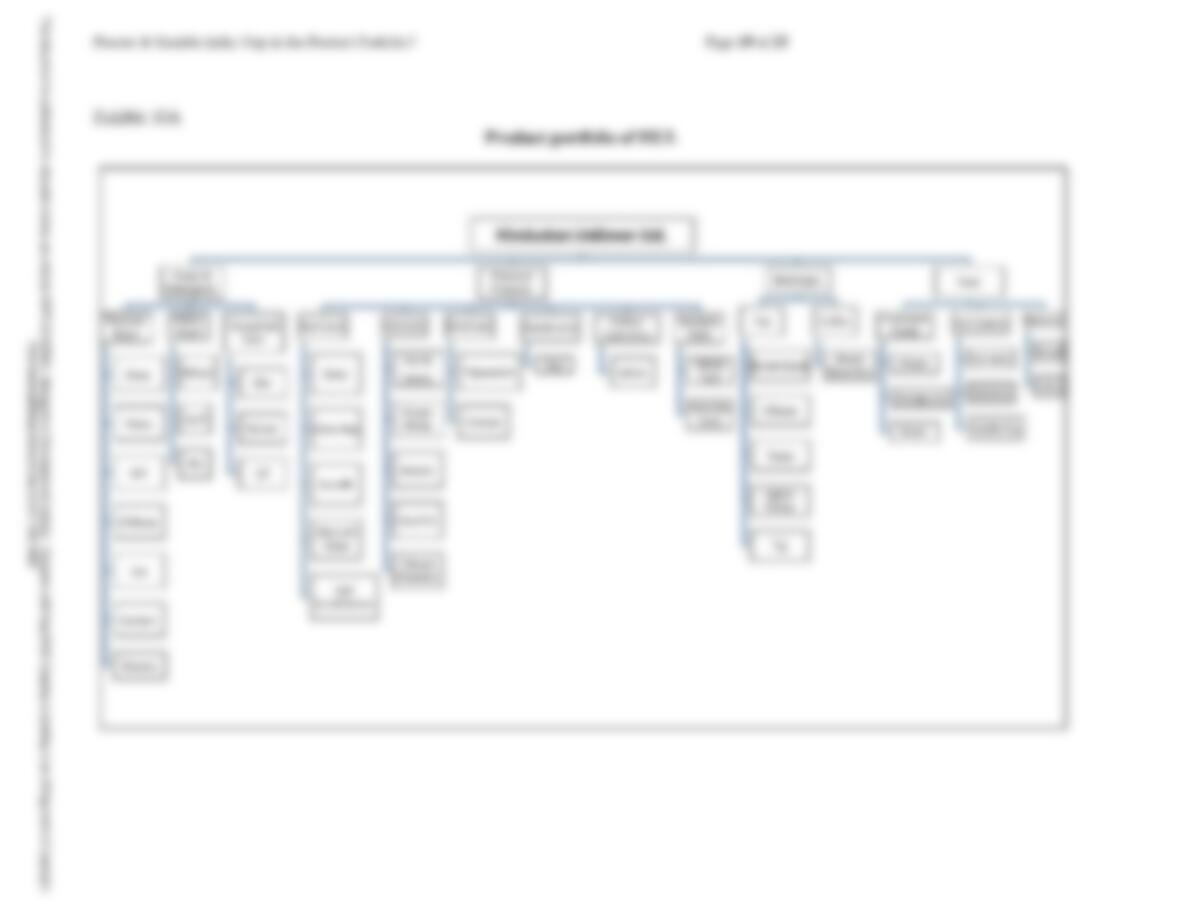

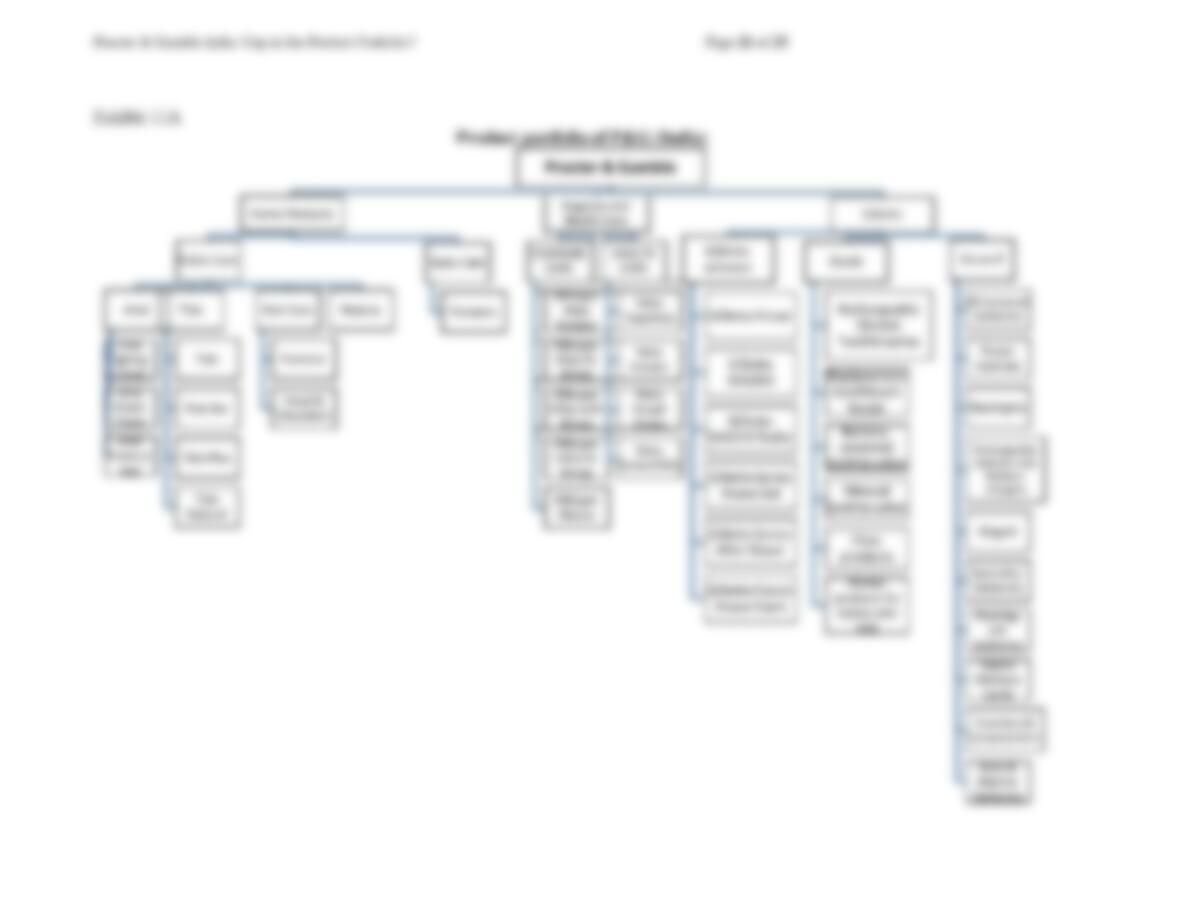

trump card (see Exhibit 1 for P&G’s market share across categories). Traditionally P&G, globally as well as in

India, thrived on premium brands such as Ariel and Whisper Ultra. However, in Asia and Africa, it started targeting

consumers across the pyramid. For example, P&G launched four variants of feminine hygiene product Whisper –

Whisper Choice at the mass end; Whisper Maxi in the mid-segment; Whisper Choice Ultra for those aspiring

looking to upgrade from the low-priced segment; and Whisper Ultra, in the premium segment. Such segmentation

led to increase in sales. Khosla said:

Most of the categories P&G is present in India are small but, over time, as disposable incomes and

penetration increase they will become mass market brands.ii

If P&G had to gain critical mass, it had to penetrate rural hinterlands. Perhaps for this reason, in the short to medium

terms, P&G decided to focus on driving distribution deeper into the villages than on launching new products and

entering new categories. Anand Mour, V. P. Indiabulls Securities said:

P&G has doubled its distribution reach over the last couple of years. And it does not lag HUL by

much. P&G’s direct reach is 1.3 million outlets as compared to HUL’s 1.6 million outlets.iii

Internally, P&G had classified the domestic market into three categories. India 1 comprised some 8.5 million

households of “affluent Indians,” India 2 was the rest of urban India that comprised 56 million households; and India

3 was the rural market consisting of 130 million households. P&G’s goal was to score wins in all three categories by

2015. For instance, for India 1, the plan was to double the revenues from key categories such as detergents, hair

care, and feminine hygiene to Rs. 11,250 million; for India 2, it intended to double revenues to Rs. 25,650 million

by riding on brands such as Tide and Head & Shoulders; and for India 3, it planned to take up revenues from Rs.

