1

Blackhole with stocks (industrial company)

James Thriftless was the head of financial control at the industrial company Blackhole, a small

company that manufactures a single part used in the automobile industry, and had held this

position ever since the company was formed. He had always had the full confidence of the

company’s founder and manager Mr Blackhole. When the business was set up, it was the first to

use an ultra-durable polymer for the product it made: when blended with rubber, this made the

part more hardwearing. In fact he called his product the Stamina, and for a long time it was the

only one of its kind on this market. But in recent years other competitors had seized on the same

manufacturing process, slowly eroding Blackhole’s sales and profits.

On November 15, year N, Mr Blackhole announced that his son Harpagon would succeed him as

chairman of the company from January 1 the following year. Harpagon, an engineer by training,

had rounded off his education with an MBA from Boston and then spent several years with a

large strategy consulting firm. During their discussions, Mr Blackhole had warned his son about

the company’s commercial and strategic difficulties; however, Mr Blackhole showed little

interest in financial matters and James Thriftless was given great autonomy in such areas. It was

true that for a long time, the company’s healthy profits had spared Mr Blackhole any cash flow

difficulties.

When Harpagon joined the company on December 16, year N, he looked at the internal

management reports and observed that Blackhole had no cash budget, and financial planning was

rather succinct. Harpagon expressed his concern about the situation to James Thriftless. James

replied that Blackhole was managed under a set of decision rules that worked perfectly well, and

that as a result no cash budget was necessary: when the financial position became tight, Mr

Blackhole transferred money from his account to the company’s account. Harpagon reacted

immediately and firmly: “My father is a millionaire but I am not.”

When Harpagon asked James to introduce a budget for the coming year without delay, James

looked uncomfortable; he said he knew little about budget management and that he would

certainly need to hire an assistant to establish a budget.

Harpagon then decided to call his old friend Henry Knowledge. Knowledge was working on

several major budget management projects in a consulting firm, and Harpagon knew he was

considered an expert in the field for small and medium businesses. Fortunately for Harpagon,

Knowledge was not too busy and he came round to Blackhole that very week.

He spent two days in the company’s offices examining the accounts, memos and all available

reports. On Friday morning, Harpagon found the following note on his desk:

“Dear Harpagon,

I had to leave last night for Pittsburgh. During the two days I’ve spent at your company, I’ve

noted the following:

1. You have no budget or control system.

2. James Thriftless is a good accountant.

2

3. Thriftless knows nothing about basic management rules, and is not interested in production,

strategy or sales.

I’ll be back on Monday morning to talk things over with you. I recommend that you contact

Penny Pincher, a financial controller I know. I’ve left her contact details with your secretary.

Regards, Henry.”

Harpagon was perplexed by this note and decided to find out who Penny Pincher was. He

telephoned her. She explained that she had a MS (Master’s degree) in management and had

worked for several years in a small company where she had set up the entire management control

system. It was all running smoothly now and she was in fact planning to look for another job.

Henry Knowledge arrived on Monday morning as promised. Swift as ever, Henry told his friend:

“You must hire Penny as your financial manager, you’re heading for disaster. What’s more, I

think she can come and help straight away. James has got to go, he’s too expensive for what he

does.” And that very afternoon, James was dismissed with an indemnity. The same evening,

Penny agreed to work for Harpagon. She could start next Monday after negotiations with her

current employer.

When she arrived the following week, Penny set to work without delay. Constructing a budget

from scratch was not easy, but that did not worry Penny unduly.

She began by an interview with Mr Blackhole senior, who was still working in the company. He

explained the company’s past and present context: the market for the Stamina product, the main

competitors and the main customers. She collected further information by reading about the

automobile market and the automotive companies, which were Blackhole customers. Then she

talked to Harpagon, who explained the strategy he intended to adopt: in his opinion, the product

was a good one but not sufficiently differentiated from competitors’ products. He was

considering two areas for action: production cost must be reduced in order to restore margins, and

meanwhile, other outlets must be found to boost sales. This type of part could, for example, be

used in the railway or aeronautic industries, but these markets had never been approached.

