Page 1 of 2

Solution to Problem- 3-2

a) Purchasing manager

The purchasing manager believes that he has performed well as he has reduced purchase costs by using a new

supplier. The material price variance is favourable by $48,000 which could be due to good negotiating and buying

skills, a reduction in quality or changing market conditions. The market for the purchase of seeds is stable, so the

price reduction is not due to market conditions.

The material usage variance is significantly adverse at $52,000 indicating that wastage has increased.

Poorer quality seed could be responsible for this. Alternatively, labour problems may have resulted in increased

wastage. However, the labour efficiency variance is favourable so this looks less likely to be the cause.

The sales price variance is also significantly adverse at $85,000 and this indicates that the price of the product had

to be reduced. Again, given that the market for the product is stable, the cause could be assumed to be quality

issues caused by the purchase of poorer quality seed. This could also explain the fall in sales resulting in an adverse

sales volume variance of $21,000.

Therefore, rather than performing well as he believes, it could be argued that the production manager is

responsible for a loss amounting to $110,000 (85,000 + 52,000 + 21,000 – 48,000).

Production director

The production director feels unfairly criticized for increasing the labour rate. His actions resulted in an adverse

labour rate variance of $15,000. This adverse variance can be justified if labour efficiency improved as a result. The

labour efficiency variance was $18,000 favourable and the labour idle time variance was also favourable by $12,000.

These variances indicate an improvement in the productivity of the workforce, even though they were working

with poorer quality materials.

The total effect of the production director’s actions in increasing the wage rate is an increase in profits of $15,000

(18,000 + 12,000 – 15,000). The improvement may however only be temporary, as workers become accustomed to

the new wage level and their efficiency and motivation drops again.

b) Standard contribution per ton:

Amount in $ Amount in $

Sales price 240

Less:

Rice seed (1.4 tons X $60) 84

Labour (2 hours X $18 X 10/9) 40

Variable overhead (2 hours X $30) 60

Marginal costs of production 184

Standard contribution 56

219

Variances:

Selling price variance

Amount in $

8,000 X $(1,800,000/8,000 – 240)

120,000 (A)

Sales volume variance Tons

Actual sales in tons 8,000

Budgeted sales

in tons

8,400

Variance in tons

400 (A)

X standard contribution per unit

× $56

22,400

(A)

Material price variance

12,000 tons should have cost (X $60) 720,000

but did cost 660,000

60,000 (F)

Material usage variance

8,000 tons should use (X 1.4) 11,200 tons

but did use 12,000 tons

Variance in tons 800 tons

X standard cost per ton × $60

48,000 (A)

Page 2 of 2

Labour rate variance

15,800 hours should cost (X

$18)

284,400

but did cost

303,360

18,960

(A)

Labour efficiency variance

8,000 tons should take (X

2 hours)

16,000 hours

but did take 15,000 hours

Variance in hours 1,000 (F)

X standard rate per hour (X $18/0.9) X $20

20,000 (F)

Idle time variance

Idle time should have been (10% x 15,800) 1,580 hours

but was (15,800 – 15,000) 800 hours

Variance in hours 780 (F)

x

standard rate per hour

x

$20

15,600

(F)

Variable overhead expenditure variance

Budgeted variable production overhead (15,000 x

$30)

450,000

Actual expenditure

480,000

30,000

(A)

Variable overhead efficiency variance

8,000 tons should take (X 2 hours) 16,000 hours

but did take 15,000 hours

Variance in hours 1,000 (F)

X standard rate per hour x $30

30,000 (F)

Fixed cost expenditure variance

Budgeted fixed costs 210,000

Actual fixed costs

200,000

10,000

(F)

Budgeted profit statement

Amount in $

Amount in $

Sales (8,400 tons X $240) 2,016,000

Less: Rice seed (1.4 tons x $60 x 8,400 tons) 705,600

Labour (2 hours x $20 x 8,400 tons) 336,000

Variable overhead (2 hours x $30 x 8,400 tons)