3,510 million to Rs. 8,100 million on the back of low-cost distribution models.

LAUNDRY DETERGENTS

Laundry detergent, a Rs. 99 billion market, with a CAGR of 8.4% during 2004–2009 was the largest segment that

FMCG (Fast Moving Consumer Goods) players operated in (see Exhibit 2 for sales from different segments). The

segment had the potential to drive P&G’s growth. The two brands – Ariel and Tide enabled P&G to garner 7.6%

Seema Gupta, Assistant Professor of Marketing, Kanchan Mishra and Ashish Maheshwari prepared this case for class discussion. This case is not

intended to serve as an endorsement, source of primary data, or to show effective or inefficient handling of decision or business processes.

Copyright © 2013 by the Indian Institute of Management Bangalore. No part of the publication may be reproduced or transmitted in any form or

by any means – electronic, mechanical, photocopying, recording, or otherwise (including internet) – without the permission of Indian Institute of

Management Bangalore.

Procter & Gamble India: Gap in the Product Portfolio?

Page 2 of 23

share of the laundry detergent market. The repositioning of Tide in 2004 and the launch of Tide Natural in 2009

generated positive consumer response and led to increase in P&G’s sales (see Exhibit 3 for sales of various brands).

The success in the mid-segment made the marketing team ponder if P&G should take the plunge in the economy