For the time being, Harpagon gave Penny a forecast for the number of parts that could reasonably

be sold in the coming month:

Actual sales: Estimated sales

October N: 1,500 units December N: 1,800 units

November N: 2,300 units January N+1: 2,000 units

February N+1: 2,200 units

March N+1: 1,900 units

April N+1: 2,100 units

She then visited the head of production to find out about the manufacturing process. In fact, the

company’s manufacturing process for its only product, the Stamina, was particularly simple. It

was produced from a unique raw material (a polymer/rubber blend) supplied to the production

line every morning from a safety stock. The various operations involved in production took place

during the day, and at the end of the day all the finished parts were stored in a warehouse. Since

parts were finished by the end of the day, there were never any products in process overnight.

With his excellent knowledge of the workshop, the head of production was able to tell her the

variable cost of different items and fixed workshop costs per product unit:

3

Direct variable costs

Materials costs per unit 0.75

Direct labour costs per unit 1.25

Total 2.00

Variable overheads

Indirect labour costs per unit 0.20

Energy costs per unit 0.10

Other indirect costs per unit 0.50

Total 0.80

Fixed costs (weekly amounts)

Employees 100

Procurement overhead 300

Electricity 75

Factory insurance 125

Other overheads 110

Total 710

Penny decided to check this information against the accounts, which were up to date at the end of

November. In the general accounts, she managed to identify the costs related to the workshop.

Identifying the variable and fixed costs, she was able to compare total variable costs to variable

costs for the units produced over the period and see that the estimates for unit costs were

accurate. She also found the amount of fixed costs as stated by the head of production.

She noted that sales and management costs amounted to approximately €781 per week. This

amount comprised the following:

Payroll (including benefits in kind and payroll taxes): 400

Rental 200

Depreciation of office equipment 100

Other functional services 81

Total 781

Penny returned to see Harpagon with these initial figures, to discuss the assumptions to be

applied in the budget. Together they defined a certain number of general principles:

1. The estimations for variable production costs were certainly accurate; given the objective

of reducing these costs, but taking a cautious approach for the first quarter, it was decided

to leave them as they were.

2. Fixed production costs were certainly €710; however, this amount did not include

estimated depreciation; therefore, fixed production costs should be increased by the

amount of depreciation; the value of the factory and machinery and equipment could

reasonably be estimated at €70,000; the machinery and equipment probably had a

recoverable value of €25,000; depreciation was to be calculated monthly over a 5–year

useful life, on a straight-line basis. All these expenses were part of the production cost of

goods sold.

3. As the figures supplied for fixed production costs, distribution costs and management

costs were for one week, it was decided to apply a coefficient of 4.5 to estimate the

monthly amount.

4

4. To take into account the new strategic orientation, Harpagon asked Penny to budget € 900

in expenses per month to develop sales (direct marketing to potential customers).

5. It was decided that the sale price would remain fixed at €7 per unit for the first quarter;

sales commissions were set at 10% of sales revenues.

Lastly, Penny asked Harpagon what he wished to do with the shareholder’s current account. He

told her his father was going to recover his money (€30,000). Harpagon decided to pay €10,000

into this current account, but wished to withdraw €1,400 per month from the company’s accounts

for his own requirements.

Penny gathered some more information she was going to need:

• The time schedule of invoice settlement by customers was as follows:

o During the month of sale 30%

o Month following the month of sale 40%

o Second month following the month of sale 20%

o Third month following the month of sale 10%

• Materials purchases were payable in 30 days. Consequently, settlements were made in the

month after the month of purchase. According to forecasts, 1,700 units of raw materials

were to be purchased during December N.

• All other expenses (payroll, overheads, commission, rental, etc) were paid in the month of

purchase.

• The stock of raw materials had been estimated at 800 units at December 31 N, and there

were 750 units of finished products.