504,000 1,545,600

Contribution 470,400

Less

fixed costs 210,000

Budgeted profit 260,400

Operating statement:

Budgeted contribution…………

470,400

Variances

Favourable

Adverse

Sales price

120,000

Sales volume

22,400

(142,400)

Material price 60,000

–

Material usage –

48,000

Labour rate –

18,960

Labour efficiency 20,000

–

Idle time 15,600

–

Variable overhead efficiency 30,000

–

Variable overhead expenditure

–

30,000

125,600

96,960

28,640

Actual contribution

356,640

Budgeted fixed cost:

210,000

Less:

Fixed cost expenditure variance

10,000

Actual fixed cost

200,000

Actual profit 156,640

Solution

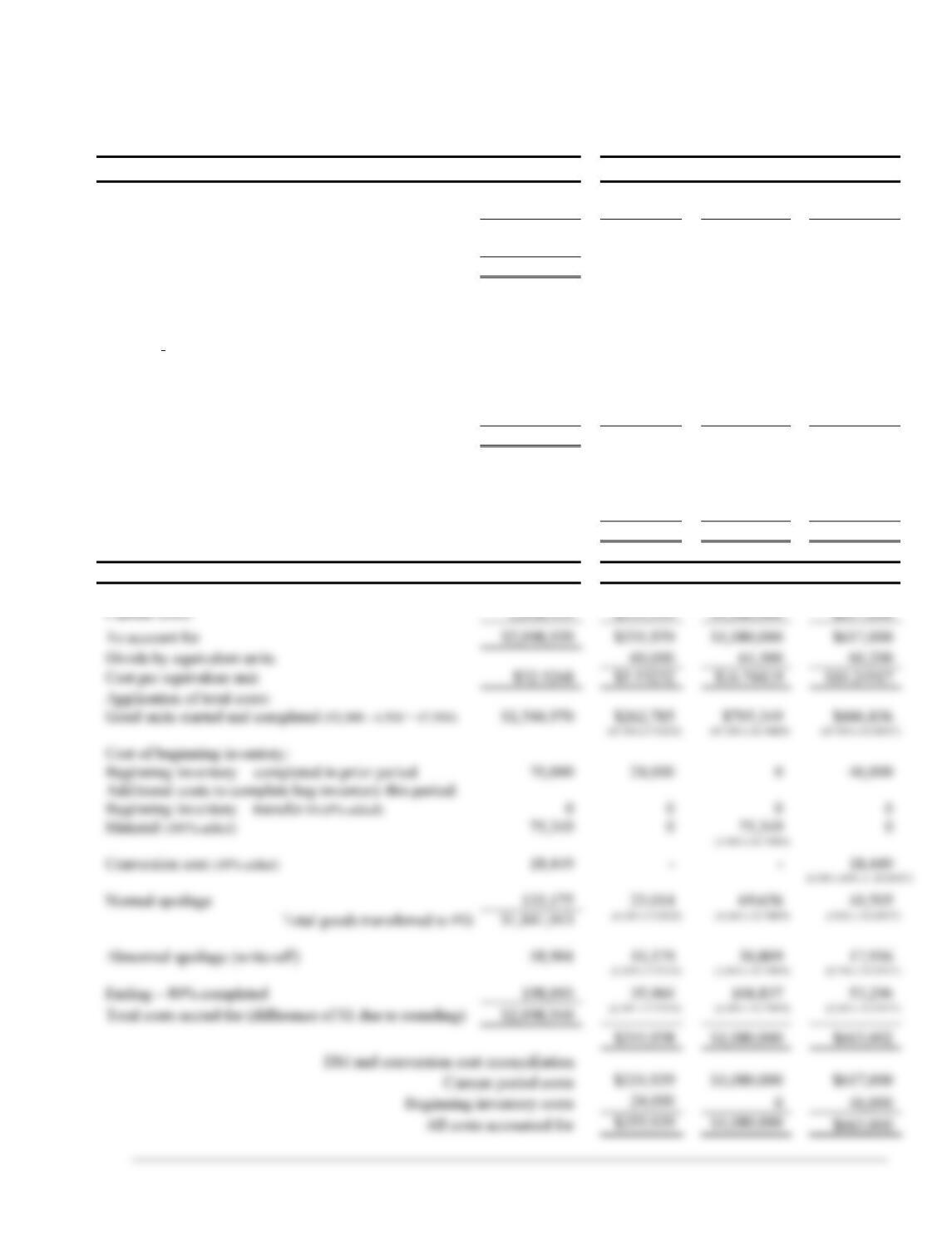

Solution: Process Costing – Rao Incorporated – 4-1

Department A

Physical Flow of Production Equivalent Units

Physical Units

DM Conversion

WIP, beginning 3,100

Units started 64,400

To account for 67,500

Units completed and transferred 60,000

60,000 60,000

WIP, ending 4,000 4,000 1,400

(4,000 × 35%)

Spoilage (67,500 – 64,000 = 3,500):

Normal spoilage (60,000 × 5% = 3,000) 3,000

3,000 2,550

(3,000 X 85%)

Abnormal spoilage (3,500 – 3,000 = 500) 500

500 425

(only 85% of conversion applied to spoilage) (500 X 85%)

Total units accounted for 67,500

Work done to date 67,500 64,375

Less: work done on beginning inventory in prior period:

DM (100% applied b/c DM added last period) (3,100)

Conversion (70% applied b/c 70% added last period) (2,170)

(3,100 × 70%)

Work done during current period 64,400 62,205

Financial Flow of Production Cost of Production

WIP, beginning (DM 21,700 + conv. 11,935) $ 33,635 – –

Current costs 314,975 $183,300 $131,675

To account for $348,610

Divide by equivalent units 64,400 62,205

Cost per equivalent unit $4.96306 $2.84627 $2.11679

Application of total costs:

Units started and completed (60,000 – 3,100) $282,398 $161,953 $120,445

Cost of beginning inventory: (56,900 x 2.84627) (56,900 x 2.11679)

Beg. Inventory – previously completed 33,635 21,700 11,935

Material (0% added b/c added last period) 0 0 –

Conversion cost (30% added this period) 1,969 – 1,969

(3,100 x 30% x 2.11679)

Cost of normal spoilage 13,937 8,539 5,398

(3,000 x 2.84627) (2,550 x 2.11679)

Total cost of goods transferred to Dept. B $331,939

Abnormal cost (write-off) $ 2,323 $ 1,423 $ 900

(500 x 2.84627) (425 x 2.11679)

Ending WIP 14,349 11,385 2,964

(4,000 x 2.84627) (1,400 x 2.11679)

Total costs accounted for $348,611

(difference of $1 due to rounding) $205,000 $143,611

DM and conversion cost reconciliation

Current costs $183,300 $131,675

Beginning inventory costs 21,700 11,935

All costs accounted for $205,000 $143,610

Continued to page-2

Department B

Physical Flow of Production Equivalent Units

Physical

Units

Transf. In DM Conversion

WIP, beginning (60% complete) 4,500

Units transferred in 60,000

To account for 64,500

Good units completed and transferred 52,000 52,000 52,000 52,000

WIP, ending (80% complete) DM added @ 75% and CC evenly 6,500 6,500 6,500 5,200

(6,500 × 80%)

Spoilage (64,500 – 58,500 = 6,000):

Normal spoilage (52,000 × 8%) 4,160 4,160 4,160 3,952

(4,160 x 95%)

Abnormal spoilage (6,000 – 4,160) 1,840 1,840 1,840 1,748

(1,840 x 95%)

Work done to date 64,500 64,500 64,500 62,900

Less: work done on beginning inv. in prior period:

No material added b/c added last perid, all trnsfrd in completed last period (4,500) 0 0

Conversion (60% complete in prior period) 0 0 (2,700)

(4,500 x 60%)

Work done during current period 60,000 64,500 60,200

Financial Flow of Production Cost of Production

WIP, beginning (con $46,000 + tran. $24,000) $ 0,000 — — —

Page-2