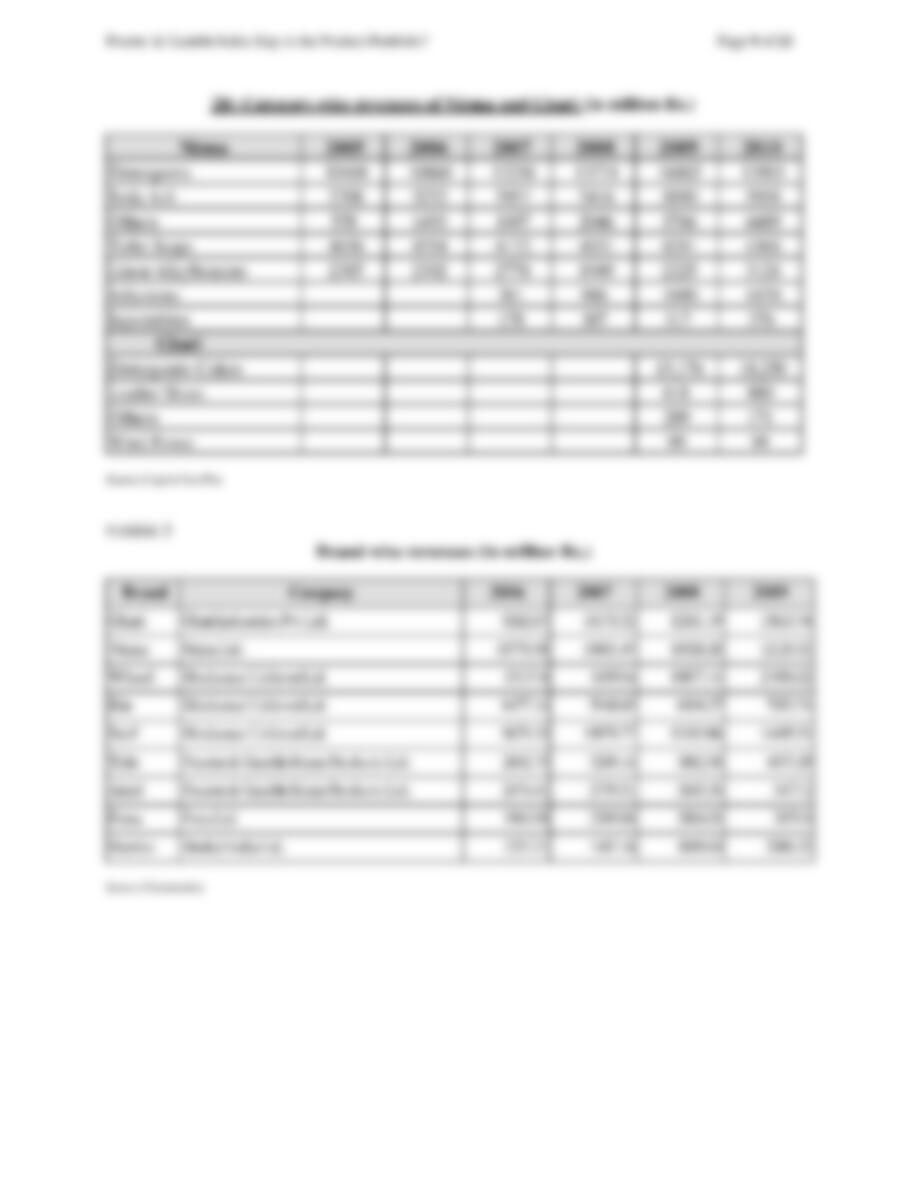

segment too. Hand-wash detergents used by the economy segment were more than thrice the size of the concentrated

powder detergents. Moreover, hand-wash detergent market was growing at a faster rate than concentrated powder

detergent (see Exhibit 4 for revenues of detergents by type).iv With high penetration in urban markets, future growth

would be driven by rural markets, majority of whom were in the bottom of the pyramid (BoP). The success of

regional players – Nirma and Ghari, whose market share was double that of P&G was a testimony to the potential of

the BoP market. The marketing team at P&G wondered if it was time to fill the void at the BoP.

The laundry detergent industry was consolidated by four major players – HUL, P&G, Nirma, and Rohit Surfactants

(makers of Ghari brand), accounting for more than 75% of the market. HUL was the market leader with 46% market

share, followed by Ghari with 13.7%, Nirma with 13.1%, and P&G with 7.6% share (see Exhibit 5 for company-

wise and brand-wise market share). HUL owned three brands – Surf Excel, Rin, and Wheel; whereas P&G owned

two brands – Ariel and Tide. While Ariel and Surf Excel competed in the premium concentrated detergent segment;

Tide and Rin competed in the mid-price segment and Wheel, Nirma, and Ghari competed in the economy segment.

HUL ENTRY IN INDIA

In 1888, Lever Brothers started exporting “Sunlight” laundry soap to India. Soon after, the company launched

Lifebuoy in 1895. Other brands such as Pears, Lux, and Vim were introduced in India in 1918. These set the stage

for an era of branded FMCG in India.v In 1930s, Unilever set up three subsidiaries in India which were merged in

1956 to form Hindustan Lever Limited (HLL).

Traditionally, Indians had used bars to wash their clothes, a process involving the scrubbing of wet garments with

soap and then beating them with a club or against a stone. By introducing the revolutionary Surf washing powder in

1959, HUL affected a switch from the club to the bucket. Surf was an immediate success. However, only a fraction

of consumers could afford Surf. Most of the rural poor continued to use soap bars. To meet their needs, HLL

launched Rin bar in 1969, which also became a success.

RISE OF NIRMA

In 1969, Karsanbhai Patel, an entrepreneur in Gujarat launched “Nirma” a yellow-colored detergent powder at a

price one-third of HUL’s Surf. Nirma became an instant hit. Nirma was granted several concessions in taxes and

wage rules for being a cottage industry. For more than a decade, Nirma was virtually unchallenged as it tapped rural

markets, offered generous margins to trade and aired catchy ads on TV and radio. By 1985, Nirma commanded a

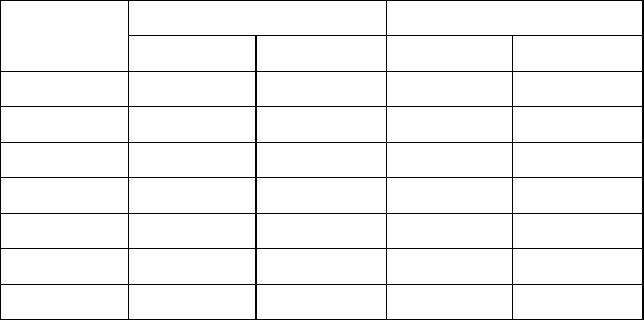

58% market share (by volume) and had become the largest detergent brand ahead of HUL’s Surf (Table 1).vi

Table 1 Comparative market share and price of Surf and Nirma

Year

Market Share

Price per kg (Rs.)