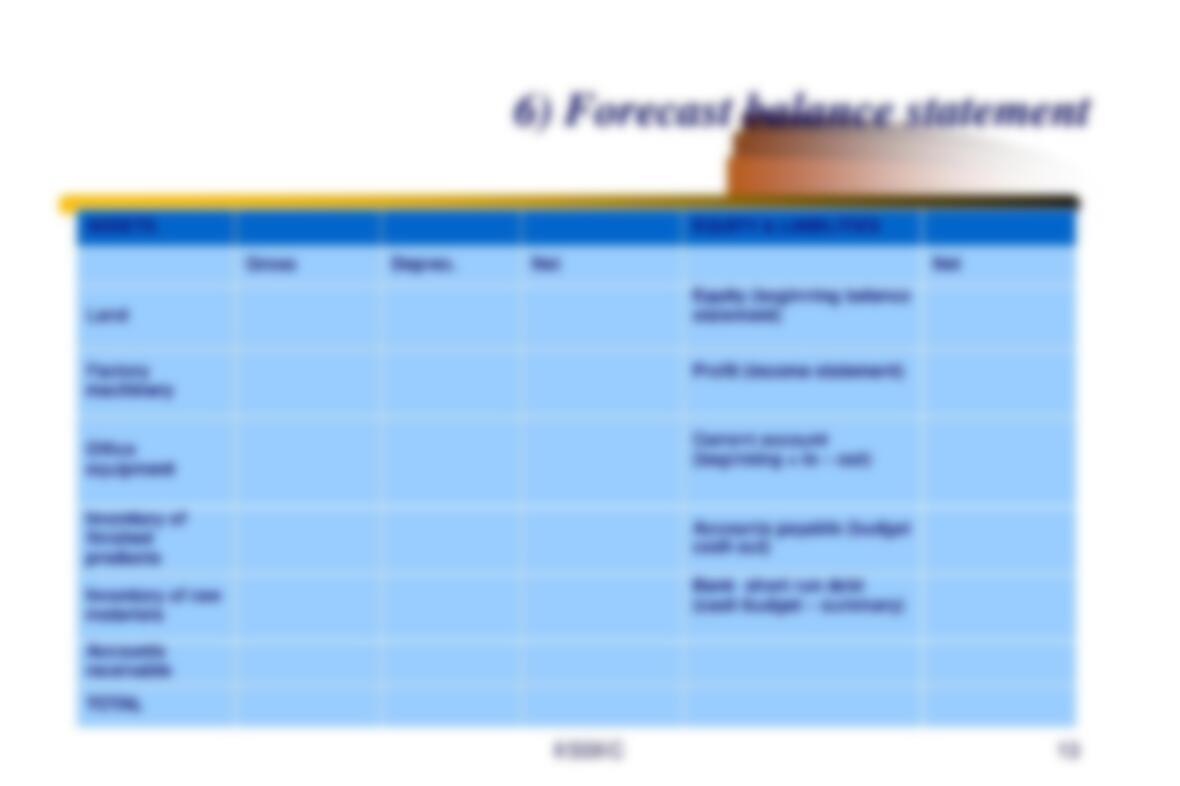

Finally, Penny drew up a projected balance sheet at January 1, N+1 based on the documents

analysed and the accounting position at the end of November:

Assets

Equity and Liabilities

Land

Factory machinery

Office equipment

Stock of finished products (€4.72

per unit)

Stock of raw materials

Accounts receivable

Cash

5000

70000

13122

3540

600

14700

10000

Share capital

Current accounts

Accounts payable

85687

30000

1275

TOTAL

116962

TOTAL

116962

Penny got down to work. She prepared a forecast budget for the first quarter (projected income

statement, cash budget and projected balance sheet at March 31, N+1) in the following stages:

