Page 1 of 6

A Comprehensive Problem of all variances

The Spring Mint Company, a manufacturer of chewing gum, uses a standard cost system. Standard product

and cost specifications for 1,000 lbs. of chewing gum are as follows:

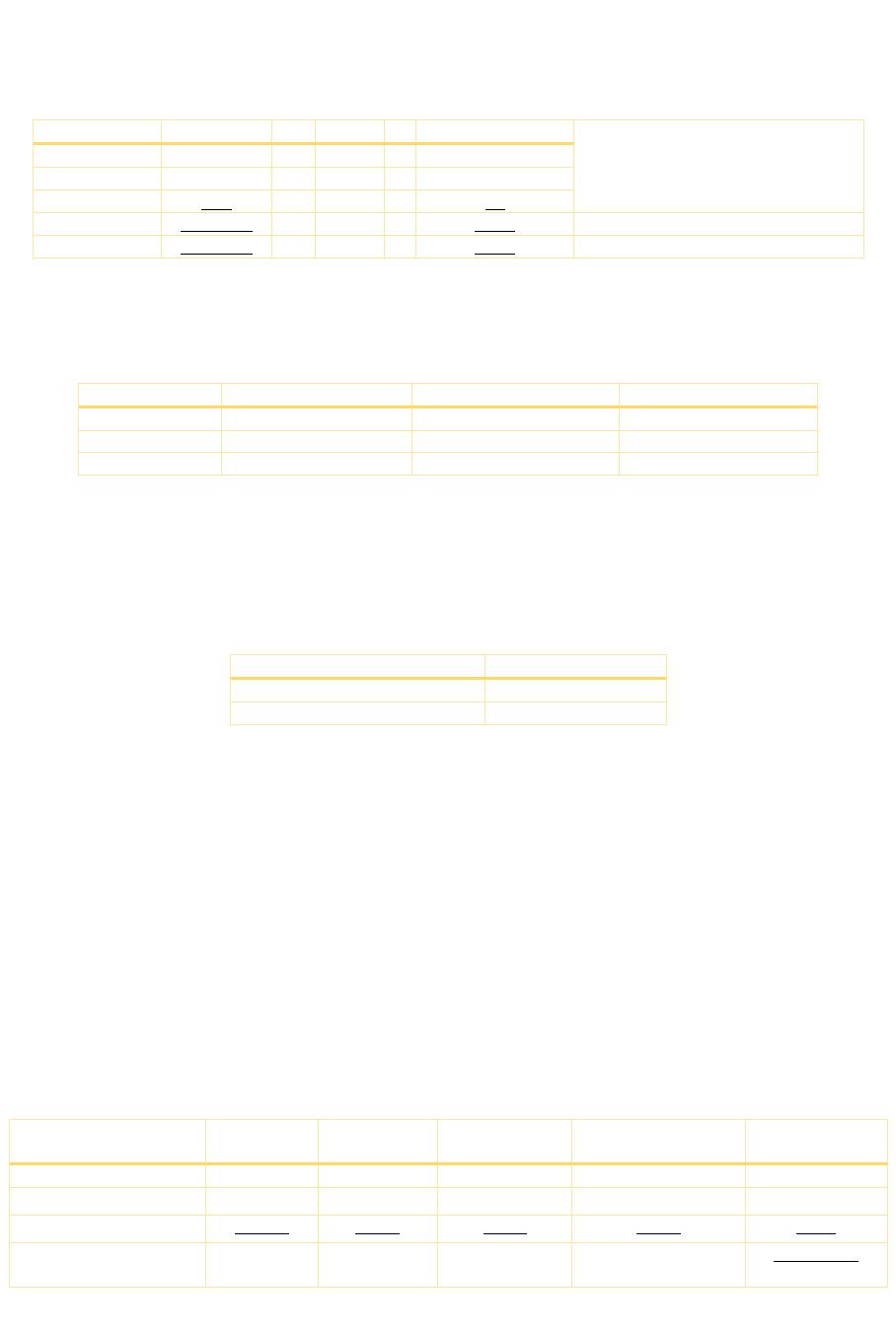

Quantity

×

Price

=

Cost

Gum ba

se

800

$0.25

$200

Corn syrup

200

$0.40

80

Sugar

200

$0.10

20

Input

1,200 lbs

$300

$300 / 1,200 lbs = $0.25 per lb.