Surf

Nirma

Surf

Nirma

1977

30.6

11.9

12.80

4.35

1978

26.3

11.7

12.25

4.75

1979

24.7

21.3

11.95

4.45

1980

21.8

31.0

18.50

6.00

1981

19.4

33.2

20.20

6.25

1982

15.2

43.2

21.05

6.00

1983

11.5

51.5

20.90

6.25

Procter & Gamble India: Gap in the Product Portfolio?

Page 3 of 23

Table 2 (Contd.)

1984

9.4

57.3

22.20

6.80

1985

8.4

58.1

23.15

7.20

1986

8.4

59.1

23.70

8.00

1987

7.4

61.6

27.10

8.50

(1$ = Rs. 60, in July 2013)

To counter the threat of Nirma, HLL extended Sunlight from bars to powders and matched its price with Nirma.

HLL launched the memorable “Lalitaji” ad campaign to position Surf as a rational purchase. However, all these

efforts remained unsuccessful in curbing Nirma’s march. In 1988, “Wheel” was launched as a low-cost detergent

that promised cleaning without the burning and itching caused by Nirma’s high soda ash content. By 1990, it

surpassed Nirma to become the market leader. One of the reasons for success of HUL had been its intensive

distribution network.

DISTRIBUTION AT HUL

HUL had developed a highly efficient distribution system in urban India. Goods were sent to a depot, or a carrying

and forwarding agent (CFA) who stocked and dispatched HUL’s products for a service fee. HUL had at least one

depot per state. In each town, a redistribution stockist was appointed who ordered and received stocks from CFA

and sold them to wholesale and retail outlets in that area. HUL was organized into four profit centers – Detergents

(personal wash, fabric wash, and household care); Personal products (Skin, hair care, oral care, deodorants and

talcum powder and specialty); Beverages; and Food. Owing to the large number of brands, variants and stock

keeping units (SKUs) owned by HLL, it was virtually impossible for one stockist to manage all of HLL brands and

SKUs. Hence, each profit center had its own sales force and stockist.

HUL could not replicate this system in rural India because the population and potential business was too small for

each profit center to appoint a stockist exclusively. Hence, for rural markets that were accessible, HUL leveraged its

scale and appointed one stockist common to all businesses. In 1997, it launched a distribution model “Streamline”

for reaching rural markets that were inaccessible but had high potential. It appointed rural distributors (RDs) who in

turn appointed star sellers among the wholesalers in neighboring villages. A star seller would purchase stocks from

the RD and then distribute those to retailers in smaller villages using local means of transport such as motorcycles,

rickshaws, and bullock carts. These initiatives enhanced HUL’s reach into rural markets, enabling it to reach an

additional population of about 220 million in 100,000 villages.

However, that still left over 500,000 villages in inaccessible and low potential markets representing a population of

over 500 million. To extend its reach to these markets, HLL launched Project “Shakti” in 2000.vii HLL partnered

with members of the self-help groups (SHGs), mostly poor illiterate women who received micro credit from SHGs,

and offered them opportunities for micro-enterprise. The Shakti entrepreneur bought HLL products and sold them to

retailers and end-consumers in nearby villages. Wheel was the largest selling brand of the Shakti initiative.