5

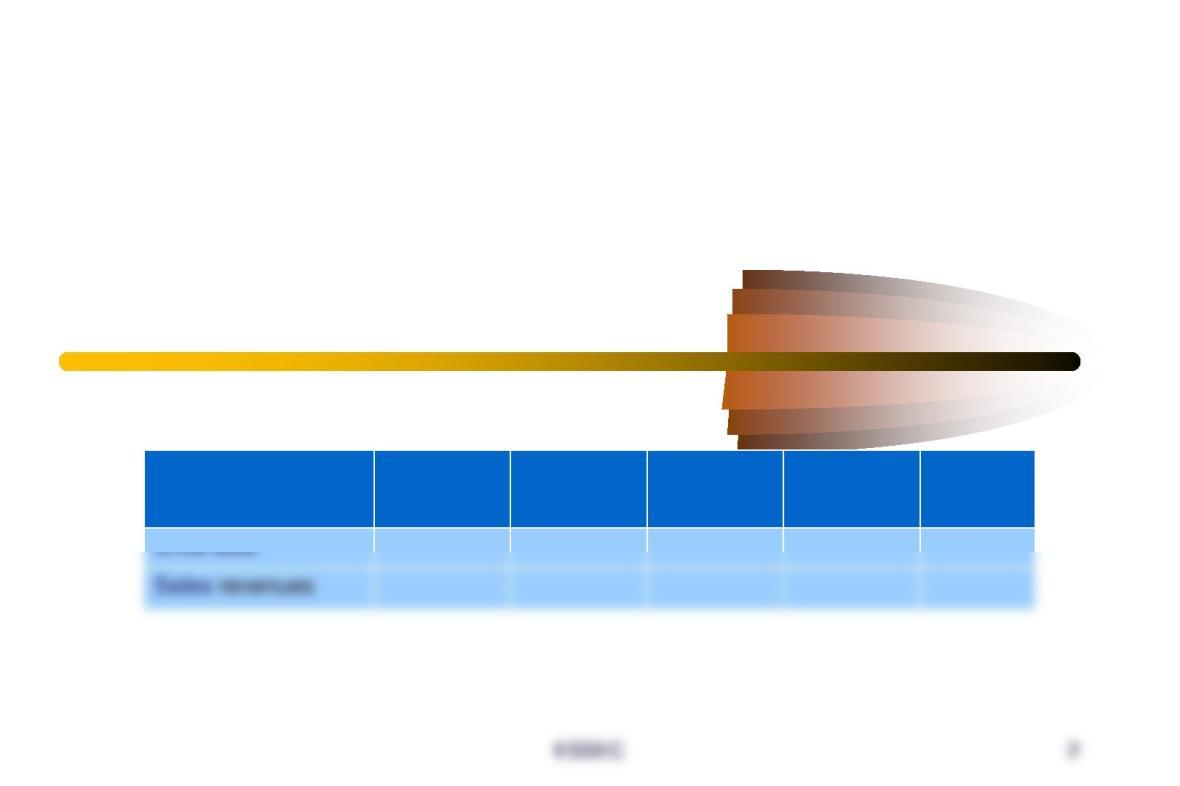

1. Sales budget

The first stage was to establish the sales budget in monthly figures and for the first quarter. To do

so, she completed the table attached in the appendix.