*

Output

1,000 lbs

$300

$300 / 1,000 lbs = $0.30 per lb.

*

*Weighted average.

The production of 1,000 lbs. of chewing gum required 1,200 lbs of raw materials. Hence the yield is 1,000 lbs

/ 1,200lbs. or 5/6 of input. Materials records indicate.

Materials

Beginning Inventory

Purchases in January

Ending Inventory

Gum bas

e

10,000 lbs

162,000 lbs@ 0.24

15,000 lbs

Corn Syrup

12,000 lbs

30,000 lbs

@ 0.42

4,000 lbs

Sugar

15,000 lbs

32,000 lbs

@ 0.11

11,000 lbs

To convert 1,200 lbs. of raw materials into 1,000 lbs of finished product required 20 hours at $6.00 per hour

or $0.12 per lbs. of finished product. Actual direct labor hours and cost for January are 3,800 hours at $23,104.

Factory overhead is applied on a direct labor hour basis at a rate of $5 per hour ($3 fixed, $2 variable), or $ 0.1

per lb. of finished product. Normal overhead is $20,000 with 4,000 direct labor hours. Actual overhead for the

month is $22,000, Actual finished production for January is 200,000 lbs.

The standard cost per pound of finished chewing gum is:

Materials

$0.30 per lb.

Labor

$0.12 per

lb.

Factory overhead

$0.10 per lb

.

Required:

Calculate:

1. Materials price, mix, quantity and yield variance.

2. Labor rate, efficiency, and yield variance.

3. Overhead yield variance using two and three variance methods.

Solution to the Comprehensive Problem

Calculation of Materials Variance:

The materials variances for January consists of price variance, mix variance, yield variance, and quantity

variance.

Materials Price Variance:

The company calculates the materials price variance using the procedure explained on “direct materials price

variance” page and recognizes variances when materials are purchased.

Materials

Quantity

Actual Price

Standard

Price

Unit Price

Variance

Price variance

Gum base

$1

62,000

$0.24

$0.25

$(0.01)

)

1,620

$(

Corn syrup

30,000

$0.42

$0.40

$0.02

$600

Sugar

32,000

$0.11

$0.10

$0.01

$320

M

aterials price

variance

$(700) fav.

Materials Mix Variance:

The materials mix variance results from combining materials in a ratio different from the standard materials

specifications. It is computed as follows:

Actual quantities at individual standard materials costs:

Gum base 157,000 @ $0.25

$39,250

Corn syrup 38,000 @ $0.40

$15,200

Sugar 36,000 @ $0.10

$3,6

00

Actual quantity at weighted average of standard materials cost

input 231,000 lbs × $0.25

$57,750

Materials mix variance (unfavorable)

$300U

Materials Yield Variance:

Material yield variance is computed as follows:

Act

ual quantity at weighted average of standard materials cost input 231,000 lbs ×

$0.25

$57,750

Actual

output

quantity at standard materials cost (200,000 lbs × $0.30)

$60,000

Material yield variance (Favorable)

$(2,250)F

F = Favorable

U = Unfavorable

The yield variance occurred because the actual production of 200,000 lbs. exceeded the expected output of

192,500 lbs. (5/6 of 231,000) by 7,500 lbs. The yield difference multiplied by the standard weighted materials

cost of $0.30 per output pound equals the favorable yield variance of $2,250.