Together, Wheel, Rin, and Surf Excel contributed 25% to Shakti’s turnover in 2005.viii

P&G’S ENTRY IN INDIA

P&G India came into existence in 1985 when Richardson Hindustan Ltd., became the affiliate of Procter & Gamble,

USA for its Vicks range of products. After the liberalization of Indian economy in 1991, P&G set up its subsidiary

in India and launched its compact detergent brand, Ariel. Compact detergents provided better cleaning performance

while reducing the amount of detergent needed per wash. To compete with Ariel, HUL launched Surf Ultra with the

campaign “Daag dhoondte rah jaoge” in 1992. Later in 1994, HUL launched Rin detergent powder to compete in

the mid-segment. P&G signed an agreement with Godrej to manufacture and market detergents, soaps, and other

consumer products in India. P&G acquired 51% stake in the joint venture “P&G Godrej” with an investment of $22

million and procured “Key” and “Trilo” detergent brands from Godrej. P&G wanted to leverage the strong sales and

distribution network of Godrej, but the alliance failed and was terminated in 1996. While soap brands such as

Cinthol and Marvel went back to Godrej, P&G retained the detergent brands Trilo, Key, and Ezee. In 1998, P&G

Procter & Gamble India: Gap in the Product Portfolio?

Page 4 of 23

sold Ezee, Trilo, and Key to Cussons India Pvt. Ltd. to focus on its flagship brand, Ariel. P&G deemed these

products not suitable to its strategic plans.

In 1999, P&G launched ‘‘Ariel Power Compact’’ and ‘‘New Ariel Front-o-mat,’’ to further bolster its presence in

the premium segment. Ariel Power Compact claimed superior stain-removing capabilities without the need for bar

soaps. It was introduced in two fragrances – wet odor (perfume given off while the clothes were washed) and dry

odor (perfume that lingered on after the clothes had been dried and ironed). Ariel Front-o-mat on the other hand, was

the only detergent specifically made for front-loading washing machines. The variant was endorsed by IFB.

LAUNCH OF TIDE IN INDIA

P&G launched Tide detergent in India in 2000. Tide was P&G’s largest global brand in its portfolio of 334 brands. It

was positioned on the platform of ‘‘outstanding whiteness’’ owing to its anti-redeposition technology.ix It also

claimed to improve the washing experience through its pleasant lemon fragrance that lingered on the clothes hours

after washing. Tide was launched in the premium segment at a price of Rs. 120 per kg and found little consumer

acceptance. The turnaround for the brand came in 2004 when P&G slashed its prices drastically and repositioned it

in the mid-price segment where it competed with Rin and gained market share steadily.x

AGGRESSIVE MARKETING BY GHARI

The FMCG sales slowed down in early 2000s owing to failed monsoons and shift of discretionary income to

electronic goods, automobile, etc. Low-cost players such as Ghari detergent gained market share by pricing their

products aggressively and offering higher trade discounts and consumer promotions. Ghari kept lower net profit

margin of 9% when the industry average was 12–13%. Also, the company worked on a shoestring advertising and

marketing budget. Its advertising budget was less than 5% when most national brands spent 13–15% of their

revenues.xi Ghari focused on its home market – Uttar Pradesh, a northern state to begin with. Uttar Pradesh, with a

population of 167 million, accounted for over 12% of the country’s FMCG sales. Thus, of the 3,000 Ghari dealers in

the country, 900 were in Uttar Pradesh and 9 of the company’s 18 manufacturing units were in Uttar Pradesh. Once

the home base was secured, it spread out to other states. In 2010, about 60% of Ghari’s sales was derived from Uttar

Pradesh, Madhya Pradesh, and Maharashtra.

LAUNCH OF SURF EXCEL BLUE AND SURF EXCEL QUICK WASH

In late 1990s, HUL re-launched Surf Ultra as Surf Excel. The core positioning of stain removal was retained. In

early-2000s, Surf Excel which had a 65% market-share in the premium segment against 30% of Ariel started

stagnating. HUL upgraded the quality of Surf and Wheel and reduced the price of Surf Excel by 15%. HUL re–

staged Surf to Surf Excel Blue to unite the franchise and strengthen the brand equity of Surf Excel.xii Surf Excel

Blue was positioned as a color care variant that would remove stains but not fade color.xiii

In the mass market, HUL introduced Wheel Active, a white powder. Wheel Active’s campaign “liberation from

hard-work” emphasized the proposition of cleaning with ‘‘less effort.’’ In 2003, HUL launched “Surf Excel Quick