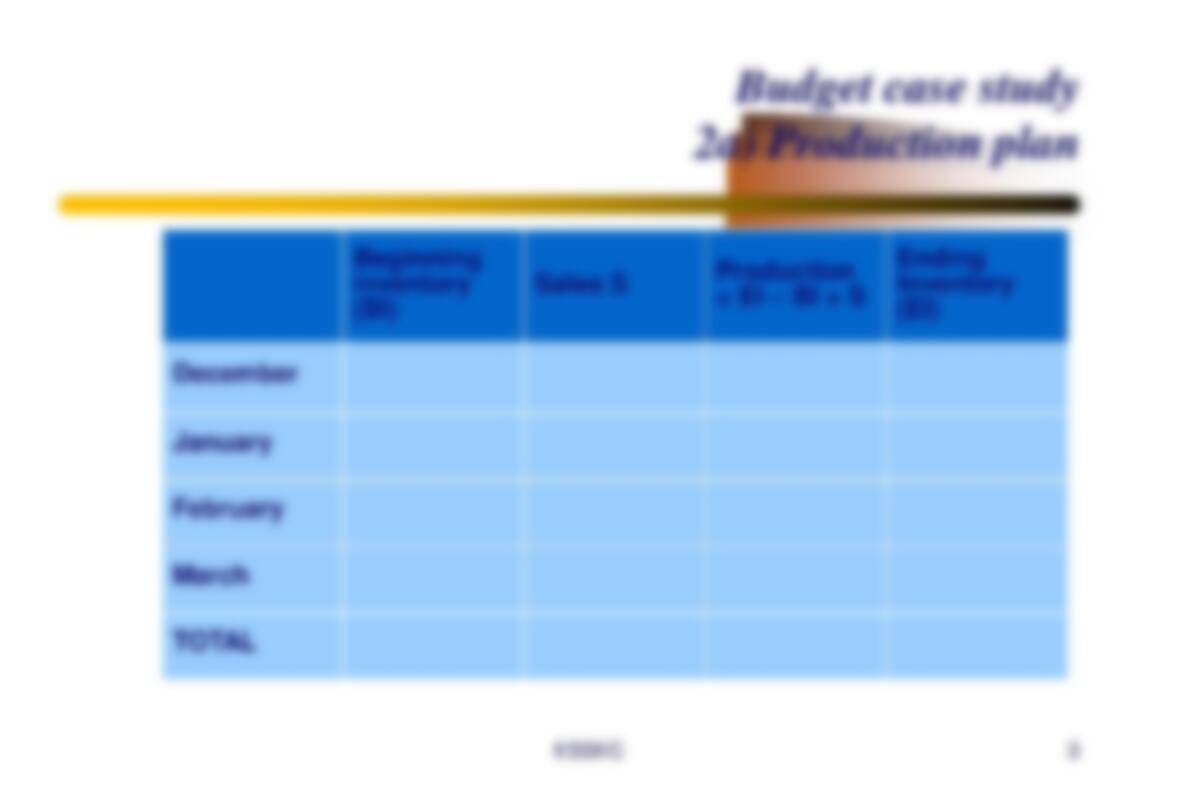

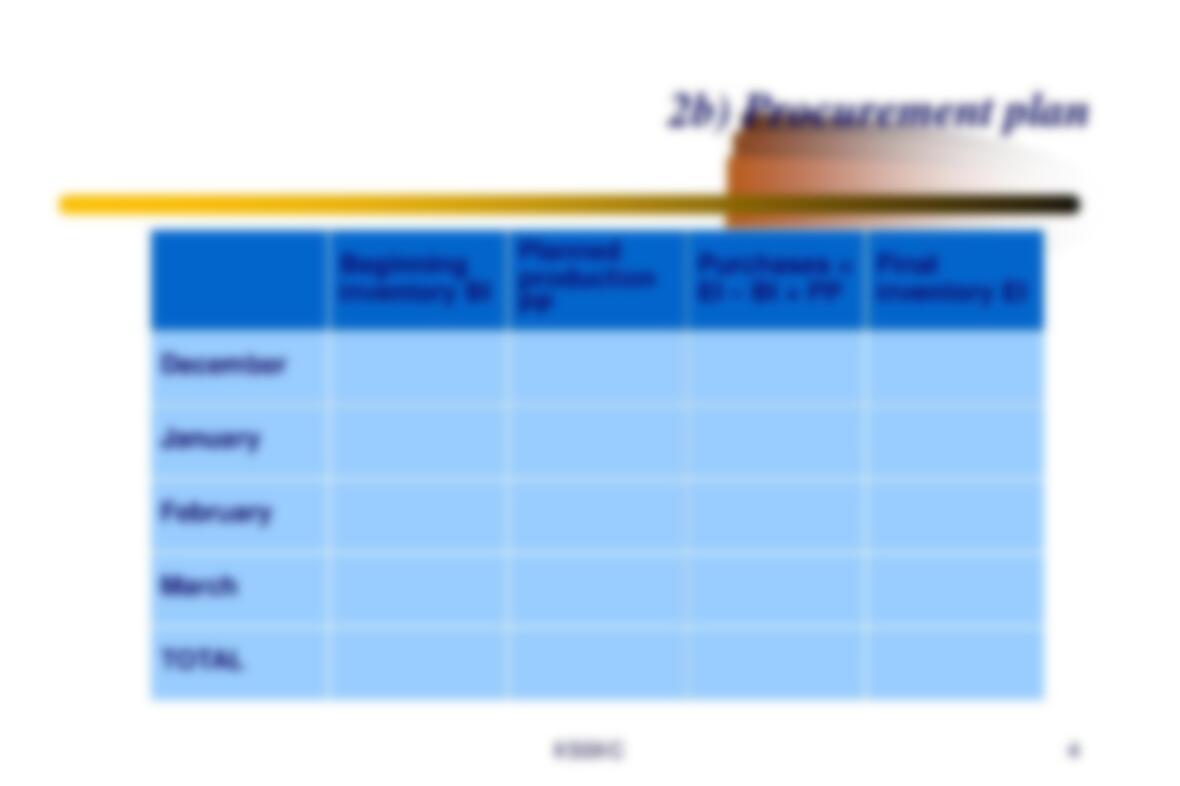

2. Production budget

The second important stage in Penny’s work was to establish a production plan and a materials

procurement plan (tables in the appendix) for the first quarter of N+1.

