Copyright Reserved

No. of Pages – 09

No. of Questions – 06

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

CA PROFESSIONAL (STRATEGIC LEVEL I) EXAMINATION –

DECEMBER 2013

13304 – STRATEGIC MANAGEMENT ACCOUNTING

Instructions to candidates:

(1) Time allowed:

Reading and planning : 15 minutes

Writing : 3 hours

(2) Marks : 100 marks

(3) (i) Section A – Question No. 01 is compulsory.

(ii) Section B – Answer any four (04) questions.

.

(4) Begin each answer on a separate page. Submit all workings.

(5) All answers should be in English Language, in the answer booklets provided.

____________________________________________________________________________

SECTION – A

Question No. 01

Hands Lanka (Pvt) Ltd (HL) which engaged in manufacturing fabric gloves is a group company

of Industrial Equipment Plc (IEP). Currently HL is making losses due to the competition. HL has

recently developed a specialty dipped glove (new product) and the management is contemplating

a project of a dipping plant. Total investment in machinery and installation will be Rs. 400

million out of which Rs. 300 million should be paid now and balance at the end of the first year

from now (Year 1). At the end of five years from now (expected lifetime of the project) the

residual value would be Rs. 50 million.

(2)

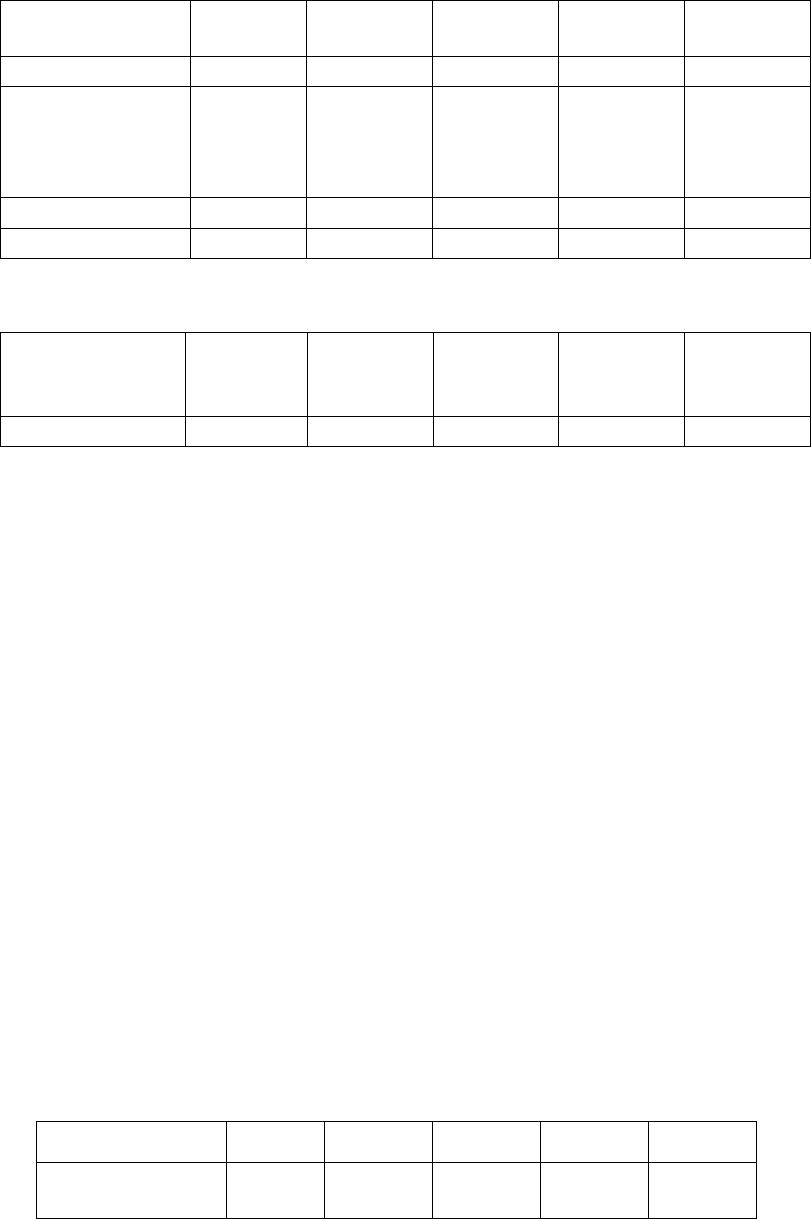

You have been given the following forecasted cash flows and profits for the project, which are

stated according to the present day costs and prices.

Year 1

(Rs. Mn)

Year 2

(Rs. Mn)

Year 3

(Rs. Mn)

Year 4

(Rs. Mn)

Year 5

(Rs. Mn)

Sales

530

580

592

525

500

Materials

Labour

Overheads

Interest

240

48

120

20

260

50

120

15

265

52

120

10

255

48

115

5

240

45

110

–

Total expenses

428

445

447

423

395

Profit before tax

102

135

145

102

105

Working capital in present day’s cost terms are:

Beginning

of year 1

(Rs. Mn)

Beginning

of year 2

(Rs. Mn)

Beginning

of year 3

(Rs. Mn)

Beginning

of year 4

(Rs. Mn)

Beginning

of year 5

(Rs. Mn)

Working capital

100

110

120

130

140

Additional information:

HL has spent Rs. 400,000 to develop this new product. A competitor of HL has already

offered Rs. 1 million for the technology of manufacturing this product.

The machinery will be installed in a rented floor area owned by IEP for a rental of Rs. 1

million per year during the project period, which cost is included in overheads. This area is

presently rented out by IEP to another subsidiary for the same amount. If the area is given to

HL, this subsidiary will rent another location from a third party, which will cost Rs. 1.5

million per year.

Selling prices of the gloves and working capital requirements are expected to increase by 5%

per year while material and labour costs are expected to increase by 10% per year. Working

capital will be released at the end of the project period.

Depreciation is charged on straight-line basis and included in the overheads. Overheads are

expected to increase by 5% every two years.

Profits are taxable at 12% and HL has a carried forward tax loss of Rs. 30 million which will

be utilised for this project subject to a maximum of 35% of assessable income. Depreciation

allowance for machine is 33 1/3% per annum. Taxes are assumed to be paid in the year in

which they are incurred.

HL’s real after tax Weighted Average Cost of Capital (WACC) is 15% per year, and nominal

after tax WACC is 20% per year. Management of IEP will accept the project if it generates a

positive net present value from the group’s viewpoint.

Discounting rates are given in the following table.

Discounting Rate

Year 1

Year 2

Year 3

Year 4

Year 5

15%

20%

0.870

0.833

0.756

0.694

0.658

0.579

0.572

0.482

0.497

0.402

You are required to :

(a) Evaluate the acceptability of the project using net present value (NPV) and the internal

rate of return (IRR) from the group’s viewpoint. (You are advised to state the amounts for

your calculation in Rupees thousands.)

Explain the treatment of the following in your appraisal :

Cost of product development incurred by HL

Annual rent cost to be paid by HL to IEP

Interest expense of HL

Discounting rate (16 marks)

(b) The engineering firm, which has quoted for the machinery installation of HL’s new

project, has given the following costs and time estimates for the installation activities.

Activity

Preceding

Activity

Cost (Rs.)

Duration

in weeks

A

B

C

D

E

F

G

–

A

A

B

D

B

C

540,000

140,000

200,000

220,000

290,000

480,000

180,000

6

1

2

3

2

3

1