Wash” which used special formulations for low foam that reduced water consumption and time taken for rinsing by

50%. The value proposition was low scrub, low rinse, and quick to wash, which was sharply against the perception

that less foam meant a not–so–good detergent. HLL thus made a statement on how sustainability and business could

go hand–in-hand. Henry King, Science and Technology leader for sustainability at Unilever said:

Detergent business relies on access to vast amounts of water – not so much at Unilever’s own

facilities, but upstream and downstream in the product life-cycle as farmers grow crops and

customers wash their clothes. We looked for regions where there was water stress and tried how

our products could ease the strain.xiv

PRICE WARS – THE CLASH OF GIANTS

In 2003, P&G initiated price-cuts to grab higher market share; HUL followed suit (Table 2). Sanjay Behl,

Marketing Manager, HLL said:

Procter & Gamble India: Gap in the Product Portfolio?

Page 5 of 23

We are lowering the price barriers for our consumers so that they can have access to our high

quality products.

Shantanu Khosla, P&G’s Country Manager remarked:

Most families that use low-priced detergents in India use Ariel and Tide sachets for expensive

clothes. The price reduction on sachets should encourage more consumers to use them for all

clothes and definitely more often.xv

The price war resulted in lowering the profitability of the two giants.

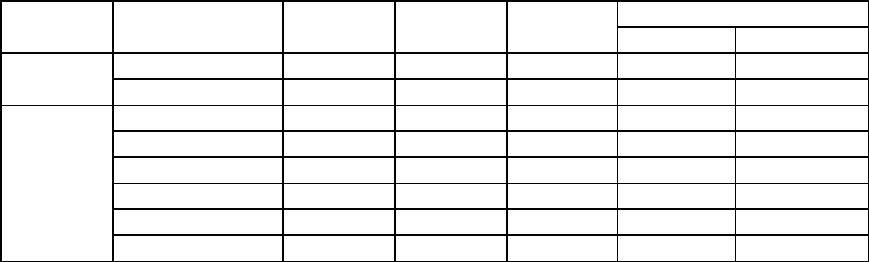

Table 2 Revised pricing structure of P&G and HUL brands

Company

Brand

Original Price

(Per kg)

Revised Price

(Per kg)

Change (%)

Category Realignment

From

To

P&G

Ariel

135

99

–27

Premium

Premium

Tide

85

46

–46

Mid Priced

Popular

HUL

Surf Excel

140

100

–29

Premium

Premium

Surf_Excel Blue

90

67

–26

Mid Priced

Mid Priced

Rin Supreme

80

60

0

Mid Priced

Mid Priced

Rin Shakti

40

40

0

Popular

Popular

Wheel Active

26

26

0

Sub Popular

Sub Popular

Wheel Green

20

20

0

Sub Popular

Sub Popular

Source: http://www.pg-india.com/hp/history.htm

However, caught off-guard by the price cuts was the Rin franchise. HUL discontinued Rin Supreme powder. Surf

Excel Blue was sold at a 50% premium to Tide. Rin Shakti, priced in the same band as Tide, was perceived to be

relatively inferior (see Exhibit 6 for variants and their prices). HUL responded by improving the formulation and

packaging of Rin Shakti and re-launched it as Rin Advanced.xvi This marked the transformation from the “Uski

saari, meri saari se safed kaise” campaign in the 90s to “Safedi ka Shehanshah” with Amitabh Bachchan. The brand

improved its market share.

P&G took this opportunity to launch a bar variant of its Tide detergent in 2004 at a price similar to HUL’s Rin

Supreme.xvii Its launch coincided with the withdrawal of Ariel detergent bar. Chester Twigg, Director, Sales &

Marketing, P&G India remarked:

95% consumers in India use a combination of powder and bar. Instead of trying to change the

consumer’s choice, we thought we must leverage on their existing preference.xviii

The new product was unique compared to the available detergent bars for it had green speckles called “Whiteons,” a

P&G proprietary technology, which helped in whitening the fabric. Its technology ensured that it did not melt too

much in water but was easy to apply. It had a lemony and refreshing fragrance that remained on the clothes even

hours after the wash.xix The price cut strategy helped P&G record an increase in market share.xx

CHANGING MARKET DYNAMICS

Nirma which was the second largest brand after Wheel in the mid-2000s was caught in the crossfire between HUL

and P&G. Nirma’s market share slipped from 16% to 14%. The reduction in the prices had reduced the premium

nature of the compact detergent market. Surf, Ariel, and Tide were viewed as more affordable and this encouraged

consumers to switch over from mass brands to premium brands. Nirma launched an offensive by offering big

discounts. Reduced profitability made Nirma look for alternative growth areas and reduce its dependence on

detergents.xxi

Procter & Gamble India: Gap in the Product Portfolio?