As no production or stock plans existed, the head of production supplied some operating rules

based on experience acquired in the company:

(1) production for a given month should be scheduled such that the stock of finished products at

the end of the month is equal to half of the expected sales level for the following month;

(2) materials purchases should be scheduled such that the company has enough raw materials

available to make 700 products. Consequently, the minimum month–end stock must contain 700

units in raw materials.

Based on these production plans, Penny’s next task was to calculate the production cost that

would then be used to establish the projected income statement. To do so, she completed the table

attached in the appendix.

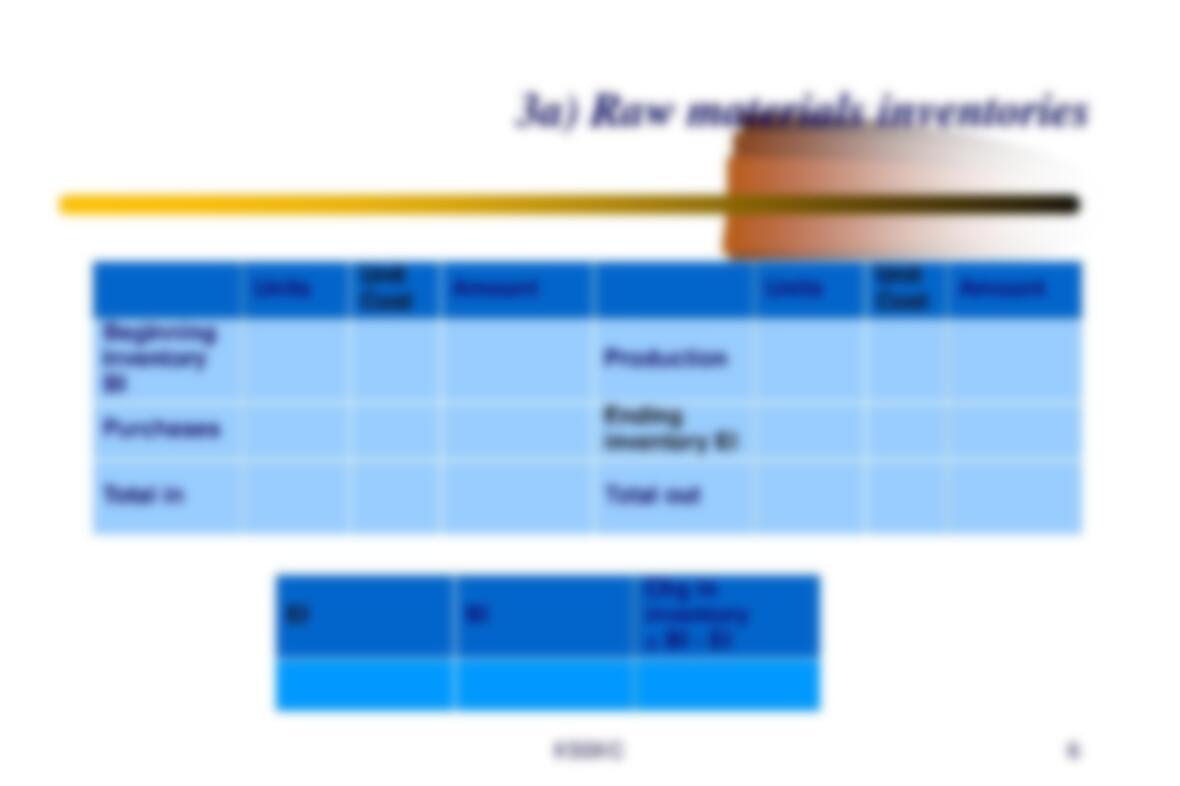

3. Stock accounts

To complete the income statement, Penny next had to establish the accounts for the raw materials

and finished product stocks. She used the weighted average cost per unit method already used in

the company (see table in appendix).