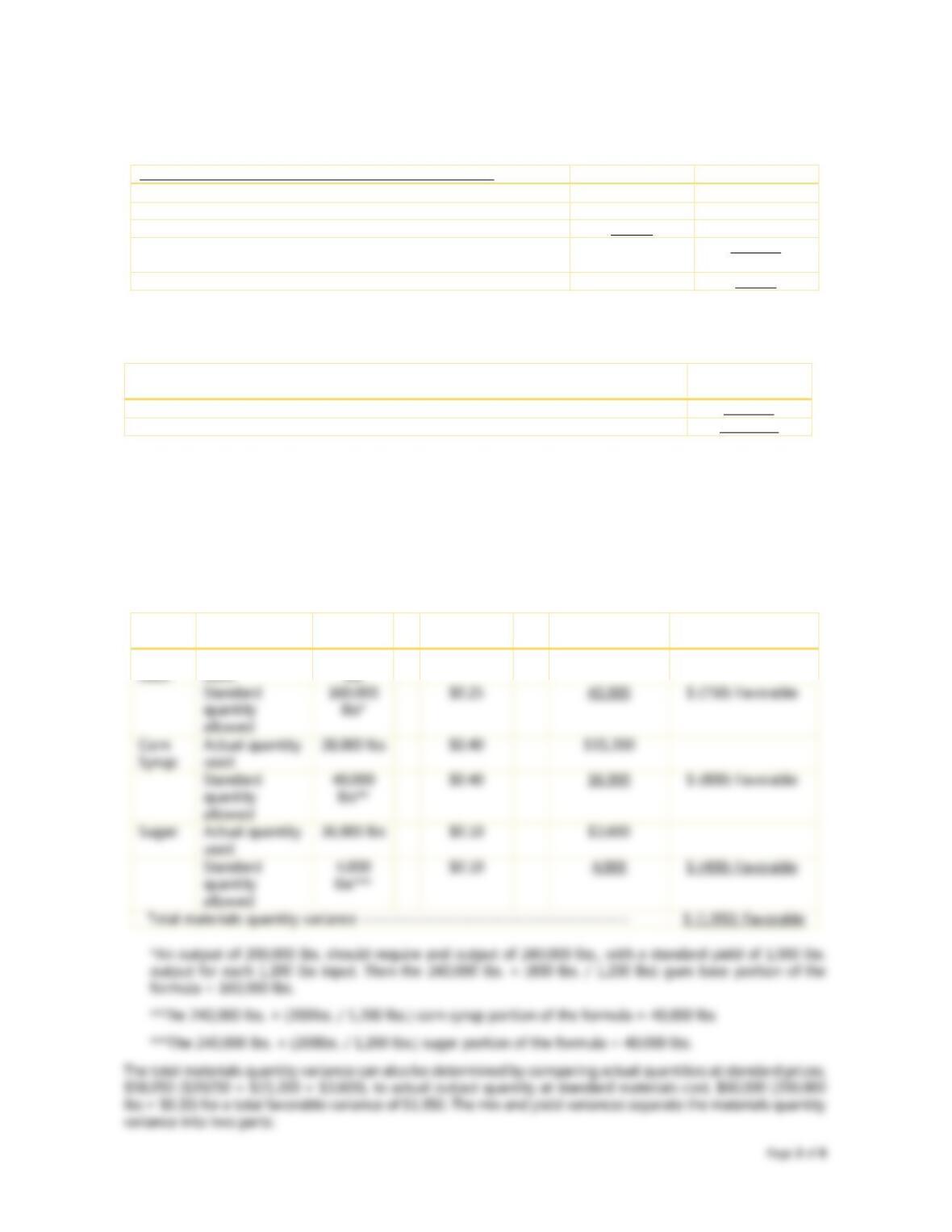

The materials quantity variance can be calculated for each item as follows:

Unit

×

Standard

unit cost

=

Amount

Materials quantity

variance

Gum

Actual quantity

157,000

$0.25

$39,250

Standard

160,000

$0.25

40,000

$ (750) Favorable

Corn

Actual quantity

38,000 lbs

$0.40

$15,200

Standard

40,000

$0.40

16,000

$ (800) Favorable

Sugar:

Actual quantity

36,000 lbs

$0.10

$3,600

Standard

4,000

$0.10

4,000

$ (400) Favorable

Total materials

quantity variance

$ (1,950) Favorable