Page 6 of 23

To strengthen and deepen its premium segment positioning, Surf Excel launched Surf Excel Matic in 2005. It aimed

at addressing the needs of the fast growing washing machine consumers for in-machine stain removal. Surf Excel

Top Load and Front Load were the two variants under Surf Excel Matic. In the same year, when every detergent

brand was vying for share with the clichéd anti-stain campaign, Surf Excel broke the clutter by adopting stains. The

brand philosophy behind this positioning was that when children go out and play and get dirty, they do not just

collect stains, they experience life, make friends, share with each other, and learn from each other. Dirt should not

act as an obstacle towards the learning experience.xxii The brand struck a chord with the consumers with its ‘‘dirt is

good’’ positioning. In 2006, HUL graduated from Rin Supreme bar to Surf Excel bar. The product brought together

the stain removal properties of Surf Excel and whitening properties of Rin Supreme in the same bar.

HUL recognized the importance of burgeoning mid-price segment (termed “Aspirers”) and acknowledged that its

future strategies would aim to tap into this segment better (Figure 1).

Figure 1 Changing customer base in Indian market

2003 180 million households 2013 231 million households

Source: NCAER

In line with its above strategy, HUL strengthened the Rin brand. In 2007, Rin introduced the first ever “shades of

whiteness” in the laundry category, offering proof of whiteness to consumers with the “Kya Saboot Hai” campaign

with Boman Irani. In 2008, Rin was re–launched and provided “Dugni Safedi, Dugni Chamak” as compared to

ordinary powders. Rin Matic, a specialist washing machine powder, was launched in 2008.xxiii

To strengthen its product offerings in the mid-segment, P&G launched Tide Naturals in 2009. It was positioned as

providing relief from irritation of hands caused by lower quality detergents. Tide Naturals promised superior

cleaning and whitening and good fragrance. It was priced aggressively at Rs. 50 per kg and was about 30% cheaper

than Tide. The advertisement of Tide Naturals had visuals of lemon and sandalwood. xxiv The new variant received

good response from consumers. To combat Tide Naturals, HUL brought down the price of Rin from Rs. 70 to Rs.

50.xxv HUL also took Tide Naturals to the court regarding its advertisement. It contended that Tide Naturals was

giving the impression to consumers that it contained natural ingredients such as lemon and sandalwood. Responding

to the court, P&G admitted that Tide Naturals did not have any natural ingredients; rather it had synthetic

compounds that imparted the goodness and freshness of sandalwood and lemon.xxvi Sumeet Vohra, Director-

Marketing, P&G said:

The shape of India is going to change from pyramid

to a diamond.

3

Rich

11

46

Aspirers

124

131

Strivers

96

Procter & Gamble India: Gap in the Product Portfolio?

Page 7 of 23

The use of generic word naturals does not communicate the presence of natural ingredients. It is a

nomenclature the consumer responds to.xxvii

In 2010, HUL unleashed a high-decibel campaign for its Rin brand explicitly comparing it with Tide and claiming

that Rin gave better whiteness.

RE-EXAMINING THE PRODUCT MIX OF P&G?

After making successful inroads into the mid-segment with Tide and Tide Naturals, P&G wondered if it should

launch a brand for the economy segment too. Tide Naturals was priced 50% higher than Wheel. Should P&G launch

another brand to compete with Wheel and fill the void at the bottom of the pyramid? Should P&G launch more

variants for its existing brands? Are the variants clearly positioned in terms of the promised benefits (see Exhibits 7

& 8 for ads and storyboards of brands)? Research conducted by P&G on Indian consumers indicated that fragrance