Carolina Cobos – June 2016

Page 1 of 7

Moody’s Credit Ratings and the Subprime Mortgage Meltdown

1.a. Case Summary

This case discussed the causes of the 2008 financial crisis pointing to the critical role played by

Moody’s corporation and other credit rating agencies. Founded in 1909, Moody’s began rating

bonds for businesses, specifically analyzing the investment’s return. Over time, Moody’s core

business model changed. In the 2000s, they began rating the creditworthiness of the mortgage-

backed securities. These instruments are a mixture of subprime and low risk mortgage notes, and

carry higher fees and points of interest than traditional corporate bonds. The sale of these bonds

led to an increase in the amount of money dumped into pensions and hedge funds. As a result,

demand for these securities increased as mortgage lenders were pressured into lending to low–

qualified buyers housing. Over time, owners were failing in their loans and the real estate market

in the U.S.A collapsed, leading to foreclosures, mortgages delinquencies, and the devaluation of

housing related securities.

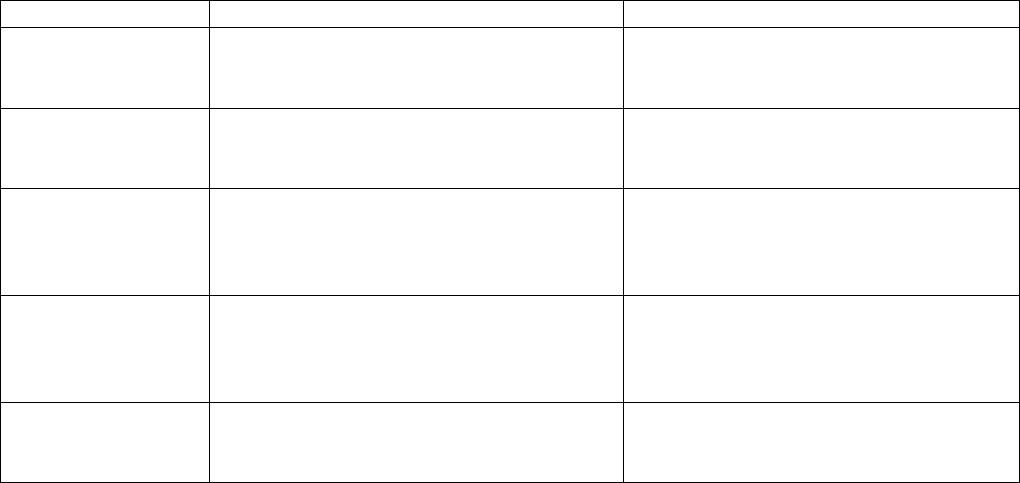

1.b. Interest, concerns and power of the key stakeholders.

Stakeholder

Interests

Power

Borrowers

–Find better rates/deals

-Be able to pay debts

-Boycotting

-Stop making payments

-Legal power: Suit for damages

Lenders /Investment

banks

-Generate loan volume

-Want high rates

-Economic power

-Refuse credits

-Control market

Credit rating

agencies/competitors

-Collect debts and Interests

-Receive payments

-Win the business and maintain market share

-Maintaining rating quality

-Can place the financial system at risk

-Informational power: access to valuable data

Investors

-Receive accurate information from credit rating

agencies

-Receive satisfactory return of investment

–Don’t having rating downgrades

-Purchasing from competitors

-Legal power: Suit for damages

Government

-Promote economic development

-Promote social improvements

-Allowing or disallowing commercial activity

Adopting regulations and laws

-Political power: legislations, regulations,

Carolina Cobos – June 2016

lawsuits

Top Managers

-Generate more revenue for their companies

-Receive high bonuses/rewards

-Manipulate or change the business strategies

1) Borrowers considered “high risk”, were taking advantage of the new opportunity to have loans

with bad credit. They have the power to stop paying the fees and create economic disruptions in

lenders. Also, those customers affected such as the retired community have the power the suit for

damages.

2) Lenders originated mortgages to customers with doubtful ability to repay the loans.

Investment banks purchased securities based on the mortgages, whose value was dependent on