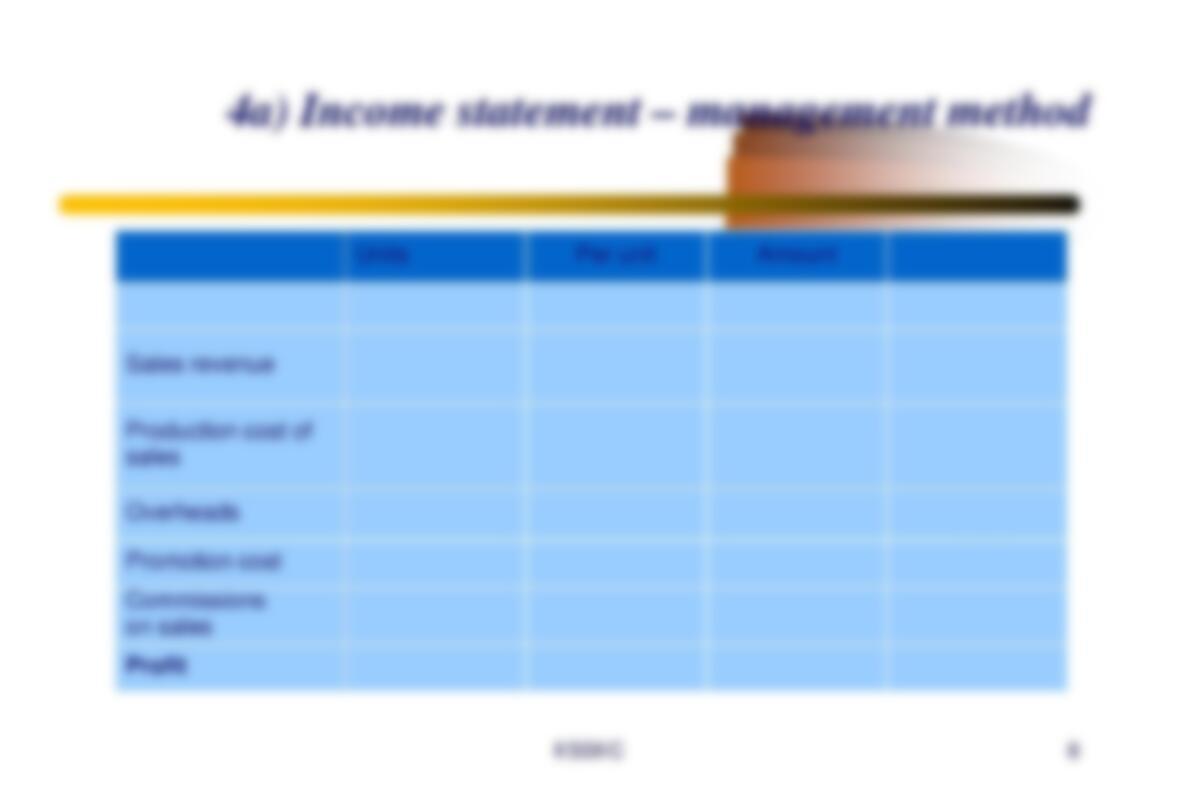

4. Projected income statement

Based on the previous calculations, Penny was able to draw up a projected income statement for

the first quarter of N (format supplied in appendix).

5. Cash budget

After constructing the income statement, Penny decided to turn her attention to the cash position.

She prepared the monthly cash forecasts for the first quarter by filling in the table shown in the

appendix.

6. Projected balance sheet

The final stage in the budget process applied by Penny was the establishment of the projected

balance sheet at March 31, N+1 (format in appendix).

7. Finally, based on all the budget statements drawn up, Penny decided to issue a short summary

memo on the principal components of the company’s financial position, and some

recommendations for Harpagon.

ESSEC 1

Management control and business

supervision

Session 2: forecast budget and monitoring process,

links with strategy

Budget case –tables to complete

1) Sales budget

January February March TOTAL Unit

selling

price